Is the zero lower bound actually a ‘2%-lower bound’?

Following my recent reply to Ben Southwood on the relationship between mortgage rates, BoE base rate and banks’ margins and profitability (see here and here), a question came to my mind: if the BoE rate can fall to the zero lower bound but lending rates don’t, should we still speak of a ‘zero lower bound’? It looks to me that, strictly in terms of lending and deposit rates, setting the base rate at 0% or at 2% would have changed almost nothing at all, at least in the UK.

The culprit? Banks’ operational expenses. Indeed, it looks like the only way to break through the ‘2%-lower bound’ would be for banks to slash their costs…

Let’s take a look at the following mortgage rates chart from one of my previous posts:

From this chart, it is clear that lowering the BoE rate below around 2.5% had no further effect on lowering mortgage rates. As described in my other posts, this is because banks’ net interest income necessarily has to be higher than expenses for them to remain profitable. When the BoE rate falls below a certain threshold that represents operational expenses, banks have to widen the margins on loans as a result.

From this chart, it is clear that lowering the BoE rate below around 2.5% had no further effect on lowering mortgage rates. As described in my other posts, this is because banks’ net interest income necessarily has to be higher than expenses for them to remain profitable. When the BoE rate falls below a certain threshold that represents operational expenses, banks have to widen the margins on loans as a result.

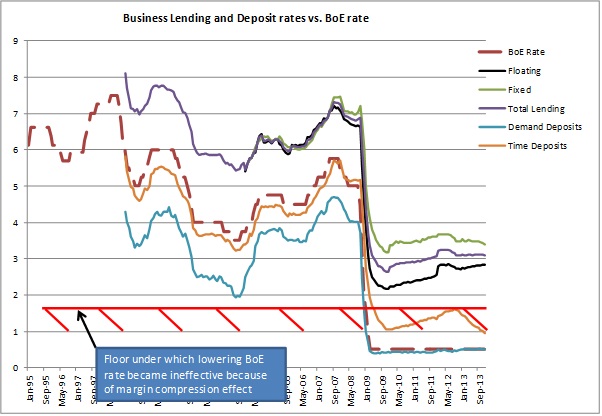

What about business lending rates? Since business lending is funded by both retail and corporate deposits (and excluding wholesale funding for the purpose of the exercise), the analysis must take a different approach. Banks don’t often disclose the share of corporate deposits within their funding base, but I managed to find a retail/corporate deposit split of 75%/25% at a large European peer, which I am going to use as a rough approximation to estimate banks’ business lending margins. Here are the results of my calculations (first chart: margin over time deposits, second chart: margin over demand deposits):

No surprise here, the same margin compression effect appears as a result of the BoE rate collapsing (as well as Libor, as floating corporate lending is often calculated on a Libor + margin basis, unlike mortgages, which are on a BoE + margin basis). Before that period, changes in the BoE and Libor rates had pretty much no effect on margins. After the fall, banks tried to rebuild their margins by progressively repricing their business loan books upward (i.e. increasing the margins over Libor).

No surprise here, the same margin compression effect appears as a result of the BoE rate collapsing (as well as Libor, as floating corporate lending is often calculated on a Libor + margin basis, unlike mortgages, which are on a BoE + margin basis). Before that period, changes in the BoE and Libor rates had pretty much no effect on margins. After the fall, banks tried to rebuild their margins by progressively repricing their business loan books upward (i.e. increasing the margins over Libor).

Here again we can identify a 1.5% BoE rate floor, under which lowering the base rate does not translate into cheaper borrowing for businesses:

This has repercussions on monetary policy. The banking/credit channel of monetary policy aims at: 1. easing the debt burden on indebted household and businesses and, 2. stimulating investments and consumption by making it cheaper to borrow. However, it seems like this channel is restricted in its effectiveness by banks’ ability in passing the lower rate on to customers. Banks’ short-term fixed cost base effectively raises the so-called zero lower bound to around 2%. The only way to make the transmission mechanism more efficient would be for banks to drastically improve their cost efficiency and have assets of good-enough quality not to generate impairment charges, which is tough in crisis times. Unfortunately, there are limits to this process, and a bank without employee and infrastructure is unlikely to lend in the first place…

This has repercussions on monetary policy. The banking/credit channel of monetary policy aims at: 1. easing the debt burden on indebted household and businesses and, 2. stimulating investments and consumption by making it cheaper to borrow. However, it seems like this channel is restricted in its effectiveness by banks’ ability in passing the lower rate on to customers. Banks’ short-term fixed cost base effectively raises the so-called zero lower bound to around 2%. The only way to make the transmission mechanism more efficient would be for banks to drastically improve their cost efficiency and have assets of good-enough quality not to generate impairment charges, which is tough in crisis times. Unfortunately, there are limits to this process, and a bank without employee and infrastructure is unlikely to lend in the first place…

Don’t get me wrong though, I am not saying that lowering the BoE rate (and unconventional monetary policies such as QE) is totally ineffective. Lowering rates also positively impact asset prices and market yields, ceteris paribus. This channel could well be more effective than the banking one but it isn’t the purpose of this post to discuss that topic. Nevertheless, from a pure banking channel perspective, one could question whether or not it is worth penalising savers in order to help borrowers that cannot feel the loosening.

PS: I am not aware of any academic paper describing this issue, so if you do, please send me the link!

Balkanise or globalise banking, there is no middle way

The Fed published new rules last week that effectively require foreign banks in the US to follow the same rules as American ones, including the recent Dodd-Frank Act. Foreign banks will have to adapt their legal structure and ‘adequately’ capitalise their subsidiaries in order to comply with local capital and liquidity requirements as well as local stress tests. Before that, most banks relied on their foreign parent for liquidity and capital support if needed. I don’t really welcome such changes for a few reasons.

First, it balkanises banking, in an era of globalisation, during which global multinational companies as well as large SMEs look for financing throughout the world to grow their activities. Banks that have global operations provide a single entry point to such firms, smoothening relationship, Know-Your-Customer processes and enhancing financing speed and reliability. Companies can quickly raise funds in Germany or in Latin America without having to rebuild a new relationship (and to deposit funds) with another local (and potentially weaker) bank. As the EU has already pointed out, this move by the Fed also invites retaliation by other regulators around the world. This could trigger a chain reaction not dissimilar to post-1929 tariff battles. Capital flows, foreign investments and economic growth would be the first ones to suffer. People would follow.

Nevertheless, the Fed might have a point in that it would reduce financial instability…in the US… in the short term. However, this is exactly why global authorities were currently working together to make sure that common frameworks were in place to resolve failing banks and ensure similar regulations were applied across various jurisdictions. The Fed’s decision undermines the trust and all the work that had been done so far. It is also the proof that regulators will often tend to defend their own narrow national interests, and the source of their power, rather than the broader ‘greater good’.

Finally, such a decision might even eventually create further instability. Large non-American banks, already under pressure from their shareholders and own national regulators, are now reviewing their US activities in order to figure out ways to circumvent the rules. Some banks already book a part of their US business in Europe. Expect this trend to accelerate and the balance sheet of some emerging markets subsidiaries to grow… In the end, the Fed’s new rules may well lead to further regulatory arbitrage, making banks’ balance sheets even more opaque to external observers, undermining the market process and its necessary overseeing mechanism. And even if isolated and ring-fenced, when the global financial system collapses, the US system is likely to follow.

Photo: Parliament.uk

News digest: Scotland, CoCos and electronic trading

Sam Bowman had a very good piece on the Adam Smith Institute blog about Scotland setting up a pound Sterling-based free banking system unilaterally (yeah I know I keep mentioning this blog now, but activity there seems to have been picking up recently). It draws on George Selgin’s post and is a very good read. One particular point was more than very interesting in the context of my own blog (emphasis added):

George Selgin has pointed to research by the Federal Reserve Bank of Atlanta about the Latin American countries that unilaterally use the dollar. Because these countries – Panama, Ecuador and El Salvador – lack a Lender of Last Resort, their banking systems have had to be far more prudent and cautious than most of their neighbours.

Panama, which has used the US Dollar for one hundred years, is the most useful example because it is a relatively rich and stable country. A recent IMF report said that:

“By not having a central bank, Panama lacks both a traditional lender of last resort and a mechanism to mitigate systemic liquidity shortages. The authorities emphasized that these features had contributed to the strength and resilience of the system, which relies on banks holding high levels of liquidity beyond the prudential requirement of 30 percent of short-term deposits.”

Panama also lacks any bank reserve requirement rules or deposit insurance. Despite or, more likely, because of these factors, the World Economic Forum’s Global Competitiveness Report ranks Panama seventh in the world for the soundness of its banks.

I don’t think I have anything to add…

SNL reported yesterday that Germany’s laws seem to make the issuance of contingent convertible bonds (CoCos) almost pointless. This is a vivid reminder of my previous post, which highlighted some of the ‘good’ principles of financial regulation and which advocated stable, simple and clear rules, a position I have had since I’ve opened this blog. All authorities and regulators try to push banks (including German banks) to boost their capital level, which are deemed too low by international standards. CoCos, which are bonds that convert into equity if the bank’s regulatory capital ratio gets below a certain threshold, are a useful tool for banks (as it allows them to prevent shareholder dilution by issuing equity) and investors (whose demand is strong as those bonds pay higher coupon rates). Yet lawmakers, who love to bash banks for their low level of capitalisation, seem to be in no hurry to provide a clear framework that would allow to partially solve the very problems they point at in the first place… This is a very obvious example of regime uncertainty. As one lawyer declared:

One thing is clear: Nothing is clear

Bloomberg reports that FX traders are facing ‘extinction’ due to the switch to electronic trading. In fact, this has been ongoing for now several years, with asset classes moving one after another towards electronic platforms. Electronic trading now represents 66% of all FX transactions (vs. 20% in 2001). Traditional traders are going to become increasingly scarce and replaced by IT specialists that set and programme those machines. Overall, this should also mean less staff and a lower cost base for banks that are still plagued by too high cost/income ratios. Part of this shift is due to regulation, which makes it even more expensive to trade some of those products. This only reinforces my belief that regulation is historically one of the primary drivers of financial innovation, from money market funds to P2P lending…

Some ‘good’ principles of financial regulation

Readers of this blog know the extent of my love for banking regulation. I love regulation. I really do. Otherwise I wouldn’t have much to write about.

Irony aside, I recently read a very good paper by Calomiris (Financial Innovation, Regulation, and Reform, 2009, which you can find here) that made me give regulation a rethink (to be frank, I was disappointed that there’s not much about financial innovation in this paper, but the rest is pretty good).

Calomiris is a free-market guy. He makes it clear is most of his papers, this one included:

The risk-taking mistakes of financial managers were not the result of random mass insanity; rather they reflected a policy environment that strongly encouraged financial managers to underestimate risk in the subprime mortgage market. Risk-taking was driven by government policies; government’s actions were the root problem, not government inaction.

He is right. But he also seems to be a ‘realist’ (if ever this really means anything). He considers that, given our current distortive institutional framework, the best thing we can do is to mitigate its effect through proper regulation. He writes:

If there were no governmental safety nets, no government manipulation of credit markets, no leverage subsidies, and no limitations on the market for corporate control, one could reasonably argue against the need for prudential regulation. Indeed, the history of financial crises shows that in times and places where government interventions were absent, financial crises were relatively rare and not very severe.

[…But] it is not very helpful to suggest only regulatory changes that are very far beyond the feasible bounds of the current political environment. […] Absent the elimination of [all the policies described above], government prudential regulation is a must.

In a way, he has a point. Whereas I’d like to see the implementation of a free banking system, I also have to admit that this possibility is pretty unlikely to ever reoccur (unless a once in a thousand years financial collapse suddenly strikes). Which led me to think about a ‘second best’. This ‘second best’ solution should follow the principles I described here (where I argued in favour of a stable rule set and regulatory framework) and here (where I agreed with Lars Christensen and John Cochrane and argued against macro-prudential regulations). This is what I wrote:

Stable rules are a fundamental feature of intertemporal coordination between savers and borrowers, between investors and entrepreneurs. In order for economic agents to (more or less) accurately plan for the future, for entrepreneurs to develop their business ideas and anticipate future demand, for savers to invest their money and know that their property rights are not going to disappear overnight and accordingly plan their own delayed consumption and provide entrepreneurs with directly available funds, the economic system needs a stable and predictable rule framework. Production and investments take time and as a result involve uncertainty, which should not be exacerbated by an instable rule set. The rule of law is part of this framework. Monetary policy, financial regulation and government policies should follow the same pattern, instead of being discretionary.

What I am about to describe is a non-exhaustive list of ‘good’ principles of regulation that fit (to an extent) a free-market framework. I may update the list over time. Following the principles above, and even though not perfect, a ‘second best’ solution would have to be:

- As least distortive as possible (i.e. introducing as few loopholes and incentives to game the rules as possible)

- As stable as possible (i.e. no discretionary powers), and

- As simple, transparent and clear as possible (i.e. a few clear and straightforward rules are better than a multitude of obscure and complex ones)

On the monetary policy side, despite its flaws, NGDP targeting seems to be the only ‘easily implementable’ policy that meets the three criteria. I won’t discuss it here (see The Money Illusion, The Market Monetarist, Worthwhile Canadian Initiative, and many other blogs for more information). On the slightly ‘less easily implementable’ side, the ‘productivity norm’ would nonetheless be an even better alternative (see George Selgin’s implementation here, from page 64 onwards).

What about financial and banking regulation? In order to respect the three fundamental rules described above, regulators should:

- Define few transparent, straightforward limits and ratios based on objective and easily measurable criteria that are neither pro- nor counter-cyclical

- Not impose their own perception of risk to the market

- Not vary regulatory limits and requirements over time

- Not publicly shame financial institutions that respect regulatory requirements even if borderline-compliant: the regulators’ role is to make sure that institutions respect the requirements, period

- Publicly make clear that regulations only represent minimums, that regulators are only here to make those minimums respected, and that it is the role of market actors to identify stronger from weaker institutions within those regulatory-defined limits

- Not interfere with financial institutions’ strategy and internal organisational structures: harmonising business models takes the risk of weakening the whole system

- Refrain from making any comment unrelated to the (non)compliance of institutions to regulatory requirements

- Allow the market process to run its course and not institutionalise moral hazard by implementing bailout and other backstop mechanisms

Banking regulation is divided into micro-prudential and macro-prudential regulation. The former provides individual banks with rules they have to respect at all times, independently of the performance of the whole economy. The latter provides all banks with rules that vary according to the state of the economy, independently of the performance of each bank. Following the principles above, fixed and straightforward sets of micro-prudential regulations may be acceptable. On the other hand, most macro-prudential regulations would be eliminated given their discretionary component and their variability over time. It is indeed very hard for regulators to identify bubbles and other excesses (see White, 2011, here). They have a poor track record at it. Discretion could well prevent a bubble from growing too much but it could also prevent a genuinely growing market to reach its full potential. Regulators suffer from the central planner’s problem. As Hayek said in his essay The Use of Knowledge in Society:

The peculiar character of the problem of a rational economic order is determined precisely by the fact that the knowledge of the circumstances of which we must make use never exists in concentrated or integrated form, but solely as the dispersed bits of incomplete and frequently contradictory knowledge which all the separate individuals possess.

I can already hear the rebuttals: “but counter-cyclical macro-prudential policies would help mitigate the bust after the boom!” To which I would respond: “how do you identify a ‘boom’?” For a bust to occur, a boom must be unsustainable. Solid and sustainable growth may well happen and should not be interfered with by counter-cyclical regulations that would in fact not be counter-cyclical at all in this case. Nominal stability is primarily the role of monetary policy, which should promote a stable framework to the real economy. An unsustainable boom is likely to emanate from nominal instability. The goal of regulation is not to mitigate the effects of destabilising monetary policies.

Of course, this does not mean that one should not strive to reduce political and regulatory distortions. ‘Idealists’ (if ever this also means anything) are a necessary part of a healthy democratic process. Moreover, too much compromise can be dangerous: where to fix the limit? Because the very distortive sources are still present, crises can still occur and provide extra arguments to further expand the regulatory burden.

PS: I’ll provide examples of regulations that comply or not with those principles in a subsequent post. This post would have been too long otherwise!

A clarification on mortgage rates for ASI’s Ben Southwood

Ben Southwood from the Adam Smith Institute replied to my previous post here. I am still confused about Ben’s claim that the spread varied “widely”. As the following chart demonstrates, the margins of SVR, tracker and total floating lending over the BoE base rate remained remarkably stable between 1998 and 2008, despite the BoE rate varying from a high 7.5% in 1998 to a low of 3.5% in 2003:

Everything changed in 2009 when the BoE rate collapsed to the zero lower bound. Following his comments, I think I need to address a couple of things. Two particular points attracted my attention. Ben said:

If other Bank schemes, like Funding for Lending or quantitative easing were overwhelming the market then we’d expect the spread to be lower than usual, not much higher.

His second big point, that the spread between the Bank Rate and the rates banks charged on markets couldn’t narrow any further 2009 onwards perplexes me. On the one hand, it is effectively an illustration of my general principle that markets set rates—rates are being determined by banks’ considerations about their bottom line, not Bank Rate moves. On the other hand, it seems internally inconsistent. If banks make money (i.e. the money they need to cover the fixed costs Julien mentions) on the spread between Bank Rate and mortgage rates (i.e. if Bank Rate is important in determining rates, rather than market moves) then the absolute levels of the numbers is irrelevant. It’s the spread that counts.

It looks to me that we are both misunderstanding each other here. It is indeed the spread that counts. But the spread over funding (deposit) cost, not BoE rate! (Which seems to me to be consistent with my posts on MMT/endogenous money.) Let me clarify my argument with a simple model.

Assumptions:

- A medium-size bank’s only assets are floating rate mortgages (loan book of GBP1bn). Its only source of revenues is interest income. The bank maintains a fixed margin of 1% above the BoE rate but keeps the right to change it if need be.

- The bank’s funding structure is composed only of demand deposits, for which the bank does not pay any interest. As a result, the bank has no interest expense.

- The bank has a 100% loan/deposit ratio (i.e. the bank has ‘lent out’ the whole of its deposit base and therefore does not hold any liquid reserve).

- The bank has an operational cost base of GBP20m that is inflexible in the short-term (not in the long-term though there are upwards and downwards limits) and no loan impairment charge.

Of course this situation is unrealistic. A 100% loan/deposit bank would necessarily have some sort of wholesale funding as it needs to maintain some liquidity. It would also very likely have a more expensive saving deposit base and some loan impairment charges. But the mechanism remains the same therefore those details don’t matter.

In order to remain profitable, the bank’s interest income has to be superior to its cost base. Moreover, the bank’s interest income is a direct, linear function, of the BoE rate. The higher the rate, the higher the income and the higher the profitability. As a result, the bank’s profitability obeys the following equation:

Net Profit = Interest Income – Costs = f(BoE rate) – Costs,

with f(BoE rate) = BoE rate + margin = BoE rate + 1%.

Consequently, in order for Net Profit > 0, we need f(BoE rate) > Costs.

Now, we know that the bank’s cost base is GBP20m. The bank must hence earn more than GBP20m on its loan book to remain profitable (which does not mean that it is enough to cover its cost of capital).

The BoE rate is 2%, making the rate on the mortgage book of the bank 3%, leading to a GBP30m income and a GBP10m net profit. Almost overnight, the BoE lowers its rate to 0.5%. The bank’s loan book’s average rate is now 1.5%, and generates GBP15m of income. The bank is now making a GBP5m loss. Having inflexible short-term costs, it’s only way of getting back to profitability is to increase its margin by at least 0.5%. The bank’s net profit profile is summarised by the following chart:

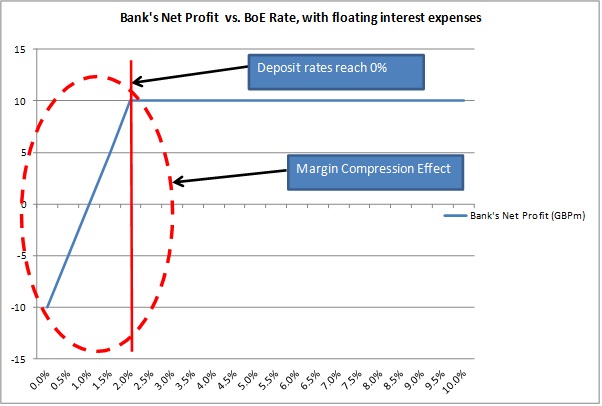

However, a more realistic bank would pay interest on its deposit base (its funding). Let’s now modify our assumptions and make that same bank entirely demand deposit-funded, remunerated at a variable rate. The bank pays BoE rate minus a fixed 2% margin on its deposit base. As a result, what needs to cover the banks operational costs isn’t interest income but net interest income. The bank’s net profit equation is now altered in the following way:

Net Profit = Net Interest Income – Costs

Net Profit = Interest Income – Interest Expense – Costs

Net Profit = f1(BoE rate) – f2(BoE rate) – Costs

with f1(BoE rate) = BoE rate + margin = BoE rate + 1%,

and f2(BoE rate) = BoE rate – margin = BoE rate – 2%.

The equation can be reduced to: Net Profit = 3% (of its loan book) – Costs, as long as BoE rate >= 2% (see below).

Let’s illustrate the net profit profile of the bank with the below chart:

What happens is clear. Independently of its effects on the demand for credit and loan defaults, the BoE rate level has no effect on the bank’s profitability. Everything changes when deposit rates reach the zero lower bound (i.e. there is no negative nominal rate on deposits), which occurs before the BoE rate reaches it. From this point on, the bank’s interest income decreases despite its funding cost unable to go any lower. This is the margin compression effect that I described in my first post. In reality, things obviously aren’t that linear but follow the same pattern nevertheless.

Realistic banks are also funded with saving deposits and senior and subordinated debt, on which interest expenses are higher. This is when schemes such as the Funding for Lending Scheme kicks in, by providing cheaper-than-market funding for banks, in order to reduce the margin compression effect. The other way to do it is to reflect a rate rise in borrowers’ cost, while not increasing deposit rates. This is highly likely to happen, although I guess that banks would only partially transfer a rate hike in order not to scare off customers.

Overall, we could say that markets determine mortgage rates to an extent. But this is only due to the fact that banks have natural (short-term) limits under which they cannot go. It would make no sense for banks not to earn a single penny on their loan book (and they would go bust anyway). Beyond those limits, the BoE still determines mortgage rates.

Although I am going to qualify this assertion: the BoE roughly determines the rate and markets determine the margin. At a disaggregated level, banks still compete for funding and lending. They determine the margins above and below the BoE rate in order to maximise profitability. They, for instance, also have to take into account the fact that an increase in the BoE rate might reduce the demand for credit, thereby not reflecting the whole increase/decrease to customers as long as it still boosts their profitability. Those are some of the non-linear factors I mentioned above. But they remain relatively marginal and the aggregate, competitively-determined, near-equilibrium margin remains pretty stable over time as demonstrated with the first chart above.

With this post I hope to have clarified the mechanism I relied on in my previous post, but feel free to send me any question you may have!

Mortgage rates are still determined by the BoE

Ben Southwood from the Adam Smith Institute wrote an interesting piece this week. I have an objection to his title and the conclusion he reached. Ben wrote:

However, it was recently pointed out to me that since a high fraction of UK mortgages track the Bank of England’s base rate, a jump in rates, something we’d expect as soon as UK economic growth is back on track, could make mortgages much less affordable, clamping down on the demand for housing.

This didn’t chime with my instincts—it would be extremely costly for lenders to vary mortgage rates with Bank Rate so exactly while giving few benefits to consumers—so I set out to check the Bank of England’s data to see if it was in fact the case. What I found was illuminating: despite the prevalence of tracker mortgages the spread between the average rate on both new and existing mortgage loans and Bank Rate varies drastically.

Wait. I really don’t reach the same conclusion from the same dataset. This is what I extracted from the BoE website (using the BoE’s old reporting format, as the new one only started in 2011):

Banks and building societies offer two main types of floating rate mortgages: standard variable rate (SVR) and trackers. Trackers usually follow the BoE rate closely. SVR are slightly different: margins above the BoE rate are more flexible. Banks vary them to manage their revenues but usually fix them for an extended period of time before reviewing them again. During the crisis, some banks that had vowed to maintain their SVR at a certain spread angered their customers when this situation became unsustainable due to low base rates. Some banks and building societies made losses on their SVR portfolio as a result and had to break their promise and increase their SVR.

What we can notice from the chart above is clear: since the mid-1990s, it is the BoE that determine both mortgage and deposit rates. Not the market. All rates moved in tandem with the BoE base rate. Still, the linkage was broken when the BoE rate collapsed to the zero lower bound in 2009. And this is probably why Ben declared that

but what is clear is that tracker mortgages be damned, interest rates are set in the marketplace.

I think this is widely exaggerated. Ben missed something crucial here: banks have fixed operational costs. Banks generate income by earning a margin between their interest income (from loans) and interest expense (from deposits and other sources of funding). They usually pay demand deposits below the BoE rate and saving/time deposits at around the BoE rate, and make money by lending at higher rates. From this net interest income, banks have to deduce their fixed costs (salaries and other administrative expenses) and bad debt provisions.

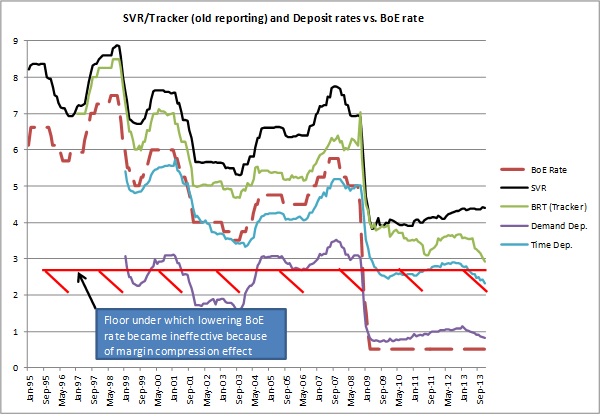

There is a problem though. Setting the BoE rate near zero involves margin compression. Banks’ back books (lending made over the previous years) on variable rates see their interest income collapse. Banks’ deposit base is stickier: many saving accounts are not on variable rates. Therefore, there is a time lag before the deposit base reprice (we can see this on the chart above: whereas lending reprices instantaneously when the BoE rate moves, deposits show a lag). Moreover, near the zero bound, the spread between demand deposit rates and the BoE rates all but disappears. The two following charts clearly illustrate this margin compression phenomenon:

It is clear that banks started to make losses when the BoE rate fell, as the margin on the floating rate back book (stock) became negative. Using the new BoE reporting would make those margins look even worse*. To offset those losses, banks started to increase the spread on new lending, leading to a spike on the interest margin of the front book (green line above). Banks can potentially reprice their whole loan book at a higher margin, but this takes time, especially with 15 to 30-year mortgages. Consequently, banks not only increased the spread on new lending, but also decided to break their SVR promises and increase their back book SVR rates (see black line in charts). This usually did not go down well with their customers, but some banks had no choice, having entered the crisis with too low SVRs.

What happens to a bank whose net interest income is negative (assuming it has no other income source)? It reports net accounting losses as it still has fixed operational expenses… Continuously depressed margins explain why banks’ RoE remains low. For banks to report net profits, their net interest income must cover (at least) both operational expenses and loan impairment charges. What Ben identified as ‘market-defined interest rates’ or the ‘spread over BoE’s rate’ from 2009 onwards is simply the floor representing banks’ operational costs, under which banks cannot go… The only other (and faster) way to rebuild banks’ bottom line would be to increase the BoE rate.

A mystery though: why didn’t banks decrease their time deposit rates further? I am unsure to have an answer to that question. A possibility is that the spread between demand and time deposits remained the same. Another possibility is that banks’ time deposit rates remained historically roughly in line with UK gilts rates. Decreasing time deposit rates much below those of gilts would provide savers with incentives to invest their money in gilts rather than in banks’ saving accounts.

What would a rate hike mean? Ben thinks it would have little impact, probably because the spread over BoE seems to show quite a lot of breathing space before the base rate impacts lending rates. I don’t think this is the case. A rate increase would likely push lending rates upwards on bank’s back book (i.e. banks are not going to reduce the spread in order to maintain stable mortgage rates). Why? Banks’ net interest margin and return on equity are still very depressed. Moreover, new Basel III regulations are forcing banks to hold more equity, further reducing RoE. Consequently, banks will seek to rebuild their margin and profitability, making customers pay higher rates to compensate for years of low rates and newly-introduced regulatory measures.

* I am unsure why the BoE changed its reporting and what the differences are, but reported lending rates are much lower than with the old reporting standards. Tracker mortgage rates even seem to be lower than time deposit rates. See below and compare with my first chart. If anybody has an explanation, please enlighten me:

Update: I replaced ‘ceiling’ with ‘floor’ in the post as it makes a lot more sense!

Update 2: Ben Southwood replies here…

Update 3: …and I replied there!

Bundesbank’s Dombret has strange free market principles

Andreas Dombret, member of the executive board of the Bundesbank, made two very similar speeches last week (The State as a Banker? and Striving to achieve stability – regulations and markets in the light of the crisis). When I started to read them, I was delighted. Take a look:

If one were to ask the question whether or not the market economy merits our trust, another question has to be added immediately: “Does the state merit our trust?”

[…]

Sometimes it seems as if we are witnessing a transformation of values and a redefinition of fundamental concepts. The close connection between risk-taking and liability, which is an important element of a market economy, has weakened.

Conservative and risk-averse business models have become somewhat old-fashioned. If the state is bearing a significant part of the losses in the case of a default of a bank, banks are encouraged to take on more risks.

[…]

[High bonuses and short-termism] are the result of violated market principles and blurred lines between the state and the banks. They are not the result of a well-designed market economy but rather indicative of deformed economies. However, the market economy stands accused of these faults.

Brilliant. I was just about to become a Dombret fan when…I read the rest:

In my view, the solution is to be found in returning the state to its role of providing a framework in which the private sector can operate. This means a return to the role the founding fathers of the social market economy had in mind.

They knew that good banking regulation is a key element of a well-designed framework for a well-functioning banking industry and a proper market economy in general.

[…]

This is where good bank capitalisation comes into play. It is the other side of the coin. Good regulation should directly address the key problem. If the system is too fragile, an important and direct measure to reduce fragility is to have enough capital.

[…]

Good capitalisation will have the positive side effect of reducing many of the wrong incentives and distortions created by taxpayers’ implicit guarantees and therefore making the bail-in threat more credible ex ante.

And from the second article:

In view of all this, I believe that two elements will be especially important in making banks more stable: capital and liquidity. Deficits in both of these things were factors which contributed significantly to the financial crisis. The state can bring in regulation to address these deficits, and has done so very successfully.

And on shadow banking:

In terms of financial stability, the crux of the matter is that these entities can cause similar risks to banks but are not subject to bank regulation.And the shadow banking system can certainly generate systemic risks which pose a threat to the entire financial system.

Much the same applies to insurance companies. Although they aren’t a direct component of the shadow banking system, they can also be a source of systemic risk. All of this makes it appropriate to extend the reach of regulation.

Sorry but I will postpone joining the fan club…

Mr. Dombret correctly identifies the issue with the financial system: too much state involvement. What is his solution? More state involvement. It is hard to believe that one person could come up with the exact same solution that had not worked in the past. Were the banks not already subject to capital requirements before the crisis? Even if not ‘high’ enough they were still higher than no capital requirement at all. So in theory they should have at least mitigated the crisis. But the crisis was the worst one since 1929, and much worse than previous ones during which there were no capital requirements. Efficient regulation indeed…

Like 95% of regulators, he makes such mistakes because of his (voluntary?) ignorance of banking history. A quick look at a few books or papers such as this one, comparing US and Canadian banking systems historically, would have shown him that Canadian banks were more leveraged than US banks on average since the early 19th century, yet experienced a lot fewer bank failures. There is clearly so much more at play than capital buffers in banking crises…

Moreover, he views formerly ‘low’ capital requirements as a justification for bankers to take on more risks to generate high return on equity. This doesn’t make sense. For one thing, the higher the capital requirements the higher the risks that need to be taken on to generate the same RoE. It also encourages gaming the rules. This is what is currently happening, as banks are magically managing to reduce their risk-weighted assets so that their regulatory-defined capital ratios look healthier without having to increase their capital.

Mr. Dombret starts by seriously questioning the state’s ability to manage the system and highlights the very harmful and distortive effects of state regulation to eventually… back further and deeper state regulation.

A question Mr. Dombret: what are we going to do following the next crisis? Continue down the same road?

Can please someone remind Mr. Dombret of what a free market economy, which he seems to cherish, means?

Picture: Marius Becker

Banks’ branches/IT problems, and bank regulation vs. freedom

Barclays this week unsurprisingly announced the closure of a quarter of its 1600 branches. A ‘person familiar with the plans of Barclays’ said:

This is a fundamental 100-year transformation of the banking industry, that’s what I think we are seeing.

He/she is right. Though this has been obvious to banking innovators for a while already. SNL expands on that here and mentions high cost/income in retail banking. An analyst:

No bank in Europe can avoid the online banking issue. It is the future of the bank business.

As I have already said, it questions the plans of some of British politicians to cap the market share of large banks. How could their plan work when banks are already slashing branches by the thousands and when new and growing banks are increasingly established online or within other types of stores (see Tesco Bank, which has no actual branch but ‘in-store branches’ within its Tesco supermarkets). Politicians are able to foresee trends and innovation you said? How can one trust people who can only offer yesterday’s solutions to tomorrow’s problems? Same question about general banking regulation…

Anyway, banks also have some serious work to do. Many of them have antiquated IT systems, which makes us think that a transition to an IT-heavy (or perhaps IT-only…) banking business model won’t be smooth… UK banks have experienced a number of IT problems over the past few months (payment systems down mainly) as a result of their underinvestment in basic IT and the accumulation of various systems on top of one another following acquisitions, without never having really tried to integrate them all.

I personally check my accounts a lot more often now that I have access to smartphone apps, and I am certainly not the only one to do so. With the growth of mobile and contactless payments and the reduction in the number of hard cash transactions, the pressure on banks’ IT systems will become enormous. Increased mobile transaction volumes will also impact mobile telecom networks, though they often more rapidly update their systems than banks. What’s going to be interesting is that banks will increasingly rely on the infrastructure of private mobile and internet telcos. This emergent symbiosis may well accelerate the development of mobile networks, in terms of speed, security and coverage.

And banks better be in a hurry. As they now have payment systems competitors such as Paypal or Bitcoin, which ironically would also benefit from the same technological developments. Telcos could potentially also enter the payment space, as Kenya’s Safaricom did with M-Pesa.

Unrelated, a good piece by Sean Ryan on SNL (gated link) called “Bank regulation versus Americans’ freedom”, and reminiscent of one of my previous posts. This is Sean:

The power to regulate banks is impeding the ability of law-abiding citizens to exercise their rights. Washington is full of people with very strong ideas about how the rest of us should live, and I fear that increasingly intrusive bank regulation has given them an opening to do something about it.

[…]

Given the rapid proliferation of nominally legal activities being exiled from the economic mainstream by bank regulators, it seems only a modest exaggeration, and less modest by the week, to suggest that we are incubating a fourth branch of government. And this one isn’t so hamstrung by those pesky checks and balances.

I couldn’t have said it better myself.

Recent Comments