Some new (more or less useful) research

A few noticeable papers have been published recently. They are not particularly ground-breaking but some offer interesting insights and datasets. Here are summaries:

– The Effects of Unconventional Monetary Policies on Bank Soundness, an IMF working paper by Lambert and Ueda, is an interesting piece of research though its results are no surprise:

Unconventional monetary policy is often assumed to benefit banks. However, we find little supporting evidence. Rather, we find some evidence for heightened medium-term risks. First, in an event study using a novel instrument for monetary policy surprises, we do not detect clear effects of monetary easing on bank stock valuation but find a deterioration of medium-term bank credit risk in the United States, the euro area, and the United Kingdom. Second, in panel regressions using U.S. banks’ balance sheet information, we show that bank profitability and risk taking are ambiguously affected, while balance sheet repair is delayed. (my emphasis)

I’m not a great fan of the first part of their study, in which they run a regression between monetary policy events and banks’ share prices, credit spreads and CDS spreads: they do not take into account government support, which considerably affects the perceived creditworthiness of a number of banks. Their second part (what I highlighted in the abstract above) is more interesting though not that surprising. I have already described many times how profitability, and hence internal capital generation, were subdued in a close to zero interest rate environment.

– Identifying Excessive Credit Growth and Leverage, an ECB staff working paper by Alessi and Detken, is also interesting given the methodology but… seems to be stating the obvious. According to the paper, some of the best indicators of ‘excess leverage’ in the economy are…bank credit/GDP or the debt service ratio… (see table below)

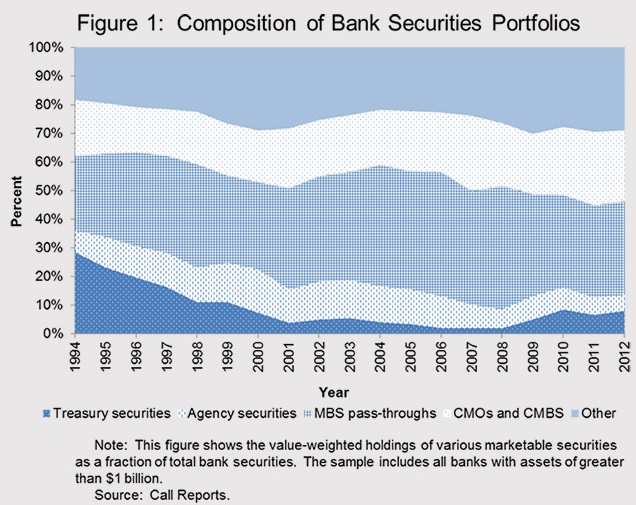

– A little older, Banks as Patient Debt Investors, is an introductory speech to forthcoming research by Jeremy Stein, member of the Board of Governors of the Fed. This is perhaps the most interesting and theoretical of the papers I have read over the past few days and I am looking forward to dissecting the final published version. This is Stein:

I have argued that there is a synergy between banks’ stable funding model and their investing in assets that have modest fundamental risk but whose prices can fall significantly below fundamental values in a bad state of the world. This synergy helps explain both why deposit-taking banks might have a comparative advantage at making information-intensive loans and, at the same time, why they tend to hold the specific types of securities that they do.

He makes some interesting remarks, though I have the impression that he misstates the actual accounting treatment of ‘Available for Sales’ assets, which he uses to justify his model. This might lead him to the wrong conclusions. A fall in the value of AFS assets will indeed not affect net income but will negatively affect equity/capitalisation through the bank’s comprehensive income statement, possibly undermining some of his conclusions or some of his reasoning. However, it is too early to judge, and I’ll read the whole finished paper once it is published.

Stein also presented an interesting chart to back his research. Most of US banks’ securities portfolios are comprised of assets that benefit from low risk-weights under Basel. I would have liked to see this chart starting from the 1970s (i.e. pre-Basel era).

PS: I wish to thank Ben Southwood, from the Adam Smith Institute, for providing me with some of those links

Recent Comments