Is Greece invalidating endogenous money theories?

Most of you already know the trouble Greece is in. What’s interesting is that, what’s happening to its banking system seems to not really reflect the view of some endogenous money theorists…

As Tim Worstall points out on the ASI blog, if banks really were able to create money out of thin air, the Greek banking system would have no reason to be on the brink of collapse for liquidity reasons (I won’t be mentioning insolvency risks here). Worstall’s blog post is admittedly overly-simplistic: while modern monetary theory (MMT) does believe in endogenous outside money creation, it remains more realistic and plausible than some of the alternative endogenous theories such as that of the authors of the BoE research paper I challenged a few weeks ago, and which I believe Worstall was in fact targeting.

Remember, this BoE staff paper was stating:

The bank therefore creates its own funding, deposits, in the act of lending, in a transaction that involves no intermediation whatsoever.

Well, the fact that Greek banks had to close for a whole week to prevent liquidity shortage seems to me to say a lot about their ability to create their own funding… See below a chart from the WSJ that clearly invalidates this view. As deposits are taken out of the system (= reserves withdrawal), Greek banks have had to replace the funding loss with central bank borrowing in order to remain liquid:

But in the case of Greece, even the supply side assumption is under pressure: under the ELA programme, the ECB is only willing to provide limited liquidity to Greek banks, and against good quality collateral.

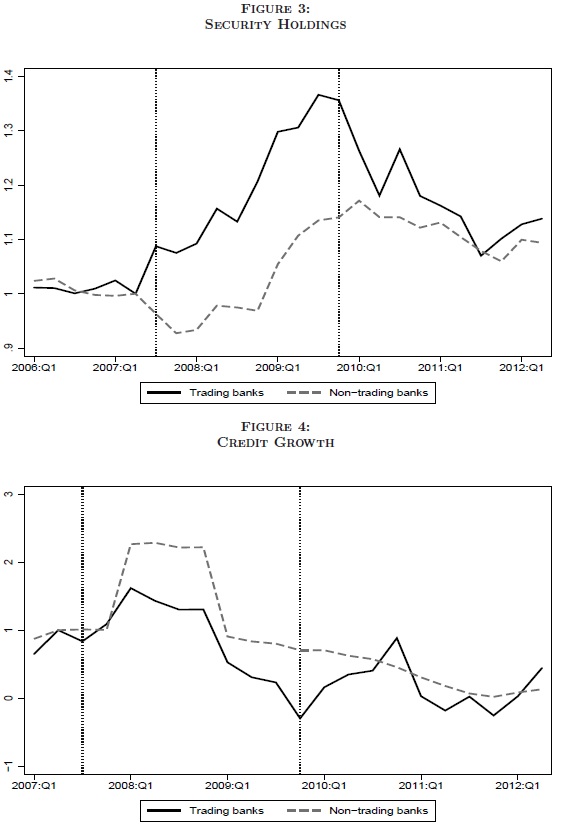

But that’s not it. Some Bundesbank staff members also just published a new research paper titled Securities trading by banks and credit supply: micro-evidence, which attempted to understand the implications of variations in trading activity on the supply of credit to the economy. In theory (simplified loanable funds model), banks have only one resource pool (= reserves) to use on two possible options: lending to customers or buying securities*. In a world of scarce resources, increasing one should decrease the second. However, endogenous money theorists would say that this dichotomy is a myth; that banks are not constrained by the availability of reserves and hence can expand both activities at the same time as long as it makes economic sense. According to them, the only real constraints on banks are regulatory ones such as minimum capital requirements.

What did the researchers find? (my emphasis)

We find that banks with higher trading expertise increase their overall investments in securities during a crisis, especially in securities that had a larger drop in price. Furthermore, this effect is more pronounced for banks with a higher level of capital and in lower-rated and long-term securities. In fact, we do not find significant differential effects for triple-A rated securities. Interestingly, the overall ex-post returns are about 12.5% for trading-expertise banks in the crisis. In contrast to behavior in securities markets, banks with higher trading expertise reduce their overall supply of credit in crisis times. The estimated magnitude of decrease in lending is approximately five percentage points. The reduction in credit supply is more pronounced for trading banks with higher capital. We also find that the credit reduction is binding at the firm level. Given that credit from banks with trading expertise constitutes a large fraction of overall credit in Germany, and that Germany is a bank-dominated economy, the results suggest that this could have a significant impact on the availability of credit to firms during the crisis at the macro level.

In short, the paper found that increased securities trading crowded-out lending in crisis time, despite banks not being constrained by regulatory capitalisation. While the paper is unclear about the effect of trading in non-crisis time given the much smaller fluctuations in volume, and while it doesn’t fully invalidate the MMT and other endogenous views, the results are definitely interesting and seem to provide empirical validity to the traditional loanable funds model.

*Of course, it’s not that simple and banks can indeed create claims on base money/reserves that are themselves used as money. But they are constrained by the availability of base money to do so. See my multiple posts on the topic.

HT: Ben Southwood

Update 1: The fact that the ECB is not willing to provide an infinite amount of reserves to Greek banks may not be such a challenge to the MMT version of the endogenous theory framework after all. The collateral that Greek banks can provide mostly comprises Greek government bonds, which are ‘barely’ acceptable as collateral under ECB rules. I am not an MMT expert (only know their banking theory), but they seemed to indicate that sovereign indebtedness wasn’t such an issue. So the EU/ECB institutional framework and rulebook may not be a real challenge to the MMT banking theory, but I would qualify it as a potential ‘weakness’ (which needs more analysis).

Update 2: MC Klein has an interesting post on the FT Alphaville blog. He points out that a number of Greek banks were given a clean bill of health during last October’s EU stress tests and so solvency shouldn’t be an issue, at least according to the EU. However, Draghi doesn’t seem to honour his ‘whatever it takes’ promise, despite the supposed health of Greek banks. So in the end, the potential ‘weakness’ I mentioned above may well be more challenging than that for the MMT version of the endogenous money theory.

Update 3: Also see this chart from this speech from Lowe, Deputy Governor of the Reserve Bank of Australia, and notice how funding types growth offset each other.

23 responses to “Is Greece invalidating endogenous money theories?”

Trackbacks / Pingbacks

- - 3 September, 2015

Leave a comment

Recent Comments

| pslebow on ‘Sovereign money’:… | |

| pslebow on A critique of Werner’s view on… | |

| Hugo Kramer on Welcome to Spontaneous Fi… | |

| Nathan on A critique of Werner’s view on… | |

| Nathan on More, more, more money endogen… |

I recently wrote a paper on expansion of credit in Africa. My findings were that African banks had mostly funded the growth in lending through a massive growth in customer deposits (and not foreign currency funding for example) . One of the review comments I received was “loans create deposits” and therefore my analysis was wrong headed. When is someone going to confront this heresy of “loans create deposits”. Why is “loans to deposits” ratio important then? BIS seem to be the only people advocating for stable bank funding through customer deposits….

Sorry for the late reply, only back to blogging now!

Agreed, the ‘loans create deposits’ view seems to be unaware of the whole issue of bank funding (which they often called internally ‘collecting deposits’).

I believe you misunderstand the endogenous money view. Loans do create deposits in aggregate.On the other hand, a single bank can receive deposits when e.g. a depositor switches to that bank from another one, and that bank will by definition acquire more reserves. But this only means that the bank that the depositor left lost an equal amount of deposits and reserves.

Endogenous money does not dispute that a single bank does not try to attract deposits, since it’s the cheapest way to acquire reserves. But in aggregate its the loans that necessarily create deposits.

Did you try to read all the posts I wrote on the topics?

I suggest you do.

You may also want to have a look at this Bank of England bulletin, where they essentially endorse the endogenous view of money creation: http://www.monetary.org/wp-content/uploads/2016/03/money-creation-in-the-modern-economy.pdf

I know it of course. And it is full of contradictions, as I wrote there:

Also, it’s not the view of the BoE. It’s the view of *some* economists within the BoE. And they’re wrong.

What about Canada,Australia, New Zealand et. al. where they have no reserve requirements ?

You keep referring to points I have addressed in other posts, and I’m not going to rewrite the whole thing here.

Sorry for not being a frequent reader of your blog to know when and what you have addressed. You could at least direct me to the relevant post.

I have only noticed you claiming that in systems with no reserve requirements, banks *still* maintain a level of reserves that they deem appropriate for settlement needs.

I fail to see how this goes against the endogenous money view (it does not claim that banks have no use or need for reserves at all). The point is that if there are no reserve requirements, then how are banks constrained by the quantity of reserves?

On the other hand, you have mentioned elsewhere countries with reserve requirements e.g. Turkey or China where variation on the minimum required reserves proved successful for monetary policy.

First let’s make it clear that an endogenous money system or one of fractional reserve banking is not a natural law. Rather it is a matter of choice. The implication is that if a central bank chooses an interest rate as an intermediate target, then by definition it must let the quantity of reserves float. On the other hand, a CB that chooses the monetary base as its intermediate target then it will again by definition loose control of the interest rate. Unless you are claiming that one can control both quantity and price.

I am claiming that they can control neither. They can only attempt to influence one of those (often with disastrous results).

As for my writings, I earlier gave you the link of a piece I wrote criticising the BoE economists paper, from which you can access some of my longer critiques. You can also just search ‘endogenous’ on this blog.

But as it looks like this is a little complex, see the endogenous money section of this post:

Since then, a few other things were written but that’s a good start.

My comment is too late but I accidentally stumbled upon this post.

Money endogeneity does not imply unlimited balance sheet expansion regardless of solvency, or for that matter, political issues.

Endogeneity implies that a solvent bank will always be able to obtain liquidity. Truth is, Greek banks are largely insolvent, but for other reasons, they managed to come out of the stress tests just fine. That the ECB decided to restrain liquidity for banks that it itself declared solvent is not a flaw of the endogenous view of money.

Sorry for the late reply.

“Endogeneity implies that a solvent bank will always be able to obtain liquidity.”

Not necessarily, price is an issue, and more importantly, liquidity is an issue. Liquidity is a specific form of solvency and is monitored by market participants.

Hi again !

I’m not sure I understand your argument.

For starters, I believe liquidity and solvency are different matters. An asset/ liability mismatch in terms of maturity is solved differently than an outright insolvency. For example see the criticism on the handing of the IMF of the FI’s trouble during the Asian crisis. The argument was that they treated an illiquidity problem as one of insolvency.

And then, we should also remember why Central Banks were created in the first place. I cannot recall other episodes of Central Bank’s denying liquidity to solvent banks. Especially when the CB itself has deemed them solvent. After all, why would a “liquid” bank require liquidity assistance?

Well, I suggest you try to borrow money with repayment due 2020 for a project whose cash flows are only expected in 2030 and then attempt to convince your bank that, if you can’t pay it back, it’s not that you’re insolvent but merely that you’re illiquid.

I’m sure it will go down well!

And since when private borrowing is the same as Central Bank liquidity operations? How bank runs are to be avoided (and HAVE been avoided) if central banks refuse to provide liquidity to solvent banks ? The Fed was created precisely to reduce bank run episodes. How has it achieved that if not by providing liquidity on demand to solvent banks ?

I think you misunderstand my point.

‘Solvency’ can be a question of point of view. Central banks are supposed to exert judgement as to whether the institutions they lend to are solvent. And the difference between solvency and liquidity are not always clear cut. Are banks just having a temporary liquidity problem because some customers had a temporary cash flow issue or does this represent a solvency event? Asset/liability management is not just a question of liquidity. An event of default is an event of default, whether or not the bank will have the ability to pay next week or next year: it still defaulted on its obligation.

As to the success of the Fed, well…

When have banks run been avoided thanks to central banks? I can’t recall. I do recall the queues in front of Northern Rock and the runs on some of the US banks during the crisis though.

Further, turning back to the Asian crisis, I wonder how your “repayment due 2020 with cash flows by 2030” resembles the bank run there? Hell, even the run on Greek banks? The bank run would have been halted had the central banks intervened to ensure depositors are not going to loose their money. If panic would have been containted, withdrawals would decline, hence there would not be such a large bulk of liabilities “maturing” immediately.

By the way:

“Seasonal Accommodation and the Financial Crises of the Great Depression: Did the Fed “Furnish an Elastic Currency?”

Click to access Seasonal_Nov_Dec1992.pdf

“Are banks just having a temporary liquidity problem because some customers had a temporary cash flow issue or does this represent a solvency event? Asset/liability management is not just a question of liquidity. An event of default is an event of default, whether or not the bank will have the ability to pay next week or next year: it still defaulted on its obligation.”

So a bank with e.g. negative net worth, or weak capital ratios is the same as a bank that is having a run of depositors which would have been avoided had the CB stepped in. No wonder then why you mention Northern Rock, when my initial comment was that endogenous money view implies that a solvent bank can always acquire reserves on demand.

Somehow an illiquid bank is largely similar to an insolvent one to you, yet Northern Rock was liquid (and solvent enough) that the run it experienced is evidence of the inability (and failure) of central banks to halt bank runs? Talk about being contradictory.

I think you are missing fundamental reasons why there would be a run on specific entities in the first place.

There have been multiple runs during the crisis. Central banks cannot control everything. You seem to take a lot of things for granted.

“One of the core ideas of central banking is to provide an “elastic currency”, i.e. one in which the important transitory fluctuations in base money demand

no longer need to disturb via interest rate effects economic conditions. What matters for the key economic decisions, namely to save or consume, to borrow and invest, are interest rates mainly of medium and longer maturity. With an extreme (and non-white noise) volatility of short-term rates, volatility of longer-term rates will also increase. Such volatility will create noise in

economic decisions, and hence lead the economy away from equilibrium. Therefore, a necessary condition for promoting monetary base targeting seems to be that interest rates do not matter at all”

https://www.ecb.europa.eu/pub/pdf/scpwps/ecbwp372.pdf?45b110aa94d14117d8ed98277c4d55a4

If that’s not a clear indication for the existence of endogenous money then I don’t know what is.

@crossover: what happened to the link between micro and macro economics? if at the micro level “deposits create loans”, why would that turn upside down at the macro level and become “loans create deposits”