Dampening crises: cross-border lending and risk-weights

I’ve been reviewing tons of academic papers recently, hence why you see me posting a lot of research reviews. I’ll have a specific post on macro-prudential policy next week hopefully, but today I wish to briefly mention an interesting October 2015 paper from Philippe Bacchetta and Ouarda Merrouche: Countercyclical Foreign Currency Borrowing: Eurozone Firms in 2007-2009.

The piece is interesting because it refers to two topics I have covered at length on this blog: the importance of international financial integration and cross-border lending (implying the importance of not restricting cross-border intragroup capital and liquidity flows), as well as the negative impact of Basel’s risk weights on lending to corporations.

They looked at how a tightening domestic credit supply during a crisis impacted firms that wished to borrow. They found that reduced credit appetite from European banks led riskier corporates to switch to US banks as funding source, which in turn dampened the effects of the crisis on those firms:

We decompose our empirical analysis into three steps. In a first step we verify that foreign credit is countercyclical: when Eurozone banks tighten lending standards, riskier borrowers are more likely to obtain a loan from a foreign bank rather than from a domestic bank. We find that this effect at the intensive margin is attributable to US banks. The willingness of US banks to replace Eurozone banks can be explained by the fact that during this period and until 2012 US lenders operated fully under Basel I. Under the Basel I framework, the risk weight on risky and safe corporate debt is the same. This means that US banks have greater incentive than Eurozone banks to load onto risky corporate debt.

Did you read that? They believe that US banks were more at ease with lending to riskier borrowers because Basel 1’s risk-weights (and therefore capital requirement) were the same for both risky and safe corporates. Regulatory arbitrage at its best. This again demonstrates how Basel’s risk weights distorted the allocation of credit in the economy, as explained literally millions of times on this blog.

They then concluded that transitioning to Basel 2 subsequently made the crisis worse:

The way bank capital is regulated appears to play an important role in the process. The fact that US banks operated under Basel I meant that they had an incentive to shift to riskier corporate loans when Eurozone banks retrenched. Our analysis therefore illustrates how the move from Basel I to Basel II with risk-sensitive capital requirements has contributed to amplify the credit cycle. Basel III goes some way towards addressing the problem through the introduction of mandatory buffers, a capital preservation buffer and a countercyclical buffer, that are built-up in good times and can be released in bad times to avoid a credit crunch.

I wouldn’t agree so much with their statement about Basel 3 however, which relies on the fact that regulatory authorities would be able to foresee and/or correctly assess the economic situation and take the right decisions at the right times; something some of the studies about macro-prudential policies I recently read warned about (more in a following post). A clear knowledge dispersion issue.

Finally, what this paper emphasises is the importance of cross-border lending in dampening the effects of a credit crunch. As I described in my series on intragroup funding, regulators have been trying to silo liquidity and capital in each separate banking groups’ legal entity. I believe this is misguided as it will limit or prevent cross-border funding flows and therefore the ability of subsidiaries to extend credit in foreign countries when necessary. And by attempting to strengthen each separate subsidiary, regulators are likely to make groups as a whole weaker.

PS: I spent a couple of hours earlier this week drafting a post warning against over-interpreting temporary market movements, following a few posts on the topic written by Scott Sumner (see here, here and here). I eventually decided against, as I have written about the topic before and I just couldn’t bother (perhaps I’ll change my mind later). Let’s just say that seeing market movements in the seconds or minutes following an announcement as an indicator of how markets perceived this announcement is a massive misinterpretation of the way financial markets and trading (and even worse now: HFT) work. No market actor has the ability to instantaneously process and analyse complex new information (that is why there are economists, analysts, and other commentators to enlighten market makers and investors). If EMH is valid, it is certainly not within a few minutes timeframe.

In the comment section of one of his posts, he even mentioned the wisdom of crowds as a benefit of democracy. As if Public Choice theory had never existed. No don’t get me started. Please.

Political connection and bank performance

This is a short post about a curious, but interesting, paper I recently read. Titled The dark side of political connection: Exchange easy loans for the political career of bank CEOs, and written by Chen, Hasan, Lin and Yen (CHLY thereafter), the paper demonstrates that banks with political connections underperformed ‘independent’ ones during the crisis.

This probably won’t come as a surprise to many of you. A quick read through Calomiris and Haber’s Fragile by Design shows the critical and disastrous influence of politics on banking and economic performance. Still, the paper is worth a look as it provides further empirical evidence.

CHLY define ‘government banks’ as banks with at least 20% state ownership. They then subdivide this group into two: those with CEOs that served as politicians are called ‘political banks’ and the other ones are ‘non-political banks’. A first comment: I believe their sample underestimate political connections. They probably only pick banks that have the strongest connections. There are non-state-owned banks whose CEOs used to be or have subsequently become politicians, or have been to school with current government officials and have very close links with them. Their sample doesn’t capture such cases. Weirdly, their sample seems to exclude countries such as the US, UK or Germany. No reason is provided.

Based on this admittedly limited dataset, they analyse the evolution of the asset quality, as well as a number of performance indicators (return on equity and assets, cost/income…), of those banks during the crisis. They find that

Political banks significantly approve more low-quality loans than non-political banks, such that they are confronted with a higher ratio of nonperforming loans to gross loans during the crisis. This ratio indicates that politically connected banks become increasingly inefficient and pursue a more risky lending behavior. Further, these lower quality loans cause significant underperformance as measured by the return on assets, return on equities, net interest income to total assets, and the cost to income ratio during the crisis years.

CHLY also find that institutional framework, low corruption, strong governance, and institutional ownership mitigate the impact of political connection on the agency problem. ‘Non-political government banks’ also seem to be partly protected from most of the bad effects that plague ‘political banks’.

Moreover, they find that politically-connected CEOs grant more low quality loans for their own benefit, and that many of those CEOs (almost 30%) were offered political jobs after the crisis. They conclude that

the politically connected CEOs, who have poor operating performance, are less likely to be penalized by the bank or politics. They even have a bright future political career after the crisis. This evidence is consistent with our political connection hypothesis that these CEOs use their power and influence to relax lending standards and reap private benefits.

And some people still question the conclusions of the Public Choice school… Worse, many others want to nationalise the money creation framework (see Positive Money), falsely believing in a fully independent central bank that would always act for the greater good. Others want to nationalise the whole banking system, as if this recipe had never been tried before. Go figure.

Basel capital requirements, labour reallocation and productivity

Last week I wrote two posts about recent research on the impact of Basel’s capital requirements on mortgage pricing and sovereign bond demand, which I believed were evidence of Basel enabling an ‘Austrian-type’ business cycle. Today, this is the last post of this mini-series, and it covers another great research report published by Claudio Borio and his team: Labour reallocation and productivity dynamics: financial causes, real consequences.

As often with Borio, this is a great paper. And it does seem to provide further evidence of Basel allowing distorted allocation of credit with dramatic economic consequences. However, I do need to point out that the paper does not explicitely point at Basel as the cause of the misallocation (but instead supposes that collateral availability plays a role). Rather, this is my own interpretation of it. The correlation looks pretty strong.

The paper looks at forty years of credit and productivity data across 20 advanced economies. It finds that

the decline in the allocation component during credit booms overwhelmingly reflects shifts in employment towards low productivity growth sectors. […] In other words, credit booms do not appear to affect the sectoral distribution of productivity gains, turning potentially high productivity growth sectors into low productivity growth ones. Rather, they induce labour shifts into lower productivity growth sectors. Productivity in industries with rapid long-run productivity growth does not grow any more slowly during credit booms, but these industries attract relatively fewer workers.

So credit booms and/or change in the allocation of credit do not alter the inherent productivity of each sector but rather shift labour between sectors. They also find that “labour reallocation is quantitatively the main channel through which credit booms affect productivity.” The key question being: which sectors benefit, and at the expense of which ones?

And here, the answer couldn’t be clearer (my emphasis):

The results suggest that manufacturing and construction are the two sectors primarily responsible for the slowdown. When either sector is withdrawn, the negative correlation goes away or at least weakens compared with the benchmark case. Interestingly, removing the financial sector does not affect our results.

Combining this result with the previous one, the conclusion is clear. Aggregate productivity slows down during credit booms primarily because employment expands more rapidly in the construction sector, which structurally features low productivity growth. And employment expands more slowly or contracts in manufacturing, which is structurally a high productivity growth sector.

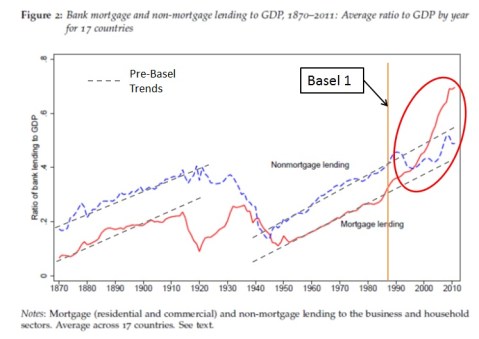

This is in line with what I would expect given that Basel’s capital requirements favour real estate lending over other types. Remember this chart from Jorda et al, which I modified:

Coincidence? Highly unlikely I believe. Although it still isn’t fully clear why manufacturing suffers more than other non-real estate sectors, and this deserves further investigation.

Moreover, they find that once a crisis hits, this misallocation of capital and labour leads to a painfully slow recovery as post-crisis productivity growth is reduced.

They reached a few, but highly important, conclusions, which I have already mentioned on this blog a number of times.

First, they believe that the ‘secular stagnation’ hypothesis should be seen under a different light:

Our findings suggest a different mechanism, in which the slow recovery after the Great Financial Crisis is the result of a major financial boom and bust, which has left long-lasting scars on the economic tissue (eg BIS (2014), Rogoff (2015)). More specifically, they suggest that what some see as a comparatively disappointing US growth performance in the pre-crisis years, despite a strong financial boom, was actually disappointing, in part, precisely because of the boom. And so has been the post-crisis weak productivity growth.

They also warn about the effects of monetary policy in such a world, which could amplify the misallocation:

Nor is it surprising if monetary policy may not be particularly effective in addressing financial busts. This is not just because its force is dampened by debt overhangs and a broken banking system – the usual “pushing-on-a-string” argument. It may also be because loose monetary policy is a blunt tool to correct the resource misallocations that developed during the previous expansion, as it was a factor contributing to them in the first place.

While a number of economists would argue that current monetary policy isn’t loose, the argument still stands. Loose or not, the allocation of credit still occurs through Basel’s lens. And Borio ends this paper by highlighting that there may be a mechanism that distorts credit allocation that he hasn’t yet uncovered. Well, perhaps banking regulation would be a good starting point for further research. Unfortunately, Borio works for the BIS, which devised our whole bank regulatory framework…

Basel capital requirements and sovereign bond demand

This is the second post of this short series reviewing recent research on the distortions introduced by the Basel banking framework, in light of the ‘RWA-based ABCT’. Two days ago I focused on the influence of capital requirements on mortgage pricing. Today I’m going to focus on a new quite interesting (albeit predictable?) piece of research that looks at the influence of the Basel framework on the demand for government bonds (see Preferential Regulatory Treatment and Banks’ Demand for Government Bonds by Clemens Bonner, see also Voxeu summary article here).

Bonner not only analyses the effects of capital requirements, but also of liquidity requirements, mostly introduced by the post-crisis Basel 3 accords. His dataset comprises Dutch banks (which were subject to a Dutch equivalent to Basel 3’s Liquidity Coverage Ratio, the ‘DLCR’). To identify whether banks’ demand for government bonds is caused by regulatory or internal risk management effects, he hypothesises that a change in demand around reporting date is likely to imply that regulatory reporting is the main driver.

He first looks at the impact of liquidity rules (the x-axis represents days of the month, and increased demand for the asset is represented by a descending curve):

If a bank’s regulatory liquidity position affects its net purchases of government bonds over the entire month, it cannot be established whether this effect comes from regulation or from internal risk management targets. With the DLCR affecting banks’ net purchases only from day 18 onwards, it can be concluded that there is limited evidence of an internal effect incentivizing banks with lower liquidity holdings to purchase more government bonds or sell more other bonds. The combined evidence of the DLCR affecting banks’ demand only towards the end of the month and the slopes presented in Figure 5 show clear signs of a regulatory effect, suggesting that the DLCR incentivizes banks to substitute government bonds for other bonds.

He then applies the same logic to capital ratios:

Similar to liquidity, Figure 6 shows that the regulatory capital position is an important determinant of banks’ net purchases of government bonds. One can see that a lower regulatory capital ratio in the previous month causes banks to buy considerably more government bonds and sell more other bonds.

He concludes:

Our results suggest that preferential treatment in microprudential capital and liquidity regulation increases banks’ demand for government bonds. On top of that, it seems to cause a substitution effect, with banks buying more government bonds while selling more other bonds. Further, we find suggestive evidence that this “regulatory reaction” reduces banks’ lending.

As expected, it’s pretty clear that sovereign bonds, thanks to their preferential regulatory treatment (no capital required and quasi-obligation to hold them as part of your high-quality liquid assets portfolio) boosted the demand for them. This, in turn, should have depressed their yields and allowed governments to benefit from lower interest rate than in an unhampered market. Low yields are always good for debt binges.

Worse, and also as expected, the increase in demand for those bonds led to a decrease in demand for corporate bonds, which is likely to have had the opposite effects on yields and on the profitability and investments of those firms.

PS: I think I should rename the ‘RWA-based ABCT’ into ‘Basel ABCT’. The RWA name was mostly valid in pre-Basel 3 times but now that Basel 3 has introduced extra ways of distorting demand, supply and yields, ‘Basel ABCT’ sounds more appropriate.

Basel capital requirements and mortgage pricing

Do we still need evidence that Basel’s capital requirements distort interest rates and capital allocation in the economy? Yes we do. We need as much evidence as we can in order to present a bulletproof case against current banking regulation.

I have argued since this blog’s inception that the pricing distortions hardwired in Basel’s framework led to fundamental misallocations that could trigger economic crises (the ‘RWA-based ABCT’) and progressively provided empirical evidence in support of this case. Just a few weeks ago, I reported that recent (and not so recent) pieces of research were (unsurprisingly in my opinion) attacking Basel on the ground that it unnecessarily penalised SME lending.

This post is the first of a series of three new short posts covering research papers published over the past few months which, you guessed it, seem to add to this growing body of evidence.

The first one, titled Higher Bank Capital Requirements and Mortgage Pricing: Evidence from the Countercyclical Buffer (CCB), is also the first paper I read that shows that macro-prudential regulation could have some effect! Although this effect is limited and it is unclear (and uncontrolled) if credit growth cannot happen through other channels.

But what I’m interested in is the impact of the countercyclical buffer (CCB), a macro-prudential tool that allows policymakers to adjust capital requirements according to where in the economic cycle they believe we stand. It’s all discretionary and they will often get it wrong (assuming they are not influenced by politics) of course, but at least it allows us to live test the reactions of private actors to this exogenous constraint and measure the resulting distortion in credit supply and pricing.

In this case, Switzerland raised the CCB for mortgage lending only, leaving other sorts of lending untouched, which effectively tightened the spread between mortgage capital requirements and the rest. Remember that mortgage (or sovereign) lending benefited from much lower capital requirements than corporate lending, making it more profitable at equal levels of risk to extend credit for real estate purposes. In theory, and given a fixed money supply, this incentive should lead to increased mortgage supply and lowered interest rates on mortgage products. Hence, a reduction in the capital differential would likely reduce the supply of mortgage and/or raise interest rates.

So what did the paper find? That the CCB was changing the composition of mortgage supply and raising mortgage interest rates:

Results […] point out that capital-constrained banks raise their rates relatively more after the CCB’s regulatory shock than do their unconstrained peers. In line with the joint estimation, these constrained banks now charge on average 2.72 bp more which reflects their tradeoff between approaching the now even closer intervention threshold and additional profits. The constrained indicator is not statistically significant in either estimation.

Results […] reveal that banks that specialize in the mortgage business increase their mortgage rates after the CCB activation by on average 5.57bp relative to non-specialized competitors. Higher capital requirements force banks to hold more equity capital for each mortgage already on their balance sheets. Some of that additional cost on their existing portfolio is passed on to new customers. Again, the specialized indicator is insignificant in both regressions

This is encouraging evidence, although not comprehensive. It would have been interesting to find out whether or not other sorts of lending benefited from changes in their supply and/or pricing.

Regarding the conclusion that the CCB might be an effective macro-pru tool, the paper did not control for domestic or international leakage (i.e. credit growth through other channels) and it remains to be seen whether or not banks are not willing to go down the risk scale in order to extract higher rates for the same amount of capital (which would come at the expense of financial stability down the line).

A few thoughts for JPK on negative rates and AD

Following my post on negative rates and banking instability, JP Koning commented and left a very interesting question:

Are you of the opinion that a rate cut into negative territory would reduce aggregate demand?

First, I’d like to apologise to JP for the very late reply. I had a crazy past week (for those who don’t know, I compete in powerlifting)…

While drafting an answer, I came to the conclusion that I should actually write a very short post as this might be of interest to a number of my readers. Here are some of my thoughts:

I think it’s tricky to answer. It will vary a lot depending on local factors and local culture.

But I believe that, if ever negative rates provide a boost to demand, it will be minimal and not worth the risk of extra financial instability it creates.

But quantitatively it’s really hard to say.

Some of the factors involved are (I’m surely missing a few other ones):

– Are banks going to charge retail customers or not?

– If they do, what is the local propensity to save more/spend more/withdraw cash/change nothing in response, and in which amplitude?

– Also, how will this affect the turnover on banks’ deposit base, and hence their funding stability, as deposits have traditionally been among the most stable funding sources. In line with the theory of my previous post, empirical evidences show that banks with less stable funding structures tend to contract their lending more (or at least grow their loan book more slowly) in periods of stress (see this very interesting paper by Ivashina and Scharfstein for instance). And less lending implies less demand.

– If not, how are banks going to deal with the decline in profitability while having to implement seriously disrupting banking reforms and generate extra capital to comply with regulatory requirements, while still retaining their shareholder base? Banks without shareholders just disappear. And an economy without banks usually doesn’t perform very well.

– Also, in order to prevent their RoE from evaporating, what is going to be the propensity of profitability-constrained banks to start hunting for extra yield by lowering underwriting standards, potentially endangering medium to long-term financial stability? And I fear that, in such case, banks would once again get blamed for the resulting crisis, leading to even more government intervention in the financial system. This can’t be good.

So there cannot be a definitive answer to JP’s question, with local culture and banking characteristics being determinant factors.

Recent Comments