Basel vs. ECB’s TLTRO: The fight

(and vs. BoE’s FLS)

Following my previous post on the mechanics of ECB negative deposit rates, I wanted to back my claims about the likely poor effect of the central bank TLTRO measure on lending.

I argued that despite the cheap funds provided by the ECB to lend to corporate clients (particularly SMEs), Basel’s risk-weighted assets would stand in the way of the scheme as they keep distorting banks’ lending incentives (same is true regarding the BoE and the second version of its Funding for Lending Scheme).

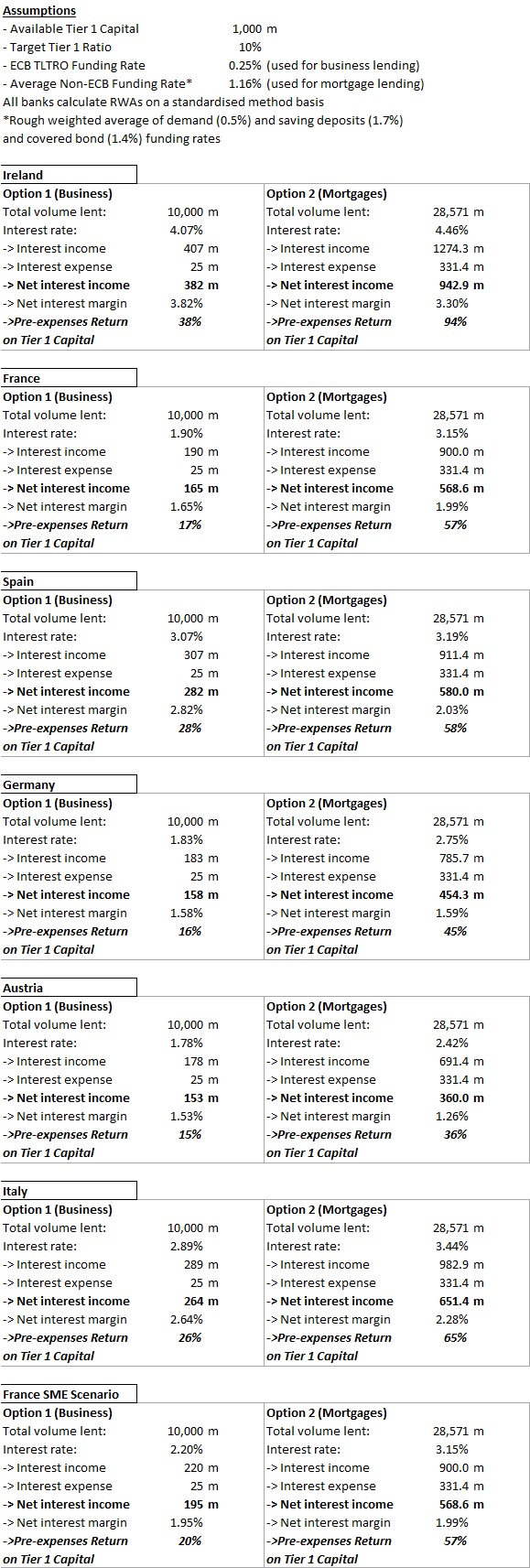

I extracted all the most recent new business and mortgage lending rates from the central banks’ websites of several European countries. Unfortunately, business lending rates are most of the time aggregates of rates charged to large multinational companies, SMEs, and micro-enterprises. Only the Banque of France seemed to provide a breakdown. So most business lending rates below are slightly skewed downward (but not by much as you can see with the French case).

Using this dataset, I built a similar scenario to the one I described in my first RWAs and malinvestments post (as it turned out, I massively overestimated business lending rates in that post…). I wanted to find out what would be the most profitable option for a bank: business lending or mortgage lending, given RWA and capital constraints (banks target a 10% regulatory Tier 1 capital ratio). The results speak for themselves:

Despite the cheap ECB loans, and given a fixed amount of capital, banks are way more profitable raising funding from traditional sources to lend to households for house purchase purposes…

Admittedly, the exercise isn’t perfect. But the difference in net interest income and return on capital is so huge that tweaking it a little wouldn’t change much the results:

- I assume that all business lending is weighted 100%. In reality, apart from the French SME scenario, large corporates (often rated by rating agencies) benefit from lower RWA-density under a standardised method. This would actually raise the profitability of business lending through higher volume (and increased leverage), though not by much. Mortgages are weighted at 35% under that method.

- I assume that all banks use the standardised method to calculate RWAs. In reality, only small and medium-sized banks do. Large banks use the ‘internal rating based’ method, which allows them to risk-weight customers following their own internal models. Here again, most corporates can benefit from lower RWAs. But mortgages also do (RWA-density often decreases to the 10-15% range).

- Cross-selling is often higher with corporates, which desire to hedge and insure their financial or non-financial business positions. Corporates also use banks’ international payment solutions. This adds to revenues.

- Business lending is often less cost-intensive than retail lending. Retail lending indeed traditionally requires a large branch network, which is less the case when dealing with corporates (often grouped within regional corporate centres, though not always for tiny enterprises). However, retail banking is progressively moving online, providing opportunities to banks to cut costs and improve their profitability.

- The lower RWA-density on mortgages allows banks to increase lending volume and leverage. However, this also requires higher funding volumes. In turn, this should increase the rate paid on the marginal increase in funding, raising interest expense somewhat in the case of mortgages.

In the end, even if the adjustments described above reduce the profitability spread by 10 percentage points, the conclusion stands: banks are hugely incentivised to avoid business lending, facilitating misallocation of capital on a massive scale, in particular in a period of raising capital requirements… Moreover, banks also benefit from favourable RWAs for securitised products based on mortgages (CMBS, RMBS…), compounding the effects.

To tell you the truth, I wasn’t expecting such frightening results when I started writing that post… Please someone tell me that I made a mistake somewhere…

Central banks, regulators and politicians will find it hard to prop up business lending with regulations designed to prevent it.

7 responses to “Basel vs. ECB’s TLTRO: The fight”

Trackbacks / Pingbacks

- - 11 June, 2014

- - 28 August, 2014

- - 23 September, 2014

- - 20 February, 2015

- - 29 October, 2015

Leave a comment

Recent Comments

| pslebow on ‘Sovereign money’:… | |

| pslebow on A critique of Werner’s view on… | |

| Hugo Kramer on Welcome to Spontaneous Fi… | |

| Nathan on A critique of Werner’s view on… | |

| Nathan on More, more, more money endogen… |

Excellent post, only the Business lending rates strike me as somewhat too low, but this could be skewed due to volume weighted loan tenors. In order to capture liquidity costs accurately you would have to compare maturity adjusted rates somehow..

Please also consider, that most SMEs in Europe are overlevered anyway and new ventures are too risky by nature to lend to them (they need equity not debt). Given our high debt/gdp ratios and high costs of running a business (taxes, social security) it might not even be easy for banks to find creditworthy debtors. Better to lend to the guy with a strong income/wealth when he buys his 2nd or 3rd house/flat in some european capital. That’s what I am observing in Vienna at least…

Yes I was myself shocked by those low business lending rates. This is why I wanted a breakdown for SMEs.

I picked what I believe are the most appropriate ones. But central bank reporting varies a lot. Some rates are average accross all sorts of lending, some can be just unsecured, some just 1yr+ maturity, some just Eur1m+… I tried to pick the ones that represented a larger share of the volume of lending.

Nevertheless, all rates only varied by a few bp to 1.5% max. So the conclusions wouldn’t be altered much…

Also, I believe there is a selection bias in business lending rates:

– Banks now often only lend to their top customers (small and large)

– Many businesses report that banks would not lend to them at any rate or at prohibitive rates only, therefore don’t borrow and aren’t included in the stats

– Many surveys show that businesses self restrain from borrowing as they believe (rightly or wrongly) that banks would not extend credit to them anyway, and therefore aren’t included in the stats.

Yes corporates are overindebted but it is also the case of households…