The surprising effects of negative rates on German banks

Several banks have already made public their intentions to withdraw their excess reserves from the ECB, following the central bank’s decision to charge banks for keeping excess reserves deposited with it (i.e. negative deposit rates). It is unclear what’s going to happen to this cash. If it is redeposited at another Eurozone bank, then it still ends up on an ECB account. Euros could potentially be placed somewhere outside the Eurozone to reduce the aggregate amount of excess reserves in the system, but there is no guarantee they would not come back either (through non-Euro companies paying Euro suppliers for instance). Banks could also withdraw paper money, but this involves storage costs.

Very low ECB main rates already represented a pressure on banks’ net interest margins. The ECB negative deposit rates were seen as a way to bolster the interbank money markets. Unfortunately, many banks are now also retracting from interbank markets altogether because of the very poor yields obtained on those placements… thanks to the low ECB main rate. Seen this way, very low ECB refinancing rates and negative ECB deposit rates look contradictory.

But there’s something new.

In Germany, some banks (mostly the largest ones), are now passing on negative rates to… their clients. Handelsblatt reported last week that institutional clients such as mutual funds and insurers have now been asked to pay interests on short-term deposits… To be honest, I wasn’t really expecting such a move, given the instability it can create in banks’ funding structure. However, the effects remain for now limited as retail clients, as well as other types of corporate clients, are unaffected.

Let’s get back to our basic bank’s profit equation:

Economic Profit = II – IE – OC – Q

where II represents interest expense, IE interest income, OC operating costs (which include impairment charges on bad debt), and Q liquidity cost.

As we recently saw, low ECB interest rates impact II downward, negative ECB deposit rates impact IE upward, meaning ceteris paribus that the only thing banks can do to remain profitable in the short-run is to cut fixed costs (OC). Ex-post, banks can also influence IE by repricing their loan book upward.

This is indeed what has been happening in Germany: banks have been cutting staff, deleveraging, and outsourcing expenses to low-cost countries. The spread between new lending rates and the ECB main rate has also remained consistently high since the rate cuts, and has even started to increase again following the most recent rate cuts (see below, blue arrows represent rate cuts, red arrows represent spread increases).

By passing negative deposit rates onto customers, banks found a way of quickly increasing II to partially offset the increase in IE. The effects are faster than further increasing the interests charged on lending, as it directly impacts the outstanding stock of deposits (unlike repricing, whose pace depends on the volume and maturity profile of the bank’s loan book).

However, this provides customers with an incentive to withdraw their deposits, introducing instability in the banks’ funding structure, increasing Q. Given the limited range of customer concerned so far, those banks probably thought it was a worthwhile temporary bet. Indeed, increasing their lending volume to reduce their excess reserves, or investing those reserves somewhere, would also have increased Q anyway. Furthermore, those institutional clients are likely to have significant brokerage/trading/custody relationships with those banks, making it difficult for them to close their accounts and move funds away without disrupting their business.

I have no information regarding the implementation of such policies by other banks of the Eurozone so far. If those policies become widespread, the ECB’s decisions will not only have been pointless, but they will also have succeeded in making the funding structure of the whole Eurozone banking system more unstable and in reducing the purchasing power of non-bank corporations that have to maintain deposits in the Eurozone.

Unintended (intended?) consequences

In my previous post, I described how politicians (in this case, Vince Cable) were confused by the impacts of banking regulations. The large amount of new and modified rules that have been striking the financial sector over the past few years are bringing their lot of unintended consequences. Unless some of those consequences were actually perfectly intended…

About a week ago, The Economist reported the collapsing global financial links:

One of the main casualties of the cringe is the very institution of correspondent banking. This is the informal mesh of arrangements allowing the customer of a bank in one country to send money to someone in another country, even if the bank in question does not have a branch there. The system is as old as international finance itself, dating back to the earliest promissory notes and letters of credit written by banks in classical times. Yet it is now being threatened by an overzealous interpretation and enforcement of rules aimed at preventing money-laundering and starving terrorists of funds. […]

The exact size of the retreat is difficult to gauge because of a dearth of recent global data, but executives at such firms say they are dropping as many as a third of their correspondent relationships. One big firm says it is cutting or scaling back about 1,000 linkages; another, 1,800. Such ruthlessness will have a dramatic impact because these institutions are the main nodes through which the world’s banks link up with one another. […]

It is not just in distant and benighted places that the consequences of this severity are being felt. In Britain students from Iran, Sudan and Syria cannot open bank accounts. In America, foreign diplomats and embassies complain that they too are being denied access to banking.

Do-gooders are being caught in the net, too. Charities such as Save the Children, the Red Cross and Christian Aid have struggled to transfer funds to places like Syria due to sanctions. Even after obtaining explicit approval from American regulators, some have found it difficult to convince banks to send money.

We’re indeed on our way to the de-globalisation of banking, with all the systemic risks this involves. Whether or not the outcome of this particular policy was intended by regulators is something I cannot answer. But in general, regulators have been actively working on the fragmentation of the global banking system, as we’ve recently seen.

The research paper from the London School of Economics found the daily changes in the valuation of margin, which traders are required to post, may rise tenfold by using central clearing houses. That compared to banks being allowed to clear the same deals between themselves.

The paper’s conclusion that banks may face greater operational risks and more demands on their liquidity underlines regulators’ and market participants’ concerns that a post-crisis global political accord designed to strengthen the financial system may only succeed in shifting risk.

I haven’t read the study yet (and actually couldn’t even find it on the LSE SRC website), but it does look like the outcome of those new rules is going to be reduced interlinks (through derivative contracts) between banks.

Let’s sum up. New rules that favour a fragmented banking system are:

- Ringfencing different parts within individual banks/legal entities

- Asking for separate capital and funding structures between subsidiaries of a same group

- Reducing the ability of various entities of a same banking group to transfer liquidity and capital

- Reducing interconnectivity and financial agreements between banks of different countries

- Making derivative trading and settlements more expensive

- I’m surely forgetting a lot of other things

My guess is that it will take a few years (possibly early 2020s) to find out what kind of monster this magic regulatory potion really created.

Vince Cable realises too late what banking regulation involves

Back from holidays, and a lot of things to cover…

Let’s start with Vince Cable, Britain’s Secretary of State for Business, who is making a U-turn, though not yet quite finished, as he progressively realises how much he ignored about the pernicious effects of banking regulation.

The way the regulatory system operates has undoubtedly had a suffocating effect on business lending and particularly on our exporters.

Not surprisingly, the result is that banks pump out lending in the mortgage market, while lending to small businesses is restricted. This directly stems from the rules on which the regulatory model is based and has had a very damaging impact.

You may well recognise that he is referring to risk-weighted assets (RWAs), which have been a recurrent theme of this blog (and the focus of my three latest posts). Vince Cable had already sparked controversy pretty much exactly a year ago, when he first attacked the BoE for being a ‘capital Taliban’:

One of the anxieties in the business community is that the so called ‘capital Taliban’ in the Bank of England are imposing restrictions which at this delicate stage of recovery actually make it more difficult for companies to operate and expand.

This is a welcome reaction by one of the country’s top politician. However, let’s go back a few years to find the same Mr Cable vehemently supporting the exact same reforms he now criticises, while fully rejecting bankers’ claims that increased capital requirements would allocate funding away from SMEs (see here, here, here, here and here):

Banks and industry groups have argued more regulation could force institutions to curb lending to small- and medium-sized businesses at a time when the economy is slowing.

Prediction which turned out to be correct.

Mr Cable’s went from blaming banks for the crisis and justifying stronger regulatory requirements to blaming those same requirements for the weak level of business lending in the UK. Unfortunately, his U-turn isn’t fully completed and Mr Cable attacks the wrong target. Capital requirements are defined in Basel, the Swiss city. And he supported them in the first place, without evidently knowing what those rules involved. He also seemingly showed a poor understanding of banking history as his support for banking insulation through ring-fencing demonstrated (though most regulators are to blame as well).

Better late than never? Perhaps, but probably too late to have any effect going forward… Politicians’ and regulators’ rush to design banking rules in order to please the public opinion is making everyone worse off in the end.

Photo: Rex Features

The era of the neverending bubble?

The IMF got the timing right. It published last week a new ‘Global Housing Watch‘, and warned that house prices were way above trend in a lot of different countries all around the world. The FT also reports here:

The world must act to contain the risk of another devastating housing crash, the International Monetary Fund warned on Wednesday, as it published new data showing house prices are well above their historical average in many countries.

As I said, perfect timing, as this announcement follows my previous post on the influence of Basel’s RWAs on mortgage lending.

As long as international banking authorities don’t get rid of this mechanism, we are likely to experience reoccuring housing bubbles with their devastating economic effects (hint for Piketty: and investors/speculators will have an easy life making capital gains).

PS: I am on holidays until the end of the week, so probably not many updates over the next few days.

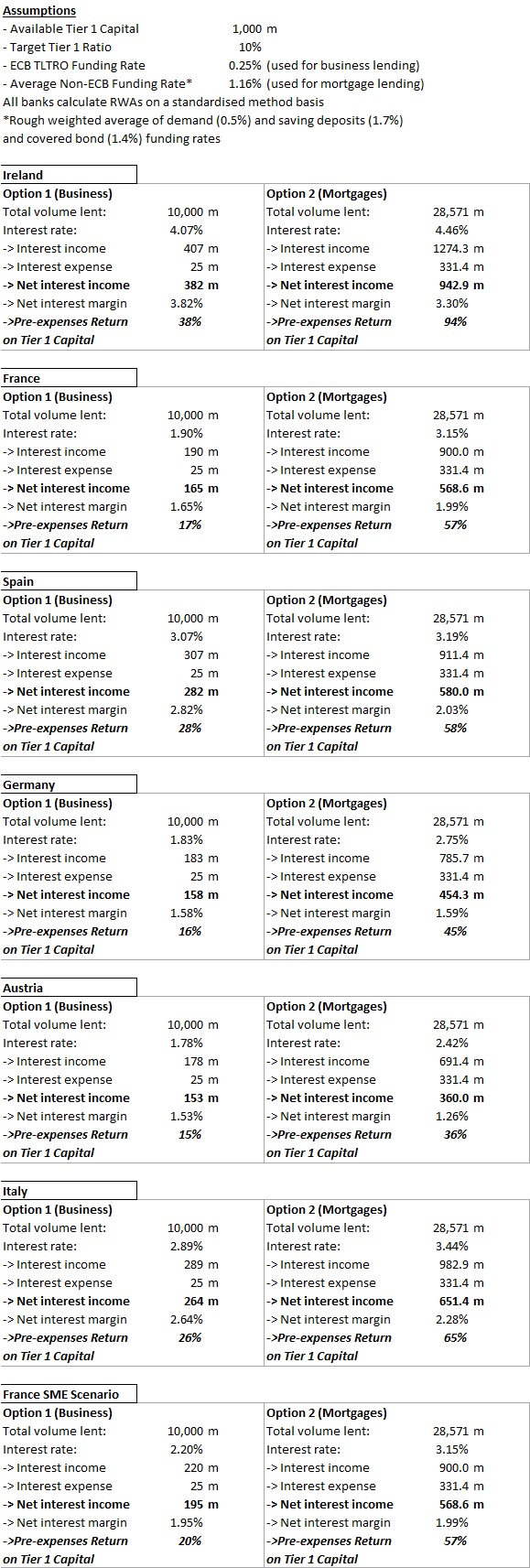

Basel vs. ECB’s TLTRO: The fight

(and vs. BoE’s FLS)

Following my previous post on the mechanics of ECB negative deposit rates, I wanted to back my claims about the likely poor effect of the central bank TLTRO measure on lending.

I argued that despite the cheap funds provided by the ECB to lend to corporate clients (particularly SMEs), Basel’s risk-weighted assets would stand in the way of the scheme as they keep distorting banks’ lending incentives (same is true regarding the BoE and the second version of its Funding for Lending Scheme).

I extracted all the most recent new business and mortgage lending rates from the central banks’ websites of several European countries. Unfortunately, business lending rates are most of the time aggregates of rates charged to large multinational companies, SMEs, and micro-enterprises. Only the Banque of France seemed to provide a breakdown. So most business lending rates below are slightly skewed downward (but not by much as you can see with the French case).

Using this dataset, I built a similar scenario to the one I described in my first RWAs and malinvestments post (as it turned out, I massively overestimated business lending rates in that post…). I wanted to find out what would be the most profitable option for a bank: business lending or mortgage lending, given RWA and capital constraints (banks target a 10% regulatory Tier 1 capital ratio). The results speak for themselves:

Despite the cheap ECB loans, and given a fixed amount of capital, banks are way more profitable raising funding from traditional sources to lend to households for house purchase purposes…

Admittedly, the exercise isn’t perfect. But the difference in net interest income and return on capital is so huge that tweaking it a little wouldn’t change much the results:

- I assume that all business lending is weighted 100%. In reality, apart from the French SME scenario, large corporates (often rated by rating agencies) benefit from lower RWA-density under a standardised method. This would actually raise the profitability of business lending through higher volume (and increased leverage), though not by much. Mortgages are weighted at 35% under that method.

- I assume that all banks use the standardised method to calculate RWAs. In reality, only small and medium-sized banks do. Large banks use the ‘internal rating based’ method, which allows them to risk-weight customers following their own internal models. Here again, most corporates can benefit from lower RWAs. But mortgages also do (RWA-density often decreases to the 10-15% range).

- Cross-selling is often higher with corporates, which desire to hedge and insure their financial or non-financial business positions. Corporates also use banks’ international payment solutions. This adds to revenues.

- Business lending is often less cost-intensive than retail lending. Retail lending indeed traditionally requires a large branch network, which is less the case when dealing with corporates (often grouped within regional corporate centres, though not always for tiny enterprises). However, retail banking is progressively moving online, providing opportunities to banks to cut costs and improve their profitability.

- The lower RWA-density on mortgages allows banks to increase lending volume and leverage. However, this also requires higher funding volumes. In turn, this should increase the rate paid on the marginal increase in funding, raising interest expense somewhat in the case of mortgages.

In the end, even if the adjustments described above reduce the profitability spread by 10 percentage points, the conclusion stands: banks are hugely incentivised to avoid business lending, facilitating misallocation of capital on a massive scale, in particular in a period of raising capital requirements… Moreover, banks also benefit from favourable RWAs for securitised products based on mortgages (CMBS, RMBS…), compounding the effects.

To tell you the truth, I wasn’t expecting such frightening results when I started writing that post… Please someone tell me that I made a mistake somewhere…

Central banks, regulators and politicians will find it hard to prop up business lending with regulations designed to prevent it.

The (negative) mechanics of negative ECB deposit rates

The ECB has finally announced last week that it would be lowering its main refinancing rate from 0.25% to 0.15%, and that it would lower the rate it pays on its deposit facility from 0% to -1%. The ECB hopes to incentivise banks to take money out of that facility and lend it to customers*, providing a boost to the broad money supply and counteracting deflation risks.

The interest rate of the ECB deposit facility is supposed to help the central bank define a floor under which the overnight interbank lending rate (EONIA) should not go. The reason is that deposits at the ECB are supposedly risk-free (or at least less risky than placing the money anywhere else). Consequently, banks would never place money (i.e. excess reserves) at another bank/ investment (which involves credit risk) for a lower rate. When the deposit facility rate is high, banks are incentivised to reduce their interbank lending exposures and leave their money at the ECB (and vice versa). On the other hand, the main refinancing rate is supposed to represent an upper boundary to the interbank lending rates: theoretically, banks should not borrow from another bank at a higher rate than what it would pay at the ECB. In practice, this is not exactly true, as banks do their best to avoid the stigma associated with borrowing from the central bank.

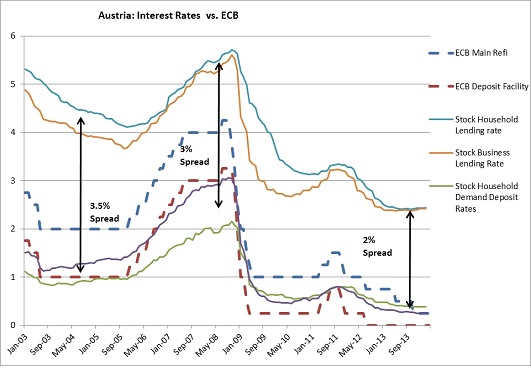

Unfortunately, there is a fundamental microeconomic reason why banks cannot diminish their lending rate indefinitely. I have already described how banks are not able to transmit interest rates lower than a certain threshold to their customers due to the margin compression effect (see also here). Indeed, banks’ net interest income must be able to cover banks’ fixed operating costs for the bank to remain profitable from an accounting point of view. When rates drop below a certain level, banks have to reprice their loan book by increasing the spread above the central bank rate on the marginal loans they make, breaking the transmission mechanism of the lending channel of monetary policy. As we have already seen, in the UK, that threshold seems to be around 2%.

But the same thing seems to happen in other European countries. This is Ireland (enlarge the charts)**:

We can notice the margin compression effect on the first chart. The lending rate stops dropping despite the ECB rate falling as banks reprice their lending upward to re-establish profitability (evidenced from the second chart, where interest rates on new lending increase rather than decrease).

This is France:

This is Austria:

Clearly, what happens in the UK regarding margin compression also occurs in those countries. When the ECB rate dropped, outstanding floating rate lending rates also dropped (because floating rate lending is indexed on either the ECB base rate or on Euribor), causing pressure on revenues. As long as deposit rates could also fall (this varies a lot by country, as French banks never pay anything on demand deposits), the loss in interest income was offset by reduced interest expense. But once deposit rates reached 0 and couldn’t fall any lower, banks in those countries experienced margin compression and their net interest income started to suffer. Moreover, this happened exactly when loan impairment charges peaked because of increased credit risk.

Banks in emerging countries have constantly high non-performing loans ratios. But they still manage to remain (often highly) profitable by maintaining very high net interest income and margins. In Western Europe, banks saw their net profits all but disappear with rates dropping that low. As a result, it is likely that the new ECB rate cut won’t affect lending rates much…

Nonetheless, the ECB had been trying to revive, or encourage, interbank lending throughout most of the crisis, and had already lowered to its deposit rate to 0%. Nevertheless, banks maintained cash in those accounts. Why would a bank leave its money in an account that pays 0%? Because banks adjust those interest rates for risk. An ECB risk-adjusted 0% can be worth more than a risk-adjusted 4% interbank deposit at a zombie/illiquid/insolvent bank. However, the ECB is clearly not satisfied with the situation: it now wants banks to take their money out of the facility and lend it to the ‘real economy’.

How do the combination of low refi rate and negative ECB deposit rates impact banks? Let’s remember banks’ basic profit equations:

Accounting Profit = II – IE – OC, and Economic Profit = II – IE – OC – Q

where II represents interest expense, IE interest income, OC operating costs (which include impairment charges on bad debt), and Q liquidity cost.

For a bank to remain economically profitable (or even viable in the long-term), the rate of economic profit must be at least equal to the bank’s cost of equity.

To maximise their economic profits, banks look for the most-profitable risk-adjusted lending opportunities. ‘Lending’ to the ECB is one of those opportunities. Placing money at the ECB generates interest income. This interest income is more than welcome to (at least) maintain some level of accounting profitability (though not necessarily economic profitability) when economic conditions are bad and income from lending drops while impairment charges jump***.

With deposit rates at 0, banks’ income became fully constrained by financial markets and the economy. With rates in negative territory, not only banks see their interest income vanish but also their interest expense increase. From the equations above, it is clear that it makes banks less profitable****. On top of that, lending that cash can make banks less liquid, which increases their riskiness and elevates their cost of capital (the ‘Q’ above). The question becomes: adjusted for credit and liquidity risk, is it still worth keeping that cash at the ECB? The answer is probably yes.

(unless banks find worthwhile investments outside of the Eurozone, which wouldn’t be of much help to prop up Euro economies…)

To summarise, ‘II’ is negatively impacted by a low base rate whereas ‘IE’ reaches a floor (= margin compression). ‘IE’ then increases when the central bank deposit rate turns negative. Meanwhile, ‘OC’ increases as loan impairment charges jump due to heightened credit risk. Profitability is depressed, partly due to the central bank’s decisions.

Many European banks aren’t currently lending because they are trying to implement new regulatory requirements (which makes them less profitable) in the middle of an economic crisis (which… also makes them less profitable). As a result, the ECB measures seem counterproductive: in order to lend more, banks need to be economically profitable. Healthy banks lend, dying ones don’t.

The ECB is effectively increasing the pressure on banks’ bottom line, hardly a move that will provide a boost to lending. The only option for banks will be to cut costs even further. And when a bank cut costs, it effectively reduces its ability to expand as it has less staff to monitor lending opportunities, and consequently needs to deleverage. Once profitability is re-established, hiring and lending could start growing again.

A counterintuitive (and controversial) approach to provide a boost to lending would be to subsidise even more the banking sector by increasing interest rates on both the refinancing and deposit facilities.

Defining the appropriate level of interest rates would be subtle work though: struggling over-indebted households and businesses may well start defaulting on their debt. On the other hand banks’ revenues would increase as margin compression disappears, making them able to lend more eventually. The subtle balance would be achieved when interest income improvements more than offset credit losses increases. Not easy to achieve, but pushing rates ever lower is likely to cripple the banking system ever more and reduce lending in proportion (while allowing zombie firms to survive).

Furthermore, banks are repricing their loan book upward anyway, making the ECB rate cuts pointless. The process takes time though and it would be better for banks to rebuild their revenue stream sooner than later. The ECB could still use other monetary tools to influence a range of interest rates and prices through OMO and QE measures, which would be less disruptive to banks’ margins.

Finally, the ECB has launched its own-FLS style ‘TLTRO’, a scheme that provides cheap funding to banks if they channel the funds to businesses. Similarly to the BoE’s FLS, I believe such scheme suffers from delusion. Banks are currently deleveraging to lower their RWAs in order to comply with the harsher capital requirements of Basel 3. If there is one thing banks want to avoid, it is to lend to RWA-dense customers such as SMEs… (and instead focus on better RWA/risk-adjusted profitable lending such as… mortgages). Banks can also already extract relatively low wholesale funding rates by issuing secured funding instruments such as covered bonds. (UPDATE: see this follow-up post on that topic)

* This does not mean that banks would ‘lend out’ money to customers, unless they withdraw it as cash. But by increasing lending, absolute reserve requirements increase and banks have to transfer money from the deposit facility to the reserve facility.

** Data comes from respective central banks. They are not fully comparable. I gathered data from many different Eurozone countries, but unfortunately, some central banks don’t provide the data I need (or the statistics database doesn’t work, as in Italy…). Spreads are approximate ones calculated between the middle point of deposit rates and the middle point of lending rates. Analysis is very superficial, and for a more comprehensive methodology please refer to my equivalent posts on the UK/BoE.

*** Don’t get me wrong though. Fundamentally speaking, I am not in favour of such central bank mechanisms as I believe this is akin to a subsidy that distorts banks’ risk-taking behaviour. In a central banking environment, like Milton Friedman I’d rather see the central bank manipulate interest rates solely through OMO-type operations.

**** Of course this remains marginal. But in crisis times, ‘marginal’ can save a bank. Let’s also not forget booming litigation charges, currently estimated at USD104Bn… Evidently making it a lot easier for banks to lend as you can imagine…

In case anybody still doubted that RWAs affect banks’ lending allocation…

Just a very very quick post tonight.

Our business is constrained by the capital we have available to cover risk-weighted assets (RWA) resulting from the risks in our business, by the size of our on- and off-balance sheet assets through their contribution to leverage ratio requirements and regulatory liquidity ratios, and by our risk appetite. Together, these constraints create a close link between our strategy, the risks that our businesses take and the balance sheet and capital resources that we have available to absorb those risks. As described in “Equity attribution framework” in the “Capital management” section of this report, our equity attribution framework reflects our objectives of maintaining a strong capital base and guiding businesses towards activities that appropriately balance profit potential, risk, balance sheet and capital usage.

Where does this come from? The 2013 annual report of UBS, the largest Swiss bank (page 150).

How banks are incentivised by Basel’s risk-weighted assets is clear. What provides has a low capital treatment (= low RWA), has relatively low default risk, is highly collateralised, even though it doesn’t bring in much interest income? Yep, mortgages (as well as some tranches of securitised products such as RMBSs, and sovereign debt).

Calomiris and Haber are pretty much spot on

I recently finished reading Fragile by Design, the latest book of Charles Calomiris and Stephen Haber.

Let’s get to the point: it’s one of the best books of banking I’ve had the occasion to read. It is a masterpiece of banking and political history and theory.

Calomiris and Haber describe the stability and efficiency of banking systems in terms of local political arrangements and institutions, which contrasts with most of nowadays’ theories that don’t distinguish between banking systems in various countries and way too often seem to draw conclusions on banking from the US experience only.

They describe banks’ stability in terms of a ‘Game of Banks Bargains’: the tendency for populists and bankers to form coalitions that aren’t favourable for society as a whole but favourable for politicians’ short-term political gains and bankers’ short-term profits. Needless to say, this alliance is built at the expense of long-term stability and efficiency. Only countries that have built political institutions to counteract the effects of populist policy proposals have experienced a stable financial environment since the early 19th century.

This thesis is extremely convincing and, while I find it unsurprising, it is so well documented that it is sometimes almost shocking. It clearly goes against mainstream Keynesian and Post-Keynesian theories, which consider financial collapses as a result of the normal process of human ignorance and panics. According to those theories, banks will fail at some point, hence the need for regulation and intervention early on. From most Keynesian books and articles I’ve read so far, collapses just happen. I’ve always been bewildered by the lack of underlying explanation: “that’s just the way it is”. Hyman Minsky’s Stabilizing an Unstable Economy is the perfect example: it draws general conclusions about the banking sector and the economy from a period of a couple of decades in the US… Knowledge of financial history quickly proves those arguments wrong.

The book isn’t without flaws however. It describes and compares the history of banking systems in England, the US, Canada, Mexico and Brazil. I found that either Brazil or Mexico could have been skipped (as covering both didn’t bring that much more to the thesis) in order to study more in depth another European (French, German, Italian) and/or Asian (Japanese, Indian…) banking system.

Also, while the (long) description of the political ramifications that led to the US subprime crisis is stunning, I believe the authors’ thesis is incomplete. There is no doubt that the populists/housing agencies/bankers alliance (or forced alliance) amplified the crisis by generating way too many low-quality housing loans through declining underwriting standards. However, this cannot be the only reason behind the crash. As I have described in many posts, properties have boomed and crashed all around the world in a coordinated fashion during the same period due to regulations incentivising house lending (and securitized products based on housing loans), as well as low interest rates. It is hard to argue that the Irish or the Spanish housing markets were the victims of US populists and US subprime lending…

Finally, what Calomiris and Haber describe is that free-market banking systems are less prone to systemic failures. From their work, it is clear that: 1. the fewer rules the banking system is subject to and 2. the less government intervention in the finance industry, the more stable the financial system. They demonstrate that the more lightly regulated Canadian system and the Scottish free-banking system were seen as almost ideal. Nevertheless, they seem to refrain from explicitly argue in favour of free-banking systems for some reason. I found this a little odd.

I certainly disagree with their view that banks can only exist when the state exists and charter them because of their interrelationship (i.e. states can raise financing through banks and banks get competitive advantages in return). Their arguments are really unconvincing: 1. it isn’t because such occurrences are rare in recent history that they cannot happen and 2. we have consistently witnessed throughout history, and in particular over the past decades, the spontaneous emergence of unchartered financial institutions (from money market funds to P2P lending firms) that respond to a private need for financial services. I do not think those are ‘utopian fantasies’ as this is happening right in front of us right now… States started to select, allow, charter and regulate those institutions when they needed finance. This does not imply that a limited and pacifistic state necessarily needs to use the same constraining tools.

In the end, those flaws remain minor and the book is easily one of my favourites. It deserves much more attention than what the media have given them so far (indeed, they go against the traditional ‘banking is inherently unstable’ tenet…). Unfortunately, the media are more interested in bank-bashing stories, putting in the spotlight much weaker books such as The Bankers’ New Clothes (by Admati and Hellwig)…

PS: FT’s John Kay also talks about the book here.

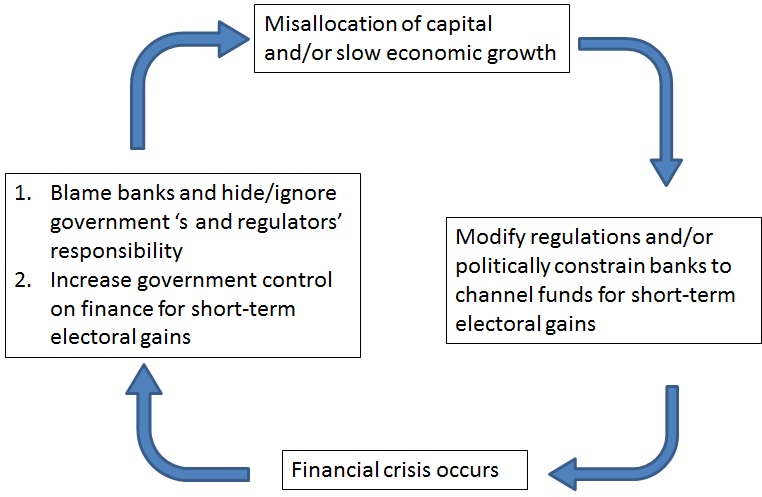

The political banking cycle

A couple of weeks ago, The Economist reported that Mel Watt, the new regulator of the US federal housing agencies Fannie Mae and Freddie Mac, wanted those two agencies to stop shrinking and continue purchasing mortgage loans from banks in order to help homeowners and the housing market (also see the WSJ here). To twist the system further, the compensation of the agencies’ executives will be linked to those political goals. Mr Watt used to be one of the main proponents of more accessible house lending for poor households through Fannie and Freddie before the crisis.

As The Economist asks, “what could go wrong?”…

Lars Christensen and Scott Sumner also find this ridiculously misguided government intervention horrifying. I find myself in complete agreement (and this is an understatement). Who could still honestly say that we are (or were) in a laissez-faire environment?

This, along with UK’s FLS and Help to Buy schemes, made me think that there has been a ‘political banking cycle’ throughout the 20th century. Why 20th century? From all the banking history I’ve read so far, populations seemed to better understand banking before the introduction of safety net measures such as central banks, deposit insurances or systematic government bail-outs. When financial crashes occurred, blame was usually shared between governments and banks, if not governments only. This is why many crises triggered deregulation processes rather than reregulation ones. This contrasts with the mainstream view our society has had since the Great Depression: when a financial crash happens, whatever the government’s responsibility is, banks and free market capitalism are the ones to blame.

This political cycle looks like that:

The worst is: it works. Politicians escaped pretty much unscathed from the financial crisis despite the huge role they played in triggering it*. The majority of the population now sincerely believes that the crisis was caused by greedy bankers (see here, here, here and here). This is as far from the truth as it can be (I don’t deny ‘greed’ played a role though, but channelled through and exacerbated by a combination of other factors, i.e. moral hazard etc.). Unfortunately, it is undeniable: politicians won. And not only politicians won, but they also managed to self-convince that they played no role in the crisis, as the example of Mr Watt shows (he either truly believes that government intervention in the US housing market was a good thing, or he has an incredibly cynical short-term political view).

The crucial question is: why did 19th century populations seem more educated about banking? The answer is that the lack of state paternalism through various protection schemes forced bank depositors and investors to oversee and monitor their banks. Once protection is implemented, there is no incentive or reason anymore to maintain any of those skills.

Who is easier to manipulate: a knowledgeable electorate or an ignorant one?

PS: This chart is mostly accurate for democracies that have a populist tendency. Not all countries seem to be prone to such cycle (this can be due to cultural or institutional arrangements).

* I won’t get into the details here, but if you’re interested, just read Engineering the Financial Crisis, Fragile by Design or Alchemists of Loss……. or simply this NYT article from 1999.

Recent Comments