A couple of comments on ‘House of Debt’

I just read House of Debt, the latest book by Mian and Sufi, which got a relatively wide coverage in the media, so I thought I should write a quick post about it.

Overall, it’s a good book, accessible for those who do not have a background in economics or finance. What I particularly liked about the book is its emphasis on leverage. The boom in household and business leverage over the past two decades inevitably fuelled an unsustainable boom in aggregate spending. Bringing indebtedness back to more ‘normal’ values also inevitably reduces spending power*. Yet, too many economists seem to take this pre-crisis trend as normal.

They are also right to advocate letting banks fail, as well as question the non-monetary banking intermediation channel (as proposed by Bernanke in his famous article Non-Monetary Effects of the Financial Crisis in the Propagation of the Great Depression) and the effectiveness of monetary policy following a debt boom.

However, the authors never explain the underlying causes of the leverage boom and the crisis. It seems to be assumed that financial innovations (i.e. securitization mostly) appear all of a sudden, enabling an unsustainable boom to take place. What role did monetary policy play during the period? Or banking regulation? Those questions remain unanswered. Yet, as I’ve been explaining for now close to a year, the combination of those two factors was critical in triggering the boom in financial innovation, leverage, and malinvestments. I wish Mian and Sufi had provided their thoughts on that topic in their book.

They provide evidence that house prices increased the most in counties with inelastic housing supply. Still, they also strongly increased in those with elastic housing supply… They focus on the Asian ‘savings glut’, which would have flowed into the US. Perhaps, but it doesn’t mean that the Fed rate wasn’t too low, and many countries all around the world also experienced booming housing markets. Moreover, mortgage delinquencies started when the Fed increased its base rate… Despite being a US-centric book, there is also no discussion of the particular populist political framework at play in designing both the peculiar US banking system and the crisis, as described by Calomiris and Haber.

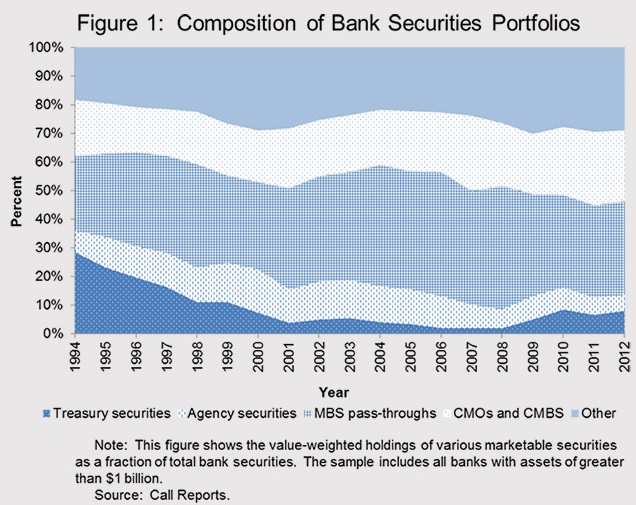

As a result, they seem to identify the rise in securitization as a fraud. I believe this is not the case. Banks started holding securitized assets on their balance sheet because of their beneficial capital treatment. There is little sign that they tried to originate bad assets to defraud naïve investors. Indeed, take a look at the chart below (from a recent post): banks also invested in such products and self-retained tranches of those they had originated throughout the boom period, and continue to do so. This points to ignorance of the risks. Not fraud.

I encourage you to read the book for its very good data gathering. Despite some of its (relatively minor) flaws, the book does much to debunk some myths through the appropriate use of empirical evidence.

* This doesn’t mean that there wasn’t also an excess demand for money at that time. Just that a decreased money supply through debt deflation exacerbated the problem.

New research at last asks the right questions on RWAs

A new piece of research by the US Treasury Department’s Office of Financial Research has started questioning the use and definitions of Basel regulations’ risk-weighted assets (RWAs), which they view as a “rather curious scheme”… RWAs are critical in the Basel framework as they have been underlying regulatory capital ratios since the introduction of Basel 1 back in 1988. Readers of this blog know that I blame RWAs for being a major factor in the economic distortions and resources misallocation that directly led to the crisis (reduction in business lending, jump in real estate lending, securitizations and sovereign lending…) (see also here… and everywhere on this blog).

The authors’ thesis is similar to mine (emphasis added):

This is a rather curious scheme, if we consider that risk is not ordinarily considered additive. One might construe the additive formulation as conservative, but capital requirements affect which assets a bank chooses to hold, so the choice of risk weights affects a bank’s asset mix and not just the overall risk of its portfolio. A risk-weighting scheme may be conservative in its effect on overall risk and yet introduce unintended distortions in the levels of different kinds of lending activities. […]

For our investigation, we take a risk-weighting scheme to have two primary interlinked objectives: to limit the overall risk in a bank portfolio and to do so without an unintended distortion of the mix of assets held by the bank. The first of these objectives is common to all capital regulation, but the second is specific to a risk-weighting scheme because risk weights implicitly assign prices (in terms of additional capital) to asset categories and thus inevitably create incentives for banks to choose some assets over others.

They add that the literature supporting the use (and validating the level) of risk-weights is rather thin, unlike the literature on the nature of banks’ capital (the so-called ‘Tiers’), which has been the focus of most new regulatory measures while RWAs have remained pretty much unchanged.

They propose to tie risk-weights to asset profitability and develop a mathematical framework to help regulators to do so (as they are unlikely to obtain enough information to accurately set their level). This is interesting, but I’d rather get rid of risk-weights altogether: market actors can already assess banks’ profitability vs. asset mix risk and invest accordingly. There is also another issue with such a scheme: assets that do not appear profitable (and hence risky) at first do not necessarily mean they are not, as secured real estate markets demonstrated over the last decade. Moreover, ‘riskier’ business lending rates are currently lower than ‘safer’ mortgage lending ones. Profitability of riskier assets is sometimes subdued, either for relationship purposes (in order to generate revenues elsewhere), and/or if lending terms/collateral nature/haircuts are deemed reasonable. I have to admit that I did not have the time to read their mathematical description in depth and I might be missing something.

Meanwhile, the BoE’s Funding for Lending Scheme still struggles to revive lending to UK businesses. As policy-makers are unlikely to read this blog, perhaps this new research will help?

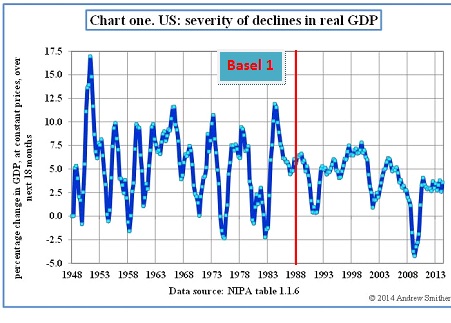

PS: I extracted the following chart from an FT blog post published yesterday and added Basel 1 to it (which introduced risk-weights and led to a decline in business lending). US real GDP growth seems to start declining exactly when business lending falls below trend (compare with second chart):

Some new (more or less useful) research

A few noticeable papers have been published recently. They are not particularly ground-breaking but some offer interesting insights and datasets. Here are summaries:

– The Effects of Unconventional Monetary Policies on Bank Soundness, an IMF working paper by Lambert and Ueda, is an interesting piece of research though its results are no surprise:

Unconventional monetary policy is often assumed to benefit banks. However, we find little supporting evidence. Rather, we find some evidence for heightened medium-term risks. First, in an event study using a novel instrument for monetary policy surprises, we do not detect clear effects of monetary easing on bank stock valuation but find a deterioration of medium-term bank credit risk in the United States, the euro area, and the United Kingdom. Second, in panel regressions using U.S. banks’ balance sheet information, we show that bank profitability and risk taking are ambiguously affected, while balance sheet repair is delayed. (my emphasis)

I’m not a great fan of the first part of their study, in which they run a regression between monetary policy events and banks’ share prices, credit spreads and CDS spreads: they do not take into account government support, which considerably affects the perceived creditworthiness of a number of banks. Their second part (what I highlighted in the abstract above) is more interesting though not that surprising. I have already described many times how profitability, and hence internal capital generation, were subdued in a close to zero interest rate environment.

– Identifying Excessive Credit Growth and Leverage, an ECB staff working paper by Alessi and Detken, is also interesting given the methodology but… seems to be stating the obvious. According to the paper, some of the best indicators of ‘excess leverage’ in the economy are…bank credit/GDP or the debt service ratio… (see table below)

– A little older, Banks as Patient Debt Investors, is an introductory speech to forthcoming research by Jeremy Stein, member of the Board of Governors of the Fed. This is perhaps the most interesting and theoretical of the papers I have read over the past few days and I am looking forward to dissecting the final published version. This is Stein:

I have argued that there is a synergy between banks’ stable funding model and their investing in assets that have modest fundamental risk but whose prices can fall significantly below fundamental values in a bad state of the world. This synergy helps explain both why deposit-taking banks might have a comparative advantage at making information-intensive loans and, at the same time, why they tend to hold the specific types of securities that they do.

He makes some interesting remarks, though I have the impression that he misstates the actual accounting treatment of ‘Available for Sales’ assets, which he uses to justify his model. This might lead him to the wrong conclusions. A fall in the value of AFS assets will indeed not affect net income but will negatively affect equity/capitalisation through the bank’s comprehensive income statement, possibly undermining some of his conclusions or some of his reasoning. However, it is too early to judge, and I’ll read the whole finished paper once it is published.

Stein also presented an interesting chart to back his research. Most of US banks’ securities portfolios are comprised of assets that benefit from low risk-weights under Basel. I would have liked to see this chart starting from the 1970s (i.e. pre-Basel era).

PS: I wish to thank Ben Southwood, from the Adam Smith Institute, for providing me with some of those links

Free banking: the track record

Sam Bowman, from the Adam Smith Institute, just published a very good paper arguing that, in case it decides to declare its independence, Scotland should ‘sterlingise’ and recreate a free banking system similar to the one it used to have in the 18th and 19th century. This report has been featured in many newspapers today (BBC, City AM, The Scotsman, The Guardian, The Wall Street Journal, The Huffington Post, The Telegraph…). Whether or not the current socialist-minded Scottish government is likely to implement such radical liberalisation of its banking system is another issue…

In this report, Sam Bowman also reproduces two very important tables (originally from George Selgin’s article Are banking crises free markets phenomena) highlighting the track record of free (or mostly free) and regulated banking from the late 18th till the early 20th century. Guess which type of banking system was more stable…

‘Unfree’/regulated banking:

Free/lightly regulated banking:

Secular stagnation: factoring in banking regulation

David Beckworth wrote a good post on the secular stagnation hypothesis, highlighting the problem with the interpretation of the natural rate by secular stagnation theorists. This is Beckworth:

First, real interest rates adjusted for the risk premium have not been in a secular decline. Everyone from Larry Summers to Paul Krugman to Olivier Blanchard ignore this point in the book. They all claim that real interest rates have been trending down for decades. The editors of the book, Coen Teulings and Richard Baldwin, even claim that this development is the ‘prima facie’ evidence for secular stagnation. What they are doing wrong is only subtracting expected inflation from the observed nominal interest rate. They also need to subtract the risk premium to get the natural interest rate, the interest rate at the heart of the story. For it is the natural interest rate that is affected by expected growth of technology and the labor force.

He is right. But I believe there is more to the story.

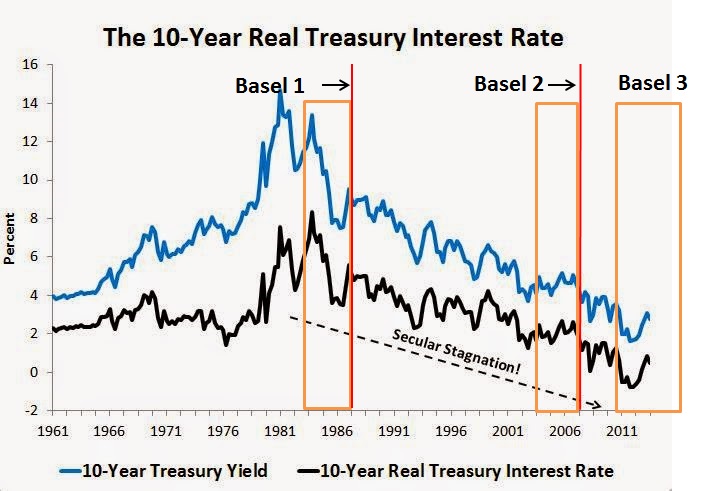

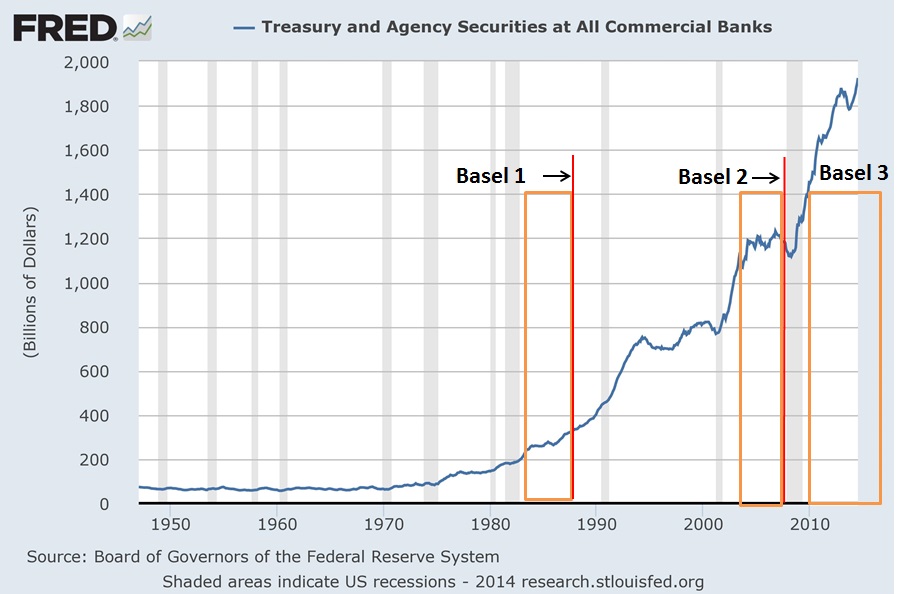

This is Beckworth’s chart highlighting the apparent secular decline in interest rates as believed by secular stagnation adherents. I added to it Basel 1, Basel 2 and Basel 3 introductions (red lines) and discussions (orange area) (unlike in Europe, only a few US banks had implemented Basel 2 when the crisis started):

What is striking is the fact that Treasury yields started declining exactly when Basel 1 was being discussed and implemented. There is a clear reason for this: Basel introduced risk-weighted assets, and government securities were awarded a 0% risk-weight, meaning banks could purchase them and hold no capital against them. As I have described before, banks were then incentivised to pile in such assets to maximise RoE, as a quick risk-adjusted return on capital calculation demonstrates. Basel 1 also introduced risk-weights for other asset classes such as business and mortgage lending. Structural changes in lending* and government securities markets occurred directly post-Basel. I believe this is no coincidence.

Take a look at the following chart. Until the 1980s, the volume of US government securities on US banks’ balance sheet was pretty much constant. Everything changed from the 1980s onward:

As a share of banks’ total assets (see chart below), US government securities literally spiked after Basel 1 was introduced, only to decline (as a share of total assets) as banks started piling in other assets that benefited from generous capital treatments such as securitisations and insured mortgages (though this doesn’t mean demand faded as banks balance sheets grew quickly over the period, just that demand for other assets was even stronger). Post-crisis, Basel 3 renewed the demand for US sovereign debt as it 1. modified the capital treatment of some previously lowly-weighted assets and 2. introduced minimum liquidity requirements (LCR) as well as margins and collateral requirements that require the use of high-quality liquid assets such as Treasuries.

We identify the same pattern as a share of total securities on US banks’ balance sheet**:

The demand for Treasuries also boomed throughout the financial sector due to those margin/collateral/liquidity requirements that apply (mostly post-Basel 3), not only to commercial banks, but also to broker dealers and investment managers:

All those regulations evidently artificially increase demand for US government-linked securities, pushing their yields down.

But I guess you’re going to tell me that Beckworth’s adjusted risk-free Treasury yield was actually stable over the whole period (chart below). Actually, unlike what Beckworth claims, it does look like there is a slight decline since the end of the 1980s. Moreover, ups and downs almost exactly coincide with banks decreasing/increasing their relative holdings of Treasuries (see above, third chart). Finally, there is also another option: that the natural (risk-free) rate of interest’s trajectory was in fact upward, which would be hidden by financial regulations’ artificially-created demand…

However, this analysis is incomplete: it does not account for foreign banks’ demand for Treasuries, which is also a widely-held asset as part of banks’ liquidity buffers (and in particular when their own sovereign fails…). I unfortunately don’t have access to such data.

In the end, the use of Treasury yield (even adjusted) as an estimate of the natural rate of interest is unreliable given the numerous microeconomic variables that distort its level.

* See this chart from one of my previous posts:

** Post-WW2’s very high figures (close to 100%) reflect the low level of corporate securities issued following the Great Depression and WW2, the high issuance volume of US sovereign debt to fund the war, as well as restrictions on banks’ securities holding to facilitate such wartime issuances.

Macroprudential policy tools: a primer (guest post by Justin Merrill)

In case you hadn’t heard, there’s a new fad in central banking called “macroprudential regulation.” During the Great Moderation there was a belief that low and stable inflation would be sufficient to stabilize financial markets and the economy. When the Great Moderation turned into the Great Recession, this paradigm shifted, but I’m afraid that the wrong conclusions are being drawn. In a series of posts, I shall explain what macroprudential policies are, who some popular people making the arguments for them are and what the risks of the policies are.

Most places I’ve read about macroprudential policies are vague in their description and only list a couple of the tools that central bankers/regulators can use. The policies are intended to prevent systemic risk by preventing/diffusing concentrations of risk. I hope to provide here a nearly comprehensive list of the tools. Conceptually, the tools can be categorized into four categories and theoretically all of the following risks may contribute to asset bubbles or financial instability:

- Leverage/Market Risk

- Reducing leverage is intended to reduce the risk of insolvency in case of a fall in asset prices.

- Liquidity

- Increasing liquidity reduces the risk that payments won’t be made to creditors and may curb fire-sales from credit crunches.

- Credit Quality

- Controlling credit quality intends to prevent future non-performing loans from debtors that would be most susceptible to economic shocks.

- FX/Capital Controls

- FX/Capital controls attempt to prevent hot money from pushing up asset prices and prevents firms from being over-exposed to FX risk from unhedged positions.

Also note that time-varying/dynamic/counter-cyclical rules are a popular concept and can be applied to possibly all of the following tools.

Leverage/Market Risk

- Debt/equity ratios: Also commonly referred to as “capital” in the banking sector. Requiring more funding from equity reduces the risk of insolvency.

- Margin requirements: Determines how much investment can be made with borrowed money. There is a high correlation between margin debt and asset prices.

- Provisioning: Banks account for loss provisions in their financial statements. If they expect losses or are required to hold higher provisions, they will hold a higher equity buffer to offset the losses. If actual losses are less than expected, the bank records a profit.

- Restrictions on profit distribution: If debt/equity ratios are above what regulators want, they may require the firm to retain earnings instead of pay dividends.

- Collateral, hypothecation and haircuts: Regulators may determine which assets may be used as collateral, how much collateral is required for lending, and how much of a haircut is applied to the asset in the repo market. If market prices fall below the repo price the seller may not buy it back. Haircuts (over-collateralization) and margin calls are used to mitigate this risk. Repos and reverse-repos are being increasingly used by central banks as a new tool for an exit strategy from QE and since QE has drained the private markets of credit-worthy assets. Repos also can have broader participation than open market operations (OMOs), the Fed Funds market or deposits at the central banks. OMOs are restricted to primary dealers and deposits at the Fed are restricted to members of the Federal Reserve System and membership is restricted to qualifying commercial banks.

- Too Big To Fail (TBTF) taxes: TBTF taxes have been proposed to reduce the concentration of risk or political power of a single firm as a sort of Pigouvian tax to offset externalities. The taxes could be an assessment on firms whose assets are above an arbitrary cutoff (such as $1 trillion), on firms whose assets exceed a percentage of GDP, or on firms that own above a certain percent of market share.

Liquidity

- Reserve requirements: Reserve requirements are a unique item on this list since they are considered a traditional monetary policy tool. Even though use of changing reserve requirements fell out of favor as a traditional tool, it has gained renewed interest in conjunction with QE, especially in countries with pegged currencies, such as China. This allows the central bank to increase the monetary base without creating price or asset inflation.

- Limits on maturity mismatch: Financial intermediaries such as banks generally engage in maturity transformation by borrowing short and lending long. This can create a funding risk if they are unable to roll over their debts at a reasonable rate. Also, the long dated assets they hold will have more convexity, which means they will be more sensitive to changes in interest rates.

- Liquidity Coverage Ratios (LCR): Basel regulations require financial institutions to hold a level of highly liquid assets to cover their net outflows over a period of time.

Credit Quality

- Caps on the loan-to-value (LTV) ratio: Requiring a larger down payment reduces the risk that the borrower will walk away in case of a decline in property value. It also helps the bank profitably resell the property in case of foreclosure.

- Caps on the debt-to-income (DTI) ratio: DTIs help gauge the borrower’s ability to repay the loan.

- Lending Policies- “No second homes” and risk weighting: Lending policies can target specific sectors of the economy or have specific goals. These can include requiring a larger down payment on second homes, increased risk weightings for real estate, discouraging foreign buyers, and discouraging house flipping by having higher taxes on short term sales.

FX/Capital Controls

- Caps on foreign currency lending: Foreign currency lending that is unhedged exposes the borrower to FX risk.

- Limits on net open currency positions/currency mismatch: Borrowing and investing in different currencies exposes FX risk.

- Capital controls: Capital controls are used to prevent hot money flows in and out of a country that could fuel a boom and bust. Controls are also used for financial repression and increasing domestic investment. Additionally, capital controls are often used in conjunction with a fixed exchange rate, like in China. This is due to the Trilemma. If China wants to peg its currency to the USD and control its domestic interest rate for monetary policy, it must have capital controls. Otherwise, the higher interest rate in China would attract hot money deposits from abroad and there would be an asset boom. The alternatives to a pegged currency with capital controls are a floating exchange rate with free capital or a currency board with free capital.

Links

http://www.imf.org/external/pubs/ft/fandd/basics/macropru.htm

Central banks: an expanding regulatory toolkit

Following my latest post on central banks as the new central planners, a very recent New York Fed Staff Report by Adrian, Covitz and Liang demonstrates the extent of possible central banks’/regulators’ involvement in financial markets, and therefore in what ways they can control, or attempt to control, the allocation of resources within the financial system. Here is a summary of various classes of tools (most of them discretionary) that monetary and financial authorities can play with:

– Monetary policy: the authors classify monetary policy as a “broader tool” that “would affect the rates for all financial institutions”. Indeed, central banks not only set the short-term refinancing rates and reserve requirements and run open market operations, but now also have in place interest rates paid on excess reserves, fixed-rate full allotment reverse repos, as well as various temporary long-term lending facilities such as the BoE’s Funding for Lending Scheme or the ECB’s LTRO and TLTRO, and temporary liquidity facilities such as the ABCP MMF liquidity facility, and can decide what collateral to accept and what securities to purchase, way beyond the traditional Treasury-based OMO.

– Asset markets: central banks can regulate what they view as ‘imbalances’ in the valuation of some asset markets by tightening underwriting standards as well as “through regulated banks and broker-dealers by tightening standards on implicit leverage through securitization or other risk transformations, or by limiting the debt they provide to investors in either unsecured or secured funding markets, if the asset prices are being fuelled by leverage.” In the case of real estate markets and household burdens, central bankers can impose LTV restrictions* and other similar macro-prudential policies.

– Banking policies: central banks have under their control all traditional micro-prudential regulatory tools. In addition, Basel 3 provide them with some flexibility in setting macro-prudential regulatory tools that apply specifically to the banking system, such as counter-cyclical capital requirements (capital conservation buffer, equity systemic surcharge…). Other ad-hoc tools include: sectoral capital requirements (higher/lower capital charges/RWAs for specific asset classes), dynamic provisioning, stress tests…

– Shadow banking policies: harder to regulate, central banks could “address pro-cyclical incentives in secured funding markets, such as repo and sec lending, […] propose minimum standards for haircut practices, to limit the extent to which haircuts would be reduced in benign markets. Other elements of this proposal include consideration of the use of central clearing for sec lending and repo markets, limiting liquidity risks associated with cash collateral reinvestment, addressing risks associated with re-hypothecation of client assets, strengthening collateral valuation and management practices, and improving report, disclosures, and transparency.” Other direct tools include “the explicit regulation of margins and haircuts for macroprudential purposes.”

– Nonfinancial sector: “Tools to address emerging imbalances in asset valuations likely would also address building vulnerabilities in the nonfinancial sector. For example, increasing* [sic] LTVs or DTIs on mortgages, which could reduce a leverage-induced rise in prices, could also limit an increase in exposures of households and businesses to a collapse in prices, thereby bolstering their resilience.”

Given the increased scope of central banks’ operations, it is clear that market prices can be manipulated and distorted in all sort of ways. To be fair however, not all those powers are currently concentrated in the central bankers’ hands. In many countries, there are still a few different institutions that perform those tasks. Nevertheless, the trend is clear: most of those powers are increasingly taken over by and aggregated at central banks.

While this new paper advocates the use of such tools, it admits that their effectiveness and effects on the financial system and the broader economy remains untested and uncertain:

New government backstops to address the risks arising from shadow banking, of course, can be costly. First, an expansion along these lines would require a new regulatory structure to prevent moral hazard, which can be expensive and difficult to implement effectively. Second, an expansion of regulations does not reduce the incentives for regulatory arbitrage, but just pushes it beyond the beyond the existing perimeter. Third, there is a limited understanding of the impact that such a fundamental change would have on the efficiency and dynamism of the financial system.

In a subsequent guest post, Justin Merrill will investigate macro-prudential policy tools more in depth.

* The paper mistakenly describes those potential measures as “increasing” LTV ratios to mitigate house price and household indebtedness increases. I believe this is a typo, even though the same claim reappears several times throughout the paper (if not a typo then the authors have no clue how LTVs work…).

Hummel vs. Haldane: the central bank as central planner

Recent speeches and articles from most central bankers are increasingly leaving a bad aftertaste. Take this latest article by Andrew Haldane, Executive Director at the BoE, published in Central Banking. Haldane describes (not entirely accurately…) the history and evolution of central banking since the 19th century and discusses two possible paths for the next 25 years.

His first scenario is that central banks and regulation will step backward and get back to their former, ‘business as usual’, stance, focusing on targeting inflation and leaving most of the capital allocation work to financial markets. He views this scenario as unlikely. He believes that the central banks will more tightly regulate and intervene in all types of asset markets (my emphasis):

In this world, it would be very difficult for monetary, regulatory and operational policy to beat an orderly retreat. It is likely that regulatory policy would need to be in a constant state of alert for risks emerging in the financial shadows, which could trip up regulators and the financial system. In other words, regulatory fine-tuning could become the rule, not the exception.

In this world, macro-prudential policy to lean against the financial cycle could become more, not less, important over time. With more risk residing on non-bank balance sheets that are marked-to-market, it is possible that cycles in financial assets would be amplified, not dampened, relative to the old world. Their transmission to the wider economy may also be more potent and frequent. The demands on macro-prudential policy, to stabilise these financial fluctuations and hence the macro-economy, could thereby grow.

In this world, central banks’ operational policies would be likely to remain expansive. Non-bank counterparties would grow in importance, not shrink. So too, potentially, would more exotic forms of collateral taken in central banks’ operations. Market-making, in a wider class of financial instruments, could become a more standard part of the central bank toolkit, to mitigate the effects of temporary market illiquidity droughts in the non-bank sector.

In this world, central banks’ words and actions would be unlikely to diminish in importance. Their role in shaping the fortunes of financial markets and financial firms more likely would rise. Central banks’ every word would remain forensically scrutinised. And there would be an accompanying demand for ever-greater amounts of central bank transparency. Central banks would rarely be far from the front pages.

He acknowledged that central banks’ actions have already considerably influenced (distorted?…) financial markets over the past few years, though he views it as a relatively good thing (my emphasis):

With monetary, regulatory and operational policies all working in overdrive, central banks have had plenty of explaining to do. During the crisis, their actions have shaped the behaviour of pretty much every financial market and institution on the planet. So central banks’ words resonate as never previously. Rarely a day passes without a forensic media and market dissection of some central bank comment. […]

Where does this leave central banks today? We are not in Kansas any more. On monetary policy, we have gone from setting short safe rates to shaping rates of return on longer-term and wider classes of assets. On regulation, central banks have gone from spectator to player, with some granted micro-prudential as well as macro-prudential regulatory responsibilities. On operational matters, central banks have gone from market-watcher to market-shaper and market-maker across a broad class of assets and counterparties. On transparency, we have gone from blushing introvert to blooming extrovert. In short, central banks are essentially unrecognisable from a quarter of a century ago.

This makes me feel slightly unconfortable and instantly remind me of the – now classic – 2010 article by Jeff Hummel: Ben Bernanke vs. Milton Friedman: The Federal Reserve’s Emergence as the U.S. Economy’s Central Planner. While I believe there are a few inaccuracies and omissions in Hummel’s description of the financial crisis, his article is really good and his conclusion even more valid today than at the time of his writing:

In the final analysis, central banking has become the new central planning. Under the old central planning—which performed so poorly in the Soviet Union, Communist China, and other command economies—the government attempted to manage production and the supply of goods and services. Under the new central planning, the Fed attempts to manage the financial system as well as the supply and allocation of credit. Contrast present-day attitudes with the Keynesian dark ages of the 1950s and 1960s, when almost no one paid much attention to the Fed, whose activities were fairly limited by today’s standard. […]

As the prolonged and incomplete recovery from the recent recession suggests, however, the Fed’s new central planning, like the old central planning, will ultimately prove an unfortunate and possibly disastrous failure.

The contrast between central bankers’ (including Haldane’s) beliefs of a tightly controlled financial sector to those of Hummel couldn’t be starker.

Where it indeed becomes really worrying is that Hummel was only referring to Bernanke’s decision to allocate credit and liquidity facilities to some particular institutions, as well as to the multiplicity of interest rates and tools implemented within the usual central banking framework. At the time of his writing, macro-prudential policies were not as discussed as they are now. Nevertheless, they considerably amplify the central banks’ central planner role: thanks to them, central bankers can decide to reduce or increase the allocation of loanable funds to one particular sector of the economy to correct what they view as financial imbalances.

Moreover, central banks are also increasingly taking over the role of banking regulator. In the UK, for instance, the two new regulatory agencies (FCA and PRA) are now departments of the Bank of England. Consequently, central banks are in charge of monetary policy (through an increasing number of tools), macro-prudential regulation, micro-prudential regulation, and financial conduct and competition. Absolutely all aspects of banking will be defined and shaped at the central bank level. Central banks can decide to ‘increase’ competition in the banking sector as well as favour or bail-out targeted firms. And it doesn’t stop here. Tighter regulatory oversight is also now being considered for insurance firms, investment managers, various shadow banking entities and… crowdfunding and peer-to-peer lending.

Hummel was right: there are strong similarities between today’s financial sector planning and post-WW2 economic planning. It remains to be seen how everything will unravel. Given that history seems to point to exogenous origins of financial imbalances (whereas central bankers, on the other hand, believe in endogenous explanations, motivating their policies), this might not end well… Perhaps this is the only solution though: once the whole financial system is under the tight grip of some supposedly-effective central planner, the blame for the next financial crisis cannot fall on laissez-faire…

Raising capital requirements? Not that useful

The recent news of the near-bankruptcy of UK-based Cooperative Bank and Portugal-based Banco Espirito Santo made me question the utility of regulatory capital requirements. What are they for? Is raising them actually that useful? It looks to me that the current conventional view of minimum capital requirements is flawed.

In the pre-crisis era, banks were required to comply with a minimum Tier 1 capital ratio of 4% (i.e. Tier 1 capital/risk-weighted assets >= 4%). Most banks boasted ratios of 2 to 5 percentage points above that level. Basel 3 decided to increase the Tier 1 minimum to 6%, and banks are currently harshly judged if they do not maintain at least a 4% buffer above that level.

Indeed, given the possible sanctions arising from breaching those capital requirements, bankers usually thrive to maintain a healthy enough buffer above the required minimum. Sanctions for breaching those requirements include in most countries: revoking the banking licence, forcing the bank into a state of bankruptcy and/or forcing a restructuring/break-up/deleveraging of the balance sheet. Hence the question: what is the actual effective capital ratio of the banking system?

Companies – as well as banks in the past – are usually deemed insolvent (or bankrupt) once their equity reaches negative territory. At that point, selling all the assets of the company/bank would not generate enough money to pay off all creditors (while shareholders are wiped out).

Let’s assume a world with no Tier 1 capital but only straightforward equity, and without regulatory capital requirements. Following the basic rule outlined above, a bank with a 10% capital ratio can experience a 10% reduction in the value of its assets before it reaches insolvency. Let’s now introduce a minimum capital requirement of 6%. The same bank can now only experience a 4% reduction in the value of its assets before breaching the minimum and be considered good for resolving/restructuring/breaking-up by regulators.

For sure, higher minimum requirements have one advantage: depositors are less likely to experience losses. The larger the equity buffer, the stronger the protection.

However, there are also several significant disadvantages.

Given regulators’ current interpretation of the rules, higher minimum requirements also imply a higher sanction trigger. This creates a few problems:

- Raising the minimum threshold does little to protect taxpayers if regulators believe that a bank should be recapitalised, not when its Tier 1 gets close to or below 0%, but when it simply breaches the 6% level. In such case, it might have been possible for the bank’s capital buffer to absorb further losses without erasing its whole capital base and calling for help. For instance, Espirito Santo’s regulators said that its recapitalisation was compulsory: it reported a 5% equity Tier 1 ratio, below the 7% domestic minimum. And the state (i.e. taxpayers) obliged. But… It still had a 5% equity buffer to absorb further losses. Perhaps this would have been sufficient to absorb all losses and spare the taxpayers (perhaps not, but we may never find out).

- When approaching the minimum requirement, bankers are incentivised to start deleveraging in order to avoid breaching. Alternatively, they can be forced by regulators to do so. This has negative consequences on the availability of credit and on the money supply, possibly worsening a crisis through a debt deflation-type bust in order to comply with an artificially-defined 6% level.

- While depositors’ protection can be improved, it isn’t necessarily the case of other creditors, especially in light of the new bail-in rules that make them share the pain (so-called ‘burden-sharing’). Those rules kick in, not when the bank reaches a 0% capital ratio, but when it breaches the regulatory minimum (see here).

- Reaching the minimum requirement can also be self-defeating and self-fulfilling: fearing a bankruptcy event and the loss of their investments, shareholders run to the exit, pushing the share price down to zero and… effectively bringing about the insolvency of the bank. This doesn’t make much sense when a bank still has a 6% capital buffer. Espirito Santo suffered this fate until trading was suspended (see below).

So what’s the ‘effective’ Tier 1 capital ratio? Well, it is the spread between the reported Tier 1 and the minimum regulatory level. A bank that has an 8% Tier 1 under a 4% requirement, and a bank that has a 10% Tier 1 under a 6% requirement have virtually* the same effective capital ratio: 4%.

Regulatory insolvency events also cause operational problems. Espirito Santo was declared insolvent by its regulators but… not by the ISDA association! Setting regulatory minimums at 5% or 25% would have no impact on the issues listed above, as long as this logic is applied. To make regulatory requirements more effective, sanctions in case of breach should be minimal or non-existent in the short-term but should kick in in the long-term if banks’ capitalisation remains too low after a given period of time.

Regulatory minimums exemplify what Bagehot already tried to warn against already at his time: they are bound to create unnecessary panics. Speaking of liquidity reserves (the same reasoning as above applies), he said in Lombard Street:

[Minimums are bad] when legally and compulsorily imposed. In a sensitive state of the English money market the near approach to the legal limit of reserve would be a sure incentive to panic; if one-third were fixed by law, the moment the banks were close to one-third, alarm would begin, and would run like magic. And the fear would be worse because it would not be unfounded—at least, not wholly. If you say that the Bank shall always hold one-third of its liabilities as a reserve, you say in fact that this one-third shall always be useless, for out of it the Bank cannot make advances, cannot give extra help, cannot do what we have seen the holders of the ultimate reserve ought to do and must do.

* ‘virtually’ as, as described above, depositors protection is nonetheless enhanced, though even this is arguable given what happened in Cyprus

Flawed models + history ignorance = disastrous policy-making

Ben Southwood pointed to new research on banking which I thought would beautifully complement the point I was trying to make in my previous post on the ignorance of history.

The author designs a model that leads him to conclude that

contrary to conventional wisdom, competition can make banks more reluctant to take excessive risks: As competition intensifies and margins decline, banks face more-binding threats of failure, to which they may respond by reducing their risk-taking. Yet, at the same time, banks become riskier. This is because the direct, destabilizing effect of lower margins outweighs the disciplining effect of competition; moreover, a substantial rise in competition reduces banks’ incentive to build precautionary capital buffers. A key implication is that the effects of competition on risk-taking and on failure risk can move in opposite directions.

The paper declares that “a decline in margins caused by heightened competition [would lead to] a more conservative stance and less aggressive risk-taking” and that “high profits that can be reaped in less-competitive environment [would allow] for more risk-taking”. The author describes the literature as generally believing that… the opposite is true.

The paper declares that “a decline in margins caused by heightened competition [would lead to] a more conservative stance and less aggressive risk-taking” and that “high profits that can be reaped in less-competitive environment [would allow] for more risk-taking”. The author describes the literature as generally believing that… the opposite is true.

My first reaction is: it is so much more complex than that. Banks have different cultures and risk-aversions within the same context. This is why some fail why others remain strong throughout a given period. There is no pre-programmed behaviour that would push banks to act in a certain way. Within a given banking system and at a given point in time, banks offer investors a range of RoE and volatility of returns: investors can then diversify their banking investment portfolio according to their need and risk appetite. Some will prefer a high return/high volatility of earnings/high risk bank and require a higher cost of capital; others will go for stability and lower returns*. Banks are not trying to maximise RoE. Banks are trying to maximise RoE on a risk-adjusted basis**.

According to the author, historical experience demonstrates that competition makes banks riskier, and that this prediction is consistent with empirical evidence. Wait… Really? What kind of ‘competition’? In what context? Under what sort of banking, political and economic framework? Historical experiences of as close as possible to pure competition show the exact opposite of this claim. Indeed, the empirical evidence the author refers to is this 2009 paper, which statistically analysed current data from the Bankscope database. There is no reference to historical events, political circumstances, banking design and restrictive regulations. All types of banks, from the US granular unit banks to the Chinese giant government-controlled oligopoly banks are aggregated and ‘conclusion’ on competition is reached. This is bad research.

The paper is full of dubious claims, such as this one:

In our model, highly profitable banks optimally build equity capital buffers to guard against failure, whereas banks operating in more-competitive environments seek to minimize their capital.

Once again, this conclusion is so far from historical reality as to be meaningless. There are examples of oligopoly-type banks operating on thin capital buffers and free banking experiences in Scotland showed that competition led banks to accumulate large capital buffers. We also find examples of banks with local monopolies operating on a small equity base due to a particular banking structure. Banking system design and risk culture are key. Research pieces such as this one are over-simplistic and provide policy-makers with the wrong diagnoses.

But looking at the model’s assumptions, it becomes clear that the analysis was made in a vacuum. The banking system consists of one bank (no lending competition…), owned and run by infinitely lived shareholders, whose competitors are money market funds. Economics and finance is a matter of time-constrained resources management, and infinitely lived owners/bankers have different incentives and priorities from those whose life is finite and uncertain… Other unrealistic assumptions that skew the models include: money market funds that effectively compete with the (only) bank’s deposit rate for depositors’ funds, or very granular time periods during which the bank has no flexibility to raise capital or deal with its balance sheet issues, resulting in very binary outcomes at the end of each period. And, of course, this ‘competitive’ system includes deposit insurance and capital requirements.

In the end, we can reasonably question what this model proves, if anything. This exemplifies the problems I have with financial and economic models in general: they are not reliable. And this is an understatement.

For instance, the conclusions reached by this model are precisely the opposite of those reached by other models built for previous similar studies. What does this mean? Which ones are right (if any)? Which ones are wrong (if any)?

I used to be a scientist and have a Master’s degree in engineering. I also used to believe that everything could be modelled. I was wrong. Economic systems do not benefit from universal physical constants.

When I started my career in financial services, I tended to use mathematical and statistical tools (trends, correlations) to forecast some financial information. A senior analyst warned me: “it never works.” He was right, but I didn’t believe him to start with and continued experimenting nonetheless, until I noticed that ‘intuition’, ‘knowledge’ and ‘wisdom’ would serve me more than mathematics. What was I trying to forecast? Revenues of a listed firm. Nothing really complex.

Unfortunately, most economists and central bankers still believe they can model the whole economy – or, as seen above, the whole banking system – using maths. Given the inaccuracy of quarterly revenue and profit per share estimates, modelling something infinitely more complex (the whole economy), which involves an infinite number of ever-changing, erratic and poorly-rational variables (i.e. humans), sounds like an enormous, if not impossible, project. Still, this is what academic DSGE models have been trying to do for a few decades. With great success as we have been witnessing since 2007.

I agree (for once) with this post by Noah Smith, who rightly asks:

So why doesn’t anyone in the finance industry use them? Maybe industry is just slow to catch on. But with so many billions upon billions of dollars on the line, and so many DSGE models to choose from, you would think someone at some big bank or macro hedge fund somewhere would be running a DSGE model. And yet after asking around pretty extensively, I can’t find anybody who is.

One unsettling possibility is that the academic macroeconomists of the ’70s and ’80s simply bit off more than they could chew. Modeling a big thing (like the economy) as the outcome of a bunch of little things (like the decisions of consumers and companies) is a difficult task. Maybe no DSGE is going to do the job. And maybe finance industry people simply realize this.

Of course, many people working in finance still try to forecast the future. But their forecasts are in competition with each other and none of them has the power to make the decision that central banks or policy-makers can make for the whole economy, with potentially disastrous consequences. The Fed’s, ECB’s and BoE’s forecasts have constantly been way off the mark throughout the crisis. I also know from certain sources that some of central banks’ models are less elaborate than rating agencies’. I’ll let the reader conclude.

The example above clearly demonstrates why economics should avoid relying on mathematics and simplified assumptions. Time to stop ignoring history.

* In a banking system with no deposit insurance, the same applies: depositors have the choice between higher deposit rates/higher risk or lower and safer ones.

** This is where moral hazard and bad regulatory incentives applies: by distorting risk-aversion and assessment.

Recent Comments