‘Sovereign money’: a bad idea

Commenter Intajake recently asked what I thought of some BoE research aiming at allowing the general public to hold accounts directly at the central bank. While in this particular case the BoE is considering the use of a crypto-currency/blockchain-type structure to facilitate the implementation of such a system, it’s definitely not a new idea. A number of activists have been advocating a nationalised system of current accounts for decades; more recently, Positive Money has been very vocal in defending ‘transaction accounts’ of ‘risk-free sovereign money’ held by the central bank (see their paper here; which, while not mentioning blockchain, sounds remarkably similar to the BoE “central bank digital currency” initiative).

Coincidentally, Thomas Jordan, Chairman of the Swiss National Bank, also commented on the matter in a speech in January. This follows a campaign for the introduction of sovereign money which led to the organisation of a referendum in the country (next June). Despite this campaign calling for more power to be granted to the SNB, it is interesting to see that Jordan, and the SNB in general, rejects the idea and mostly sees drawbacks to it.

Essentially, Thomas’ rejection of the initiative revolved around six main points:

- Political interference would have negative effects on the lending function of the SNB, which would now be centralised:

With the introduction of sovereign money, the SNB would be landed with a difficult role in lending. The initiative calls for the SNB to guarantee the supply of credit to the economy by financial services providers. In order to carry out this additional mandate, the SNB could provide banks with credit, probably against securitised loans. Depending on the circumstances, the SNB would have to accept credit risks onto its balance sheet and, in return, would have a more direct influence on lending. Such centralisation is not desirable. The smooth functioning of the economy would be hampered by political interference, false incentives and a lack of competition in banking.

- Sovereign money would restrict the supply of credit as the deposit creation function of banks disappears:

Second, sovereign money limits liquidity and maturity transformation as banks would no longer be able to create deposits through lending. Sovereign money thus restricts the supply of liquidity and credit to households and companies. The financing of investment in equipment and housing would likely become more expensive.

- Financial stability would not improve as investors and borrowers will keep making mistakes:

Investors and borrowers will always make misjudgements. A switch to sovereign money would thus not prevent harmful excesses in lending or in the valuation of stocks, bonds or real estate. Also, while the sovereign money initiative targets traditional commercial banks, let us not forget the role played by ‘shadow banks’ in the global financial crisis of 2008/2009.

- Sovereign money requires money supply management, which is in contradiction with SNB’s current inflation targeting mandate.

- Money supply management and inflation targeting both involve ability to reduce the money supply when necessary, usually through open-market operations. However, it is unclear how this process would work in a ‘debt-free’ sovereign money framework.

- The acceptance of the initiative would plunge the Swiss economy into extreme uncertainty.

I believe Jordan makes some very good points, and I’m particularly sympathetic to numbers 1, 2 and 5. The centralisation of the lending function in an institution subject to political power is what worries me most.

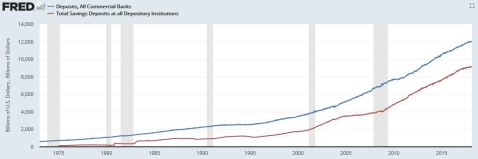

As saving deposits represent the largest type of deposits in the US (76%, if my reading of FRED is correct, see below) and possibly in Europe (I can’t find similar data), one could argue that sovereign money current accounts would only impact banks modestly. I believe there is more than meet the eye here.

First, savings have considerably grown as share of total deposits over the past two decades, possibly as a result of QE; in the couple of decades before the crisis they represented a more modest 40 to 60% of total deposits. Second, in the era of near-zero interest rates, a number of savers would probably think that the rewards of keeping their savings at ‘risky’ commercial banks is not worth the risk and instead transfer their savings to the central bank. After all, a large share of saving deposits is actually available on demand and the difference between a 0 and 0.25% remuneration rate is rather minimal. Moreover, saving deposits represent the largest share of non-wholesale funding for the banking system mostly due to the large number of small saving banks in the economy, many of which are specialised in non-productive mortgage lending, and which provide a number of more remunerative long-term time deposit products.

The larger banks, which have larger corporate lending books, rely more on demand deposits/current accounts for funding. Those banks are often the only institutions able to provide financing on a bilateral or syndicated basis to the largest of businesses, which are also the most politicised of companies. A very quick look at the latest financial statements of some of the world largest banks shows: HSBC Bank reported 86% of deposits available on demand, Deutsche Bank 61%, BNP Paribas 78%; JPMorgan reported 39% of total ‘transaction’ accounts and only 4% of time deposits and Wells Fargo 32% and 7% respectively; Mizuho reported 58% of demand deposits.

As those banks’ funding sources start dwindling, banks will have no choice but to turn towards their central bank for funding. As the central bank becomes the main funding provider of the banking system, it also starts having a say in regards to the allocation of credit in the economy, in particular when it involves politicised multinational corporations; lending competition becomes suppressed.

It is quite worrying that sovereign money activists have still not incorporated any element of Public Choice theory – or merely economic history – into their framework and don’t realise the dangers of having the state almost fully in control of the allocation of the money supply.

What the world needs is more competition in banking, not less. Instead of supporting the centralisation of deposit-taking and lending, those activists should instead support the new challenger banks and other fintech startups that are currently emerging. Many of those recently started taking deposits through new current account offerings and such ‘sovereign money’ initiatives would simply kill them off. Be careful what you wish for.

6 responses to “‘Sovereign money’: a bad idea”

Trackbacks / Pingbacks

- - 22 October, 2019

Leave a comment

Recent Comments

| pslebow on ‘Sovereign money’:… | |

| pslebow on A critique of Werner’s view on… | |

| Hugo Kramer on Welcome to Spontaneous Fi… | |

| Nathan on A critique of Werner’s view on… | |

| Nathan on More, more, more money endogen… |

Thanks for this analysis.

Sticking to the main premise of purely allowing the general public to have access to a Central Bank account.Cleary the main concern is a migration of funding deposits from the banks’ balance sheet(a Banks’ reserve account) to single central bank accounts for individuals.Which in turn would eviscerate the banks’ lending capacity and force an over reliance on the Central bank.

“As those banks’ funding sources start dwindling, banks will have no choice but to turn towards their central bank for funding. As the central bank becomes the main funding provider of the banking system,”

I would have thought that main issue with this would be cost,it would simply be too costly for banks to perpetually refinance at CB.

The main concern you raise about the concentration of decision making in Capital allocation and it possibly being politicized is undesirable.

I did think the idea of having members of the public have Central Bank accounts was attractive initially for two reasons’) It is a public good, so why not allow all member of the public have access to it.ii)We are poorly equipped to deal with a bank failure. Private banks don’t seem to operate in a competitive market. Any failing bank is effectively rescued by the state. Simply because banks hold the general publics’ deposits on their balance sheet. Management and Equity(shareholders) also seem to suffer no loss in remuneration. Why not reduce this vulnerability and inevitable moral hazard by allowing the general public to have access to the same institutional framework that private banks have i.e a reserve account at the BoE.

So that when banks do fail it would not be crisis requiring state intervention.And a bank would operate just like any other business and fail if it performs badly at capital allocation just like a firm in any other industry would fail if it underperforms at it’s specialization.

What is clearly desirable however is a financial system with lots of individual little nodes throughout an economy where credit allocation decision making is broadly decentralized and distributed.

I guess it is a trade off between imperfect systems.

Just published a follow up post.

Unsure why you are saying this though:

“I would have thought that main issue with this would be cost,it would simply be too costly for banks to perpetually refinance at CB.”

Costly or not, if there is no other choice… Financing rates would likely impact lending rates across the board to maintain some sort of margin.

Yes, you are quite right the increase funding costs would be passed on to the end borrower to protect the banks’ margin.

Just going over BoE sterling monetary framework(on the site).

Their are several different types of liquidity at different terms and for different collateral.I am not sure which one Banks would be using under the hypothetical situation of deposit funding disappearing(shifting to BoE accounts).Especially as the CB require collateral -whereas depositors don’t require any.

What do you think about the moral hazard issue and implicit subsidy,do you think it’s a legitimate(if ultimately insufficient) concern?

As I describe in my post, lending would be at risk of becoming a lot more politicised and loanable funds directed towards sectors that regulators (or politicians) believe should grow.

Jordan is completely and totally clueless. Re his first point “the SNB could provide banks with credit” as Positive Money clearly explains, central banks under Sovereign Money do not provide commercial banks with money to lend out: it’s up to commercial banks (much as now) to attract whatever money they can from depositors, bond-holders and shareholders with a view to lending it out. Though PM literature does admittedly suggest that in emergencies, the central bank might supply money to commercial banks to lend out. Personally I’m against that measure.

Re his second point, i.e. that credit would become more expensive, yes it probably would. But what of it? The important point is that the ability to print money (an ability that commercial banks have) is a subsidy of those banks (as explained by Ben Dyson and Joseph Huber). Subsidies do not make economic sense normally. I.e. the rise in interest rates stems from the removal of a subsidy. The net effect would be a rise in GDP.

Given Jordan’s obvious ignorance on this topic, I can’t be bothered with any more of his stuff.