The limitations of the market monetarist story of the recession

The market monetarist story of the ‘Great Recession’ got published in the NYT two days ago in a column written by Beckworth and Ponnuru. I’m happy to see market monetarist ideas spread in the mainstream, but not fully happy because they still give a narrow view of what happened during the crisis, in my opinion.

And this column is no exception to the rule: market monetarism can explain a large part of the bust, but cannot explain the boom that led to the bust. Unfortunately, they are intrinsically linked and forgetting the mechanism that led to the economic implosion also lead them to draw partly wrong conclusions about what the Fed and other central banks could have done to ‘save the economy’.

This is Beckworth and Ponnuru:

What the housing-centric view underemphasizes is that the housing bust started in early 2006, more than two years before the economic crisis.

This is not what I saw. To me, the crisis started during the 2007 summer as the increasing level of defaults in the real economy triggered a number of funds to collapse (BNP Paribas and Bearn Stearns come to mind). The fact that events did not happen simultaneously does not imply that they were not linked. Indeed, as I describe below, it is extremely unlikely that financial stress would trigger a sudden economic collapse. Financial problems are usually a symptom that can turn into an amplifier. But rarely a root cause.

Then:

This housing decline caused financial stress by sowing uncertainty about the value of bonds backed by subprime mortgages. These bonds served as collateral for institutional investors who parked their money overnight with financial firms on Wall Street in the “shadow banking” system. As their concerns about the bonds grew, investors began to pull money out of this system.

This is the Gary Gorton ‘run on repo’ story. But this is not the only account of the financial crisis. Indeed, it is a very US-centric and incomplete theory, which forgets that housing booms occurred all around the world and that the primary driver of financial stress was not a withdrawing of wholesale (short-term repo in particular) funding from banks and other shadow banks, but a fear that the housing bust would make the banking system insolvent. The collateral story is only a part of this: most Spanish, Irish or German banks had nothing to do with the large wholesale-funded Wall Street broker-dealers that used some RMBSs as collateral in a number of trades. ‘Normal’ banks did not make extensive use of repos. They considered RMBSs, CMBSs and CDOs as higher-yielding investments, which they mostly held on balance sheet, sometimes as part of their liquidity portfolio.

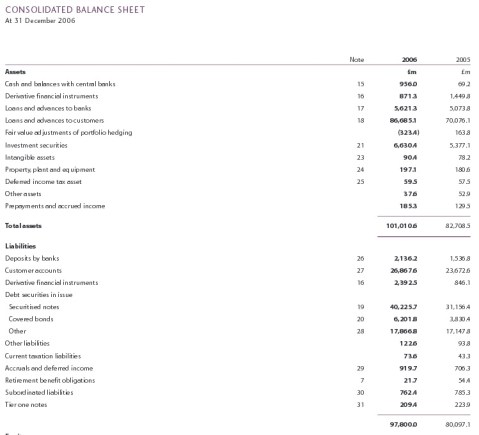

Moreover, remember UK-based Northern Rock. It suffered a bank run because depositors feared it could collapse. Why did they fear it could collapse? Because it was running out of liquidity as it was mostly wholesale-funded (but wasn’t using exotic securities as collateral for trades and wasn’t funded much with repos – see its end-2006 balance sheet below; this was a pretty straightforward retail bank, apart from the fact that it had a very high loans/deposit ratio of about 320%).

And why did its wholesale funding evaporated? For two reasons: 1. it had large exposures to the falling British housing market, and investors feared that it would fall into bankruptcy, and 2. some of the wholesale funding the bank was relying on was based on selling RMBS and CMBS to the market, which were not based on US subprime mortgages, but were still viewed as risky as house prices were on a downward path. Other British banks, which were seen as more diversified and safer by the market, such as HSBC, did not suffer such fate. So the ‘run on repo’ story of the financial crisis cannot comprehensively explain what happened.

They continue:

In retrospect, economists have concluded that a recession began in December 2007. But this recession started very mildly. Through early 2008, even as investors kept pulling money out of the shadow banks, key economic indicators such as inflation and nominal spending — the total amount of dollars being spent throughout the economy — barely budged. It looked as if the economy would be relatively unscathed, as many forecasters were saying at the time. The problem was manageable: According to Gary Gorton, an economist at Yale, roughly 6 percent of banking assets were tied to subprime mortgages in 2007.

Here, they assume too much. First, they assume that economic problems appear as soon as financial stress starts occurring. There is no evidence of that, and the slow and progressive slowdown in lending triggered by financial issues affect the economy with a lag. It is when total credit, and hence total money supply, starts contracting that the economy starts suffering.

Second, they assume that the problem was ‘manageable’, once again according to Gorton’s misleading figure. This is misunderstanding the underlying accounting. 6% of banking assets that fall by more than 50% in value is huge. Let me repeat that: it is huge. It means that more than 50% of banks’ capital has been disintegrated. Remember that, at this time, banks’ leverage (equity/assets) was in the 5 to 7% range, and even lower outside the US (like 2.5% to 6%). Meaning that a fall of asset value of between 5 and 8% was sufficient to make institutions insolvent (and even less if considering the harsher Basel criteria). Against all evidence, Beckworth and Ponnuru are telling us that it was ‘manageable’…

Moreover, and even more importantly, it is not only securities linked to subprime mortgages that fell in value: a number of non-subprime loans defaulted (or didn’t, but the fall in house prices forced banks to massively increase their provisioning, leading to losses that further eroded their capital base), in turn securities based on non-subprime loans also lost value, stock prices were falling, fixed income securities’ spreads were widening… Consequently, the percentage of US banks’ assets at risk wasn’t just 6%; it was much higher (although I can’t put an exact figure on this). There was nothing manageable about that. The amount of malinvestments that had accumulated before the crisis was staggering.

Don’t get me wrong though. Beckworth and Ponnuru are mostly right. Central banks did make huge mistakes. And inflation targeting is a bad policy that cannot properly respond to supply shocks. I cannot agree more. And I see a rule-based policy such as NGDP targeting as a second best to free banking (or perhaps third, if we include Selgin’s productivity norm).

But as I described in a separate post (to which Scott Sumner responded here, albeit avoiding my main points), too many economists simply tend to avoid talking about banks. Yet they face structural rigidities which, as I wrote in a number of other posts, make them crucial. Bank accounting frameworks and regulations directly impact the way monetary policy is transmitted and the way the broader money supply grows. Given how banking regulation is structured, malinvestments are hard-wired in lending expansion, meaning you don’t even need easy money to eventually trigger a crash. Accounting matters too: change a single rule such as mark-to-market accounting, and you’d surely have never experienced a crisis of the same scale.

So we can stick to the story that describes the crisis as a fall in NGDP, or we can question whether or not this NGDP growth trend was sustainable in the first place, or even whether or not the components of NGDP were sustainable (whereas the aggregate figure was) as Salter and Cachanosky would point out. It is not the topic of this post. But I believe we should not oversimplify the events that led to and followed the crisis. Yes, central banks’ reactions in the first year of the crisis were poor. The market monetarist story (i.e. tight monetary policy) is a good depiction of what amplified the crisis. But certainly not a comprehensive explanation of the boom and its subsequent dramatic correction.

PS: I have a few posts in the pipeline that review recent research that provides further empirical evidence in favour of my version of the story (i.e. regulation that leads to unsustainable housing, sovereign debt and exotic securities boom while depressing corporate lending – and hence possibly playing a major role in the weak recovery and the secular stagnation theory).

Hello bail-in – Goodbye bail-in

Some time ago, I wrote on the increasing complexity and opacity of bank capital standards, and mentioned the new TLAC and MREL frameworks, which effectively require banks to hold a certain amount of ‘bail-inable’ senior debt on their balance sheet in order to absorb losses if the institution fails. You may certainly have heard that the EU is full speed on the banking union thing and that everything is going to be marvellous.

Well it didn’t take long for the EU to undermine its own policies. Never underestimate politicians. In order to facilitate the implementation of the bail-in regime, Germany passed a law making all senior bondholders junior to depositors. Many people expected other countries to follow suit, but instead, France is working on a low to make senior bail-inable bondholders to become ‘junior-senior’, that is, to rank below all other senior bondholders and depositors but above junior bondholders in case of the bankruptcy of the firm. This doesn’t quite fit within the German framework. And it’s going to make it complicated when a cross-border multinational collapses.

And it continues, with Portuguese regulators actually cherry-picking which bondholders would suffer losses on the basis of ‘safeguarding financial stability’ and ‘based on public interest’ (see Bloomberg). Greece also avoided bailing in creditors when it benefited from its latest bailout. Meanwhile, Italian regulators aren’t happy because it is common in the country for savers to invest their money in retail bonds issued by banks.

Rating agencies confirmed that new rules might not end up applying to all investors equally, mostly due to political risk.

Clearly, the EU isn’t ready for anything close to a banking union. Cultures, practices and non-banking legal frameworks are too different to get ‘harmonised’ (at least in less than decades), as I pointed out elsewhere (see here). Despite the ECB taking over as single common regulator, local political discretion trumps rule application. When a bankruptcy occurs, it’s going to be necessary to disentangle the many layers of formal intertwined rules already in place combined with/modified by discretionary actions at various hierarchical levels. To say that it’s going to be a huge mess is an understatement.

Kant and Kirzner on the ‘enlightened’ market process

I have been updating myself on political philosophy, theory and history of thought for most of last year and I came across an interesting insight from Immanuel Kant.

Taken from an essay titled An Answer to the Question: ‘What is Enlightenment?, it is revealing as to the necessary conditions for a free market to function and, I believe complementary to Hayek’s and Kirzner’s view of the market process.

Kirzner, in his very clever Competition & Entrepreneurship takes position against the traditional neo-classical equilibrium view of markets. He argues that viewing microeconomic relationships under an equilibrium lens prevents us from understanding the underlying very dynamic and critical entrepreneurial process at play. He explains that entrepreneurs, far from being price takers mechanically adapting their structure of production to exogenous price changes, permanently thrive to find new ways to attract customers by differentiating products in ways that the market currently does not (seem to) exploit.

Kirzner’s story of entrepreneurship is a story of perceiving. As by nature humans are partly ignorant, it is an entrepreneur’s superior perception of opportunities that provide him with (often temporary) supernormal profits and perhaps lead him to a (also often temporary but deserved, and in customers’ short-run interest) monopoly position. Hence structures of production are constantly changing, driven (rightly or wrongly) by those perceived opportunities. Those opportunities exist because information is imperfect and constantly evolves: customers’ tastes, technological boundaries change. As no market actor is omniscient, opportunities arise. Moreover, entrepreneurs themselves can alter the market (and hence prices) by coming up with a new type of product (think about Apple and its iPhone).

Importantly, the market process takes time. There is no instantaneous entrepreneurial change. The market process works by trial and error. This means that, not only will there be some losers, but what is viewed as an ‘imperfect’ situation by some people can last for some time. Monopolies can be undone by more creative competitors (if barriers to entry aren’t artificially raised), but this process requires patience. And Kirzner emphasises the importance of letting entrepreneurs and the market experiment and search for the right solution, that is, the importance of freedom.

Kant defines ‘enlightenment’ as “man’s emergence from self-incurred immaturity”. In turn, this ‘immaturity’ emanates, “not from lack of understanding, but of lack and resolution and courage to use it without the guidance of another”, perhaps due to “laziness and cowardice”. He says:

It is so convenient to be immature! If I have a book to have understanding in place of me, a spiritual adviser to have a conscience for me, a doctor to judge my diet for me, and so on, I need not make any effort at all. I need not think, so long as I can pay; others will soon enough take the tiresome job over for me. The guardians who have kindly taken upon themselves the work of supervision will soon see to it that by far the largest part of mankind (including the entire fair sex) should consider the step forward to maturity not only as difficult but also as highly dangerous. Having first infatuated their domesticated animals, and carefully prevented the docile creatures from daring to take a single step without the leading-strings to which they are tied, they next show them the danger which threatens them if they tried to walk unaided. Now this danger is not in fact so very great, for they would certainly learn to walk eventually after a few falls. But an example of this kind is intimidating, and usually frightens them off from further attempts.

As a result, Kant believes that it is hard for each separate individual to become ‘mature’. However,

There is more chance of an entire public enlightening itself. This is indeed almost inevitable, if only the public concerned is left in freedom. (my emphasis)

According to Kant, freedom is key in enabling ‘maturity’ of the masses and hence ‘enlightenment’. Without freedom, society effectively remains in a state of underdeveloped slavery. However, here again the ‘enlightenment’ process isn’t instantaneous. Even once granted freedom to think freely, “the public can only achieve enlightenment slowly.”

While the remaining of Kant’s essay mostly focuses on religious matters, his reasoning is absolutely key to understanding the very essence of a free market. The parallel with Kirzner’s understanding of the market process is striking.

Both writers, in their own way, focus on freedom as the key enabler to prosperity. Freedom allows market actors to become more ‘mature’ by forcing them out of their ‘guided laziness’ to provide for themselves by slowly experimenting and discovering what the needs and tastes of potential customers are. This experimentation process takes time and is bound to lead to some mistakes and failures. But ultimately, through the experimentation of a multitude of entrepreneurs that have limited local knowledge and fragmented pieces of information, market order emerges. Markets, and society, become ‘enlightened’.

K&K also warn about the negative effects of the intervention of ‘guardians’ (for Kant) and government (for Kirzner). Enlightenment cannot be achieved if guardians intervene to attempt to ‘protect’ their ‘docile creatures’. And the market process cannot play its capital and goods allocative role if government intervenes to regulate monopolies or distort the capital allocation mechanism based on flawed welfare maximisation considerations.

In short, governments should get out of the way and certainly not attempt to protect consumers through paternalistic policies. Government’s only role is to ensure the continuity of the Rule of Law. Unfortunately, and as I have pointed out in a number of posts, our modern democratic process, along with the increased speed at which information circulates, has transformed society into an impatient one. When what is considered as a problem by some arises (whether it is a monopoly or a market ‘inefficiency’), governments are pushed to act, the sooner the better. Consequently, the crucial learning process that is inherent to Kant’s philosophy and Kirzner’s market process is prevented from functioning. The ‘docile creatures’ never learn, the ‘guardians’ gain ever more power, and the market process never achieves its full allocative effectiveness. In the long-run, we all end up poorer.

Unfortunately, there has been an almost continuous and disastrous trend in ‘protection’ in the post-WW2 era. In the finance industry protection has translated into thousands of pages of regulation (protection acting on the supply side), as well as regulators preventing customers from making their own choices and mistakes (protection on the demand side). A latest example was published by The Economist last week in an article titled Anti-choice: Regulators are keen to stop people making mistakes. Worryingly, the supposedly classical liberal newspaper doesn’t even question this paternalistic regulatory trend.

Preventing people from making mistakes is wrongheaded. Kant pointed it out in the 16th century and Kirzner and numerous others reformulated this view since the early 19th. Those views indirectly unleashed the industrial revolution. Regrettably, we have forgotten those teachings and this trend has now moved into reverse for a number of decades. The mechanism is simple: freedom and time forces society out of its laziness, leading to enlightenment, which leads to an effective, self-correcting and anti-fragile market process. By not respecting this sequence, we have forced our society to live through constantly recurring crises and, to require ever more ‘protection from ourselves’. Sadly, the solution to our woes has now become politically controversial: freedom and patience.

PS: I wrote a post about the importance of failure in free markets more than two years ago here. I also added that financial crashes following a liberalisation period were ‘normal’. That is, that they were part of the learning process that Kant describes. When the financial sector was tightly under control, market actors and consumers’ learning was effectively suppressed. Liberalisation restarts the process, hence the unsurprising crashes…

George Selgin weighs in on the excess reserves/MM debate

I used to feel lonely in the ‘banks do/don’t lend out reserves’ debate. Almost everyone on the blogosphere seemed to have been converted by either a rough ‘banks create money out of thin air’ (see here and here) or a more subtle MMT endogenous money version of the story (see here). Reserves, we were told, were pretty much useless in the ‘modern’ monetary system. They were only used for interbank settlements (which actually still implies some serious constraints on lending and deposit expansion, but whatever).

So all the Fed’s, ECB’s and BoE’s quantitative easing was futile because the excess reserves those policies created merely kept accumulating with no chance of ever being ‘lent out’, because the banking system as a whole could not get rid of excess reserves. It’s not how it worked we were told. We were doomed to live in a world of permanently high excess reserves.

Imagine my relief when George Selgin started publishing three massive posts on interest on reserves and the crisis (here, here and here, and of course, let’s not forget Justin Merrill’s post, which made similar remarks). It’s a fascinating and highly recommended read. I just wish to point out a couple of his comments on the new reserve myth.

Here’s George:

it’s simple: “reserves” and “excess reserves” aren’t the same thing. Banks can’t collectively get rid of “reserves” by lending them — the reserves just get shifted around, exactly as Walter and Courtois suggest. But banks most certainly can get rid of excess reserves by lending them, because as banks acquire new assets, they also create new liabilities, including deposits. As the nominal quantity of deposits increases, so do banks’ required reserves. As required reserves increase, excess reserves decline correspondingly. It follows that an extraordinarily large quantity of excess reserves is proof, not only of a large supply of reserves, but of a heightened real demand for such, and of an equivalently reduced flow of credit.

And again:

Here is that silly fallacy again: for the question isn’t whether a lower rate of IOR can reduce banks’ total reserve balances. It is whether it can reduce their excess (“idle”) balances by inducing them to lend more. For while such lending wouldn’t serve to reduce the aggregate stock of reserves, it would lead to an increase in the nominal quantity of bank deposits, and a proportional increase in banks’ required reserves. So, even as they caution their readers that “Language Matters,” Antinolfi and Keister blunder badly by neglecting to heed the crucial distinction between the total quantity of bank reserves, which no amount of bank lending can alter, and the quantity of excess reserves, which, by means of sufficient bank lending, might always be reduced to zero.

And after quoting Frances Coppola, he concludes:

There you have it: banks can hold on to reserves, and yet lend all they wish to (though not, for some reason, overnight). Such a marvelous business! Whoever said that one can’t have one’s cake and eat it, too?

Frances Coppola wasn’t really pleased and replied on Forbes. But she left me confused. She does start by saying that she had been ‘sloppy’ with her use of the term ‘excess reserves’:

For the US, it would indeed be possible for a bank to reduce its excess reserves by converting them to required reserves.

But then, in the comment section, she adds a qualification in her reply to George Selgin:

I have never said that individual banks could not “lend away” excess reserves. Clearly banks do lend reserves to each other: I have said this many times. But I dispute that banks COLLECTIVELY can lend away excess reserves. Banks do not lend reserves to non-banks. The only way reserves can leave the banking system is in the form of physical cash. That is the point I was making in the Forbes post you quoted.

Wait, I don’t follow. There is no case of fallacy of composition here. What is true for an individual bank is also true for the system as a whole. A given bank can get rid of excess reserves by growing its loan book. This triggers a reserve drain (either by cash withdrawal or interbank settlement), leading to a reduction in the amount of reserves that this bank holds at the central bank, and an offsetting gain for the receiving bank (if interbank transfer).

But, given a fixed amount of excess reserves in the banking system, the system as a whole simply has to increase the amount of credit (and hence deposits) it extends in order to get rid of the reserves that it has in excess. For instance, if the system has 500 units of required reserves and 100 of excess reserves (600 in total), and that it is subject to a 10% reserve requirement, it merely has to grow its lending by 1,000 units to get rid of its excess. Total reserves in the system would not change (600), but excess reverses would all but vanish as they get converted into ‘required’ ones. This is precisely George’s point.

(of course things work a bit differently in systems with no reserve requirements, but as I have said elsewhere, an informal, market-determined, reserve requirement play the same role)

Let me remind my readers that the same situation occurred during the Great Depression. Excess reserves spiked and the money multiplier collapsed (see this previous post of mine and the following nice chart from Mark Sadowski). It then took 30 years for the multiplier to bounce back from its lows to close to its previous highs:

However, she’s very right that banks are/were also constrained by capital and liquidity requirements, and that the crisis is likely the primary driver of a reduction in lending. But it doesn’t seem to me that George disputes this.

I tend to agree with her that George seems to be underestimating the impact of regulatory capital requirements to an extent. I described in another post that regulators don’t seem to care much about regulatory minima or about whether or not a bank still have some loss-absorbing capital left: they force bank management to raise capital when it becomes lower than where they’d like it to be (even if capital ratios remain above minima they have themselves defined in the first place… go figure).

Consequently, despite having ‘excess capital’ from a formal and official point of view, banks did not have enough capital from the discretionary point of view of regulators in charge. They were forced to maintain or raise capital levels in the middle of the worst financial crisis in 50 years. Hard to think of a better pro-cyclical stance. Worse, from 2010 onwards, new tighter regulatory requirements were progressively implemented, which is in effect not the most effective way of kick-starting an economic recovery.

PS: I think Frances’ point that commercial banking rates were well above IOER and so are unlikely to hinder lending is more unclear than she thinks. Only risk-adjusted rates could give us an answer, as credit risk premia jump during a crisis, and capital requirements increase as customers suffer from rating downgrades. Moreover, liquidity risk also jumps so the liquidity premium associated to lending is raised (i.e. better to reduce profitability temporarily to survive in the long-run by not putting pressure on reserves). So at the end of the day, it’s hard to say whether the margin made on those loans was sufficient to cover the increased risk of loan loss and the increased risk of getting illiquid, especially after factoring in the operating costs of monitoring those borrowers (as opposed to pretty much zero operating cost in leaving the money at the central bank).

A critique of Werner’s view on banking

I have already published a quick critique of one of Prof Richard Werner’s previous papers on banking theory and money endogeneity some time ago, but, following the publication of a new, follow-up, paper on the same topic I thought I should deconstruct his arguments a little more comprehensively.

Werner published last September a follow up paper to his previous one Can banks individually create money out of nothing?, titled A lost century in economics: Three theories of banking and the conclusive evidence. Werner adheres to a form of endogenous money theory that differs from the MMT version. And, as I have repeatedly wrote on this blog, I strongly disagree with those theories. Werner’s view is pretty specific though, and, unlike MMT doesn’t seem to be an ‘endogenous outside money theory’. It is wrong nevertheless.

Overall, my criticisms are similar to those I had about his previous papers. I think that the main (big) issue with Werner’s papers is that he distinguishes three main banking theories that are in reality mostly undistinguishable, and proceeds to draw misleading conclusions from those effectively virtual definitions. He classifies banking theories as follows:

- Financial intermediation theory: supposedly dominant in the economics field, with proponents such as Keynes, Mises, Gorton, Diamond and Dybvig, Tobin, Bernanke, Krugman, Admati and so forth, and which says that banks aren’t different from other non-bank financial institutions. Werner describes this theory as “banks borrow from depositors with short maturities and lend to borrowers at longer maturities” and are “unable to create money.” According to Werner, this theory implies that deposits are held in segregated accounts and hence not shown on banks’ balance sheet.

- Fractional reserve theory: supposedly mostly agrees with the previous theory but disagrees with it in that the banking system creates money (read, deposits) through the ‘money multiplier’ process, with Phillips and his Bank Credit, as well as Samuelson, Hayek but also Keynes (who apparently supports two opposite theories… though I wouldn’t be surprised knowing him) as main proponents.

- Credit creation theory: supposedly at odds with the two previous theories, as banks are considered to be able to create money out of thin air by the simple act of lending or buying assets, and without securing deposits/reserves first. Apparent supporters were Macleod, Schumpeter, Wicksell, and even…Keynes (yes, him again…)… Werner sums up the theory as “according to the credit creation theory then, banks create credit in the form of what bankers call ‘deposits’, and this credit is money.” An ‘important’ difference with the fractional reserve theory is that a single bank can create deposits. This is the theory Werner subscribes to.

I believe there is a big misunderstanding here. In reality, those three ‘theories’ all massively overlap, if not represent the exact same thing. I am still absolutely baffled by Prof Werner’s claim that believing that banks are financial intermediaries imply that deposits are held in segregated accounts… He then attempts to disprove this theory by simply…opening banks’ annual reports. But everybody already knows that deposits appear on banks’ balance sheet. I have never ever seen any claim to the contrary, in any textbook or banking theory article. Depositors have been legally considered bank creditors since the 19th century and, as all credit/funding instruments, deposits have to appear on the liability side of the balance sheet. There really is no news here, and none of the economists who supposedly believe in the intermediation theory believe that deposits are off-balance sheet.

Second, the financial intermediation and fractional reserve theories are one and the same. As we have just explained, the financial intermediation theory never implied that deposits were segregated, like at other non-bank financial institutions. This theory is a fractional reserve theory. It mostly emanates from Tobin’s very famous article Commercial Banks as Creators of ‘Money’, in which he exposes his ‘New View’. Tobin’s article is about the limit to deposit expansion (see my take on the Tobin-Yeager debate here). He espouses the fractional reserve model. He certainly doesn’t believe in the exposition of the theory attributed to him by Werner.

Third, as the title of the Tobin’s article suggest, the two previous theories also state that banks create money by the act of lending. So they largely overlap with Werner’s definition of the Credit creation theory. However, where they disagree is in the origins of this ‘money’. For the first two theories, deposits are a source of funding that are consequently lent out to borrowers (roughly, see below). For Werner’s last theory, money is created out of thin air.

Let’s reconcile it all. It is by intermediating between savers/depositors and borrowers that fractional reserve banks create money. Maturity transformation implies that banks borrow short-term (from depositors) and lend long-term (to borrowers). Liquidity risk arises from this process, because depositors are still supposed to have access to their money, which has in fact been lent out to other customers of the bank. So banks, at the same time, are intermediaries and create money through credit extension, resulting in many different claims on the same unit of base money (i.e. reserves, or high-powered money). This is the money multiplier model.

So the ‘money’ that banks create out of thin air is in fact a claim on base money. And there are limits to this extension, which I have highlighted in my many posts on endogenous money theory.

One of those limits is the adverse clearing that occurs during interbank settlement, which is barely discussed in Werner’s papers. Werner wrongly claims in his article that “for this fractional reserve model to work, Samuelson is assuming that the new deposit is a cash deposit, and the extension of the loan takes the form of paying out cash.” He further adds:

Thus a further inconsistency is that it is a priori not clear why customer deposits or reserves should be any constraint on bank lending as claimed by the fractional reserve theory: since deposits are a record of the bank’s debt to customers, the bank is not restricted to lending only as much as its excess reserves or prior customer deposits allow. It can extend a loan and record further debts to customers, shown as newly created deposits (as the credit creation theory states).

There is no need for cash to be paid out to be a drain on the reserve/liquidity position of the bank. And banks (individually, or as a whole) cannot expand indefinitely either. Interbank settlements, through the adverse clearing process, operate as a very good limiting constraint, unless there is an exact offsetting amount that the counterparty bank owes (in which case no reserve transfer occurs and limits to expansion are defined by other criteria).

Werner does eventually mention this point however, albeit too briefly given how crucial it is:

As long as banks create credit at the same rate as other banks, and as long as customers are similarly distributed, the mutual claims of banks on each other will be netted out and may well, on balance, cancel each other out. Then banks can increase credit creation without limit and without ‘losing any money’.

While this is theoretically true, this is highly unrealistic, as I have explained in this post:

[The BoE economists] seem to believe that all banks could expand simultaneously, resulting in each bank avoiding adverse clearing and loss of reserves. This situation cannot realistically occur. Each bank wishes to have a different risk/return profile. As a result, banks with different risk profile would not be expanding at the exact same time, resulting in the more aggressive ones losing reserves at the expense of the more conservative ones in the medium term, stopping their expansion. At this point, we get back to the case I (and they) made of what happens to over-expanding single banks.

Please note that banks do not need to secure reserves before lending in the fractional reserve model, unlike what Werner claims. What they do need to do is to secure reserves before they are transferred to another bank or withdrawn as cash by the customer*. If one of those two events occurs and our bank hasn’t got the required reserves to settle, it causes an event of default. And bank managers don’t like events of default much. Which is why banks have dedicated treasury and asset/liability management teams that attempt to secure funding sources (i.e. reserves), as cheaply as possible.

All of those issues make Werner believe that modulating reserve requirements cannot work to control banking expansion. Yet all empirical evidences seem to be against him. Many central banks across the world use RR to tame or boost lending (China, Turkey, Brasil…) and evidences seem to show that it works (see here for a recent paper on Brazil for instance).

Finally, his empirical test is flawed, as was his previous one (see here). His credit creation theory of money (which is quite similar to this very rough one published by some BoE staff earlier this year) cannot be demonstrated by making a single small loan to a virtual customer of a given bank.

There is one thing that Werner got very right though, and it is that BoE publications have been overly confusing, if not completely contradictory, over the past few years. But it’s not a reason to add to the confusion.

*In an ideal world, that is, when the borrower utilises his newly acquired fund to pay another customer of the same bank, an individual bank does not have to secure reserves. But if the second customer does in turn transfer his cash to another bank, well, you know what happens.

The Regulatory Risk Strikes Back

Back to blogging (happy new year everyone), after a pretty busy two last months of the year. I have read quite a few interesting research papers that are worth mentioning on this page. They’re going to keep me busy for the next few weeks.

But first, a short post for today. I have noticed an increasing backlash against finance regulation in the second half of last year. It looks like an increasing number of academics is worrying about the potential collateral damages and hidden risks of the new regulatory framework. Meanwhile politicians are also worrying that economic growth could get affected (as well as donations by finance firms?…), which is convenient given that they favoured short-term vote-grabbing by bashing banks for years after the crisis.

According to SNL (gated link), the BIS, the temple of all banking regulation, warned that

despite its risk reduction benefits, central clearing could present other forms of systemic risk, in particular that the concentration of the management of credit and liquidity risk “may affect system-wide market price and liquidity dynamics in ways that are not yet understood”

Even more surprising, the head of supervision at the central bank of Italy declared that the new bail-in rule could “exacerbate – rather than alleviate – the risks of systemic instability caused by the crisis of individual banks.” I thought European policymakers were proud of their bail-in/resolution directive. Apparently not all of them.

In Germany, Merkel adds her voice to the growing ‘let’s put everything in common’ trend that has been dominating EU top circles over the past few years: she’s opposed to the European bank deposit guarantee scheme. And she’s probably right, given that research has demonstrated that deposit guarantees actually worsened financial stability.

And of course, the banking sector keeps complaining about regulation and monetary policy, as it has been doing for years now (rightly or wrongly, but always accused of lobbying at the expense of society): Danske Bank warns that negative rates are increasingly damaging the financial industry (margin compression, here we go again).

Some of the above claims are actually substantiated by some of the papers I will talk about over the next few weeks. So stay tuned.

Recent Comments