The inherent contradiction of regulation exposed (again)

A few weeks ago, Reuters reported that a new research report (I can’t seem to find the original paper, which is still a work in progress) published by two German academics (Wolfgang Gick and Thilo Pausch) recommended that bank supervisors “withhold some information when they publish stress test results to prevent both bank runs and excessive risk taking by lenders”.

I have pointed out multiple times that this was an intrinsic problem to bank regulation, and that Bagehot had correctly identified the issue already in his time. Our societies have, since then, tried to conveniently forget Bagehot’s wise remarks.

Reuters continues:

If depositors know from the watchdog that banks are in trouble, they will withdraw their cash, threatening lenders’ survival and causing the panic the supervisor is trying to avoid, the paper said.

Exactly. And wholesale markets are even more at risk. The authors then recommend that “the amount of information disclosed by supervisors should decrease the more vulnerable the banking sector is expected to be.” Is this going to correct the problem? Evidently not. As the public starts to understand that ‘less information about a given bank’ equals ‘riskier bank’, withholding information from the public domain will become self-defeating.

The authors also correctly highlight that

giving banks a clean bill of health also carries risks, according to Gick and Pausch, by encouraging depositors to leave their money in banks. That would undermine market discipline and lead lenders to take excessive risks, they wrote.

In the end, whatever regulators do, negative consequences follow.

Another contradiction was exposed last month when Ewald Nowotny, Governor of the Austrian central bank, warned that proposed changes to the Basel regulatory regime were “dangerous” because borrowing “could become harder for SMEs.” He added that the revised Basel framework had “a sort of bias against bank lending”, and that “banking regulators should analyze the combined effect on the real economy of the multitude of rules that are due to come into force.”

He is both right and wrong. Wrong because the Basel rules have not been loose for corporate lending since Basel was put in place in the 1980s. It’s precisely the opposite. Rules were stricter than for many other lending types, such as real estate lending, leading to the great credit distortion we have experienced over the past couple of decades, and the slow recovery as corporations were starved of credit (see many many of my previous blog posts for details).

But he’s right that the revised Basel framework will perhaps exacerbate this situation by widening the spread between the capital cost of SME lending and that of real estate lending.

This is where the great contradiction lies. Nowotny is one of the first top regulators to underline a part of the credit allocation distortion. Yet most regulators believe that higher capital costs are justified on the basis that SME/corporate lending is inherently riskier. They never admit that the Basel framework played a major role in creating the great real estate credit bubble that led to the crisis. They constantly, and stubbornly, deny that Basel’s risk-weights could have any impact on the credit supply (and hence the sectorial interest rate). Yet, they contradict themselves when, at the same time, they consider lowering those same risk-weights on a number of products (such as securitisations) to boost…their supply and demand!

Let me get this straight: risk-weights are an instance of price control (in this case, capital cost control). And economic theory clearly demonstrates that price controls are both inefficient and leads to economic distortions. You can’t stabilise the financial system using price control tools, and then blame financial institutions and economic agents for rationally reacting to your measures. You just can’t.

Update: I originally used the term ‘price-fixing’ above. I then thought ‘price control’ was more appropriate, so I modified the post.

Natural interest rates are dead, the BIS (indirectly) says

In May (I only found out a couple of weeks ago), the BIS released a big report titled Regulatory change and monetary policy, in which it investigates the effects of the new banking regulatory framework on market interest rates and the implied consequences for the conduct of monetary policy. By the BIS’ own admission, the whole yield curve has nothing ‘natural’ left.

The report is an interesting, though pretty technical read. It is also scary. Scary to see how much banking regulation is affecting interest rates all along the yield curve across most banking products. Scary to see that the suggested remediation by the BIS is more central bank involvement to counteract the effects of those regulations.

Of course, the Basel framework originates from… Basel in Switzerland, where the BIS is located, and where BIS experts have spent years drafting apparently clever rules to make our banking system apparently safer, in spite of all historical evidences and what we’ve learned about the spontaneous order of free markets (remember: “banking is different” they say). So I wasn’t expecting this BIS report to declare that the very rules it put in place was endangering the economy. And indeed it doesn’t. But it does admit that there will be ‘impacts’, which of course will be ‘limited’ and ‘manageable’. They always are.

I won’t replicate here everything that’s in that report. It’s way too long and I’ll let you take a look at it if you’re interested. There is a quite detailed description of the potential effects of the Liquidity Coverage Ratio, the Net Stable Funding Ratio, the Leverage Ratio and the Large Exposure Limits on banks’ product pricing and volume and the impact on central bank’s monetary policy operations. And despite its 30+ pages, the report isn’t even comprehensive. It forgets to look at the large distortive effects of risk-weighted assets and credit conversation factors.

What I’m going to show you below is merely the BIS researchers’ own conclusions, which they neatly summarised in handy tables. This is what they view as the potential changes in money market interest rates:

By their own admission, the cumulative effect of those new rules is unclear. And even when they believe they know which way the interest rate will move, it remains a best guess. To this table you can add the hugely distortive effects of RWAs and CCFs, which I have described on this blog a number of times.

The only conclusion is that there is no free market-defined Wicksellian ‘natural’ interest rate anymore in the marketplace. As interest rates are manipulated by regulatory measures in myriads of ways, entire yield curves across the whole spectrum of banking products and asset classes stop reflecting the pricings that market actors would normally agree on in an unhampered market. The result is a large shift in the structure of relative prices in the economy.

The economic consequences are likely to be damaging (and it is clear, at least to me, that RWAs have already done a lot of damages, i.e. the financial crisis), even though the BIS reckons that central banks could potentially offset some of those interest rates movements:

More central bank intermediation: Many of the new regulations will increase the tendency of banks to take recourse to the central bank as an intermediary in financial markets – a trend that the central bank can either accommodate or resist. Weakened incentives for arbitrage and greater difficulty of forecasting the level of reserve balances, for example, may lead central banks to decide to interact with a wider set of counterparties or in a wider set of markets.

In addition, in a number of instances, the regulations treat transactions with the central bank more favourably than those with private counterparties. For example, Liquidity Coverage Ratio rollover rates on a maturing loan from a central bank, depending on the collateral provided, can be much higher than those for loans from private counterparties.

Problem is (and the BIS also admits it): there is no way non-omniscient central bankers know by how much and in what direction rates should be offset. We here get back again to the knowledge problem. There is no way the central bank can act in a timely manner. It is also unlikely that central bankers could act free from any political interference. Finally, even if central banks managed to figure out what the ‘natural’ rate is for a given asset at a given maturity, central banks’ policies are likely to have unintended consequences by altering the rates of other products and maturities.

The effectiveness of the transmission mechanism (banking channel) of monetary policy is more than ever questioned. Rates will move in unexpected ways. And, as the BIS describes, banks could simply opt out of monetary programmes altogether:

The question is whether there are exceptional situations in which banks would refrain from subscribing to fund-supplying operations because concerns over the LR impact of the reserves that would be added to the banking system in aggregate outweigh the financial benefits accrued by participating in the operations. If so, this lack of participation could prevent a central bank whose operating framework entailed increasing the quantity of reserves from meeting its operating target.

The BIS believes that “the changing regulatory environment will, by design, affect banks’ relative demand across various types of assets and liabilities”. It summarises the potential changes in the demand for central bank tools below:

Here again, a lot of uncertainties remain.

Something looks certain however. The involvement of central banks in the financial and economic system is likely to become more intense. As regulations bound banks’ behaviour and prevent an effective allocation of capital, central banks are increasingly going to step in to boost or restrict the supply of credit to certain market actors and asset classes. See what happened with SMEs, starved of credit as Basel makes it too expensive to extend credit to such customers, while central banks attempted to offset this effect by starting specific lending programmes (such as the Funding for Lending scheme in the UK). We are here again back to Jeff Hummel’s arguments of the central bank as central planner.

Nonetheless, I am certain that capitalism and free markets will get blamed for the next round of crisis. It is becoming urgent that we replicate the achievement of academics such as Friedman and Hayek, who managed to overturn the nonsense post-War Keynesian consensus. Sadly, free markets academics seem to have virtually disappeared nowadays or at least cut off from most policymaking positions and public debate.

Financial knowledge dispersion and banking regulation

I have never hidden my admiration for Hayek’s work, in particular over the last few weeks. The name of this blog is itself derived from Hayek’s concept of spontaneous order. I view Mises as having laid the foundations of a lot of Hayek’s and modern Public Choice theory thinking (see Buchanan’s admission that Mises “had come closer to saying what I was trying to say than anybody else”). He was to me a more comprehensive theorist than Hayek, and made us understand through his methodological individualism method that human action was at the heart of economic behaviour. But Hayek’s brilliant contribution is to have built on Mises’ business cycle, market process and entrepreneurship insights to develop a coherent and deep philosophical, legal, political and economic paradigm. While some would argue that he didn’t push his logic far enough (see here or here), it remains that reading the whole body of Hayek’s work is truly fascinating and enlightening. It suddenly feels like everything is connected and that “it now all makes sense”.

Some of Hayek’s insights are verified on a day-to-day basis. He repeatedly emphasised that knowledge was dispersed throughout the economy and that no central authority could ever be aware of all the ‘particular circumstances of time and place’ in real time. This knowledge problem was core to his spontaneous order theory, which describes how market actors set up plans independently of each other according to their needs and coordinated through the price system and respect for the ‘meta-legal’ rules (what he later called ‘rules of just conduct’) of the rule of law.

I have very recently offered a critique of macro-prudential regulation based on Hayek’s and Public Choice’s insights. But his description of the knowledge problem also applies. Zach Fox, on SNL (link gated), reports that the whole of macro-prudential regulatory framework may be useless because the US agency in charge of tracking the data can only access outdated, if not completely wrong, datasets. This agency calculates ‘systemic risk’ scores from a number of data points sent by various banks. Problem: those figures keep being revised by many banks, sometimes radically, leading to large fluctuations in ‘systemic risk’ scores and regulators keep using outdated data:

SNL has only been able to track the movements by scraping each bank’s individual filing periodically over the last year. U.S. banks filed their 2013 systemic risk reports by July 2014, at which point SNL reported on the data. After noticing some differences, SNL followed up Jan. 13, 2015. In total, 12 data points had changed across the filings for eight different banks. Then, in July 2015, SNL noticed yet more revisions to the 2013 filings.

Fox concludes:

When a bank’s derivative exposure shrinks by $314 billion — roughly half the size of Lehman when it filed bankruptcy — it raises questions about the company’s ability to model accurately in real-time. When that change does not come until 16 months after the initial filing, it raises questions about the Fed’s vigilance. And when the government’s office established to track systemic risk uses incorrect, outdated data, it raises questions about the entire theory of macroprudential supervision.

(one could add: “and of micro-prudential supervision”)

In short, due to dispersed nature of financial knowledge (i.e. data) across the whole banking sector and the inherently bureaucratic nature of the data collection and analysis process, regulatory agencies do not have ability to collect accurate data in a timely manner, and hence act when really necessary.

Of course, some banks also seem to struggle to report the required data. But they are much closer to their own ‘particular circumstances of time and place’ and hence can take action way before the data even reach the regulator. Moreover, banks are organisations that comprise several layers of individuals, each of them facing their own particular circumstances. Knowledge is dispersed among bankers who deal with clients on a daily basis and goes up the hierarchical chain if and when necessary. Governmental agencies are at the very end of this chain and informed last, way after the actions have taken place (or the disaster occurred).

Of course, this does not mean that commercial banks are always effective in dealing with data and that all their decisions are taken rationally. But a central regulatory agency would not have the ability to make the bank safer either. Forcing banks to adopt certain standards in advance could help solve the problem to an extent only, as circumstances vary and standards may not be appropriate for all situations or could even exacerbate problems as I keep emphasising on this blog (and are likely to be a harmful and unnecessary drag on economic performance).

PS: The Chinese central bank is about to cut reserve requirements to boost lending according to the WSJ. Clearly China hasn’t been infected by the MMT/endogenous money virus yet.

PPS: Kinda related to this post, but definitely related to this blog, see this Hayek’s quote of the day:

Above all, however, I am bound to stress that in the course of the work on this book I have been, by the confluence of political and economic considerations, led to the firm conviction that a free economic system will never again work satisfactorily and we shall never remove its most serious defects or stop the steady growth of government, unless the monopoly of the issue of money is taken from government. I have found it necessary to develop this argument in a separate book, indeed I fear now that all the safeguards against oppression and other abuses of governmental power which the restructuring of government on the lines suggested in this volume are intended to achieve, would be of little help unless at the same time the control of government over the supply of money is removed. Since I am convinced that there are now no longer any rigid rules possible which would secure a supply of money by government by which at the same time the legitimate demands for money are satisfied and the value of that money kept stable, there appears to me to exist no other way of achieving this than to replace the present national moneys by competing different moneys offered by private enterprise, from which the public would be free to choose which serves best for their transactions.

It comes from the chapter 18 of Law, Legislation and Liberty (which I have now read), and highlights a significant evolution in Hayek’s thinking since The Constitution of Liberty, in which he had argued in favour of government managing the money supply (but should do it well of course).

Macro-pru, regulation, rule of law and public choice theory

Another rule of law-related post. It might be the anniversary of the Magna Carta that brought this topic back in fashion. Consider it as a follow-up post to my Hayekian legal principles post of a couple of weeks ago.

John Cochrane has a very long post on the rule of law on his blog (which could have been an academic article as the pdf version is 18-page long) titled The Rule of Law in the Regulatory State.

His vision is a little gloomy, but spot on I believe:

This rule of law always has been in danger. But today, the danger is not the tyranny of kings, which motivated the Magna Carta. It is not the tyranny of the majority, which motivated the bill of rights. The threat to freedom and rule of law today comes from the regulatory state. The power of the regulatory state has grown tremendously, and without many of the checks and balances of actual law. We can await ever greater expansion of its political misuse, or we recognize the danger ahead of time and build those checks and balances now.

He believes the rise of the regulatory state does not fit the standard definitions of socialism, regulatory capture or crony capitalism. He believes that we are

headed for an economic system in which many industries have a handful of large, cartelized businesses— think 6 big banks, 5 big health insurance companies, 4 big energy companies, and so on. Sure, they are protected from competition. But the price of protection is that the businesses support the regulator and administration politically, and does their bidding. If the government wants them to hire, or build factory in unprofitable place, they do it. The benefit of cooperation is a good living and a quiet life. The cost of stepping out of line is personal and business ruin, meted out frequently. That’s neither capture nor cronyism.

He thinks the term ‘bureaucratic tyranny’ could be appropriate to describe the situation, and that it is the ‘greatest danger’ to our political freedom. That is, opposing or speaking out against a regulatory agency, a politician or a bureaucrat might prevent you from obtaining the required regulatory approval to run your business.

He takes what seems to be a Public Choice view when he states that “the regulatory state is an ideal tool for the entrenchment of political power was surely not missed by its architects.”

While his post covers all sorts of industries, and while his definition of the rule of law (and its difference with mere legality) isn’t as comprehensive as Hayek’s, it remains pretty interesting. He actually has a lot to say on the current state of banking and financial regulation:

The result [of Dodd-Frank] is immense discretion, both by accident and by design. There is no way one can just read the regulations and know which activities are allowed. Each big bank now has dozens to hundreds of regulators permanently embedded at that bank. The regulators must give their ok on every major decision of the banks.

While he says that, for now, Fed staff involved in bank stress tests are mostly honest people, he is wondering how long it will take before the Fed (pushed by politicians or not) stop resisting the temptation to punish particular banks by designing stress tests (whose methodology is undisclosed) to exploit their weaknesses.

While Cochrane laments the rise of discretionary ruling and its consequences on freedom, The Economist also just published a warning, albeit a less-than-passionate one. Since the crisis, The Economist has always taken a somewhat ambivalent, if not completely contradictory double-stance (for instance, it takes position against rules in monetary policy in the same weekly issue). Here again, the newspaper believes that the crisis made new rules ‘inevitable’, because taxpayers ‘need protection from the risks of failure’. And that, as a result, regulators needed ‘flexible’ rules (MC Klein made a similar point some time ago – see my rebuttal here).

By and large, The Economist has approved that sort of rulemaking, as well as the use of macro-prudential policies (something I have regularly criticised on this blog). Nevertheless, the newspaper also complains about abuse of discretionary decision-making and the effect of regulatory regime uncertainty (a term originally coined by Robert Higgs). It doesn’t seem to have realised that the nature of what it was requesting (i.e. respect of the rule of law and control of the industry and of the monetary system by regulatory agencies) was by nature antithetical. Cochrane’s fears (as well as mine) thus seem justified if such a classical liberal newspaper cannot even realise this simple fact.

Public Choice theory could be used as a strong rebuttal to the regulatory discretion rationale. As Salter points out in a remarkable paper titled The Imprudence of Macroprudential Policy, the economic and political science behind discretionary macro-pru policies taken by bureaucratic agencies suffers from major flaws that regulators or academics haven’t even tried to address.

He highlights the fact that, as Mises and Hayek had already mentioned decades ago during the socialist calculation debate, regulatory agencies lack the information signalling system to figure out what the ‘right’ market price should be and hence act in the dark, possibly making the situation even worse* (and empirical evidences do show that it doesn’t work), and that the assumption of the macro-pru literature that capitalist (and financial) systems are inherently unstable is at best unproven. A typical example is Basel’s capital requirements: as I have long argued on this blog, RWAs incentivise the allocation of credit towards asset classes that regulators deem safe. The fact that they are aware of the allocative power that they have is clearly illustrated by the recent news that EU regulators would lower capital requirements on asset-backed securities to persuade insurance firms to invest in them! Yet they continue to blame banks for over-lending for real estate purposes and not enough ‘to the real economy’. Go figure.

Worse, Salter continues, macro-pru regulation (and his critique also applies to all other regulatory agencies) assumes away all Public Choice-related issues, taking for granted omniscient regulators always acting in the ‘public interest’. Yet proponents of strong regulatory agencies seem to ignore (voluntarily or not – rather voluntarily if we believe Cochrane) that regulatory agencies themselves can fall prey to the private interests of regulators, whether those are power, money, job… If not directly to the regulators, regulatory agencies can fall prey to voters’ irrationality, as Caplan would argue (but also Mises and Bastiat), leading elected politicians to put in place regulators executing the irrational wishes of the voters. The resulting naïve line of thought of the macro-pru and regulatory oversight school is dangerous and goes against the body of knowledge that Western civilization has accumulated since the Enlightenment period.

And such occurrences are not only present in the minds of Public Choice theorists. They are happening now. The case of the head of the British Financial Conduct Authority directly comes to mind: whether or not one agreed with his “shoot first, ask questions later” method (and many didn’t), he was removed from office by the new UK government as he didn’t fit in the new political ‘strategy’.

What can we do? Cochrane proposes a Magna Carta for the regulatory state, in order to introduce the checks and balances that are currently lacking in our system (for instance, appeals are often made with the same regulatory agency that took the decision in the first place). Buchanan would certainly argue for a similar constitutional solution that would attempt a return to the ‘meta-legal’ principles of the rule of law described by Hayek, with an independent judiciary as the main arbitrator.

The wider public certainly isn’t ready to accept such changes given its negative opinion of particular industries (they’d rather see more regulatory oversight). Consequently, the only way to convince them that constitutional constraints on regulatory agencies are necessary seems to me to remind them that regulatory discretion negatively affects them as well (and day-to-day examples of incomprehensible regulatory decisions abound). If broad principles can be agreed upon from the day-to-day experience of millions of people, they should apply more broadly to all types of sectors. As Salter concludes for macro-prudential policies (although it applies to any regulatory agency):

Market stability is ultimately to be found in institutions, not interventions. Institutions that are robust to information and incentive imperfections must be at the heart of the search for stable and well-functioning markets. Robust monetary institutions themselves depend on adherence to the rule of law and the protection of private property rights, which are the cornerstone of any well-functioning market order. Since macroprudential policy relies on unjustifiably heroic assumptions concerning the information and incentives facing private and public agents, its solutions are fragile by construction.

*Cowen and Tabarrok take another angle here by arguing that the problem of ‘asymmetric information’, which underlies most regulatory thinking, almost no longer exists in the information/internet age.

Hayekian legal principles and banking structure

The latest CATO journal contains a truly fascinating article (at least to me) of George Selgin titled Law, Legislation, and the Gold Standard. Selgin roots his arguments in Hayekian legal theory, as developed by Hayek in his books The Constitution of Liberty and Law, Legislation and Liberty*.

Hayek differentiates ‘law’ (that is, general backward-looking ‘meta-legal’ rules that follow the principle of the rule of law) from forward-looking ‘legislation’, which is unfortunately too often described as ‘law’ despite not respecting the very fundamentals of the rule of law. As such, Hayek describes the rule of law as being

a doctrine concerning what the law ought to be, concerning the general attributes that particular laws should possess. This is important because today the conception of the rule of law is sometimes confused with the requirement of mere legality in all government action. The rule of law, of course, presupposes complete legality, but this is not enough: if a law gave the government unlimited power to act as it pleased, all its actions would be legal, but it would certainly not be under the rule of law. The rule of law, therefore, is also more than constitutionalism: it requires that all laws conform to certain principles.

Therefore, the rule of law, according to Hayek, relies on general ‘meta-legal’ rules that have progressively, spontaneously, if not tacitly, been discovered and evolved in a given society to facilitate social interactions and exchanges between individuals (“a government of law and not of men”). Those custom-based rules have certain attributes, namely that they be “known and certain”, apply equally to everyone, define a clear limit to the coercive power of government, require the separation of power and finally only allow the judiciary to exert discretionary rulemaking (within the boundaries of those meta-legal rules). Hayek explains that “under a reign of freedom the free sphere of the individual includes all action not explicitly restricted by a general law.”

Within this framework, Selgin describes the appearance of the gold standard as following the generic principle described by Hayek:

The difference between private or customary law and public law or legislation is, I submit, one of great importance for a proper understanding of the gold standard’s success. For, despite both appearances to the contrary and conventional wisdom, that success depended crucially upon the gold standard’s having been upheld by customary law rather than by legislation. It follows that any scheme for recreating a durable gold standard by means of legislation calling for the Federal Reserve or other public monetary authorities to stand ready to convert their own paper notes into fixed quantities of gold cannot be expected to succeed.

According to him, the gold standard and its definition was mostly a spontaneous monetary arrangement rooted in private commercial customs, and enforced through the private law of contracts. He sums up:

In short, countries abided by the rules of the gold standard game because that game was played by private citizens and firms, not by governments.

Consequently, a gold standard put in place and enforced by governments is unlikely to work. He continues:

Although it may seem paradoxical, our understanding of the classical gold standard suggests that, if that standard had been deliberately set up by governments to enhance their borrowing ability, it is unlikely that it would have worked as intended. This conclusion follows because, once public (or quasi-public) authorities, governed by statute law rather than the private law of contracts, become responsible for enforcing the rules of the gold standard game, the convertibility commitments crucial to that standard’s survival cease to be credible.

He, as a result, doubts about the ability of the gold standard to be ‘forced’ to return through government policy, and demonstrates that post-WW1 attempts to reinstate the gold standard were doomed from the start as states “tragically misunderstood the true legal foundations” of the famous 19th century monetary arrangement. But Selgin also believes that a ‘spontaneous’ return to gold would be unlikely because the public has been ‘locked-into’ a fiat money standard, and that customary law tends to reinforce that trend – by legitimizing the practice over time – rather than providing a way out. Moreover, he concludes, if a new commodity-like standard were to emerge, nothing guarantees that it wouldn’t be based on another sort of medium (including synthetic commodities such as cryptocurrencies).

Now that I have explained the basics of Selgin’s reasoning, I will try to understand what it involves for banking structure and regulation. While free banking systems, such as Scotland’s, have arguably spontaneously evolved following a custom-based legal framework, the structure of the whole of today’s financial system comprises barely anything ‘natural’ left, as Bagehot would point out. Banking, as we know it, is a pure product of decades, if not centuries, of accumulating layers of positive legislation and government discretionary policies. In short, there is now little overlap between banking and the rule of law**.

The inherent instability of banking systems regulated by statute-based law, as opposed to the relative stability of free banking systems (which Larry White referred to as ‘anti-fragile banking and monetary systems’), is therefore unsurprising seen through Hayek’s and Selgin’s lens: governments, even with the best of all possible intentions, could simply not come up with a banking arrangement that could outperform decades or centuries of experience and decentralised knowledge gains that were reflected in rule of law-compliant free banking. Their attempt at centralising and harmonising the “particular circumstances of time and place” were self-defeating.

But the question isn’t what’s wrong about today’s financial system, but can we do anything about it? Can we get back to a rather ‘pure’, rule of law-compliant, free banking system? And my answer is, unfortunately, rather Bagehotian: despite how much I wish to witness the re-emergence of a financial structure based on laissez-faire principles, I believe it’s unlikely to happen… (but wait, there’s a new hope)

Why? For the very reason mentioned by Selgin: regulations have shaped the financial structure for such a long time that innovations and practices have been established that seem now unlikely to disappear. Let me give two examples:

- Money market funds were originally created to bypass the US regulation Q, which has since then been abolished. But MMF are still major financial players and unlikely to disappear any time soon. They have become an established part of the financial structure.

- Mathematical model-based risk frameworks, which existed before the introduction of Basel regulations but were not as widespread, and certainly not as uniform. Basel rules and domestic regulators required common standards that are now used both by analysts and commentators as data, and by bankers for internal risk, capital and liquidity management purposes, despite their limitations and the distortion they insert into the decision-making process. Abolishing Basel and its local implementations (such as CRD4 or Dodd-Frank) are unlikely to remove what is now accepted as market practice. However, less uniformisation in models and uses are likely to appear over time.

What about the very basic component of our modern banking system, the main beneficiary of statutory law, namely the central bank? Bagehot declared that “we are so accustomed to a system of banking, dependent for its cardinal function on a single bank, that we can hardly conceive of any other”, and opposed a radical transformation of the system which, unfortunately, was there to stay. Yet I believe the probability of getting rid of central banks without causing too much disruption is higher than what Bagehot believed. There are a number of countries that do not rely on any central bank, use foreign currencies as medium of exchange, and seem to do perfectly fine (such as Panama). This seems to show that market practices and relationships with central banks aren’t that entrenched and other models currently do exist, and which could spread relatively quickly.

But what is, in my view, our best hope of getting back to a financial system that follows Hayekian legal principles is Fintech. While Fintech firms have to comply with a number of statute-based laws, they nevertheless remain relatively free (for now) of the all intrusive banking rulebooks and discretionary power of regulators. As such, the multiple IT-enabled Fintech firms and decentralised technologies offer us the best hope of reshaping the financial system in a rule of law-based, spontaneously-emerging, manner. Of course, there will be bumps along the road and some business models will fail and other succeed, but this learning process through trial and error is key in shaping a sustainable system along Hayekian decentralised and experience-based principles. For the sake of our future, let’s refrain from the temptation of legislating and regulating at the first bump.

*At the time of my writing, I have only read the first one, although the second one is next on my reading list

**Although I am not an expert, the evolution of accounting standards over time seems to me to have mostly happened along rule of law principles (although Gordon Kerr, and Kevin Dowd and Martin Hutchinson, would perhaps argue otherwise, which is understandable as IFRS comes from statute-based law systems).

Update: See this follow-up post, which includes some Public Choice theory insights

Photo: Bauman Rare Books

The Economist’s flawed logic

The Economist this week accused global banks of being “badly managed and unrewarding” (also see its second, more comprehensive article here). It is true that banks have been hit by the crisis and the following regulatory outburst. But the logic underpinning the two articles of the newspaper in this week’s edition is badly flawed and only seems to demonstrate the paper’s bias against banks.

The newspaper admits that

on paper global banks make sense. They provide the plumbing that allows multinationals to move cash, manage risk and finance trade around the world. Since the modern era of globalisation began in the mid-1990s, many banks have found the idea of spanning the world deeply alluring.

Indeed. Global banks evolved from a need: the need to maintain a single (or just a few) banking relationship throughout the world. Globalisation of trade and capital flows inherently implies the globalisation of banking. The current de-globalisation trend that we witness among Western banks is dangerous as this will not help corporations grow their business and hence generate growth.

However, the Economist’s bias appears in that it does not distinguish between banks that are truly global and the rest, and between banks that suffered from the crisis, and the rest. Comparing HSBC, Standard Chartered and Citi with the likes of RBS or Societe Generale doesn’t make much sense. Some have a truly global presence in both retail and investment banking operations, while others only have representative offices or limited product ranges. They do not have the same business models and, despite this, all struggle to generate meaningful RoEs. Moreover, tiny to medium-sized domestic banks also struggle to generate RoEs that cover their cost of capital. Accusing global banks of underperformance thus makes no sense. Identifying some banks that perform relatively well because they focus on regulatory-advantaged businesses such as mortgage lending is irrelevant.

The Economist also targets both banks that needed bailouts and others that did survive the crisis with limited damages. That bailouts mostly involved banks that were not global and that some global banks indeed were saved by their diversified operations doesn’t seem to have rung a bell at the newspaper.

This is unfortunate, as The Economist does acknowledge the impact of regulatory changes:

The wave of regulation since the financial crisis is partly to blame. Regulators rightly decided not to break up global banks after the financial crisis in 2007-08 even though Citi and RBS needed a full-scale bail-out. Break-ups would have greatly multiplied the number of too-big-to-fail banks to keep an eye on. Instead, therefore, supervisors regulated them more tightly—together JPMorgan Chase, Citi, Deutsche and HSBC carry 92% more capital than they did in 2007. Global banks will probably end up having to carry about a third more capital than their domestic-only peers because, if they fail, the fallout would be so great. National regulators want banks’ local operations to be ring-fenced, undoing efficiency gains. The cost of sticking to all the new rules is vast. HSBC spent $2.4 billion on compliance in 2014, up by about half compared with a year earlier. A discussion of capital requirements in Citi’s latest regulatory filing takes up 17 riveting pages.

Indeed. Though regulation isn’t ‘partly’ to blame. It is the primary factor (along with low interest rates) driving the underperformance of banks of all sizes and shapes. The Economist itself several times attacked current regulatory reforms as being unnecessarily costly (see here and here). It now seems to have forgotten and ‘mismanagement’ has become to culprit. For any other industry, The Economist would have blamed regulatory overreach for the industry’s poor performance, in turn pleading for growth-liberating liberalisation. But not for banking. The Economist still hasn’t come to terms with the fact that banks were not the origin, but only the tool, that led to the financial crisis, and as a result remains a ‘classical liberal’ newspaper only when it wants to.

Crush RWAs to end secular stagnation?

Some BIS researchers very recently published this piece of research demonstrating that the growth of the financial sector was linked to lower productivity in the economy. MCK in FT Alphaville commented on it and reached the wrong conclusion (the title of his post is ‘Crush the financial sector, end the great stagnation?’, though he could be forgiven given that the BIS paper itself is titled ‘Why does financial sector growth crowd out real economic growth?’).

I have attempted in previous posts to explain why Basel risk-weighted assets (RWAs) were the root cause of the misallocation of bank credit and hence the misallocation of capital in the economy prior to the financial crisis: in order to optimise return on equity, bankers were incentivised by RWAs to allocate a growing share of available loanable funds to the real estate sector, creating an unsustainable boom. I also speculated that, consequently, fewer financial resources were hence available for sectors that were penalised by regulatory-defined high RWAs (i.e. business lending), and that this could be one of the main causes of the so-called ‘secular stagnation’.

I have also regularly criticized governments’ and central banks’ schemes such as FLS and TLTRO when they were announced, as they could simply not address the fundamental problem that Basel had introduced a few decades earlier.

I have recently pointed out that new studies seem to highlight that, indeed, real estate lending had overtaken business lending for the first time in the past 150 years exactly after Basel 1 was put in place at the end of the 1980s, and that the growth of business lending had been lower since then. (Same chart again. Yes it is that important)

This new BIS study is remarkably linked, although its authors don’t seem to have noticed. This is what they conclude:

In our model, we first show how an exogenous increase in financial sector growth can reduce total factor productivity growth. This is a consequence of the fact that financial sector growth benefits disproportionately high collateral/low productivity projects. This mechanism reflects the fact that periods of high financial sector growth often coincide with the strong development in sectors like construction, where returns on projects are relatively easy to pledge as collateral but productivity (growth) is relatively low. […]

First, at the aggregate level, financial sector growth is negatively correlated with total factor productivity growth. Second, this negative correlation arises both because financial sector growth disproportionately benefits to low productivity/high collateral sectors and because there is an externality that creates a possible misallocation of skilled labour.

Replace some of the terms above with RWAs and you get the right picture. What those researchers miss is that the growth of the financial sector has been similar in previous periods over the past 150 years, with no decline in secular growth rate and productivity. However, what changed since the 1980s is the allocation of this growth. And the dataset this BIS piece examines only starts…in 1980. Their conclusion that high collateral industries would attract a higher share of lending is also coherent with my views, as higher lending collateralisation reduces the required capital buffer than banks need to maintain.

MCK is right when he declares that

the growth of the financial sector has been concentrated in mortgage lending, which means that more lending usually just leads to more building. That’s a problem for aggregate productivity, since the construction industry is one of the few that has consistently gotten less productive over time. For example, Spain had no productivity growth between 1998 and 2007, a period when 20 per cent of all the net job growth can be attributed to the building sector.

But his conclusion that regulation needs to force the banking industry to get smaller is off the mark. Getting rid of the incentives created by RWAs, and the resulting unproductive misallocations, is what is needed.

Easy money is secondary to bank regulation in triggering housing booms

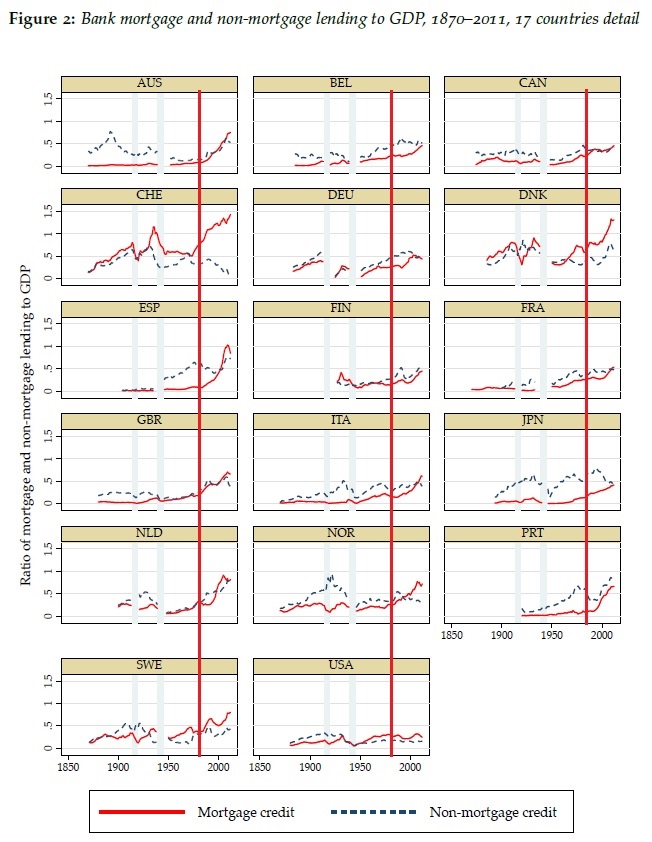

I’ve already reported on the excellent piece of research that Jordà et al published last year. Last month, they elaborated on their previous research to publish another good paper, titled Betting the House. While their previous paper focused on gathering and aggregating real estate and business lending data across most major economies since the second half of the 19th century, their new paper built on this great database to try to extract correlations between ‘easy’ monetary conditions and housing bubbles.

Remember their remarkable chart, to which I had added Basel and trend lines:

They also produced the following chart, which shows disaggregated data across countries (click on it to zoom in). I added red vertical bars that show the introduction of Basel 1 regulations (roughly… it’s not very precise). What’s striking is that, almost everywhere, mortgage debt boomed as a share of GDP and overtook business lending. It was a simultaneous paradigm change that can hardly be separated from the major changes in banking regulation and supervision that occurred at that time.

Their new study repeats most of what had been said in their previous one (i.e. that mortgage credit had been the primary driver of post-WW2 bank lending) and then compares real estate lending cycles with monetary policy. And they conclude that:

Their new study repeats most of what had been said in their previous one (i.e. that mortgage credit had been the primary driver of post-WW2 bank lending) and then compares real estate lending cycles with monetary policy. And they conclude that:

loose monetary conditions lead to booms in real estate lending and house prices bubbles; these, in turn, materially heighten the risk of financial crises. Both effects have become stronger in the postwar era.

As I said in my post on Jordà et al’s previous research, most (if not all) of what they identify as post-WW2 housing cycles actually happened post-Basel implementation. I wish they had differentiated pre- and post-Basel cycles.

They start by assessing the stance of monetary policy in the Eurozone over the past 15 years, using the Taylor rule as an indicator of easy/tight monetary policy. While the Taylor rule is possibly not fully adequate to measure the natural rate of interest, it remains better than the simplistic reasoning that low rates equal ‘easy’ money and high rates equal ‘tight’ money. According to their Taylor rule calculation, the stance of monetary policy in the Eurozone before the crisis was too tight in Germany and too loose in Ireland and Spain. In turn they say, this correlated well with booms in mortgage lending and house prices (see chart below).

At first sight, this seems to confirm the insight provided by the Austrian business cycle theory: Spain and Ireland benefited from interest rates that were lower than their domestic natural rates, launching a boom/bust cycle driven by the housing market. (While Germany was the ‘sick’ man of Europe as the ECB policy was too tight in its case)

At first sight, this seems to confirm the insight provided by the Austrian business cycle theory: Spain and Ireland benefited from interest rates that were lower than their domestic natural rates, launching a boom/bust cycle driven by the housing market. (While Germany was the ‘sick’ man of Europe as the ECB policy was too tight in its case)

And while this is probably right, this is far from being the whole story. In fact, I would say that ‘easy’ monetary policy is only secondary to banking regulation in causing financial crises through real estate booms. As I have attempted to describe a little more technically here, Basel reorganised the allocation of loanable funds towards real estate, at the expense of business lending. This effectively lowered the market rate of interest on real estate lending below its natural rate, triggering the unsustainable housing cycle, and preventing a number of corporations to access funds to grow their business. By itself, Basel causes the discoordination in the market for loanable funds: usage of the newly extended credit does not reflect the real intertemporal preference of the population. No need for any central bank action.

What ‘easy’ monetary policy does is to amplify the downward movement of interest rates, boosting real estate lending further. But it is not the initial cause. In a world without Basel rules, the real estate boom would certainly have occurred in those proportions, and quick lending growth would have been witnessed across sectors and asset classes. The disproportion between real estate and business lending in the pre-crisis years suggests otherwise.

* They continue by building a model that tries to identify the stance of monetary policy throughout the more complex pre-WW2 and pre-1971 monetary arrangements. I cannot guarantee the accuracy of their model (I haven’t spent that much time on their paper) but as described above, everything changed from the 1980s onward anyway.

PS: The ‘RWA-based ABCT’ that I described above is one of the reasons why I recently wrote a post arguing that the original ABCT needed new research to be adapted to our modern financial system and be of interest to policymakers and the wider public.

EU banking dis-union

The EU wants to put in place its now famous banking union. The ECB is taking over as the single regulator of all the banks of the Eurozone (and countries that wish to participate). The rationale is that the Eurozone banking system is getting ever more integrated within the ‘single market’, hence justifying having a single ruleset and a single supervisor. But is it really?

In a recent speech, Andrew Haldane pointed out that cross-border banking claims had strongly declined since the crisis:

But a new paper by Bouvatier and Delatte (full version here) now provides some interesting disagregated data to this trend. Controlling for the impact of the economic and financial crisis on the integration of the banking system across Eurozone countries, they conclude that

the decline in banking activities observed after the crisis was due to temporary frictions in all countries outside the euro area. In contrast, the economic downturn faced by the euro area since 2008 is not sufficient to account for the massive retrenchement of international banking activities. Euro area banks have reduced their international exposure inside and outside the euro area to a similar extent. We also find that this decline is not a correction of previous overshooting but a marked disintegration.

According to their model, Eurozone banking integration is 37% below where it should be. So much for a banking union. On the other hand, they find that non-Eurozone banking systems have increased their claims on foreign countries.

This is very interesting. However, I believe two minor issues distort some of their conclusions: 1. Their sample of banks only consider 14 OECD countries. It would have been interesting to include emerging economies. 2. Their analysis stops in 2012, which is a flaw. Since then, many non-Eurozone banks have cut in their cross-border activities as complying with the increasing regulatory burden became too onerous. I actually suspect that most banks from OECD/developed countries have started to dis-integrate, whereas banks from a number of emerging economies have actually started to grow outside of their domestic borders*.

This is very interesting. However, I believe two minor issues distort some of their conclusions: 1. Their sample of banks only consider 14 OECD countries. It would have been interesting to include emerging economies. 2. Their analysis stops in 2012, which is a flaw. Since then, many non-Eurozone banks have cut in their cross-border activities as complying with the increasing regulatory burden became too onerous. I actually suspect that most banks from OECD/developed countries have started to dis-integrate, whereas banks from a number of emerging economies have actually started to grow outside of their domestic borders*.

They do not provide the reasons behind this phenomenon. However, I believe that regulatory and political pressure is the number 1 reason behind this retrenchment. In their haste to make banks safe, regulators are actually doing the exact opposite.

I have already reported on BoE research that demonstrated that global integration of banking systems led to stability of funding flows within what researchers called the ‘internal capital markets’ of banking groups (I also added several historical examples to back this research).

More and more research is produced that actually contradicts the whole current regulatory thinking. A new study by NY Fed researchers Correa, Goldberg and Rice also confirmed the importance of banking group’s internal liquidity transfers across cross-border entities:

In global banks, internal liquidity management is a consistent driver of explaining cross-sectional differences in loan growth in response to changing liquidity risk. Those banks with higher net borrowing from affiliated entities had consistently strong loan growth (domestic, foreign, cross-border, credit) when liquidity risks increased. As shown in the last column of Table 2 Panel B, these global banks with larger unused credit commitments borrow relatively more (net) from their affiliates when liquidity conditions worsen and then sustain lending to a greater degree.

Clearly, the ability of global groups to transfer liquidity and capital across borders can play the role of risk absorber when a crisis strikes. Yet national regulators are implementing new measures that have the exact opposite effect (i.e. ring-fencing and so on). Measures that, among others, result in the disintegration of banking across the Eurozone.

Consequently, regulators’ and politicians’ enthusiasm for the banking union seems a little bit misplaced. See this recent speech by Vítor Constâncio, Vice-President of the ECB:

Another important objective of Banking Union is to overcome financial fragmentation and promote financial integration. In particular, this will constitute a key task of the Single Supervisory Mechanism.

Really? This seems to me to contradict the very actions of regulators in the EU. It can only be one way Mr. Constancio, not both ways.

Then he adds something that is, I believe, a fundamental error:

There are four ways which I expect the SSM to make a difference to banking in Europe: by improving the quality of supervision; by creating a more homogeneous application of rules and standards; by improving incentives for deeper banking integration; and by strengthening the application of macro-prudential policies.

The prudential supervision of credit institutions will be implemented in a coherent and effective manner. More specifically, the Single Rule Book and a single supervisory manual will ensure that homogeneous supervisory standards are applied to credit institutions across euro area countries. This implies that common principles and parameters will be applied to banks’ use of internal models, for example. This will improve the reliability and coherence in banks’ calculation of risk-weighted assets across the Banking Union. On another front, the harmonisation in the treatment of non-performing exposures and provisioning rules will mean that investors can directly compare balance sheets across jurisdictions.

While I believe that the single resolution mechanism can indeed be beneficial (even though it looks overly complicated and it remains to be seen how it’s going to work in practice), a single regulatory treatment of all banks across economies and jurisdictions as varied as those of the EU is mistake. Here is what I said more than a year ago about the standardisation problem:

So a standardisation seems to be a good thing as data becomes comparable. Well, it is, and it isn’t. To be fair, standardisation within a country is probably a good thing, although shareholders, investors and auditors – rather than regulators – should force management to report financial data the way they deem necessary. However, it makes a lot less sense on an international basis. Why? Countries have different cultural backgrounds and legal frameworks, meaning that certain financial ratios should not be interpreted the same way from one country to another.

Let’s take a few examples. In the US, people are much more likely than Europeans on average to walk away from their home if they can’t pay off their mortgage. Most Europeans, on the other hand, will consider mortgage repayment as priority number 1. As a result, impaired mortgage ratios could well end-up higher in the US. But US banks know that and adapt their loan loss reserves in consequence. Within Europe, legal frameworks and judiciary efficiency are also key: UK banks often set aside fewer funds against mortgage losses as the legal system allows them to foreclose and sell homes relatively quickly and with minimal losses. In France on the other hand, the process is much longer with many regulatory and legal hurdles. Consequently, UK-based mortgage banks seem to have lower loan loss reserves compared with some of their continental Europe peers. Does it mean they are riskier? Not really.

Indeed, look at the World Bank’s Doing Business data. The Economist selected a few countries below, all of them from the EU:

EU countries have very disparate legal frameworks and cultural backgrounds. What Constancio is saying is that the same criteria are going to be applied to all banks across all countries above. This does not make sense. The ‘single EU market’ remains for now a multiplicity of various heterogeneous markets, with their own rules, that have merely facilitated cross-border trade and labour movement.

This is a fundamental issue with the EU. Monetary and banking union should have come last, after all other laws had been harmonised. Not first. For now, EU politicians want to force a banking union on a geographical area that has limited legal and political integration. Let alone that domestic politicians and regulators are forcing their domestic banks to focus on business within their national borders, not within the EU borders.

* Indeed, another recent paper by Claessens and van Horen (summary on VOX here) suggests that

After a continued rise until 2008, the number of foreign banks from high-income countries has started to decline, from 948 in 2008 to 814 in 2013, mostly on account of a retrenchment by crisis-affected Western European banks.

On the other hand, banks from emerging markets and developing countries continued their pre-crisis growth and further increased their presence. Currently these banks own 441 foreign banks, representing 8% of all foreign assets, a doubling of their share as of 2007. As these banks tend to invest mainly in their own geographical regions, global banking now both encompasses a larger variety of players and at the same time is more regional, with the average intraregional share increasing by some five percentage points.

I’d rather not have a fox as bank regulator

We can sometimes read stupefying things on the internet. I almost fell off my chair yesterday when I read MC Klein’s latest banking piece on FT Alphaville. He suggests that the right way to regulate banks might well be to be “crazy like a fox”…

Throughout his ‘surprising’ post, he writes things like:

While simple rules about capital and short-term debt still have tremendous appeal, there is value in having a regulatory regime that is onerous precisely because of its complexity and its unpredictability.

And

As Matt Yglesias notes, the value of having lots of pointless but annoying rules is that they distract the bank lobbyists from the really important stuff. The swap pushout was the first in what is hopefully a long line of defence. We’re tempted to say that crafty policymakers should immediately propose several new and even more annoying rules for the banks.

Fortunately, regulators have other means of harassing their adversaries, hopefully keeping them busy enough to avoid exploiting the system too much.

Andrew Haldane must be having a heart attack right now.

This goes against some of the most basic economic principles, and against the very thing that allows any business to exist and thrive in the first place: the rule of law.

Let’s start with Matt Yglesias’ post. Perhaps not surprising for someone who once wrote that Dodd-Frank was an ‘achievement’ that created a ‘safer banking system’, Yglesias again proves that he has a very low understanding of how banking works. CDS contacts have apparently become ‘custom swaps’ that are used to “bet on the potential bankruptcy of a given country or company or the failure of a new financial product.” Hedging anyone? Insurance that can protect even the most vanilla-like institutions against some specific default risks? No, this is just an evil Wall Street speculative tool. Nevermind that some CDS are traded on behalf of clients, and banks’ positions taken to offset customers’ needs. Nevermind that siloing banking activities/liquidity/capital across different entities of a same banking group actually decrease the safety of the system (see also here).

Despite this rather limited knowledge of the industry, Klein builds on Yglesias’ reasoning: any repealed rule should be replaced by many pointless ones to distract lobbyists.

Now, I am still trying to understand the logic behind constantly adding red tape for no reason rather than judging rules and bureaucracy on their actual value-added and efficiency. Here again, nevermind that countries with the least efficient and most numerous rules are the least business-friendly, and that too much red tape and regulatory uncertainty is around the top issue for most US businesses at the moment. No, banking is (apparently) different.

Let me suggest that a few years working for a bank would probably help dispel some of those myths. That, lobbyists aren’t that dumb, and that, if they attack some specific rules, it is surely that these would be harmful for the banks (and indeed, both Yglesias and Klein are plain wrong in considering this CDS rule ‘pointless’). That the 30,000-page rulebook that Dodd-Frank created might not fully facilitate banking processes and lending. That, by constantly changing the rules as Klein suggests, banks might well be tempted to move away from any risky activity that might end up being considered unlawful at some point in the future, hurting risky lending in the process (i.e. usually SME lending, as if it were not already low enough) with all the associated potential economic consequences.

Banks have been closing entire lines of business, de-globalising, preventing international payments to go through, harming international trade and economic activity. The multiplication of rules could, not only lead to resource misallocation, but also to increased management time. Management time that would be better spent on analysing and controlling the business than on bureaucratic, ‘pointless’, but dangerous (because of potential fines) rules. Unexpected consequences if you like. Still, it looks acceptable for Klein.

This is exactly why avoiding regulatory uncertainty and discretionary policies, and applying a predictable set of rules (i.e. rule of law), is so crucial in facilitating business and economic development.

As Kevin Dowd clearly illustrates in a very good recent paper:

One has to understand that the banks have no defense against this regulatory onslaught. There are so many tens or hundreds of thousands or maybe millions of rules that no one can even read them all, let alone comply with them all: even with armies of corporate lawyers to assist you, there are just too many, and they contradict each other, often at the most fundamental level. For example, the main intent of the Privacy Act was to promote privacy, but the main impact of the USA PATRIOT Act was to eviscerate it. This state of lawlessness gives ample scope for regulators to pursue their own or the government’s agendas while allowing defendants no effective legal recourse. One also has to bear in mind the extraordinary criminal penalties to which senior bank officers are exposed. Government officials can then pick and choose which rules to apply and can always find technical infringements if they look for them; they can then legally blackmail bankers without ever being held to account themselves. The result is the suspension of the rule of law and a state of affairs reminiscent of the reign of Charles I, Star Chamber and all. Any doubt about this matter must surely have been settled with the Dodd-Frank Act, which doled out extralegal powers like confetti and allows the government to do anything it wishes with the banking system.

A perfect example of this governmental lawlessness was the “Uncle Scam” settlement in October 2013 of a case against JP Morgan Chase, in which the bank agreed to pay a $13billion fine relating to some real estate investments. This was the biggest ever payout asked of a single company by the government, and it didn’t even protect the bank against the possibility of additional criminal prosecutions. What is astonishing is that some 80 percent of the banks’ RMBS had been acquired at the request of the federal government when it bought Bear Stearns and WaMu in 2008, and now the bank was being punished for having them. Leaving aside its inherent unpleasantness, this act of government plunder sets a very bad precedent: going forward, no sane bank will now buy a failing competitor without forcing it through Chapter 11. It’s one thing to face an acquired institution’s own problems, but it is quite another to face looting from the government for cooperating with the government itself.

The argument’s logic is also very weak. If rules are believed to let excessive risks “fall through the cracks”, then they should never be adopted in the first place. Why even adopting rules which we already know create systemic risks? If regulators really believe those rules will cover most (or all) risks, there is no point in planning to replace them with other rules, just for the sake of changing the rules, as the new ones are likely to be less effective. Otherwise those new, more effective, rules are the ones that should have been implemented in the first place. The whole logic of the argument just doesn’t hold*.

What about the practicality of ever changing the regulatory framework? Here again the argument fails. There aren’t hundreds of derivative settlement options and assets acceptable as collateral or as liquidity buffer. While the theory sounds nice in FT Alphaville’s columns, it is simply not possible to implement in practice.

The financial imbalances that led to our previous crisis, for a large part, originated in the most complex banking rule set devised in history, compounded by politically-incentivised housing agendas (along with misguided monetary policy and accounting rules). Klein’s (and Yglesias’) failure is to ignore this and assume that more, and tighter, rules are more effective. Moreover, regulators’ failure to foresee crises has probably been a constant throughout history. Yet, Klein backs an ever-more complex and constantly-changing regulatory framework at the discretion of those same regulators.

Calomiris and Nissim, two academics that know and understand a thing or two about banking, declared that:

We worry that regulatory uncertainty – and especially the persistent waves of political attacks on global universal banks – is taking a toll.

It is important to recognize that bank stockholders are not alone in suffering from the low stock prices that result from these attacks. The supply of bank loans, and banks’ ability to provide other crucial financial services in support of economic growth, reflect the risk-bearing capacity of banks, which is directly related to market valuations of bank franchises. If banks’ earnings get little respect from the market, banks’ abilities to help the economy grow will be commensurately hobbled.

Even The Economist, which has been a supporter of banking regulatory reform over the past few years, is against regulatory discretion and is well-aware of regulators’ weaknesses (emphasis mine):

Attracting the capital that will make banking safer will be hard, with profit forecasts so anaemic. However it will also be made unnecessarily difficult by capricious behaviour from the very watchdogs who are ordering banks to raise the funds.

One problem is the endless tinkering with the rules. For all Mr Carney’s talk of finishing the job, global regulators have yet to set the minimum level for several of their new capital requirements. National regulators are just as bad. No bank can be certain how much capital it will need in a few years’ time. Pension funds and insurance companies rightly fret that even a tiny tweak in any of the new regulatory tests is enough to send a bank’s share price plummeting (or, less often, rocketing). […]

Banks can hardly be surprised that regulators have rewritten the rule-book and then thrown it at them. But, for the health of the system, the rules need to be predictable, transparent and consistent. Incredibly, the regulations emanating from America’s Dodd-Frank financial reforms are still being written, more than four years after the law was passed. Europe is scarcely better. Impose demanding capital rules, but stop adding more red tape: that should be the mantra of bank regulators just about everywhere.

The worst is: Klein does identify some of the problems with our current regulatory regime, which is easily gameable because of its complexity. In terms of regulation and forecasting, simple rules and models have always performed better (see some of the links above). But instead of stepping back and getting back to simpler, less distortive, rules, his policy of choice seems to be more bank-bashing, never-ending regulatory regime uncertainty, more complexity, the possible paralysis of bank lending and the build-up of risk within the more opaque shadow banking system. I guess it’s going to be a real success.

* He could reply that the very purpose of ‘pointless’ rules is that they have no real impact on anything. Let me clarify something: all rules have an impact, whether it is small, big, negative, positive, or both (and again, the CDS rule was far from pointless). He could also reply that changing the rules limit the gameability of the system. But this makes little sense, as ‘pointless’ rules changes would probably not prevent the accumulation of risk anyway and, even for ‘non-pointless’ rules, there are only a few available options as described above (changing capital requirements by 1% up or down, including or excluding A+ rated bonds as LCR-compliant, increasing/decreasing haircut requirements by 5%, and so forth, really would have very little impact on gameability or stability).

Recent Comments