Hayekian legal principles and banking structure

The latest CATO journal contains a truly fascinating article (at least to me) of George Selgin titled Law, Legislation, and the Gold Standard. Selgin roots his arguments in Hayekian legal theory, as developed by Hayek in his books The Constitution of Liberty and Law, Legislation and Liberty*.

Hayek differentiates ‘law’ (that is, general backward-looking ‘meta-legal’ rules that follow the principle of the rule of law) from forward-looking ‘legislation’, which is unfortunately too often described as ‘law’ despite not respecting the very fundamentals of the rule of law. As such, Hayek describes the rule of law as being

a doctrine concerning what the law ought to be, concerning the general attributes that particular laws should possess. This is important because today the conception of the rule of law is sometimes confused with the requirement of mere legality in all government action. The rule of law, of course, presupposes complete legality, but this is not enough: if a law gave the government unlimited power to act as it pleased, all its actions would be legal, but it would certainly not be under the rule of law. The rule of law, therefore, is also more than constitutionalism: it requires that all laws conform to certain principles.

Therefore, the rule of law, according to Hayek, relies on general ‘meta-legal’ rules that have progressively, spontaneously, if not tacitly, been discovered and evolved in a given society to facilitate social interactions and exchanges between individuals (“a government of law and not of men”). Those custom-based rules have certain attributes, namely that they be “known and certain”, apply equally to everyone, define a clear limit to the coercive power of government, require the separation of power and finally only allow the judiciary to exert discretionary rulemaking (within the boundaries of those meta-legal rules). Hayek explains that “under a reign of freedom the free sphere of the individual includes all action not explicitly restricted by a general law.”

Within this framework, Selgin describes the appearance of the gold standard as following the generic principle described by Hayek:

The difference between private or customary law and public law or legislation is, I submit, one of great importance for a proper understanding of the gold standard’s success. For, despite both appearances to the contrary and conventional wisdom, that success depended crucially upon the gold standard’s having been upheld by customary law rather than by legislation. It follows that any scheme for recreating a durable gold standard by means of legislation calling for the Federal Reserve or other public monetary authorities to stand ready to convert their own paper notes into fixed quantities of gold cannot be expected to succeed.

According to him, the gold standard and its definition was mostly a spontaneous monetary arrangement rooted in private commercial customs, and enforced through the private law of contracts. He sums up:

In short, countries abided by the rules of the gold standard game because that game was played by private citizens and firms, not by governments.

Consequently, a gold standard put in place and enforced by governments is unlikely to work. He continues:

Although it may seem paradoxical, our understanding of the classical gold standard suggests that, if that standard had been deliberately set up by governments to enhance their borrowing ability, it is unlikely that it would have worked as intended. This conclusion follows because, once public (or quasi-public) authorities, governed by statute law rather than the private law of contracts, become responsible for enforcing the rules of the gold standard game, the convertibility commitments crucial to that standard’s survival cease to be credible.

He, as a result, doubts about the ability of the gold standard to be ‘forced’ to return through government policy, and demonstrates that post-WW1 attempts to reinstate the gold standard were doomed from the start as states “tragically misunderstood the true legal foundations” of the famous 19th century monetary arrangement. But Selgin also believes that a ‘spontaneous’ return to gold would be unlikely because the public has been ‘locked-into’ a fiat money standard, and that customary law tends to reinforce that trend – by legitimizing the practice over time – rather than providing a way out. Moreover, he concludes, if a new commodity-like standard were to emerge, nothing guarantees that it wouldn’t be based on another sort of medium (including synthetic commodities such as cryptocurrencies).

Now that I have explained the basics of Selgin’s reasoning, I will try to understand what it involves for banking structure and regulation. While free banking systems, such as Scotland’s, have arguably spontaneously evolved following a custom-based legal framework, the structure of the whole of today’s financial system comprises barely anything ‘natural’ left, as Bagehot would point out. Banking, as we know it, is a pure product of decades, if not centuries, of accumulating layers of positive legislation and government discretionary policies. In short, there is now little overlap between banking and the rule of law**.

The inherent instability of banking systems regulated by statute-based law, as opposed to the relative stability of free banking systems (which Larry White referred to as ‘anti-fragile banking and monetary systems’), is therefore unsurprising seen through Hayek’s and Selgin’s lens: governments, even with the best of all possible intentions, could simply not come up with a banking arrangement that could outperform decades or centuries of experience and decentralised knowledge gains that were reflected in rule of law-compliant free banking. Their attempt at centralising and harmonising the “particular circumstances of time and place” were self-defeating.

But the question isn’t what’s wrong about today’s financial system, but can we do anything about it? Can we get back to a rather ‘pure’, rule of law-compliant, free banking system? And my answer is, unfortunately, rather Bagehotian: despite how much I wish to witness the re-emergence of a financial structure based on laissez-faire principles, I believe it’s unlikely to happen… (but wait, there’s a new hope)

Why? For the very reason mentioned by Selgin: regulations have shaped the financial structure for such a long time that innovations and practices have been established that seem now unlikely to disappear. Let me give two examples:

- Money market funds were originally created to bypass the US regulation Q, which has since then been abolished. But MMF are still major financial players and unlikely to disappear any time soon. They have become an established part of the financial structure.

- Mathematical model-based risk frameworks, which existed before the introduction of Basel regulations but were not as widespread, and certainly not as uniform. Basel rules and domestic regulators required common standards that are now used both by analysts and commentators as data, and by bankers for internal risk, capital and liquidity management purposes, despite their limitations and the distortion they insert into the decision-making process. Abolishing Basel and its local implementations (such as CRD4 or Dodd-Frank) are unlikely to remove what is now accepted as market practice. However, less uniformisation in models and uses are likely to appear over time.

What about the very basic component of our modern banking system, the main beneficiary of statutory law, namely the central bank? Bagehot declared that “we are so accustomed to a system of banking, dependent for its cardinal function on a single bank, that we can hardly conceive of any other”, and opposed a radical transformation of the system which, unfortunately, was there to stay. Yet I believe the probability of getting rid of central banks without causing too much disruption is higher than what Bagehot believed. There are a number of countries that do not rely on any central bank, use foreign currencies as medium of exchange, and seem to do perfectly fine (such as Panama). This seems to show that market practices and relationships with central banks aren’t that entrenched and other models currently do exist, and which could spread relatively quickly.

But what is, in my view, our best hope of getting back to a financial system that follows Hayekian legal principles is Fintech. While Fintech firms have to comply with a number of statute-based laws, they nevertheless remain relatively free (for now) of the all intrusive banking rulebooks and discretionary power of regulators. As such, the multiple IT-enabled Fintech firms and decentralised technologies offer us the best hope of reshaping the financial system in a rule of law-based, spontaneously-emerging, manner. Of course, there will be bumps along the road and some business models will fail and other succeed, but this learning process through trial and error is key in shaping a sustainable system along Hayekian decentralised and experience-based principles. For the sake of our future, let’s refrain from the temptation of legislating and regulating at the first bump.

*At the time of my writing, I have only read the first one, although the second one is next on my reading list

**Although I am not an expert, the evolution of accounting standards over time seems to me to have mostly happened along rule of law principles (although Gordon Kerr, and Kevin Dowd and Martin Hutchinson, would perhaps argue otherwise, which is understandable as IFRS comes from statute-based law systems).

Update: See this follow-up post, which includes some Public Choice theory insights

Photo: Bauman Rare Books

LSE and GMU vs. regulatory logic

The Telegraph, in an article titled Regulators could be responsible for the next financial crash, pointed last week at a new report by the Systemic Risk Centre of the London School of Economics that is highly critical of recent regulatory developments.

Many of their arguments are actually reminiscent of those of this blog, or of other scholars such as Kevin Dowd (see his last year paper, Math Gone Mad). They criticise: regulators’ reliance on models and their attempt at harmonizing models across the banking sector, the ‘fallacy of composition’ that making each banking entity safe separately will make the whole system safe, the effectiveness of macro-prudential measures and financial transaction taxes, and the pro-cyclical nature of politics. The whole report is quite long, but provides a handy summary at the beginning (which I attach at the bottom of this post), which highlights well their rather negative view of what regulators and politicians are currently trying to achieve:

Society faces a difficult dilemma when it comes to systemic risk. We want financial institutions to participate in economic activity and that means taking risk. We also want financial institutions to be safe. These two objectives are mutually exclusive.

This sounds like the very antithesis of every single central banker speech and regulatory report I have read over the past few years…

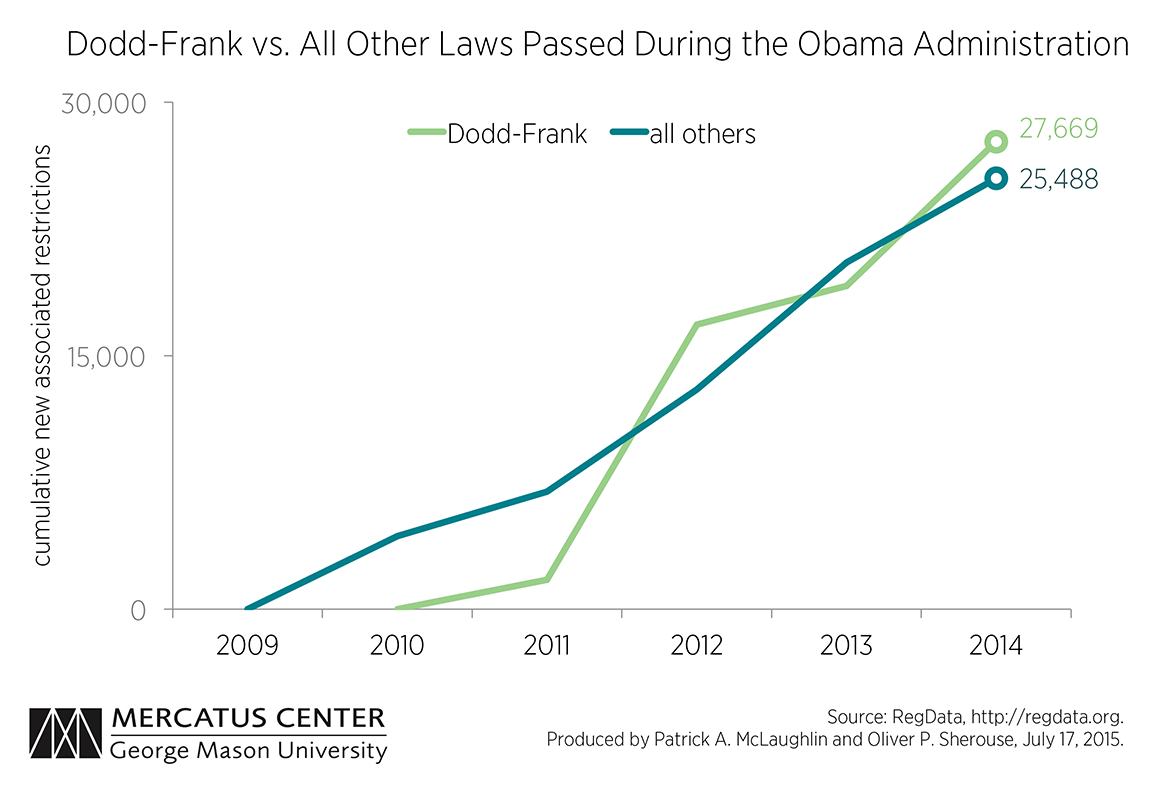

Meanwhile, the McLaughin and Sherouse from the Mercatus Center of George Mason University published a new blog post pointing out that Dodd-Frank “may be the biggest law ever”. They came up with stupefying data: Dodd-Frank actually comprises more restrictions than… all the other laws passed during the Obama administration:

Their post is also useful in debunking the myth of banking deregulation. They provide the following chart, which tracks regulatory restrictions on banks since 1970:

Their post is also useful in debunking the myth of banking deregulation. They provide the following chart, which tracks regulatory restrictions on banks since 1970:

Now we have to keep in mind that this chart only reflects restrictions (and there are limits to their methodology, which involves counting all sentences that includes certain words). Banks are also required to follow rules that do not qualify as restrictions, but still guide the way they should account for various financial items. Risk-weighted assets, for instance, aren’t restrictions per se. But they are classifications that banks had to follow when maintaining certain amounts of capital against certain types of assets. Nevertheless, it is clear from the chart that, when the crisis struck, banks were subject to more restrictions than ever!

Now we have to keep in mind that this chart only reflects restrictions (and there are limits to their methodology, which involves counting all sentences that includes certain words). Banks are also required to follow rules that do not qualify as restrictions, but still guide the way they should account for various financial items. Risk-weighted assets, for instance, aren’t restrictions per se. But they are classifications that banks had to follow when maintaining certain amounts of capital against certain types of assets. Nevertheless, it is clear from the chart that, when the crisis struck, banks were subject to more restrictions than ever!

The contrast between regulators’ actions and LSE’s complaints could not be starker, and is in fact worrying…

Contra Axel Leijonhufvud’s banking theory

I have a lot of respect for Axel Leijonhufvud. While I disagree with some of his economics, he mostly gets it. He’s a member of the monetary disequilibrium team, a sort of crossover between the Austrian/paleomonetarist/Keynesian world, a genius economic UFO. But his latest paper for the latest CATO Journal, titled Monetary Muddles, is just…weird. It demonstrates at the same time good insights, misunderstandings and lack of banking knowledge.

Leijonhufvud’s insight is that an Austrian business cycle-type crisis, such as our previous crisis (at least in his view), involves a redistribution of income:

Changes in financial regulation and in the conduct of monetary policy have not only played a very significant role in generating the financial crisis but have also been important in bringing about a large shift in the distribution of income over the last two or three decades.

This, at first, sounds very true to me (and I’ll get back to that later in the post). But the devil is in the details. Leijonhufvud gets almost his whole banking theory wrong. Yes you read correctly: (almost*) the whole of it.

First, he seems to adhere to the endogenous money theory. The culprit? Inflation targeting, which makes “bank reserves in highly elastic supply” at “the ruling repo rate”:

In my view, the complete endogeneity of the monetary base associated with inflation targeting has failed us.

I won’t repeat again why this isn’t accurate (see here, here, here, here, here, here, here…).

Second, all banking regulations and reforms that actually have endangered the banking system (he’s focusing on the US), are for him sources of stability. So the Glass-Steagal act “successfully constrained the potential instability of fractional reserve banking” and the restrictions on interstate banking/branching “gave the [US financial sector] great resilience.”

This is how he explains it:

I used the metaphor of a ship with numerous watertight compartments. If one compartment is breached and flooded, it will not sink the entire vessel. In the field of system design, this would be seen as an example of modularity (Baldwin and Clark 2000). Modular systems have several advantages over integral system. The one relevant here is that failure of one module leaves the rest of the system intact whereas failure in some part of an integral system spells its total breakdown. In the old U.S. modular system of financial intermediaries, the collapse of the S&Ls in the 1970s and early ’80s was contained to that industry. It did not bring down other types of financial intermediaries and it had no significant repercussions abroad. In the recent crisis, losses on mortgages of the same order of magnitude threatened to sink the entire American financial system and to spread chaos worldwide.

And deregulation broke this successful model:

The deregulation that turned the U.S. financial industry into an integral system is one of several instances where the economics profession failed spectacularly to provide a reasonable understanding of the subject matter of their discipline. The social cost of the failure has been enormous. At the time, the abolishment of all the regulations that prevented the different segments of the industry from entering into one another’s traditional markets was seen as having two obvious advantages. On the one hand, it would increase competition and, on the other, it would offer financial firms new opportunities to diversify risk. Economists in general failed to understand the sound rationale of Glass-Steagall. The crisis has given us much to be modest about.

Regular readers of this blog already know that the real story is pretty much the exact opposite of what Leijonhufvud believes, that financial deregulation is a myth (unless you wish to leave aside the whole Basel framework) and that US banking sector has always been fragilised by its granularity and lack of nationwide integration (you can see why here and here). His ‘watertight compartment’ metaphor isn’t applicable: banks evolve within economic systems that are not ‘watertight’, people, capital and income flow from one compartment to the other. If S&Ls failed in the US, it was because of regulations that applied specifically to them.

However, he does have some good insights when he remarks that the latest crisis implies consequences that were not originally foreseen by Mises and Hayek when they theorised the Austrian business cycle theory. This is why I called some time ago for it to be ‘updated’ in order to remain relevant and academically serious.

He is also right that the crisis implied a redistribution of income and that the pre-2008 boom involved “change in income distribution in favour of income classes whose marginal propensity to spend on the goods in the CPI basket is low.” But he sees bankers and financers as the main beneficiaries of the redistribution. While it is undeniable that the finance sector generates supranormal profits when interest rates are maintained below their natural Wicksellian level, the latest boom witnessed a much more economically damaging type of income and capital redistribution. And this one wasn’t due to monetary policy (although amplified), but to banking regulation: risk-weighted assets distorted the allocation of credit and allowed a major redistribution of capital towards real estate investors and sovereign borrowers, all of which benefited from below-equilibrium borrowing rates. This is the true issue of the latest crisis, the one that generated the malinvestments that eventually triggered our economic collapse.

I nevertheless still have a lot of respect for Axel (and will definitely keep my old copy of his book On Keynesian Economics and the Economics of Keynes: A Study in Monetary Theory on my shelve).

PS: Another minor issue with Leijonhufvud’s banking theory is his belief that banks “banks leverage their capital by a factor of 15 or so, thus earning a truly outstanding return from buying Treasuries with costless Fed money or very nearly costless deposits.” In reality, banks are often more leveraged than that but complain that, due to the low interest rate environment, they earn almost nothing on assets such as Treasuries and hence see their profitability depressed.

*His argument about the incorporation into limited liability companies of formerly fully-liable partnership investment banks is more debatable.

Austria misunderstands Hayek

A very recent speech on Austrian economics by Ewald Nowotny, Governor of the Austrian central bank, piqued my curiosity (see speech here and extra slides here). I ended up very disappointed.

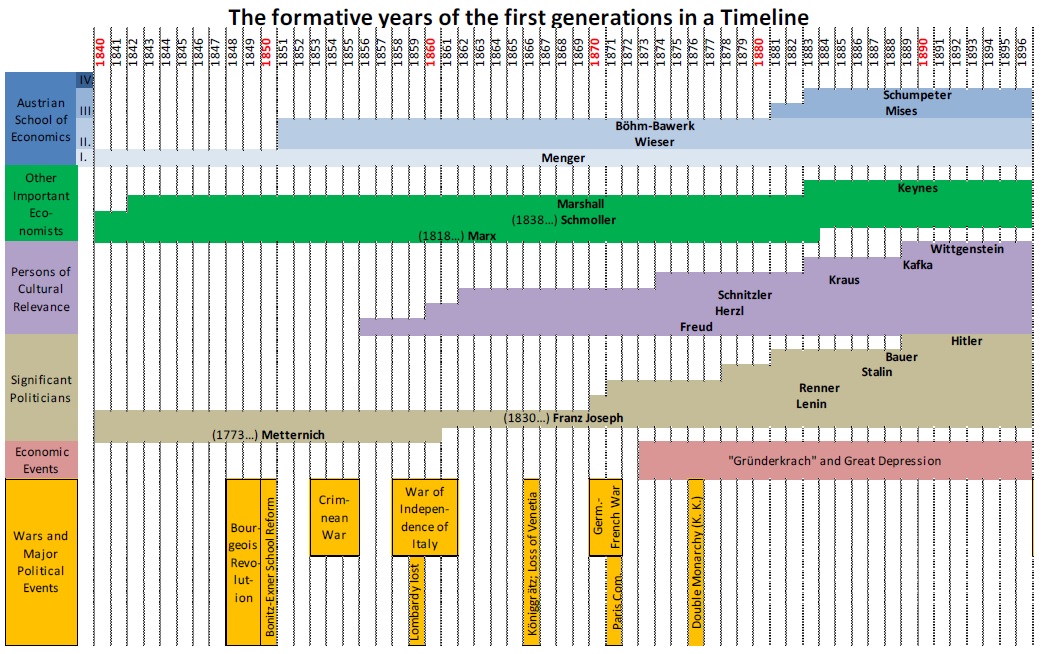

Nowotny’s speech is actually very interesting from a historical perspective. He goes over the structure of the 19th century Austro-Hungarian Empire, its limited liberalism, over-regulation, rigid societal structure, economic interventionism and limited entrepreneurial and commercial development, and describes how this influenced the individualistic state of mind of early economists of the early Austrian school, such as Carl Menger, Eugene Bohm-Bawerk and Friedrich Wieser. They introduced such critical concepts as the law of diminishing marginal utility (which entered the mainstream economic framework following the so-called ‘marginal revolution’ of Menger, Jevons and Walras), methodological individualism, and the fact that all economic activity involves uncertainty and time.

The disintegration of the empire following WW1, the hyperinflation experience, the rise of socialism and later the Great Depression reinforced this individualistic, anti-state intervention trend and led to the dynamic capital, entrepreneurial, business cycle, market structure, knowledge and law theories (all very laissez-faire) of Ludwig von Mises, Joseph Schumpeter and Friedrich Hayek. Nowotny very usefully summed up the historical events using the two following timelines:

But that’s about it. The rest of the speech is desperately anti-Austrian school, and completely misrepresents the views of some of its most famous proponents.

According to Nowotny:

contrary to more recent definitions that would define freedom as the free availability of opportunities, the definition of the Austrian school of economics always remained a negative one that exclusively defined freedom as the absence of constraints. This should become decisive for the spin that later Austrian economists took toward analytical nihilism.

While there are many definitions of ‘freedom’ within the Austrian school, not all scholars agreed with what Nowotny characterises as “the absence of constraints”. Even Murray Rothbard and his brand of anarcho-capitalism involves some constraints (via the market process or natural law). On the contrary, Hayek was very clear in The Constitution of Liberty that freedom was defined within a given general ruleset, under the framework of the rule of law. Whether analytical nihilism applies to Austrian scholars is also debatable (and it is unclear what he meant by that). The fact that they mostly rejected mathematics as an analytical tool to represent the economy does not imply that their reasoning was non-analytical (on the contrary) or that they also rejected maths as an analytical tool for economic calculation at the micro (company) level.

Nor did the statements that Hayek “completed [the Austrian school] transformation toward the libertarian fringe in which it is situated today” and that he “developed the economic concept of knowledge that already had been present in Menger’s thought into a full-blown attack against any public interventions” true. In reality, Hayek has often been slightly milder in his attacks against the state than Mises. It is clear from books such as The Road to Serfdom or The Constitution of Liberty that he considered the state as having a role in society, as long as it obeyed the rule of law and operated on the same conditions as private enterprises (although he later admitted – in a later preface to The Road to Serfdom – that he had put too much faith in the ability of government to perform a number of tasks). Some even called Hayek a “moderate social democrat” (a more than excessive statement in my view).

Equally, Hayek didn’t seem to be a great fan of free, or laissez-faire, banking either as George Selgin just pointed out (see also White’s great article Why Didn’t Hayek Favor Laissez Faire in Banking)*. The Austrian business cycle theory did not, as Nowotny asserts,

in his hands turned into a theory that regarded credit creation by public authorities as the main source of economic fluctuations. Completely ignoring that problems of this kind might also arise in the private sector, Hayek thus fervently argued for an absolute minimum state.

This was rather Mises’ view. In Monetary Theory and the Trade Cycle, Hayek seemed to believe that private commercial banks could naturally overexpand, without a central currency issuer (i.e. central bank) injecting extra cash into the economy.

Were Austrian scholars guilty of ‘therapeutic nihilism’? While they indeed declared that government treatments would in the end make things worse, they argued for the implementation of free market measures to render the economy healthier and more stable in the long run.

But the real nature of Nowotny’s ideology, which (mis)guides his destruction of Austrian scholars, remains in the single following statement:

As early as in 1930 Hayek’s prime policy recommendation to fight the crisis – published in his book “Prices and Production” – was to refrain from any interventions and wait for markets to stabilise themselves. This was a recommendation whose devastating effect only becomes clear when it is contrasted with the beneficial effects of the successful New Deal in the USA that did exactly the opposite.

Is it necessary to emphasise that the myth of the beneficial effects of the New Deal during the 1930s has been debunked by many economists over the past decades, both mainstream and unorthodox? For one thing, the New Deal surely lengthened the Great Depression in the US (see a summarised version of the arguments against the New Deal by Steve Horwitz here).

While I am not an expert on post-WW2 Austria and its economic performance, I still find it slightly ironic that Governor Nowotny, despite its obvious Keynesian tendencies, argued that ‘hard currency’ policies were in large part the reason underlying the economic revival of his country. This seems to me to be the sort of policy advocated by…Hayek or Mises, but not by Keynes.

After finishing reading the speech, it becomes clear that Nowotny has likely never read the authors he criticises. One cannot seriously declare that “uncertainty was handled by stabilizing expectations through corporatist institutions and by a generous social state” and that “knowledge dispersion was promoted by centralized collective bargaining institutions” after reading Austrian authors. This is a complete misunderstanding of Hayek’s depiction of a spontaneous order that relies on the knowledge of the “particular circumstances of time and place”. And indeed, the literature to which Governor Nowotny refers does not include any book or article from any of the authors mentioned above…

We would really have enjoyed a deep discussion of the Austrian conception of time and dynamic analyses (which Nowotny mentions) and their impact on the capital structure and the conduct of monetary policy. Instead, we end up with a traditional static equilibrium Keynesian misunderstanding of Austrian theories. Austria has sadly lost its Austrian tradition.

*Although I have to admit that Hayek’s position isn’t very clear. He seems to take a Bagehotian position: he didn’t like the way the banking system had evolved, hence he recommended (mistakenly or not ) against ending central banking

PS: See this great blog post from David Glasner on Israel Kizner, and his Austrian approach to entrepreneurship. A stark contrast with Nowotny’s speech.

PS2: I’m back from short holidays, so will blog more frequently from now on.

Radical proposals for Greece (guest post by Justin Merrill)

The origins of the Eurozone crises were a balance of payments crises caused by ECB’s collateral policies and Basel regulations, and partly fueled by the ECB’s monetary policy. Banks could hoard higher yielding sovereign debt with zero risk weighting or fund property bubbles with mispriced risk. Additionally, the ECB’s collateral policies were pro-cyclical, allowing for liquidity to fuel capital flows before the crises, then restricting liquidity to the crises countries by applying larger haircuts or removing the assets from eligible collateral altogether. This explains the capital flows before the crises and why the credit spreads were so narrow. Critics use the pre-crises lending to Greece as an example of market irrationality, but I see it as proof of a rational response to regulatory arbitrage leading to systemic risk. As Kevin Dowd has recently explained, risk weightings, stress tests and other sorts of regulations cause systemic risk by crowding into the assets regulators approve of and incentivize.

http://www.cato.org/events/math-gone-mad-systemic-dangers-federal-reserves-stress-tests

http://www.adamsmith.org/wp-content/uploads/2015/06/No-Stress-ONLINE1.pdf

I believe the solutions for the Eurozone’s problems are neither a fiscal union nor a banking union, but that’s a different post. The solution for Greece also is not more papering over with troika lending. They have a solvency problem that needs to be fixed with a combination of haircuts and supply side reforms, as well as a liquidity problem. Contrary to popular opinion, the Greeks are not lazy. According to the OECD, they work more hours per week than anyone else in the Eurozone with 2,042 average hours per year while the Germans work the least with 1,371 average hours per year. So obviously Greece has a productivity problem and needs to attract private investment, something I highly doubt a Grexit and capital controls will do.

https://stats.oecd.org/Index.aspx?DataSetCode=ANHRS

My recommendations are a mix of idealism within political constraints. It isn’t my first best, but it would probably be achievable if Greece sought these policies because their implementation is not dependent on cooperation of other institutions.

A default by Greece does not necessitate a Grexit. If Illinois defaults on its pension liabilities in the future, will we be calling for their eviction from the union? If Puerto Rico defaults on its bonds will we demand they stop using dollars? Additionally, would it even be possible to prevent continued use of the Euro if the Greeks choose to continue doing so? I think returning to the Drachma would be the worst case scenario and I have thought of non-conventional solutions that don’t involve inflating away their liabilities or enforcing capital controls which would involve the destruction of their economy, the redenomination of private contracts, and a redistribution of resources towards the public sector from the private sector. My proposal will be restricted to money and banking reforms and what to do with the debt despite the fact that there are many needed supply side tax and regulatory reforms. This is because I believe the prime cause is monetary in nature. There are many countries with low productivity growth that don’t experience Greek like crises. BOP crisis can happen for many reasons, but the symptoms are similar. Currency depreciation isn’t a universal cure, especially when fear of future devaluation is one of the prime causes of BOP crisis.

A summary of my recommendation is that Greece should:

- Default on their debt

- Keep using the Euro

- Allow free banking

The capstone of my proposal is to allow free banking, especially assuming that for one reason or another Greece will be cut off from liquidity from the ECB. This means that Greek banks would issue their own notes (and possibly token small change) and deposits that would be redeemable at par for Euros, drastically reducing the banks’ dependence on the ECB for liquidity. Banks would still use Euros for reserves and, like a currency board, they would acquire reserves through net exports and capital inflows. Deposits in Greece may have to pay a risk premium over deposits in Germany, but that is no different than now. The premium may be lower than it is now once the threat of devaluation and capital controls is taken off the table. This alone would solve most of the problems caused by the currency union without leaving it. Of course Greece would still import the ECB’s monetary policy, but this is still far better than having an independent policy and all its political trappings.

Banks may initially need to put limits on ECB issued Euro withdrawals or external transfers, but this would be a voluntary agreement with depositors, sort of like how savings deposits can have withdrawal limits and payment can be deferred by up to two weeks as a contingency clause.

So this just leaves the question of what to do about that debt. The vast majority of Greece’s debt is now owned by the Troika. The good news is since it is no longer in the banking system the threat of contagion is off the table. The bad news is that a default may have harsh external political consequences. I say “screw ‘em” for three reasons. The first reason is that Greece will have a much more sustainable budget without paying interest or repaying principal. The second reason is that a total default would mean that Greece will be cut off from credit markets and will be forced to run a balanced budget for the foreseeable future. The third reason is that whoever was stupid enough to lend money to Greece should be burned for thinking Greece was capable of repaying. The best part of this is that a default by Greece would ruin the appetite for future bailouts!

Greece should either totally stick it to their creditors or convert their debt into a parallel domestic currency that is payable for taxes and banking reserves (I would do away with reserve requirements though). This way the creditors might get most of their principal back without any outlays from the Greek government. Domestic investors or speculators would buy them from the current creditors and use them to either pay taxes or buy Greek exports. The Greek government could then make part of their payroll and pension expenses in these irredeemable treasury notes. I would recommend that the supply of these be fixed at the current amount of debt outstanding, and not a new way to finance future spending. The supply may naturally dwindle over time as notes are destroyed or lost. I imagine they would have a high velocity since Gresham’s law would mean people would prefer to hold their Euros and private notes over the T-notes. Maybe the Greek government could offer to replace worn notes from banks to extend their circulation and increase their demand. It would be interesting to see if these trade at par or at a discount.

A friend responded to my proposal with skepticism because he didn’t see how the political climate in Greece would endorse the radically free market idea of free banking. I explained that given their alternatives, one doesn’t need to be a free market supporter to see the benefits to the Greeks. They could stumble their way into it similarly to how Somalia became stateless without being anarchists. But either way: default on the debt, stay on the Euro and free the Greek banks!

Fintech: are banks now panicking?

Just a couple of years ago, P2P lending, cryptocurrencies and other financial innovations where not taken very seriously by the established banking sector. Things seem to be changing.

A number of news over the past few weeks seem to demonstrate that many banks now fear that their traditional business model is about to get disrupted and that it is perhaps better to jump on the bandwagon. We never know. Especially when your decades-old IT systems show cracks all over the place.

A number of news over the past few weeks seem to demonstrate that many banks now fear that their traditional business model is about to get disrupted and that it is perhaps better to jump on the bandwagon. We never know. Especially when your decades-old IT systems show cracks all over the place.

First, P2P lending and crowdfunding. Following a number of big name moves over the past few years (such as Lending Club hiring Morgan Stanley’s former CEO John Mack) and the IPO of Lending Club (currently valued at $6Bn, about a third of Commerzbank’s market capitalisation), what could be more symbolic than Goldman Sachs’s plan to launch its own platform? Whether or not it can succeed in attracting lenders (hard to say that you an ‘alternative’ lender/borrower attempting to disrupt finance if you use GS as a platform…), at least it can leverage its structured finance skills to securitise P2P loans and sell them to institutional investors the way I described 18 months ago. As Basel regulations that make it expensive to lend to SMEs are unlikely to disappear anytime soon, small firms are increasingly turning to those platforms, so growth is likely to remain healthy for the foreseeable future (and potentially lower the distortions and impacts of what I called the RWA-based Austrian business cycle).

Second, cryptocurrencies. What was widely seen as an idealist libertarian scheme doomed to fail is now seen as almost inevitable. Everything is moving onto the (coloured) blockchain (payments, FX/securities transfers…) and bypassing the current centralised financial system. The job market in certain areas of finance will be gloomy over the next 15 years. Evidently, financiers would rather keep their job, so are trying to come up with their own proprietary solutions. Nasdaq, the US exchange, has announced its own blockchain initiative to “facilitate the issuance, transfer, and management of private company securities”. This could change some traders’ habits as described by the FT. Same thing, Citigroup is working on its own version, which would “allow for less complicated and less costly cross-border payments and other transactions.” As is Barclays. As is Santander. As are most financial institutions I’m aware of. Their incentive is clear: let’s not get disintermediated (or at least limit the damages), and if can capture additional revenues while lowering our cost base, all the better. Additionally, an FT writer reports that bitcoin (actually, the blockchain technology) could fundamentally simplify the back office/settlement process. As I said above, brace yourself for job losses.

But is is a research analyst from BNPP Securities Services who sums up the issues the best way. According to him, the blockchain has a potentially revolutionary impact on financial markets and could well make existing firms ‘redundant’…:

What would happen if the ownership of securities were recorded in a blockchain? We envisage two scenarios for the integration of this technology in the post trade world.

The first scenario creates a total disruption. In its purest form, a distributed blockchain system allows all market participants direct access to the DSD (Decentralised Securities Depositary), to the exchange and to the post trade infrastructure (clearing & settlement). If this setup develops then existing industry players might be redundant. However, given the challenge of keeping the private key of the account safe, it is possible that investors will entrust an authority to safe keep the private keys. It is also possible that custodians will be responsible for the application layer over the blockchain or that they will launch their own network.

The second scenario is an integration within the post trade ecosystem. The distributed ledger might only be the next generation of IT infrastructure. In this scenario custodians or settlement infrastructures might use the blockchain to record the ownership and trades between themselves; however end investors will still need to use a custodian to have access to the market. The ledger will only be accessible to authorised market participants. Existing actors will remain in charge in this scenario however their level of service could change and they may deploy new services that they could not in the past because the investments required were a huge barrier to entry.

Even in emerging markets, telecommunication companies and banks now fight each other in a match that would have looked rather awkward just a decade or two ago. Equivalently, in developed markets, Apple Pay, Google, Paypal and others are starting to take on the banks. While the scope of their activities remains limited for the time being, they could do much more.

My readers know that the heavy regulatory burden on the banking system is an enabler of this disruption. As regulatory costs jump into billions, you can deduct those from technology and financial IT investments. Regulators want banks to get safer but don’t really allow them to develop safer innovative processes as they try to harmonise business models (on top of regulatory costs). This leads to economic damages, as I regularly argue on this blog, but this provides fintech startups with a great opportunity. They should seize this chance and resist the urge to call for regulatory barriers to shut out new entrants. Only this way would financial markets and the economy remain distortion-free.

PS: I had to point out the irony if this article in the FT by Mark Carney, the governor of the BoE. Carney argued that banks should not exclude vulnerable people in emerging markets. But, Mark, banks’ reactions are a natural consequence of the regulations opaque fines that you and most other regulators have been advocating for years now, despite bankers warnings that this would happen. A little late to think about the consequences of those rules, isn’t it?

Chart: The Economist

Is Greece invalidating endogenous money theories?

Most of you already know the trouble Greece is in. What’s interesting is that, what’s happening to its banking system seems to not really reflect the view of some endogenous money theorists…

As Tim Worstall points out on the ASI blog, if banks really were able to create money out of thin air, the Greek banking system would have no reason to be on the brink of collapse for liquidity reasons (I won’t be mentioning insolvency risks here). Worstall’s blog post is admittedly overly-simplistic: while modern monetary theory (MMT) does believe in endogenous outside money creation, it remains more realistic and plausible than some of the alternative endogenous theories such as that of the authors of the BoE research paper I challenged a few weeks ago, and which I believe Worstall was in fact targeting.

Remember, this BoE staff paper was stating:

The bank therefore creates its own funding, deposits, in the act of lending, in a transaction that involves no intermediation whatsoever.

Well, the fact that Greek banks had to close for a whole week to prevent liquidity shortage seems to me to say a lot about their ability to create their own funding… See below a chart from the WSJ that clearly invalidates this view. As deposits are taken out of the system (= reserves withdrawal), Greek banks have had to replace the funding loss with central bank borrowing in order to remain liquid:

But in the case of Greece, even the supply side assumption is under pressure: under the ELA programme, the ECB is only willing to provide limited liquidity to Greek banks, and against good quality collateral.

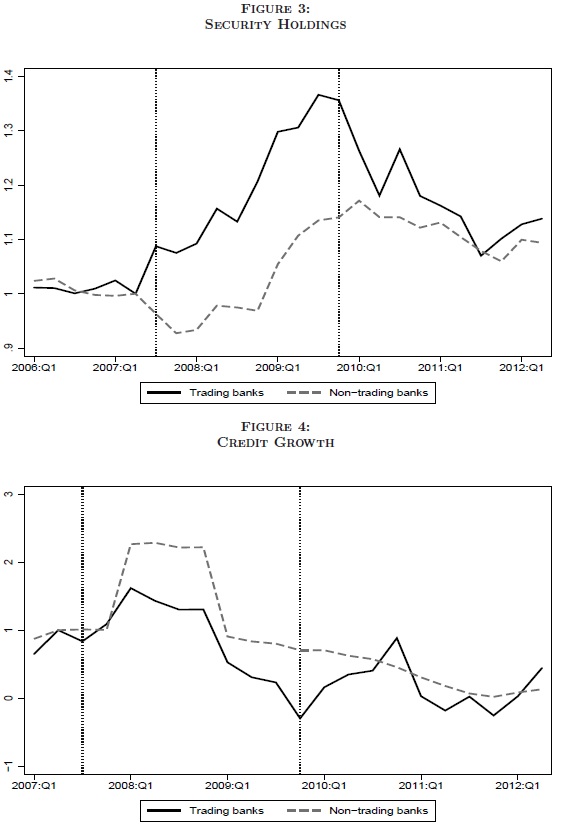

But that’s not it. Some Bundesbank staff members also just published a new research paper titled Securities trading by banks and credit supply: micro-evidence, which attempted to understand the implications of variations in trading activity on the supply of credit to the economy. In theory (simplified loanable funds model), banks have only one resource pool (= reserves) to use on two possible options: lending to customers or buying securities*. In a world of scarce resources, increasing one should decrease the second. However, endogenous money theorists would say that this dichotomy is a myth; that banks are not constrained by the availability of reserves and hence can expand both activities at the same time as long as it makes economic sense. According to them, the only real constraints on banks are regulatory ones such as minimum capital requirements.

What did the researchers find? (my emphasis)

We find that banks with higher trading expertise increase their overall investments in securities during a crisis, especially in securities that had a larger drop in price. Furthermore, this effect is more pronounced for banks with a higher level of capital and in lower-rated and long-term securities. In fact, we do not find significant differential effects for triple-A rated securities. Interestingly, the overall ex-post returns are about 12.5% for trading-expertise banks in the crisis. In contrast to behavior in securities markets, banks with higher trading expertise reduce their overall supply of credit in crisis times. The estimated magnitude of decrease in lending is approximately five percentage points. The reduction in credit supply is more pronounced for trading banks with higher capital. We also find that the credit reduction is binding at the firm level. Given that credit from banks with trading expertise constitutes a large fraction of overall credit in Germany, and that Germany is a bank-dominated economy, the results suggest that this could have a significant impact on the availability of credit to firms during the crisis at the macro level.

In short, the paper found that increased securities trading crowded-out lending in crisis time, despite banks not being constrained by regulatory capitalisation. While the paper is unclear about the effect of trading in non-crisis time given the much smaller fluctuations in volume, and while it doesn’t fully invalidate the MMT and other endogenous views, the results are definitely interesting and seem to provide empirical validity to the traditional loanable funds model.

*Of course, it’s not that simple and banks can indeed create claims on base money/reserves that are themselves used as money. But they are constrained by the availability of base money to do so. See my multiple posts on the topic.

HT: Ben Southwood

Update 1: The fact that the ECB is not willing to provide an infinite amount of reserves to Greek banks may not be such a challenge to the MMT version of the endogenous theory framework after all. The collateral that Greek banks can provide mostly comprises Greek government bonds, which are ‘barely’ acceptable as collateral under ECB rules. I am not an MMT expert (only know their banking theory), but they seemed to indicate that sovereign indebtedness wasn’t such an issue. So the EU/ECB institutional framework and rulebook may not be a real challenge to the MMT banking theory, but I would qualify it as a potential ‘weakness’ (which needs more analysis).

Update 2: MC Klein has an interesting post on the FT Alphaville blog. He points out that a number of Greek banks were given a clean bill of health during last October’s EU stress tests and so solvency shouldn’t be an issue, at least according to the EU. However, Draghi doesn’t seem to honour his ‘whatever it takes’ promise, despite the supposed health of Greek banks. So in the end, the potential ‘weakness’ I mentioned above may well be more challenging than that for the MMT version of the endogenous money theory.

Update 3: Also see this chart from this speech from Lowe, Deputy Governor of the Reserve Bank of Australia, and notice how funding types growth offset each other.

Recent Comments