The real reason the Federal Reserve started paying interest on reserves (guest post by Justin Merrill)

I am fascinated by recent policies of interest on reserves, both positive and negative. I understand the argument for the People’s Bank of China paying interest on its deposits since they have a combination of a large balance sheet and high reserve ratios in order to control their exchange rate; their banks would go broke if 20% of their assets earned no income and their domestic inflation would run rampant if they didn’t curb lending. I also understand the logic for negative interest rates to stimulate the economies in Europe. I disagree with these policies, but there’s an internally coherent argument there. What hasn’t made sense to me is the Federal Reserve’s policy of paying interest on both required and excess reserves.

Why would the Fed simultaneously start the counterproductive policies of quantitative easing (QE) and interest on reserves (IOR)? Why would the Fed pursue the deflationary policy of IOR throughout the crisis when labor markets were weak and inflation was usually below their target? What if they could have achieved their policy goals as well or better by sticking to more traditional policies and not been stuck with such a large balance sheet and potential exit problem? My cynical intuition was that it was just a backdoor bailout to banks.

Determined to find the answer, I looked for statements and other sources from the Fed to find out the history of and justifications for IOR. What I finally found confirmed my suspicions and I think shows a big flaw in the Fed’s transparency and policy. What recently renewed my interest was Chair Janet Yellen’s Congressional testimony before the Senate in February, 2015. Senator Pat Toomey asked her about interest on reserves policy. Toomey used to be a bond trader, so he’s more financially savvy than most of his peers. I will summarize their dialogue about IOR but the video is available here and starts a little before one hour-seventeen minutes in: http://www.c-span.org/video/?324477-1/federal-reserve-chair-janet-yellen-testimony-monetary-policy

PT: In the past the Fed conducted monetary policy via Open Market Operations. You have said that you intend to raise the Fed Funds rate by increasing the interest paid on reserves. Since this will transfer money to big money center banks that would have gone to tax payers, why are you doing that instead of simply selling bonds? (emphasis added)

JY: We are paying banks a rate comparable with the market, so there is not a subsidy to banks. Our future contributions may decline when interest rates rise, but our contributions to the Treasury have been enormous in recent times.

Notice what she didn’t answer? The part of his question about why they are even using IOR at all!

According to the Fed’s Oct 6, 2008, press release:

The Financial Services Regulatory Relief Act of 2006 originally authorized the Federal Reserve to begin paying interest on balances held by or on behalf of depository institutions beginning October 1, 2011. The recently enacted Emergency Economic Stabilization Act of 2008 accelerated the effective date to October 1, 2008.

So we know the Fed was interested in using IOR as a tool prior to the crisis but weren’t in a hurry to do so until after the Lehman shock. The expedited authorization came from the TARP bill. So why were they interested in using it at all, and why did it become urgent and necessary in late September, 2008? The press release mentions “Paying interest on required reserve balances should essentially eliminate the opportunity cost of holding required reserves, promoting efficiency in the banking sector” and “Paying interest on excess balances should help to establish a lower bound on the federal funds rate. […] The payment of interest on excess reserves will permit the Federal Reserve to expand its balance sheet as necessary to provide the liquidity necessary to support financial stability while implementing the monetary policy that is appropriate in light of the System’s macroeconomic objectives of maximum employment and price stability.”

So paying interest on required reserves “promotes efficiency?” I think they are channeling Milton Friedman’s observation that reserve requirements are a tax on banks by forcing them to hold non-income earning assets. I’m not a fan of reserve requirements, and maybe it could be argued that they encourage disintermediation or alternative financing schemes that aren’t subject to the regulation, such as shadow banking, and that by paying IORR it offsets that. Fine, what I think is more interesting is the justification for interest on excess reserves. Why were they trying to provide liquidity without creating price inflation or overheating the labor market? Core CPI was below 2% at the time, PCE (an indicator the Fed looks at) was sharply negative, GDP numbers for the first two quarters were really weak and unemployment was trending up and was above 6% since August. There’s a lag to data, but in the October-early December timeframe we are focusing on here, they would have at least had August’s numbers.

Still not satisfied, I looked around at almost a dozen other Fed sources that tried to justify IOR. All of the sources said two or three things in particular: “Milton Friedman told us to pay interest on required reserves in 1959*, Marvin Goodfriend told us IOR could be used as a policy tool in 2002 and in 2008 we were having a hard time hitting our Fed Funds target.” I know hindsight is 20/20, but given the economic environment explained above, if you are providing liquidity and the economy is still stalling and you are missing your Fed Funds target on the low side, the problem is your target! You must REALLY trust your models to be so confident that a Fed Funds rate of two percent is worth defending in a liquidity crisis. I was about to chalk up the policy to mere incompetence and panicking in the fog of war when I came across this wonderful essay published by the Richmond Fed. It actually gives a fully honest account of what happened and why it was deemed urgent to start IOR:

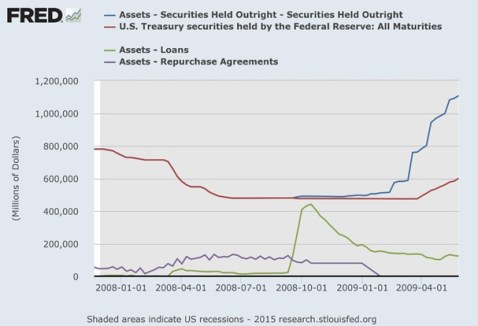

This feature became important once the Fed began injecting liquidity into financial markets starting in December 2007 to ease credit conditions. In making these injections, the Fed created money to extend loans to financial institutions. Those institutions provided as collateral securities from their portfolio that had, as a result of the financial market turmoil, become difficult to trade and value. This action essentially replaced illiquid assets in their portfolio with a credit to their account at the Fed, which would add reserves to the banking system. Adding reserves to the system will, under usual circumstances, exert downward pressure on the fed funds rate. At the time the Fed was not yet facing the zero-lower-bound on interest rates that it faces today. Thus, the injections had the potential to push the fed funds rate below its target, increasing the overall supply of credit to the economy beyond a level consistent with the Fed’s macroeconomic policy goals, particularly concerning price stability. To avoid this outcome, the Fed “sterilized” the effect of liquidity injections on the overall economy: It sold an equal amount in Treasury securities from its own account to banks. Sterilization offset the injections’ effect on the monetary base and therefore the overall supply of credit, keeping the total supply of reserves largely unchanged and the fed funds rate at its target. Sterilization reduced the amount in Treasury securities that the Fed held on its balance sheet by roughly 40 percent in a year’s time, from over $790 billion in July 2007 to just under $480 billion by June 2008. However, following the failure of Lehman Brothers and the rescue of American International Group in September 2008, credit market dislocations intensified and lending through the Fed’s new lending facilities ballooned. The Fed no longer held enough Treasury securities to sterilize the lending.

This led the Fed to request authority to accelerate implementation of the IOR policy that had been approved in 2006. Once banks began earning interest on the excess reserves they held, they would be more willing to hold on to excess reserves instead of attempting to purge them from their balance sheets via loans made in the fed funds market, which would drive the fed funds rate below the Fed’s target for that rate. When the Fed stopped sterilizing its liquidity injections, the monetary base (which is comprised of total reserves in the banking system plus currency in circulation) ballooned in line with Fed lending, from about $847 billion in August 2008 to almost $2 trillion by October 2009. However, this did not result in a proportional increase in the overall money supply. This result is likely due largely to an undesirable lending environment: Banks likely found it more desirable to hold excess reserves in their accounts at the Fed, earning the IOR rate with zero risk, given that there were few attractive lending opportunities. That the liquidity injections did not result in a proportional increase in the money supply may also be due to banks’ increased demand to hold liquid reserves (as opposed to individually lending those excess reserves out) in the wake of the financial crisis.

So the truth is that when the subprime mortgage crisis blew-up in December, 2007 the Fed started SELLING hundreds of billions in treasuries to sterilize their credit facility that engaged in repo of MBS. Since this did not provide aggregate liquidity, this was not a lender of last resort function, this was a credit policy to support MBS. Then after Bear Stearns failed in March, 2008 the Fed sold more treasuries to make billions in direct loans to firms such as Bear (to aid in their purchase by JP Morgan) and AIG. At their peak, during the Lehman shock, their direct lending totaled well over $400 billion, or about half their balance sheet.

http://research.stlouisfed.org/fred2/graph/?g=16fS

http://research.stlouisfed.org/fred2/graph/?g=16fS

The damning truth is the Fed felt the urgent need to institute IOR because they were running low on treasuries but wanted to provide more liquidity. They were afraid to initially expand their balance sheet because in October, 2008 they were still concerned about inflation! Talk about missing the mark. They were concerned because the Fed Funds rate was below their target and they couldn’t control it. What they don’t seem to realize is that the Fed Funds is a barometer of liquidity. You don’t make the weather warmer by tricking your thermometer into not going below 70 degrees. I suspect it is the “Neo-Wicksellians” like Michael Woodford who took the money out of Wicksell who are to blame for this. This is a perfect example of Goodhart’s Law: “when a measure becomes a target, it ceases to be a good measure.” You can see in the chart below they tried, and failed, to create an interest rate channel by initially pegging the interest on excess reserves lower than the target rate. Eventually they gave up and harmonized all the rates at 25 bps. The effective Fed Funds remained below that because some institutions, such as the GSEs, have access to the Fed Funds market but not deposits at the Fed. This means there’s an arbitrage opportunity for banks to borrow on the Fed Funds market and deposit at the Fed. Since GSEs were nationalized, this might be considered another public subsidy. Either way, the primary dealer model and other differential treatment of institutions is broken.

http://research.stlouisfed.org/fred2/graph/?g=16fY

http://research.stlouisfed.org/fred2/graph/?g=16fY

We no longer have the initial conditions that justified interest on reserves. We are not above the ZLB and fearing inflation while wanting to increase the balance sheet. We are in the exact opposite. The Fed should normalize, including abandoning IOR. This is Bernanke’s legacy. The same man who promised, “We won’t do it again” got so caught up in the act of directing credit, experimenting with new tools and obeying his models that he forgot to listen to Bagehot’s advice or even professor Bernanke’s.

*Friedman, Milton. 1959. A Program for Monetary Stability.

5 responses to “The real reason the Federal Reserve started paying interest on reserves (guest post by Justin Merrill)”

Trackbacks / Pingbacks

- - 14 January, 2016

Leave a comment

Recent Comments

| pslebow on ‘Sovereign money’:… | |

| pslebow on A critique of Werner’s view on… | |

| Hugo Kramer on Welcome to Spontaneous Fi… | |

| Nathan on A critique of Werner’s view on… | |

| Nathan on More, more, more money endogen… |

Very interesting post, but may I just ask, if Fed now abandoned IOR, would there be a chance of too high inflation since banks wouldn’t have any more incentive to hold their reserves. How could Fed prevent that later?

I think the Fed could abandon IOR without causing either financial turmoil or inflation by letting their balance sheet normalize over time. The Fed estimates that by maybe 2019 their balance sheet will be about $1 trillion, down from the recent highs of $4 trillion. They could accelerate that slightly and with no IOR. I also think the Fed should stop playing with the yield curve and undo Operation Twist, which means selling off their long dated assets and buying more bills.

Keep in mind that Japan did QE in the 90’s without IOR and it didn’t produce massive inflation. I don’t think the US is in the exact same economic situation, but there is precedence. In fact, Japan didn’t start paying IOR until 2010.

Whether the Fed pays IOER or not would have no impact whatsoever on the level of excess reserves. That can only change by action of the Fed buying or selling assets. IOER is a subsidy because the taxpayers bear the cast. Yellin is a lying pig, following in the footsteps of financial mass murderer of elderly savers, Bernanke.

Fed Again Issues Surreptitious SNAP Payments to Bankster Welfare Queens At Taxpayer Expense http://wp.me/p2r1d8-QbD

I agree that IOER is a taxpayer subsidy. IOER does however have an impact on the composition, but not the amount, of the Fed’s liabilities. It disincentivizes bank lending or purchasing securities that would grow the inside money supply, which would increase the public’s holding of currency and deposits that banks would legally need to hold reserves against (switching the excess reserves into currency or required reserves). So the aggregate amount of the monetary base is controlled by the Fed’s balance sheet, but the composition is influenced by IOER.