Carney attacks the ‘pretence of knowledge’ of free markets

Some speeches make you want to scream. Mark Carney’s latest is one of those.

In a recent speech titled Three truths for finance, Carney, the governor of the BoE, explains that those ‘truths’ are in fact ‘lies’, and those three lies are “this time is different”, “markets always clear”, “markets are moral”. Where to start?…

According to Carney:

The first lie is the four most expensive words in the English language: “This Time Is Different.”

I can only agree with Carney here. He continues:

This misconception is usually the product of an initial success, with early progress gradually building into blind faith in a new era of effortless prosperity.

He mentions the pre-crisis debt bubble, which ‘financial innovation’ and a ‘ready supply of foreign capital from the global savings glut’ made cheaper. Yet he never mentions central banks’ policies, which kept interest rates low over the whole period, or the fact banking regulation was the very reason behind the cheap credit supplied to a few particular sectors of the economy or also the fact that high saving rates in countries such as China mostly financed high investment rates in the same countries. No, this is due to private actors’ irrationality, who of course believed that this time was different.

But Carney’s logic is faulty. Over the recent years, it is him, and his fellow central bankers, who have kept arguing that “this time was different”, and that we needed to maintain interest rates below the lowest levels ever recorded in human history.

It gets worse when Carney mentions the second ‘lie’, which reveals his deep Keynesian thinking:

Beneath the new era thinking of the Great Moderation lay a deep-seated faith in the wisdom of markets. Policymakers were captured by the myth that finance can regulate and correct itself spontaneously. They retreated too much from the regulatory and supervisory roles necessary to ensure stability.

That “markets always clear” is the second lie, one which gave rise to the complex financial web that inflated the debt bubble.

In markets for goods, capital, and labour, evidence of disequilibria abounds.

In goods markets, there is ‘sluggishness everywhere’. Left to themselves, economies can go for sustained periods operating above or below potential, resulting, ultimately, in excessive or deficient inflation.

He adds:

If markets always clear, they can be assumed to be in equilibrium; or said differently “to be always right.”

First, it is clear that Carney does not understand the dynamic entrepreneurship process that characterises a capitalist economy. Equilibrium does not exist, and markets are in constant fluctuations as entrepreneurs and investors try to identify and benefit from what they perceive as mispricings and profit opportunities (see Israel Kirzner). Equilibrium is at best a theoretical construct, and most economists (mainstream or not) who have studied entrepreneurship and markets know this. In short, the market is a dynamic price discovery mechanism.

As a result, accusing markets of not being in equilibrium completely misses the points of having markets in the first place. If markets are in equilibrium, there is no need to act anymore. No need to come up with new ideas, create and invest.

Second, he mentions financial innovations and their effects as if they had existed in a vacuum, independently of any sort of regulation incentivising their use and distorting market outcomes. But it would mean admitting that policymakers can be dead wrong. Possibly not the message he is trying to convey.

It gets absurd when Carney uses the phrase ‘pretence of knowledge’ (his emphasis):

More often than not, even describing the universe of possible outcomes is beyond the means of the mere mortal, let alone ascribing subjective probabilities to those outcomes.

That is genuine uncertainty, as opposed to risk, a distinction made by Frank Knight in the 1920s. And it means that market outcomes reflect individual choices made under a pretence of knowledge.

I have to applaud. Carney, a Keynesian, used Hayek’s Nobel speech title, to express the exact opposite of Hayek’s idea. In his 1974 speech, Hayek explains that central planners attempting to control the economy were victim of a pretence of knowledge, because it was impossible for them to be aware of all the ‘particular circumstances of time and place’ (a phrase that he uses in most of its post-WW2 literature). Only the private market actor, who was in direct connection to his local market, could attempt to come up with the solution that satisfied the demand expressed by this market.

Yet Carney turned Hayek’s reasoning on its head. According to Carney, it is private market actors who demonstrate this pretence of knowledge as they believe they know what is right for them or what the market actually demands! He seems to assume (wrongly) that economic agents believe they are omniscient and not aware of the uncertainty inherently linked to the economic decisions they take.

Hayek would turn in his grave. He would probably tell Carney that market outcomes are the result of millions of individuals who acted on different assumptions, different risk-assessments, different knowledge and skillsets, and that this is the aggregation of all those various local variables that lead to a market outcome that can more efficiently coordinate dispersed knowledge, skills and demand than any central authority ever can. He would probably add that Carney keeps mentioning market failures without ever referring to most of the reasons underlying those failures, that is, artificial restrictions and distortions that originate in government activity (…and central banks…).

But Carney is likely to never admit such things as he is no free-market lover:

In the end, belief in the second lie that “markets always clear” meant that policymakers didn’t play their proper roles in moderating those tendencies in pursuit of the collective good.

And how would you even know how to ‘moderate’, or simply how to identify, those negative tendencies, Mr Carney? And how do you define what this so-called ‘collective good’ is? ‘Pretence of knowledge’ you said?

He then insists (his own emphasis, which says a lot):

Despite these shortcomings, well-managed markets can be powerful drivers of prosperity.

Carney’s last ‘lie’, that markets are moral, suffers from a lack of arguments. He seems to base most of his ‘markets are amoral’ rhetoric on recent examples of price-fixing in a number of rates and commodities markets. He is right that fraud is reprehensible. Yet, in those cases, it was not markets that were to blame, but a few abusers who tried to benefit at the expense of the markets. Here again Hayek would argue that there is nothing more ‘moral’ than unhampered markets that distribute services to those that need them and reward those that provide them, within the framework of the rule of law.

At the end of his speech, Carney introduces the recent BoE initiative to open a forum on re-building ‘real markets’ (his emphasis again). You want ‘real’ markets Mark? Just release them from their constraints. It’s as simple as that.

Another nail (or two) in the coffin of endogenous money theory?

Ben Southwood sent me the following new piece of research. The abstract is telling:

We provide empirical evidence for the existence, magnitude, and economic cost of stigma associated with banks borrowing from the Federal Reserve’s Discount Window (DW) during the 2007–2008 financial crisis. We find that banks were willing to pay a premium of around 44 basis points (bps) across funding sources (126 bps after the bankruptcy of Lehman Brothers) to avoid borrowing from the DW. DW stigma is economically relevant as it increased some banks’ borrowing cost by 32 bps of their pre-tax return on assets (ROA) during the crisis. The implications of our results for the provision of liquidity by central banks are discussed.

MMTers and other endogenous money theorists are very mistaken to ignore this very important phenomenon, which questions the very validity of their whole theoretical framework.

Meanwhile, SNL reports (via Valor Econômico) that Brazil is weighing up relaxing reserve requirements to boost the supply of credit. Impossible according to endogenous money theory. Unless…

In fact, Brazil plays with reserve requirements all the time. It already lowered them in May this year, in July 2014, and even in September 2012. In contrast, it had raised them in 2010 to counter inflationary pressure. Perhaps those policies did not have any effect, as endogenous money theory would speculate. In fact, research published in June 2015 on the effects of Brazil reserve requirement changes does highlight impacts on lending:

We compare the macroeconomic effects of interest rate and reserve requirement shocks by estimating a structural vector autoregressive model for Brazil. For both instruments, discretionary tightening results in a credit decline. Contrary to an interest rate shock, however, a positive reserve requirement shock leads to an exchange rate depreciation, a current account improvement, and an increase in prices.

Endogenous theorists (including some economists at the BoE) claim that their models reflect the reality of ‘modern’ fiat monetary and banking systems. A quick look at the facts seems to prove them wrong.

PS: the Farmer Hayek blog published a short interview of me over three posts. The first post covers why inflation seems low in the US. The second post what economists get wrong about banking. And the last post what my thoughts were on NGDP targeting and free banking.

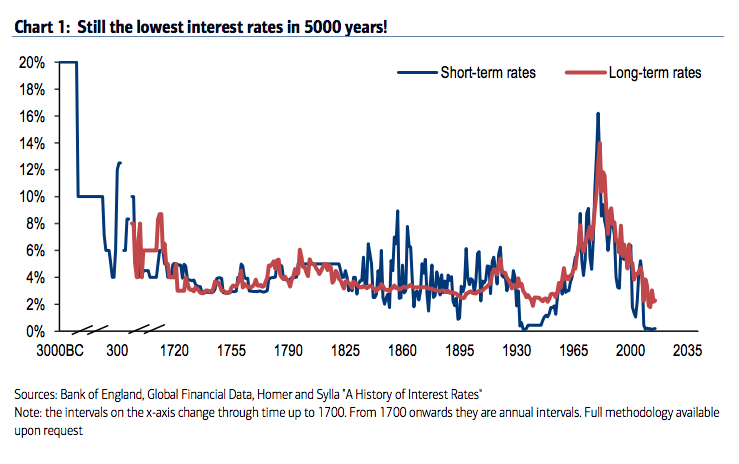

150 years of nominal interest rates distortion?

A very useful post was published on the FT Alphaville blog by David Keohane. It shows nominal interest rates levels over the past 5000 years in three different charts.

The first one comes from Andy Haldane, from the BoE:

The second one from Hartnett, from Bank of America Merrill Lynch:

The last one comes from Costa Vayenas, from UBS:

Those charts use different sources so don’t look exactly the same. Nevertheless, they all show the same striking facts. In particular, the 20th and 21st centuries seem to have been huge monetary experiments: nominal rates went both sky high and negative within a few decades… Within a period of barely more than a 100 years, rates fell to the bottom (Great Depression), then jumped ridiculously high to counteract inflationary pressure in the 1970s and 1980s (i.e. the disastrous impact of crude Keynesian macro theory) that resulted from the money multiplier recovering after the Depression, then fell to the bottom again or even negative (Great Recession).

Remember: the 20th century was the period of the generalisation of central banking. It definitely looks like they have been successful at stabilising money markets (and remember this paper by Selgin and White, which shows how successful the Fed has been at stabilising the value of the dollar since its creation). In short, great success for central bankers*.

Another interesting fact is that nominal rates started to wildly fluctuate once the BoE was granted the exclusive right to issue banknotes in the London area in 1844. Unlikely to be a coincidence.

Something that worries me though is the current state of monetary policy throughout most of the Western world. Rates are stuck at the zero bound or even went negative for the first time in history. Perhaps this is justified. But I keep wondering whether our economies currently are in a worse state than at any time in history to justify such low rates (although to be fair, Haldane’s chart does show that long-term nominal rates remain around historical levels – but not Hartnett’s).

Real interest rate charts would also have been interesting for a more comprehensive analysis of the underlying drivers of the rate movements we see here. If ever anyone has access to real interest rate data that go back several hundred years, please let me know (probably hard, or even impossible, to obtain as historical inflation data is likely to be non-existent).

In a parallel world, the BoE recently opened a forum weirdly titled ‘Building real markets for the good of the people’ which, putting aside the slightly communist tone of its chosen name, describes markets are “prone to excess” if “left unattended”**. This is another great example of central banks succeeding in making public opinion believe that economic issues originate, not in central bankers’ failed policies, not in economically distortive banking regulation, but in free markets. Which aren’t actually free. Here again Selgin had a remarkable article reporting how the Fed promotes itself.

One reaches some sort of supreme irony after contrasting those BoE statements with the charts above. Worse, central banks’ power, despite the instability they have brought to the economy for 100+ years, is growing, and their adherence to the rule of law has all but vanished (see Salter here and here arguing that a stable monetary framework such as the gold standard or NGDP targeting would respect the rule of law, unlike current regimes, and that adherence to the rule of law should be the primary consideration for judging monetary regimes).

*Sarcasm, of course

**I’m not sure what’s going on at the BoE, but a culture shift seems to be happening: anti-market rhetoric and rather strange monetary and banking theories are overtaking the institution (see my posts on endogenous money theory)

Blockchain everywhere

Banks are both scared and overexcited. Blockchain has the potential to fundamentally alter their business model, and they know it. Understanding tomorrow’s financial tech has become key to minimise business risks, key to remain relevant. A race that all financiers have joined is now going on, despite mocking Bitcoin just a couple of year ago. And blockchain is all over the news, despite most bankers having little to no understanding of what it is about. Financiers of all sorts now back blockchain-based technologies, from credit card companies to stock exchange and banks.

So a few weeks ago the NYT ironically remarked that:

Nowhere are more money and resources being spent on the technology than on Wall Street — the very industry that Bitcoin was created to circumvent.

Bloomberg reports that Blythe Masters, former MD at JPMorgan who helped kick start the credit default swap market, was now CEO of a blockchain startup, Digital Asset Holdings. Probably not what Satoshi Nakamoto, Bitcoin’s legendary creator, was expecting indeed. She says that, as I have explained on this blog, banks could massively benefit from blockchain technology if it can simplify back office operations. That is, if banks aren’t completely disintermediated first.

Matt Levin reflects on Masters’ comments and wonders why it is taking so long for the financial sector to eventually implement systems that drastically cut error-prone settlement delays (that can still be longer than 20 days, in the internet era…), and says that blockchain for banks can’t hurt. It’s certainly true, although don’t expect miracles: it’s going to take a few attempts, and perhaps a few failures or even mini-crises, for a blockchain-based system to evolve into something solid. And if it turns out that blockchain cannot offer a lasting, bulletproof solution, it will disappear.

Masters also declared that US banks were rather slow at looking at potential blockchain solutions. And indeed, most banks that seemed very active in that area, at least that I have heard of so far, were not US-based. Many of them were European, perhaps reflecting the fact that they currently are under more profitability pressure than their US peers. UBS, for instance, has been very vocal about its blockchain initiatives. See also this quite complex article on IBTimes on the various technologies behind UBS’ ideas, which include private blockchains, sidechains (transfer of assets between multiple blockchains) and ‘settlement coins’ (essentially a fiat money representation on blockchain that relies on central banks’ settlement processes):

Recently, UBS demonstrated how a bond could be automated on a blockchain, the shared ledger system similar in design to that used by Bitcoin. It also proposed a fiat currency-backed “settlement coin” to fit within the existing regulatory framework. The bank appears to be leading the way in distributed ledger technology at this time.

What’s happening is fascinating. What’s going to finally emerge remains a mystery. While individual institutions can put in place private blockchain-type systems to cut costs or offer more effective dark pool services to a selection of customers, the implementation of a ‘stock-market replacement’ blockchain requires an industry-wide agreement. And it does seem to be happening. A couple of days ago, the FT reported that 9 of the largest banks agreed to cooperate on a blockchain initiative that would define common standards and protocols (I’d just like to add that this is another example of private market actors cooperation; no need for a state to devise that sort of things in most, if not all, cases).

But blockchain technologies don’t only apply to financial services. The NYT mentioned property titles, diamond and gold ownership, airline miles. But also the music industry. And certainly a lot of other ones, as some at the MIT seem to believe with their Enigma project, or some entrepreneurs I met a few months ago at a conference, who believed that entire applications such as Facebook could be transferred onto the blockchain. It’s now ‘blockchain everywhere’.

PS: I’m on holidays abroad so have little time for updates!

Bank accounting standards can worsen recessions

There is a row over the new IFRS 9 standards. Those are new accounting rules supposed to be introduced by 2018 (outside of the US). As this FT article summarises:

Banks were unable to book accounting losses until they were incurred, even though they could see the losses coming. At times the incurred loss rule meant banks overstated profits upfront and did not make prudent provisions against expected losses, particularly in areas such as loans secured against property.

Now, as I said a few weeks ago, accounting rules seem to mostly respect the rule of law as described by Hayek, by experimenting, learning from their mistakes and evolving, step by step. The process can be slow and the experiment can turn wrong in the short run. Whether IFRS standards have respected this process is arguable.

A FT editorial declares that banks should not be able to game the rules, whatever that means. Hence it welcomes the changes. Not everyone agrees. But the FT column is contradictory. It complains that banks were “slow to react to emerging problems when the financial crisis struck” and that “they allowed outright concealment of economic realities” by shifting some assets from fair valued portfolios (i.e. marked to market) to held-to-maturity ones (i.e. reported at amortised cost). This may be right, but I’m not sure.

First, is this really ‘gaming the rules’? No, it is simply applying the rules. Second, I’ve always doubted that mark-to-market accounting really reflected the ‘fair value’ of an asset. It reflects its market price at a given time. Which isn’t the same thing. Markets panic, in particular during financial crises. This tends to temporarily amplify fluctuations in market prices. Volatility increases widely. By holding assets at fair value, you can be bankrupt on Monday and solvent on Friday. When markets have lost all notion of a fair, or equilibrium, price, it is silly to speak about banks’ assets being ‘fair valued’. This can only happen once markets have calmed down and prices only fluctuate marginally around a certain level.

Friedman and Kraus, in their great book Engineering the Financial Crisis, describe how AIG could have survived if it, counterparties and US regulators had waited a few months so that the market price of a number of its trades recovered. It could have then potentially avoided a bail-out. I don’t know the circumstances of Lehman Brothers in detail, but it is certain that its insolvency was partly triggered by short-term price fluctuations that forced short-term asset write-downs.

In fact, mark-to-market accounting can amplify recessions by making banks’ balance sheets look much worse than they really are. The result of which is that banks drastically reduce lending and lay off staff, aggravating the collapse in aggregate demand beyond what would have happened had those accounting rules not been in place. For instance, a lot of structured financial products lost half or more of their market value during the crash, but only a tiny portion actually defaulted! (see here and here) Is it worth penalising financial institutions and, in fine, the economy, for temporary changes in prices? Beware what you wish for.

Apparently, even Milton Friedman blamed mark-to-market accounting for many bank failures during the Great Depression (I don’t have an original source though; perhaps in the Monetary History of the United States, but I can’t recall).

Let’s get back to our provisioning methods. The ‘incurred loss’ model wasn’t perfect: banks under IFRS were not free to provision the amount they wanted when they wanted, the goal being to prevent bankers from ‘managing’ their profits. While this can be a laudable goal, this is also risky: as with the conflict between marked-to-market and amortised cost accounting rules described above, ‘managing’ profits can dampen economic booms and busts, at the expense of short-term financial statement reliability.

Under the new ‘expected loss’ model, banks will have to provision upfront on all loans, although only over the following 12-month period according to my understanding. It still doesn’t give banks much flexibility and only changes the timing of the provisioning. A loan becomes costlier at origination, but not over its lifetime. But as often, the comments on the two FT articles are more interesting than the article itself. And some worry that those new standards have pro-cyclical features, by statistically requiring higher level of provisioning at origination during recessions, thereby mechanically requiring more capital. Which of course would be likely to impair banks’ lending appetite when they already struggle to make decent returns on their existing capital base.

Perhaps the less economically distorting way would be to go back to pre-WW2 loan loss provisioning standards: there were apparently none. It is now well-known that 19th century and early-20th century banks used to hold a lot thicker capital buffers.

While there are many reasons why equity buffers fell (better institutional framework, better access to information, more diversified business models…), accounting standards are another reason: they progressively created loan loss reserve accounts from WW2 onwards, originally for tax reasons (see Walter here). Loan loss reserves’ purpose was to provide a buffer for expected losses, whereas equity mostly became a buffer for unexpected losses. Before that, equity was an all-purpose buffer and loans were not provisioned but directly ‘charged-off’. In the US, only 38% of banks had loan loss reserve accounts in 1948. By 1975, 94% of them did.

So to be fair with banks, the chart above should add provisioning (which is a ‘negative’ asset) to equity. A back of the envelope calculation I made some time ago seemed to show that equity/asset levels would rise by 100/300bp. Still below late 19th century levels, but not as bad as many believe. By letting bankers decide the amount of the buffer (reserves or equity) and the timing of its increase/decrease, some banks would inevitably fail, but it is also likely that, on aggregate, stability could be enhanced as pro-cyclicality is reduced.

I am not saying here that there should not be any accounting rules in place. Those would be necessary to provide investors with relatively accurate information (and there have been discussions and proposals to radically change provisioning methods. See Kerr here). But too much rigidity leading to very accurate statements at a point in time that would then be completely undermined a few months later as a crisis strikes and losses are revealed, is of limited use. And economically damaging. There might be other middle way options that I am missing, but available choices seem to me to be: point-in-time accurate and long-term inaccurate or point-in-time inaccurate and long-term accurate.

PS: See also this interesting BIS paper that reviews the literature on the relationship between accounting rules, regulation and business cycles. It takes a different view on fair value accounting and says that there is no real conclusive evidence that fire sales occurred and damaged banks’ balance sheet as a result. Maybe, but fire sales by banks don’t have to occur to make mark to market losses on assets. It also finds some pro-cyclicality due to provisioning rules, but research is preliminary and sometimes contradictory.

Cash is a vital barbarous relic

The FT recently published a column calling for the retirement of cash, this ‘barbarous relic’ (a reference to Keynes on the gold standard in his Tract on Monetary Reform). The author takes the view that, because “by far the largest amount of money exists and is transacted in electronic form”, cash has become almost irrelevant. Worse, the little amount of cash circulating in society could “cause a lot of distortion to the economic system” and “limits central banks’ ability to stimulate a depressed economy” because people could convert their deposits into cash if the central bank decides to apply negative interest rates far below zero on deposits. And, worst of all, cash is anonymous:

The second feature of cash is that, unlike electronic money, it cannot be tracked. That means cash favours anonymous and often illicit activity; its abolition would make life easier for a government set on squeezing the informal economy out of existence.

The whole article is filled with economic fallacies and what quite a few commenters called ‘fascist’ and ‘authoritarian’ measures. While I wouldn’t go as far as qualifying such views as ‘fascist’ they are surely ‘authoritarian’, and it is frightening to see that some people (including some leading economists) are willing to give up a part of their freedom to allow central authorities (either the state or a supposedly independent central bank) to monitor and control the activities of all their citizens. Here again, as usual with interventionists of all sorts, any notion of Public Choice has been forgotten: governments seem to be well-meaning, omniscient and omnipotent organisations, which would also become omnipresent if such measures were adopted. This would give governments free rein to oppress people in a subtle way or another, whether bureaucrats were right or wrong.

One commenter, in a superb reference to Star Trek (and to the concept of separation of Church and state), summed up my view with the statement that (his emphasis)

The world needs separation of money and state, not a melting consolidation of the double helix into the Borg.

A response letter to this column is also reassuring:

The state can more easily levy a value added tax in order to make tax collection easy. How nice! Here — let me put my cash in the bank in order to make it easier for government to tax it away. Then you conclude your support of the cashless society with the caveat that we minions might, just might, be allowed to carry some cash . . . but at a cost. Our cash could carry an expiration date, for example.

As you state: “The benefits of cash are significant — but they need not be offered for free.” A more Orwellian statement would be hard to find.

But, besides the threat to liberty that a suppression of cash represents, I wish to offer here another economic reason why banning cash is a bad idea.

Cash is a control system on the banking industry. Cash, which represents banks’ reserves and most liquid assets, has been the main control tool that has kept bankers in check for centuries. The threat of deposit (i.e. claims on cash) outflow prevents banks from overexpanding, mostly through the adverse interbank clearing (mostly for individual banks) or outright withdrawal (for the system as a whole, see what happened in Greece, the most extreme version of this being a bank run) mechanisms. This is a pure market discipline effect. The fact that, in normal times, most financial transactions are done electronically is irrelevant. It is because people still have the last resort option to withdraw their deposit that makes cash such a potent control tool.

Of course, some banks are mismanaged and become illiquid from time to time. Liquidity risk is one of the main risks faced by banks and is carefully monitored, despite what some endogenous money theorists, who claim that reserves would always be supplied in case of need (while forgetting the demand side of the equation), seem to imply.

There is one option though: physical cash could be retired, as long as electronic cash could be withdrawn and stored outside of the banking system. This is the Bitcoin-solution: people can keep their Bitcoins in encrypted electronic wallets on their phones or computers, which are not accessible by outsiders (unlike bank deposits).

Retiring cash outright would however unlock a crucial financial stability mechanism, which was already weakened by the introduction of deposit insurance. Several studies have indeed controversially found that deposit insurance, which tends to reduce the pace of deposit outflow, has a detrimental effect on bank stability (see Demirguc-Kunt and Detragiache here, Calomiris here, Chu here), despite what Diamond and Dybvig claimed in their famous (but flawed) model in 1983. Far from improving financial stability and allowing central banks to ‘manage the economy’ (as if this was actually possible), the suppression of cash would be a step closer to the ultimate moral hazard.

PS: I’m also curious as to what the impact of the suppression of cash on charity would be (or for tips at restaurants and elsewhere for instance). What would you reply to the question “can you spare a coin”? “What’s your bank account number?”?

Photo: Newport webpage

Natural interest rates are dead, the BIS (indirectly) says

In May (I only found out a couple of weeks ago), the BIS released a big report titled Regulatory change and monetary policy, in which it investigates the effects of the new banking regulatory framework on market interest rates and the implied consequences for the conduct of monetary policy. By the BIS’ own admission, the whole yield curve has nothing ‘natural’ left.

The report is an interesting, though pretty technical read. It is also scary. Scary to see how much banking regulation is affecting interest rates all along the yield curve across most banking products. Scary to see that the suggested remediation by the BIS is more central bank involvement to counteract the effects of those regulations.

Of course, the Basel framework originates from… Basel in Switzerland, where the BIS is located, and where BIS experts have spent years drafting apparently clever rules to make our banking system apparently safer, in spite of all historical evidences and what we’ve learned about the spontaneous order of free markets (remember: “banking is different” they say). So I wasn’t expecting this BIS report to declare that the very rules it put in place was endangering the economy. And indeed it doesn’t. But it does admit that there will be ‘impacts’, which of course will be ‘limited’ and ‘manageable’. They always are.

I won’t replicate here everything that’s in that report. It’s way too long and I’ll let you take a look at it if you’re interested. There is a quite detailed description of the potential effects of the Liquidity Coverage Ratio, the Net Stable Funding Ratio, the Leverage Ratio and the Large Exposure Limits on banks’ product pricing and volume and the impact on central bank’s monetary policy operations. And despite its 30+ pages, the report isn’t even comprehensive. It forgets to look at the large distortive effects of risk-weighted assets and credit conversation factors.

What I’m going to show you below is merely the BIS researchers’ own conclusions, which they neatly summarised in handy tables. This is what they view as the potential changes in money market interest rates:

By their own admission, the cumulative effect of those new rules is unclear. And even when they believe they know which way the interest rate will move, it remains a best guess. To this table you can add the hugely distortive effects of RWAs and CCFs, which I have described on this blog a number of times.

The only conclusion is that there is no free market-defined Wicksellian ‘natural’ interest rate anymore in the marketplace. As interest rates are manipulated by regulatory measures in myriads of ways, entire yield curves across the whole spectrum of banking products and asset classes stop reflecting the pricings that market actors would normally agree on in an unhampered market. The result is a large shift in the structure of relative prices in the economy.

The economic consequences are likely to be damaging (and it is clear, at least to me, that RWAs have already done a lot of damages, i.e. the financial crisis), even though the BIS reckons that central banks could potentially offset some of those interest rates movements:

More central bank intermediation: Many of the new regulations will increase the tendency of banks to take recourse to the central bank as an intermediary in financial markets – a trend that the central bank can either accommodate or resist. Weakened incentives for arbitrage and greater difficulty of forecasting the level of reserve balances, for example, may lead central banks to decide to interact with a wider set of counterparties or in a wider set of markets.

In addition, in a number of instances, the regulations treat transactions with the central bank more favourably than those with private counterparties. For example, Liquidity Coverage Ratio rollover rates on a maturing loan from a central bank, depending on the collateral provided, can be much higher than those for loans from private counterparties.

Problem is (and the BIS also admits it): there is no way non-omniscient central bankers know by how much and in what direction rates should be offset. We here get back again to the knowledge problem. There is no way the central bank can act in a timely manner. It is also unlikely that central bankers could act free from any political interference. Finally, even if central banks managed to figure out what the ‘natural’ rate is for a given asset at a given maturity, central banks’ policies are likely to have unintended consequences by altering the rates of other products and maturities.

The effectiveness of the transmission mechanism (banking channel) of monetary policy is more than ever questioned. Rates will move in unexpected ways. And, as the BIS describes, banks could simply opt out of monetary programmes altogether:

The question is whether there are exceptional situations in which banks would refrain from subscribing to fund-supplying operations because concerns over the LR impact of the reserves that would be added to the banking system in aggregate outweigh the financial benefits accrued by participating in the operations. If so, this lack of participation could prevent a central bank whose operating framework entailed increasing the quantity of reserves from meeting its operating target.

The BIS believes that “the changing regulatory environment will, by design, affect banks’ relative demand across various types of assets and liabilities”. It summarises the potential changes in the demand for central bank tools below:

Here again, a lot of uncertainties remain.

Something looks certain however. The involvement of central banks in the financial and economic system is likely to become more intense. As regulations bound banks’ behaviour and prevent an effective allocation of capital, central banks are increasingly going to step in to boost or restrict the supply of credit to certain market actors and asset classes. See what happened with SMEs, starved of credit as Basel makes it too expensive to extend credit to such customers, while central banks attempted to offset this effect by starting specific lending programmes (such as the Funding for Lending scheme in the UK). We are here again back to Jeff Hummel’s arguments of the central bank as central planner.

Nonetheless, I am certain that capitalism and free markets will get blamed for the next round of crisis. It is becoming urgent that we replicate the achievement of academics such as Friedman and Hayek, who managed to overturn the nonsense post-War Keynesian consensus. Sadly, free markets academics seem to have virtually disappeared nowadays or at least cut off from most policymaking positions and public debate.

Recent Comments