Pushing market rationality too far

In a new post on Switzerland, Scott Sumner said (my emphasis):

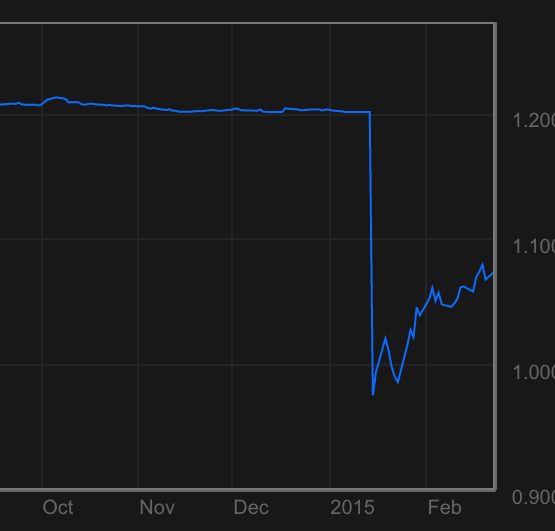

The following graph shows that the SF has fallen from rough parity with the euro after the de-pegging, to about 1.08 SF to the euro today:

And this graph shows that the Swiss stock market, which crashed on the decision that some claimed was “inevitable” (hint, markets NEVER crash on news that is inevitable), has regained most of its losses.

I often enjoy what Scott Sumner writes, but this comment is from someone who doesn’t understand, or has no experience in, financial markets. We all know that Sumner strongly believes in rational expectations and the EMH. But this is pushing market efficiency and rationality too far.

According to Sumner, “markets never crash on news that is inevitable”. Really? Is he saying that markets believed the Euro peg would remain in place forever (which is the only necessary condition for the de-pegging not being ‘inevitable’)?

In reality many investors, if not most (though it can’t be said with certainty), were aware that the peg would be removed and of the resulting potential consequences for Swiss companies. So why the crash?

While investors surely knew that the peg wouldn’t last, they didn’t know when it would end. They were acting on incomplete information. However, this is perhaps what Sumner implies: the Swiss central bank should have provided markets with a more precise statement of when, and in what conditions, the peg would end. Markets would have revised their expectations and priced in the information. This reasoning underpins the rationale for monetary policy rules and forward guidance. But in practice, providing ‘guidance’ isn’t easy: central bankers are not omniscient, have imperfect access to information and cannot accurately forecast the future in an ever-changing world. See what happened to the BoE’s forward guidance policy, which ended up not being much guidance at all as central bankers changed their minds as the economic situation in the UK evolved*.

But the rational expectations argument itself can be used to describe many different situations. If investors believe the peg will end at some point, but don’t know exactly when, it is arguably as ‘rational’ for them to try to maximise gains as long as they could and to try to exit the market just before it crashes, as it is ‘rational’ to adapt their positions to minimise their risk exposure. When the market finally does crash, it often overshoots, for the same reason: benefiting from a short-term situation to maximise profits.

Taking advantage of monetary policy is what traders do. It is their job. Of course, many will fail in their attempt. But necessarily identifying rational expectations with strong short-term risk-aversion and immediate inclusion of external information into prices is abusive.

This latest Bloomberg article shows that close to 20% of traders expect the Fed to raise rates in June, and consequently have surely put in place trading strategies around this belief, and are likely to react negatively if their expectations aren’t fulfilled. However, who doubts that a rate rise is ‘inevitable’? This demonstrates the price-distorting ability of central banks. In order to limit extreme price fluctuations and crashes, the better central banks can do is to disappear from the marketplace entirely.

*Other practical restrictions on guidance include the fact that, while professional investors are likely to be aware of their significance, the rest of the population has no idea what the hell you’re talking about, if it has even heard of it. As a result, the efforts the BoE made to reassure UK borrowers that rates would not rise in the short-run seemed pointless, as virtually no average Joe got it, implying that most people didn’t change their borrowing behaviour/plan in consequence.

I have made a case for rule-based policies a while ago, which I do believe would limit distortions to an extent.

Recent Comments

| pslebow on ‘Sovereign money’:… | |

| pslebow on A critique of Werner’s view on… | |

| Hugo Kramer on Welcome to Spontaneous Fi… | |

| Nathan on A critique of Werner’s view on… | |

| Nathan on More, more, more money endogen… |

Trackbacks / Pingbacks