LSE and GMU vs. regulatory logic

The Telegraph, in an article titled Regulators could be responsible for the next financial crash, pointed last week at a new report by the Systemic Risk Centre of the London School of Economics that is highly critical of recent regulatory developments.

Many of their arguments are actually reminiscent of those of this blog, or of other scholars such as Kevin Dowd (see his last year paper, Math Gone Mad). They criticise: regulators’ reliance on models and their attempt at harmonizing models across the banking sector, the ‘fallacy of composition’ that making each banking entity safe separately will make the whole system safe, the effectiveness of macro-prudential measures and financial transaction taxes, and the pro-cyclical nature of politics. The whole report is quite long, but provides a handy summary at the beginning (which I attach at the bottom of this post), which highlights well their rather negative view of what regulators and politicians are currently trying to achieve:

Society faces a difficult dilemma when it comes to systemic risk. We want financial institutions to participate in economic activity and that means taking risk. We also want financial institutions to be safe. These two objectives are mutually exclusive.

This sounds like the very antithesis of every single central banker speech and regulatory report I have read over the past few years…

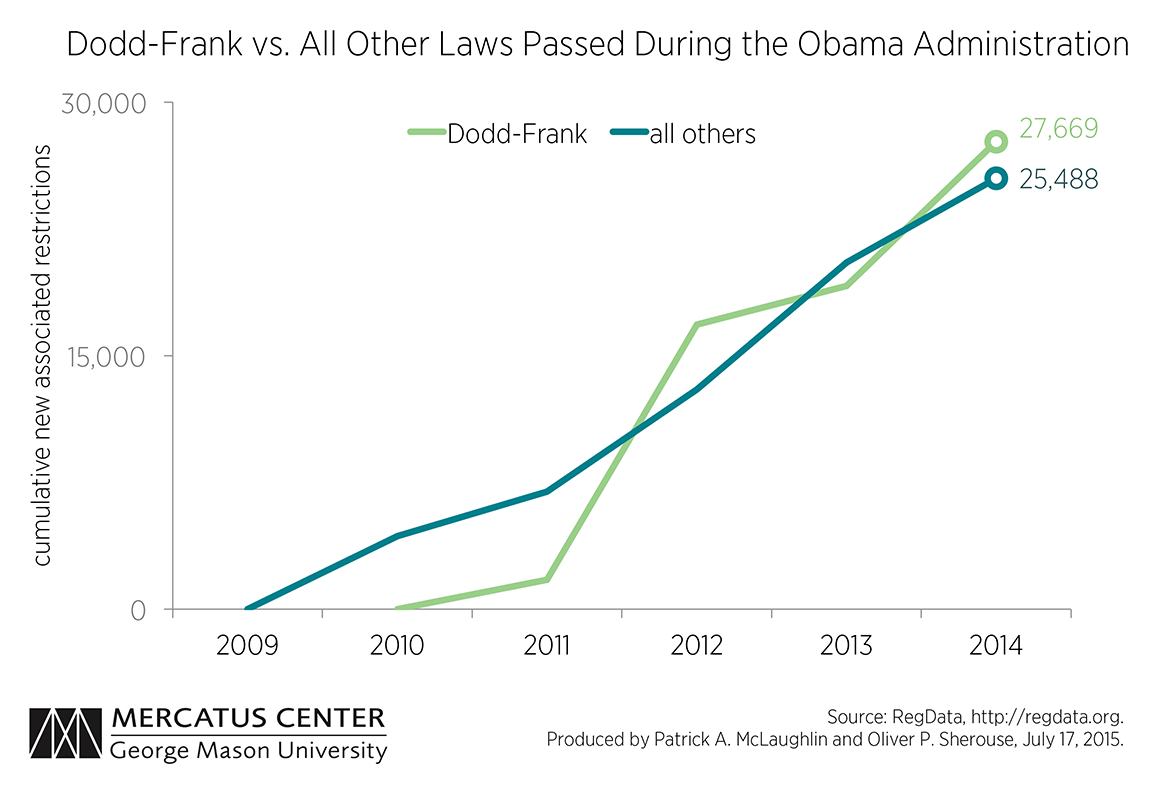

Meanwhile, the McLaughin and Sherouse from the Mercatus Center of George Mason University published a new blog post pointing out that Dodd-Frank “may be the biggest law ever”. They came up with stupefying data: Dodd-Frank actually comprises more restrictions than… all the other laws passed during the Obama administration:

Their post is also useful in debunking the myth of banking deregulation. They provide the following chart, which tracks regulatory restrictions on banks since 1970:

Their post is also useful in debunking the myth of banking deregulation. They provide the following chart, which tracks regulatory restrictions on banks since 1970:

Now we have to keep in mind that this chart only reflects restrictions (and there are limits to their methodology, which involves counting all sentences that includes certain words). Banks are also required to follow rules that do not qualify as restrictions, but still guide the way they should account for various financial items. Risk-weighted assets, for instance, aren’t restrictions per se. But they are classifications that banks had to follow when maintaining certain amounts of capital against certain types of assets. Nevertheless, it is clear from the chart that, when the crisis struck, banks were subject to more restrictions than ever!

Now we have to keep in mind that this chart only reflects restrictions (and there are limits to their methodology, which involves counting all sentences that includes certain words). Banks are also required to follow rules that do not qualify as restrictions, but still guide the way they should account for various financial items. Risk-weighted assets, for instance, aren’t restrictions per se. But they are classifications that banks had to follow when maintaining certain amounts of capital against certain types of assets. Nevertheless, it is clear from the chart that, when the crisis struck, banks were subject to more restrictions than ever!

The contrast between regulators’ actions and LSE’s complaints could not be starker, and is in fact worrying…

Recent Comments