Misunderstanding the net interest margin

Lately, there have been a lot of discussions in the media and in the academic sphere surrounding banks’ net interest margin in the low (or negative) interest rate environment. I have explained before how lowering interest rates below a certain threshold led to ‘margin compression’ (see here), which in turned depressed banks’ profitability and hence their internal capital generation, solidity and ability to lend.

The net interest margin (NIM thereafter) is roughly the difference between the average interest rate earned on assets and the average interest rate paid on funding, and is usually defined as

Net interest income / average earning assets, with NII being the difference between interest income (from loans and securities mostly) and interest expense (on deposits and other types of debt/funding instruments)

We now see conflicting articles and research pieces on the effects of low rates on banks’ NIM (see two of the most recent ones by the St Louis Fed here and other Fed researchers here). But, to my knowledge, most, if not all of those pieces make the same fundamental mistake: they do not look at risk-adjusted NIMs.

‘Risk adjustment’ is a critical concept but sadly often overlooked in the literature. I once defined the interest rate on a loan as the following:

LR = RFR + IP + CRP – C,

where LR is the loan rate, RFR is the applicable, same maturity, risk-free rate, IP the expected inflation premium, CRP the credit risk premium that applies to that particular customer and C the protection provided by the collateral (which can be zero).

As I explained elsewhere, margin compression occurs when the risk-free rate declines so much that interest rates banks pay on their funding reaches the zero lower bound while their interest income continues to decline (which led me to hypothesise that the zero-lower bound was actually a ‘2%-lower bound’ in the case of the banking/credit channel of monetary policy). This however assumes no fundamental change in the rest of the economy’s credit (or default) risk.

Indeed, in bad economic times, the CRP usually increases for most borrowers, partially offsetting the effects of the decline in the risk-free rate on new lending. Moreover, bankers can easily boost their NIM by lending relatively more to higher-risk customers or investing in higher-risk projects, even in good economic times. Consequently, it looks like the headline NIM isn’t suffering or declining that much. It can sometimes even improve, in particular when economic conditions are benign. For instance, emerging market banks often boast high NIMs, but also high default rates (and high ‘losses given default’). In such cases, margin compression seems not to be occurring. But this is just an accounting illusion.

See the example in the chart below, which represents the hypothetical evolution of the different components of a given unsecured loan rate throughout a long recession:

Once you adjust the NIM for the loan book’s underlying risk, the story is different. Banks’ interest income can rise but the risk of default on new lending, as well as that of their legacy loan portfolio, also rises. Because the CRP is often fixed at inception, legacy lending now underpays relative to its risk profile, potentially implying economic losses down the line.

Most studies don’t factor this phenomenon in. They look at unadjusted NIMs, which in many cases do not provide any useful information.

A very good and quite recent paper on banking mechanics by Claudio Borio and his team (The influence of monetary policy on bank profitability), which looks at the impact of the shape of the yield curve on margin compression and banks’ profitability, does understand that accounting plays a significant role:

The second form [of dynamic effects in the transmission of the level of interest rates to net interest income], which is more relevant, relates to accounting practices. Any interest margin on new loans also covers expected losses. But provisions in the period we examine follow the “incurred loss model”, so that, in contrast to interest rates, they are not forward-looking. As a result, extending new loans raises profitability temporarily, since losses normally materialise only a few years later at which point loans also become non-performing, eroding the interest margin. This also means that if lower market rates induce more lending, they will temporarily boost net interest margins. The strength of this effect will depend on background economic conditions. For instance, it is likely to be weak precisely when interest rates are unusually low and the demand for loans anaemic.

However, they stop short of providing a solution, or a correction, to this effect. To be fair, risk-adjusted NIMs are not directly observable and very difficult to estimate, given that disclosures about banks’ loan portfolio are very limited and that only some of their customers (i.e. large corporates) have bonds or credit default swaps traded on the secondary market. Therefore, some analysts use the following ex-post adjusted NIM ratio:

(Net interest income – loan impairment charges) / average earning assets

Default risk, expressed in the income statement by loan impairment charges (LICs – also called loan-loss provisions), is directly deducted from net interest income, making the NIM easier to compare across banks or countries. But even this version can be highly inaccurate, as LICs are backward-looking and depend on each bank’s accounting policies. In the short-run, some banks tend to over-provision, others to under-provision.

You’ve reached the end of this post perhaps wondering whether I had a solution to this problem. Unfortunately no, I don’t. But I believed that a clarification was in order. In finance, or economics in general, any decision involves risk-taking, and studies that do not take risk into account must be taken with a pinch of salt.

PS: The inflation premium is stripped out of the risk-free rate in this post, but in practice benchmark market rates such as Treasuries already factor in inflation expectations.

This post was re-published on Alt-M.

On ‘shadow money’

The shadow banking literature has vastly and rapidly expanded since the financial crisis, and has produced some interesting pieces, as well as some exaggerated claims, in my view. While I am not writing today to address those claims, I still wish to question a closely linked concept that has simultaneously sprung up in the literature and in particular in the post-Keynesian one: shadow money.

One of the most elaborated and comprehensive academic research papers on this particular topic is the recently published Gabor’s and Vestergaard’s Towards a theory of shadow money. It’s an interesting and recommended piece. But while I agree with some of their writings, I have to find myself in disagreement with a number of their points and examples* and in particular their central claim: that repurchase agreements (‘repos’ thereafter) are shadow money; that is, a type of monetary instrument used within the shadow banking system.

For some readers that might not know how a repo works, below is a concise definition provided by the IMF:

Repo agreements are contracts in which one party agrees to sell securities to another party and buy them back at a specified date and repurchase price.48 The transaction is effectively a collateralized loan with the difference between the repurchase and sale price representing interest. The borrower typically posts excess collateral (the “haircut”). Dealers use repos to borrow from MMFs and other cash lenders to finance their own securities holdings and to make loans to hedge funds and other clients seeking to leverage their investments. Lenders typically rehypothecate repo collateral, that is, they reuse it in other repo transactions with cash borrowers.

Given repos’ (and their asset counterpart: reverse repos) properties, my view is that repos aren’t shadow money but a shadow funding instrument. While it might not sound such a big issue, I believe the distinction is important from an analytical perspective as well as to avoid confusion. Let me elaborate.

Gabor and Vestergaard define shadow money as “repo liabilities, promises backed by tradable collateral.” According to them, shadow money has four key characteristics:

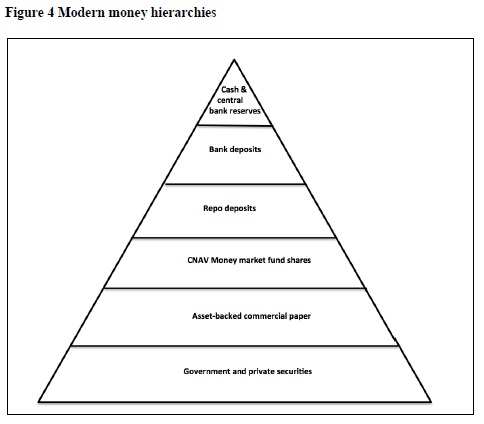

a) In modern money hierarchies, repo claims are nearest to settlement money, stronger in their ‘moneyness’ than ABCPs or MMF shares.

b) Banks issue shadow money. The incentives to issue repos are incentives to economize on bank deposits and bank reserves.

c) Shadow money, like bank money, relies on sovereign structures of authority and creditworthiness. The state offers a tradable claim that constitutes the base asset supporting the issuance of shadow claims.

d) Repos create (and destroy) liquidity at lower levels in the hierarchy of credit claims.

They offer this chart of ‘modern’ money hierarchy:

I have to object to repos being classified as ‘money’.

Money, as typically defined by economists, has three characteristics: it is a medium of exchange, a unit of account and a store of value. High-powered money (the ‘outside money’ of the financial system) currently fits this definition, as a final settlement medium.

The ‘moneyness’ concept, a term now popularised by JP Koning’s excellent blog, asserts that various types of assets have various degrees of money-like properties. In this quite old but classic post, JP argues that anything from beers and cattle to deposits benefits from some degree of moneyness. In another old post, Cullen Roche provided the following good ‘money spectrum’ chart (although I’d disagree with his outside money/deposit ranking):

Therefore, most goods and assets have some monetary properties: some can be used as media of exchange or store of value. All represent a claim of some sort on money proper. As a general (but inaccurate) rule, the more their price in terms of outside money fluctuate, and hence their conversion risk raises, the further away they are on the moneyness scale. But conversion (almost) on demand also implies that, in order to have some money characteristics, a good or asset needs to be tradable.

Now let’s get back to repos as shadow money.

Repos are a liability issued by the debtor in exchange for high-powered money, of which reverse repos are the asset counterpart held by the creditor (and hence the claim on the high-powered money originally transferred, plus interest). The debtor also transfers an extra asset (i.e. the collateral) to the creditor for security purposes at a pre-agreed haircut depending on its credit quality and market risk sensitivity.

We get here to the main point of this post: repos have little money-like property due to their non-tradability and lack of on-demand convertibility.

Indeed, a repo liability is of course non-tradable, in the same way that any debt that one owes cannot be traded for another type of liability. It can only be refinanced and/or extinguished. A reverse repo (or repo claim) however, could potentially have tradable properties, allowing a creditor to exchange his claim almost instantaneously on the market. Problem is: this does not happen. Unlike bonds or other assets, and due to the very specific features of such private agreements, there is no secondary market for repo claims. Once a repo has been agreed upon, the contract is fixed between the two parties until maturity (or default). Consequently, repo claims can effectively be assumed to have no liquidity.

Seen this way, it is hard to classify repos as ‘money’, and they certainly do not deserve their third place in the moneyness hierarchy above. So what are repos? As I previously said, they are a funding instrument. Given that the shadow banking system makes use of repos on a large scale, we can potentially call them a ‘short-term secured shadow funding instrument’. And please note that repo issuance isn’t limited to banks and broker-dealers; other institutions also use them.

You’ll be tempted to reply: “what about deposits? They have no secondary market and are not tradable either.” This isn’t strictly accurate. While they are both promises to pay a certain amount of money proper at a certain date, there is a very specific difference between deposit liabilities (‘on demand’ ones especially) and repo liabilities. Banks themselves are deposits’ secondary market: deposits can be ‘traded’ within the bank’s own balance sheet and swapped for cash on demand. And when dealing with a counterparty that does not hold an account with the same bank, banks take over the responsibility of transferring the underlying funds (i.e. high-powered money).

If repos aren’t ‘money’, what else could be considered ‘shadow money’? Well, assets provided as collateral do have liquidity, tradability, and therefore some ‘moneyness’. Those assets can sometimes be used in further transactions. This is why I am wondering whether or not there isn’t some confusion with ‘shadow money’ proponents’ terminology. While their writings clearly emphasise the ‘shadow money’ nature of repos themselves (and Poszar seems to be using the same definition here), many other academic authors have instead referred to the most commonly-used types of repo collateral (high quality and highly liquid sovereign and corporate bonds) as ‘shadow money’ (which indeed makes more sense to me, although I do not fully adhere to this concept either).

There are plenty of things worth discussing regarding this theory of shadow money and the use of repos in general, but the money-like properties of repurchase agreements isn’t one of them. Let’s focus on their funding properties instead.

*I also believe that their shadow money expansion theory is subject to the same critique as other endogenous outside money theories, such as MMT’s.

PS: the fact that repos are backed by marketable collateral does not confer any specific monetary property to repo claims. Marketable collateral is used in many other types of lending transactions, in particular in private banking-type lending. Also, repos and any other collateralised lending are expected to be repaid at par, independently of the valuation fluctuations of their underlying collateral.

PPS: Baker and Murphy build on Gabor’s and Vestergaard’s piece and just published a blog post that argues for a new ‘investment state’, in a typical post-Keynesian interventionist fashion.

This post was re-published on Alt-M.

What China can teach us about the future of banking

A few weeks ago, Citi published a quite fascinating 100-page report on financial innovations, from blockchain to P2P lending, in various regions of the world. It’s a highly recommended and very comprehensive reading that I won’t be able to summarise in a short blog post.

From this report, it is clear that China’s financial system has adopted innovations at a much faster pace than the Western world. And if there is a defining characteristic of the Chinese system, it is its very erratic and repressive regulatory framework, which made me once call China a ‘spontaneous Frankenstein banking system’:

Financial regulation in China is quite a mess. China seems to be the world testing ground for some of the most ridiculous banking rules. With all their related unexpected consequences.

In an earlier post, I also highlighted that

China is an interesting case. Underneath its very tight government-controlled financial repression hide numerous financial experiments aimed at bypassing those very controls. The Chinese shadow banking system is now a well-known financial Frankenstein, with multiple asset management companies, wealth management products and other off-balance sheet entities providing around half the country’s credit volume. The more the government tries to regulate the system, the more financial innovation finds new workarounds and become increasingly more opaque.

We already knew that the Chinese financial system was completely distorted from years of regulatory repression and crony capitalism, as a whole new report on finance in China by The Economist demonstrates (see the editorial here, and the report starting here). Echoing my worries, The Economist calls for China to ‘free up’ its ‘financial jungle’. Citi’s and The Economist’s reports now allow us to quantify the effects of those distortions. Indeed, China leads the world in fintech and digital disruption in general; it has some of the largest fintech firms and, as Citi said, it is now ‘past the tipping point’.

While its very large e-commerce has been a strong driver of the rise of alternative payment providers in the country, Citi points at a number of other factors that have facilitated the rise of those third-party payment companies, among which an under-developed banking system viewed by the public as quite unreliable (unsurprising given how tightly controlled banking is in China, which has stifled customer-oriented innovation), and ‘relaxed regulation’. Citi points out that Chinese regulators have now proposed new tightened rules for the payment sector, so brace yourself for further innovations in this space. For now, Alipay handles more than three times the volume of transaction that Paypal does, and payment firms have more retail customers than banks have and are now expanding into offline payments.

China also has the largest P2P lending market in the world, four times bigger than that of the US. Citi analysts forecast that P2P loans are going to represent a sizeable 9% of total retail lending in China by 2018.

The driver of this growth is, typically, mostly regulatory constraints on traditional banking that triggered regulatory arbitrage:

P2P lending platforms target segments that are unserved or under-served by existing banking system such as consumer credit and small and micro business lending. Traditional banks are not particularly good at serving this customer segments due to tougher Know Your Client/Anti-Money Laundering (KYC/AML) requirements as well as tightened lending standard post global financial crisis.

And one would add that capital requirements on certain category of customers (such as SMEs) play a large role here too, as I keep pointing out on this blog (see at the end of this post). The same reasons are behind the development of such lending platforms in Europe and the US. And indeed, as Citi writes:

According to China MSME Finance Report 2014 by Mintai Institute of Finance and Banking, almost 80% of SMEs were not served by the banks. The explosive growth in the P2P lending has met the needs of SMEs which cannot get formal financing.

And:

Chinese banks are under tight regulations such as reserve requirement, loan-to-deposit ratios (LDR), KYC, AML, and so on. There was however little regulations for the P2P lending sector. There is also no capital requirement.

Furthermore, Chinese monetary repression is also a driver, as P2P lending allows savers to earn higher returns. Here again, Chinese regulators are looking at ways to scrutinise and more tightly control the sector.

What are the effects of all this? As The Economist points out, China’s shadow banking sector is the largest and possibly the fastest growing in the world:

There is a fundamental difference between the Chinese banking system and the Western one however. Chinese banks, despite being extremely large, have historically had no ability to grow outside of the Communist party’s grip and no ability to adapt to consumer demand as a result. Citi points out that there were only 8.1 bank branches per 100,000 adults in China, vs. around 30 in the Eurozone and the US. With little banking presence, fintech firms have found it easy to rapidly grow.

Yet, developed economies do have a lesson to learn from the Chinese experience. The more regulatory constraints are put in place on banks, the more innovative ways around them will spontaneously emerge and the more complex and opaque (‘Frankenstein-like’) the financial system will become. And sadly, it looks like Europe and the US have decided to follow China’s footsteps.

PS: The following chart is revealing. Most of the financial products that are at most risk of disruption (SME and personal loans, deposits…) are also those that are the most affected by regulatory requirements and low interest rates.

PPS: A very good introduction to the Chinese financial mess is Walter’s and Howie’s Red Capitalism. However the book was ‘only’ updated in 2012, and plenty has happened since then, in particular in the fintech portion of China’s shadow banking sector.

PPPS: Apologies for not posting more regularly at the moment, but I ended up being busier than I thought I would be.

This post was re-published on Alt-M.

Recent Comments