When regulators face spontaneous finance

This is what I read a few days ago: ‘Shadow banking morphs and grows, confounding authority’

Despite their high-profile and tough stance (see Mark Carney here, but there are literally hundreds of other speeches and articles like this one available), regulators now admit that “after 10 years of being a hot topic there isn’t a consensus yet” on shadow banking, and that “is it banking or is it part of market-based finance? What are we going to do about it? We are nowhere near the finishing line.”

As Reuters reports:

Authorities are nowhere near to fully understanding “shadow banking” as the $75 trillion sector morphs and grows under the influence of new technology and regulation, a top markets supervisor said on Wednesday.

Regulators indeed struggle to make a sense of the Hayekian spontaneous financial order that free markets generate. Unlike banking, which has been a heavily-protected industry in most countries for more than a century, therefore making its business model quite stable, predictable and uniform, non-banking finance (what we now called shadow banking) is relatively informal and evolves all the time, driven by market actors’ needs and preferences as well as regulatory arbitrage.

We here get to a contradiction in terms. Regulators are trying to regulate entities designed to evade…regulation. This sounds quite tricky to me, and even possibly dangerous given the distortions this can bring about. I have once said that this type of financial innovation represented ‘bad’ (or ‘unnatural’) innovations. The whole cycle of regulation/regulatory evasion/re-regulation produces very opaque structures that market actors cannot make sense of, disturbing price signals and risk assessment and leading to catastrophe.

But regulating ‘good’ innovations, the ones effectively driven by customers’ needs and technological shocks, isn’t necessarily a good idea either. It is pretty much impossible, by definition, to regulate hundreds of different business models with a single regulatory toolkit. Which implies micro-regulating each firm with a discretionary set of rules that regulators believe those particular firms should follow. Economic micro-management doesn’t work and there is no reason that it should work this time.

Reuters goes on describing what’s typically happening right now:

Advances in technology – which mean there are far more ways of linking credit with borrowers, such as the use of mobile phones in Africa – have also created a new set of financial actors in what Alder dubs “modern” shadow banking.

He cited other developments such as Chinese e-commerce giant Alibaba teaming up with Lending Club to offer peer-to-peer lending for U.S. customers.

P2P lending (consumer finance, SME lending, real estate…), P2P securitization, equity and product crowdfunding, ETFs, mutual and hedge funds lending, Bitcoin and cryptocurrencies, alternative payment companies, money market funds, mobile payments, alternative currencies… All those growing financial instruments allow for hundreds of possible combinations. No wonder regulators are confused. Good luck to them.

Borio, deflation and bank intermediation

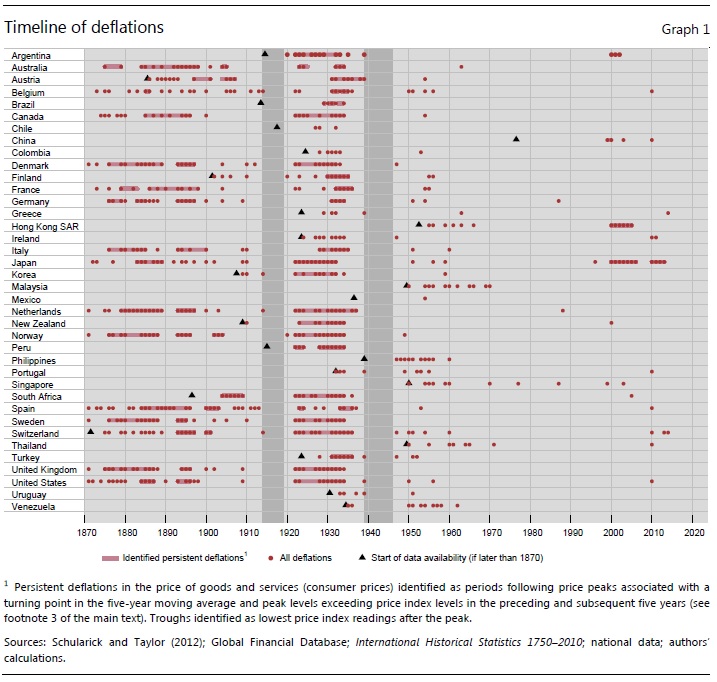

Some time ago, I wrote that the BIS seemed to be on the dark side of macroeconomics. Earlier this month, Borio et al seemed to confirm this by publishing a quite fascinating paper titled The costs of deflations: a historical perspective. A number of economists, such as George Selgin or a number of market monetarists, had already pointed out the difference between good and bad deflation, which went against the mainstream view that deflation is always a bad thing. Borio and his team went even further.

Analysing inflation data in a sample of 38 countries since 1870, they come to the remarkable conclusion that the link between deflation and low growth/recession is almost non-existent:

On balance, the relationship between changes in the consumer price index and output growth is episodic and weak. Higher inflation is consistently associated with higher growth only in the second half of the interwar period, which is dominated by the Great Depression – the coefficients are positive and statistically significant. At other times, no statistically significant link is apparent except in the postwar era, in which higher inflation actually coincides with lower output growth, with no significant change in the correlation during deflations. In other words, the only sign that price deflation coincides with lower output growth comes from the Great Depression and its immediate aftermath.

Their paper is a great data gathering exercise:

As we can see, many countries were used to experiencing long deflationary periods before the Great Depression. Surprisingly (for some), all deflationary periods actually coincided with rapid productivity growth and real income improvements. Long deflationary periods virtually disappeared after WW2 as the mainstream economic view started to associate deflation and depressions following the experience of the 1930s. While the authors do not find any correlation between deflation and slow economic growth, rerunning their regression only taking into account ‘persistent’ deflations (at least 5 years long) gave the same results: none, as long as the Great Depression is excluded (and very low if included).

However, Borio finds a strong relationship between asset price falls (house prices in particular) and decline in economic performance, both on annual and persistent bases, which seems to explain most decline in output throughout his sample period:

The results are rather striking. Once we control for persistent asset price deflations and country-specific average changes in growth rates over the sample periods, persistent goods and services (CPI) deflations do not appear to be linked in a statistically significant way with slower growth even in the interwar period. They are uniformly statistically insignificant except for the first post-peak year during the postwar era – where, however, deflation appears to usher in stronger output growth. By contrast, the link of both property and equity price deflations with output growth is always the expected one, and is consistently statistically significant.

To a bank analyst like me, this is expected. A general decline in prices of some asset classes affects banks in very specific ways. On-balance sheet, banks classify assets either as ‘held to maturity’ (HTM), ‘available for sales’ (AFS), or ‘fair valued/held for trading’ (FV). While asset price variations do not affect HTM assets, FV ones directly impact banks’ net income, and hence banks’ equity capital. AFS asset price fluctuations, on the other hand, do not affect bank’s profitability but indirectly impact banks’ capitalisation through ‘comprehensive’ income. As a result, a decline a in a number of asset prices can severely reduce banks’ capitalisation. For instance, Barclays said that

if the yields on 10-year Treasury bonds reverted back to their historical average it would wipe nearly a fifth off the tangible book value of European banks.

But falls in asset prices also affect banks through the collateral and off-balance sheet channels: they have to pledge more collateral to secure funding, limiting growth. As mortgages now represent most of banks’ assets, a general fall in property prices is the most problematic. Banks calculate the amount of provisions they need to put aside against their mortgage portfolio. In order to do this, they calculate borrowers’ probability of default (PD), their own exposure at the time of default (EAD), and the loss they would experience given an actual default (LGD). Mortgages are loans collateralised by property. The LGD component of the equation increases a lot when property prices collapse, even if the other variables remain stable.

For example, when a bank originates a 90% loan-to-value mortgage, the value of the loan remains below the value of the property (= collateral) as long as property prices don’t decline by more than 10%. (To which needs to be added legal/foreclosure/reselling costs) When property prices decline strongly enough, even if other economic factors are unaffected, banks have to increase their provisioning, which directly impacts their net income and, indeed, the strength of their capitalisation. The ability of banks to intermediate between depositors and borrowers becomes temporarily impaired, and other potential real economy borrowers suffer. As such, Borio’s results are unsurprising.

Moreover, the Basel regulatory framework seems to have amplified this phenomenon. As Borio says

And notably, the slowdown following property price peaks appears to be somewhat stronger in the postwar era.

Let’s recall this recent research, which highlighted that, due to government interference and regulation, real estate lending had become the main driver of bank’s lending growth in the post-WW2 era, to which I pointed out that most of this growth was due to changes introduced by Basel.

Those results strongly question the current central bank focus on inflation, and inflation targeting in general. While it sounds unreasonable to ask central banks to identify bubbles (they can’t), wide asset price fluctuations could be indicators that monetary policy is too ‘loose’. Remember that Wicksell defined the natural rate of interest as the rate that is neutral in respect to commodity prices. In the financial community, a growing number of investors and bankers are now warning of the potential consequences of what they view as overvalued prices (see here, here, here…).

However, the effect of monetary policy on asset prices has become harder to disentangle from Basel-only effects. How is monetary policy supposed to respond to regulatory-induced distortions? Even by trying to maintain a stable NGDP growth, another property bubble pop could severely affect the banking channel of the transmission mechanism and banks’ ability to finance the real economy.

Update: a 90% LTV loan means that the value of the loan is BELOW the property value, which is what I originally meant but wrote ‘above’ for some reason. This has been corrected. I thank Justin Merril for pointing that out.

PS: Borio’s paper also published the 2 following charts, which I reproduced below and added the introduction of Basel:

Bashing? Only in banking

Let’s go back in time. In 2008 and 2009, a global industry experienced a collapse on a scale not seen for decades, partly because it had overexpanded into areas that were unsustainable and that did not match customers’ expectations. The US was badly hit. An unprecedented $85bn bailout was set up to save three of the main US firms. A few years later, some of these had recovered. Others had been acquired by foreign companies.

This industry was the auto industry. Its fate was relatively similar to the one of the banking system. However, their post-crisis treatment cannot be more different. One industry is celebrated; the other one has become politicians’ punching bag.

The collapse of any industry is evidently catastrophic. But let me ask: how would we react if, following the crisis, governments appointed auto regulators to approve (or not) any new product developed by the industry in order to ensure that this product would match customers’ demand (as viewed by those regulators), and that as a result the firms’ future would not be endangered by a few failed products? What would we say if regulation forced all those auto companies to maintain a much higher pre-defined liquidity (and/or capital) buffer against all accrued income? Or if leverage caps were introduced to prevent any firm from taking on too much debt, despite growing revenues and investments prospects and/or new business opportunities?

My guess is that most people would be infuriated to witness such economic micromanagement. Economic planning has been attempted a number of times. And failed. Every single time. And, indeed, governments have not implemented such measures.

But clearly, the auto industry had failed and a large amount of taxpayer money was injected. Despite this, nobody (to my knowledge) talked of prosecuting auto industry employees for their failure. Nor did politicians speak of implementing auto industry-specific taxes to ‘punish’ them for their collapse and the subsequent use of taxpayer money.

But for some reason, all the measures described above suddenly become acceptable once we move into banking realms. Vengeance (and deficits), rather than reason, seems to be what guide politicians’ decisions. Take the new UK budget revealed last week, which comprises an extension of the ‘exceptional’ bank levy. The reason:

The banks got support going into the crisis; now they must support the whole country as we recover from the crisis

Such short-term political view is counterproductive in the medium-term. Regulators themselves complain that, while they try to build banks’ capital buffers, the same capital evaporates into uncontrollable, opaque and often hard to justify large fines*. To the list, regulators could now add those unending ‘exceptional’ bank levies. Extracting money from banks has effectively become a new convenient and politically acceptable way of financing the state, alongside regular taxation, debt and inflation. The rule of law seems to be evolving into the rule of government deficit.

The only effect of all those measures is to further weaken the banking system, reducing its ability to lend and therefore strengthen the economic recovery. Politicians are shooting themselves in the foot. You cannot have your cake and eat it.

Apply the same measure to any other industry and brace yourself for a public outcry. I can already hear the rebuttals from here: ‘but banking is different’. It is only partially true. Banks control a large share of the payment system, but one of the reasons is that governments have historically raised barriers to entry. Of course, if banks collapse, a number of savers may not be able to recover the entirety of their savings. But the same applies to any other non-banking investment. What would have happened to savers that had invested their life savings and pensions in auto equity and bonds if this industry had fully collapsed? Following such logic, no other non-banking firm would ever be allowed to fail as this would lead to job and savings losses.

Banks of course intermediate between depositors and borrowers. When they fail, credit cannot be properly allocated to sectors where it is economically efficient, making banking failures disruptive. But over-protecting banks make them weaker (i.e. moral hazard). And bashing bankers do not heal banks. It weakens them further. And, in the end, it weakens all of us, including politicians, legislators and regulators.

*I am not saying that fraud should not be punished. It should. But the legal basis for extracting such large amounts from banks is extremely unclear, as The Economist pointed out:

To a public angry at banks for their role in the financial crisis, this may all seem like reasonable retribution. Yet in many cases the rush to punish is overturning basic principles of justice.

Or also see this now ‘old’, but prescient, article (2012):

If banks once did banking, now they practise law. […]

A settlement often suits the authorities as well as the banks. Fines are frequently used to fund government budgets; and many a political career has been launched on the back of a high-profile deal, without the need to prove allegations in court. […]

Oklahoma’s attorney-general, Scott Pruitt, was the only one of his colleagues not to participate in the national mortgage settlement earlier this year. Mr Pruitt said it had nothing to do with genuine fairness or justice, rewarded bad behaviour and reflected an illicit expansion of regulatory power.

Basel 3, or 4, or 57, always the same problem

Basel standards have been amended with Basel 3, though the issue of risk-weighted assets (RWAs) remain. I have pointed out how economically distortive RWAs were, and I consider them to be a major factor that led to the financial crisis. Banks’s flexibility in estimating the capital they needed against certain assets was partially restored with the implementation of Basel 2’s IRB (‘Internal Rating-Based’), although those risk-weights were still validated by regulators to make sure they stuck to ‘acceptable’ standards (according to them). This resulted in Basel 1’s economic distortions remaining, if not sometimes amplified as bankers, expecting to boost RoE, were incentivised to overstate the quality of certain assets that regulators viewed favourably.

Now regulators are trying to manipulate RWAs further by implementing floors and removing their (half) reliance on credit ratings, what a number of people have already called Basel 4 (not an official name however). According to a member of the American Bankers Association reported by Euromoney:

“As Basel III was an admission that Basel II got things wrong, Basel IV is a clear recognition that there is much that is wrong with Basel III,” he says. “Yet the folks at Basel have not yet looked in the mirror and asked whether what is mostly wrong might be happening in Basel, that the simple concept of Basel I, to have some basic global capital standards, has been lost in an effort to over-engineer and micromanage at the global level the fine details of capital standards.”

Most people seem to understand the limitations of metrics-based RWAs:

BCBS wants to end the practice of risk-weighting lenders’ exposures by reference to external credit ratings and instead suggests using measures such as capital adequacy and asset-quality metrics on exposures to other banks, for example. For corporates, the BCBS argues a given borrower’s revenue and leverage should determine credit risk weights rather than ratings, with the latter typically discriminating between industries and local-accounting standards.

Bankers see plenty of problems. Since this way of risk-weighting exposure to other banks is determined by common tangible equity ratios and the non-performing assets ratio, it does not adequately take into account divergent liquidity and business-risk profiles, nor differences in supervisory processes under Pillar 2 of the Basel regime, says a senior regulatory adviser to the CEO of a large European universal bank.

The adviser adds: “Credit rating agencies look at a multitude of factors and these metrics are always richer, incorporating thorough timely reviews, and engagement with counterparties and agencies. You can also never empirically replace these qualitative assessments.”

I cannot agree more. I have seen a number of ‘models’ that attempted to estimate firms’ riskiness based on a few metrics. They are not accurate and sometimes way off. Qualitative assessment remains key. According to Euromoney, this new Basel methodology could largely amplify the RWA gap:

For example, the risk-weighting attached to corporates will jump from 30%-150% to 60%-300%. Meanwhile, the proposed risk weights for mortgages is in the 25%-100% range, compared with a flat 35% currently, based on the loan-to-value (LTV) ratio and a borrower’s indebtedness.

This won’t help correct the economic distortions that Basel has introduced. Quite the opposite. While Basel policymakers are right that there are problems with RWAs, the way they hope to correct them is far off the mark.

Moreover, I have only recently found out that Basel 3’s leverage ratio, which was supposed to correct some of those distortions by getting rid of RWAs altogether, actually introduces……a new RWA-type capital calculation framework, called ‘Credit Conversion Factors’. It effectively applies a ‘weight’ on certain type of off-balance sheet exposures in order to calculate the leverage ratio. It becomes obvious that, consequently, banks are going to be incentivised to leave aside banking products that suffer from a high CCF and pile into those that benefit from a low CCF. It is possible that CCFs end up not being as distortive as RWAs given their focus on banking products rather than on types of counterparties.

Still, Basel seems to be repeating the same mistakes over and over again. Applying any sort of ‘weighing’ system to micromanage the financial system can only lead to disaster through the economic incentives and distorted price of credit that it creates. How many iterations of Basel standards will it take to figure it out is anyone’s guess.

PS: Some of you might be surprised by this table compiled by Euromoney/SNL, which clearly shows that European banks use ridiculously low average risk-weights on their assets compared to their American peers:

Well, keep in mind that accounting standards are different. US GAAP allows for a lot more derivatives to be netted than IFRS (used by European firms). Consequently, many European banks end up with derivatives accounting for more than 35/40% of their total assets, whereas American peers’ derivatives only account for a few percent of their balance sheet, making them look much less leveraged.

The Economist’s flawed logic

The Economist this week accused global banks of being “badly managed and unrewarding” (also see its second, more comprehensive article here). It is true that banks have been hit by the crisis and the following regulatory outburst. But the logic underpinning the two articles of the newspaper in this week’s edition is badly flawed and only seems to demonstrate the paper’s bias against banks.

The newspaper admits that

on paper global banks make sense. They provide the plumbing that allows multinationals to move cash, manage risk and finance trade around the world. Since the modern era of globalisation began in the mid-1990s, many banks have found the idea of spanning the world deeply alluring.

Indeed. Global banks evolved from a need: the need to maintain a single (or just a few) banking relationship throughout the world. Globalisation of trade and capital flows inherently implies the globalisation of banking. The current de-globalisation trend that we witness among Western banks is dangerous as this will not help corporations grow their business and hence generate growth.

However, the Economist’s bias appears in that it does not distinguish between banks that are truly global and the rest, and between banks that suffered from the crisis, and the rest. Comparing HSBC, Standard Chartered and Citi with the likes of RBS or Societe Generale doesn’t make much sense. Some have a truly global presence in both retail and investment banking operations, while others only have representative offices or limited product ranges. They do not have the same business models and, despite this, all struggle to generate meaningful RoEs. Moreover, tiny to medium-sized domestic banks also struggle to generate RoEs that cover their cost of capital. Accusing global banks of underperformance thus makes no sense. Identifying some banks that perform relatively well because they focus on regulatory-advantaged businesses such as mortgage lending is irrelevant.

The Economist also targets both banks that needed bailouts and others that did survive the crisis with limited damages. That bailouts mostly involved banks that were not global and that some global banks indeed were saved by their diversified operations doesn’t seem to have rung a bell at the newspaper.

This is unfortunate, as The Economist does acknowledge the impact of regulatory changes:

The wave of regulation since the financial crisis is partly to blame. Regulators rightly decided not to break up global banks after the financial crisis in 2007-08 even though Citi and RBS needed a full-scale bail-out. Break-ups would have greatly multiplied the number of too-big-to-fail banks to keep an eye on. Instead, therefore, supervisors regulated them more tightly—together JPMorgan Chase, Citi, Deutsche and HSBC carry 92% more capital than they did in 2007. Global banks will probably end up having to carry about a third more capital than their domestic-only peers because, if they fail, the fallout would be so great. National regulators want banks’ local operations to be ring-fenced, undoing efficiency gains. The cost of sticking to all the new rules is vast. HSBC spent $2.4 billion on compliance in 2014, up by about half compared with a year earlier. A discussion of capital requirements in Citi’s latest regulatory filing takes up 17 riveting pages.

Indeed. Though regulation isn’t ‘partly’ to blame. It is the primary factor (along with low interest rates) driving the underperformance of banks of all sizes and shapes. The Economist itself several times attacked current regulatory reforms as being unnecessarily costly (see here and here). It now seems to have forgotten and ‘mismanagement’ has become to culprit. For any other industry, The Economist would have blamed regulatory overreach for the industry’s poor performance, in turn pleading for growth-liberating liberalisation. But not for banking. The Economist still hasn’t come to terms with the fact that banks were not the origin, but only the tool, that led to the financial crisis, and as a result remains a ‘classical liberal’ newspaper only when it wants to.

The demand for cash and its consequences

I came across this very interesting chart on Twitter (apparently actually coming from JP Koning’s excellent blog) showing the demand for cash over time in various countries.

The demand for cash is a form of money demand. And it varies over time and across cultures and evolves as technology changes. In most countries, the demand for cash increases around times when the number of transactions increases (Christmas/New year for instance, although some countries, such as South Korea, present an interesting pattern – not sure why). But there are very wide variations across countries: notice the difference between the Brazilian and the Swedish, British or Japanese demand for cash. Countries that have implemented developed card and/or cashless/contactless payment systems usually see their domestic demand for cash decrease and banks less under pressure to convert deposits into cash.

Overall, this has interesting consequences for the financial analysis of banks, bank management, and for the required elasticity of the currency. Every time the demand for cash peaks, banks find themselves under pressure to provide currency. Loans to deposit ratios increase as deposits decrease, making the same bank’s balance sheet look (much) worse at FY-end than at any point during the rest of the year. A peaking cash demand effectively mimics the effect of a run on the banking system. Temporarily, banks’ funding structure are weakened as reserves decrease and they rely on their portfolio of liquid securities to obtain short-term cash through repos with central banks or private institutions (or, at worst, calling in or temporarily not renewing loans)*. Central bankers are aware of this phenomenon and accommodate banks’ demand for extra reserves.

In a free banking system though, banks can simply convert deposits into privately-issued banknotes without having to struggle to find a cash provider. This ability allows free banks to economise on reserves and makes the circulating private currencies fully elastic. In a 100%-reserve banking system, cash balances at banks are effectively maintained in cash (i.e. not lent out). Therefore, any increase in the demand for cash should merely reduce those cash balances without any destabilising effects on banks’ funding structure (which aren’t really banks the way we know them anyway). However, if some of this demand for cash is to be funded through debt, this can end up being painful: in a sticky prices world, as available cash balances (i.e. loanable funds not yet lent out) temporarily fall while short-term demand for credit jump, interest rates could possibly reach punitive levels, with potentially negative economic consequences (i.e. fewer commercial transactions).

However, technological innovations can improve the efficiency of payment systems and lower the demand for cash in all those cases. Banks of course benefit from any payment technology that bypass cash withdrawals, alleviating pressure on their liquidity and hence on their profitability. Unfortunately not all countries seem willing to adopt new payment methods. The cases of France and the UK are striking. Despite similar economic structures and population, whereas the UK is adopting contactless and innovative payment solutions at a record pace, the French look much more reluctant to do so.

As the chart above did not include France, I downloaded the relevant data in order to compare the evolution and fluctuations of cash demand over the same period of time vs. the UK. Unsurprisingly, the demand for cash has grown much more in France than in the UK and fluctuations of the same magnitude have remained, despite the availability of internet and mobile transfers as well as contactless payments, which all have appeared over the last 15 years**. What this shows is that the demand for cash had a strong cultural component.

*Outright securities sale can also occur but if all banks engage in the sale of the same securities at the exact same time, prices crashes and losses are made in order to generate some cash.

** I have to admit that the cash demand growth for the UK looks surprisingly steady (apart from a small bump at the height of the crisis) with effectively no seasonal fluctuations.

Recent Comments