The real reason the Federal Reserve started paying interest on reserves (guest post by Justin Merrill)

I am fascinated by recent policies of interest on reserves, both positive and negative. I understand the argument for the People’s Bank of China paying interest on its deposits since they have a combination of a large balance sheet and high reserve ratios in order to control their exchange rate; their banks would go broke if 20% of their assets earned no income and their domestic inflation would run rampant if they didn’t curb lending. I also understand the logic for negative interest rates to stimulate the economies in Europe. I disagree with these policies, but there’s an internally coherent argument there. What hasn’t made sense to me is the Federal Reserve’s policy of paying interest on both required and excess reserves.

Why would the Fed simultaneously start the counterproductive policies of quantitative easing (QE) and interest on reserves (IOR)? Why would the Fed pursue the deflationary policy of IOR throughout the crisis when labor markets were weak and inflation was usually below their target? What if they could have achieved their policy goals as well or better by sticking to more traditional policies and not been stuck with such a large balance sheet and potential exit problem? My cynical intuition was that it was just a backdoor bailout to banks.

Determined to find the answer, I looked for statements and other sources from the Fed to find out the history of and justifications for IOR. What I finally found confirmed my suspicions and I think shows a big flaw in the Fed’s transparency and policy. What recently renewed my interest was Chair Janet Yellen’s Congressional testimony before the Senate in February, 2015. Senator Pat Toomey asked her about interest on reserves policy. Toomey used to be a bond trader, so he’s more financially savvy than most of his peers. I will summarize their dialogue about IOR but the video is available here and starts a little before one hour-seventeen minutes in: http://www.c-span.org/video/?324477-1/federal-reserve-chair-janet-yellen-testimony-monetary-policy

PT: In the past the Fed conducted monetary policy via Open Market Operations. You have said that you intend to raise the Fed Funds rate by increasing the interest paid on reserves. Since this will transfer money to big money center banks that would have gone to tax payers, why are you doing that instead of simply selling bonds? (emphasis added)

JY: We are paying banks a rate comparable with the market, so there is not a subsidy to banks. Our future contributions may decline when interest rates rise, but our contributions to the Treasury have been enormous in recent times.

Notice what she didn’t answer? The part of his question about why they are even using IOR at all!

According to the Fed’s Oct 6, 2008, press release:

The Financial Services Regulatory Relief Act of 2006 originally authorized the Federal Reserve to begin paying interest on balances held by or on behalf of depository institutions beginning October 1, 2011. The recently enacted Emergency Economic Stabilization Act of 2008 accelerated the effective date to October 1, 2008.

So we know the Fed was interested in using IOR as a tool prior to the crisis but weren’t in a hurry to do so until after the Lehman shock. The expedited authorization came from the TARP bill. So why were they interested in using it at all, and why did it become urgent and necessary in late September, 2008? The press release mentions “Paying interest on required reserve balances should essentially eliminate the opportunity cost of holding required reserves, promoting efficiency in the banking sector” and “Paying interest on excess balances should help to establish a lower bound on the federal funds rate. […] The payment of interest on excess reserves will permit the Federal Reserve to expand its balance sheet as necessary to provide the liquidity necessary to support financial stability while implementing the monetary policy that is appropriate in light of the System’s macroeconomic objectives of maximum employment and price stability.”

So paying interest on required reserves “promotes efficiency?” I think they are channeling Milton Friedman’s observation that reserve requirements are a tax on banks by forcing them to hold non-income earning assets. I’m not a fan of reserve requirements, and maybe it could be argued that they encourage disintermediation or alternative financing schemes that aren’t subject to the regulation, such as shadow banking, and that by paying IORR it offsets that. Fine, what I think is more interesting is the justification for interest on excess reserves. Why were they trying to provide liquidity without creating price inflation or overheating the labor market? Core CPI was below 2% at the time, PCE (an indicator the Fed looks at) was sharply negative, GDP numbers for the first two quarters were really weak and unemployment was trending up and was above 6% since August. There’s a lag to data, but in the October-early December timeframe we are focusing on here, they would have at least had August’s numbers.

Still not satisfied, I looked around at almost a dozen other Fed sources that tried to justify IOR. All of the sources said two or three things in particular: “Milton Friedman told us to pay interest on required reserves in 1959*, Marvin Goodfriend told us IOR could be used as a policy tool in 2002 and in 2008 we were having a hard time hitting our Fed Funds target.” I know hindsight is 20/20, but given the economic environment explained above, if you are providing liquidity and the economy is still stalling and you are missing your Fed Funds target on the low side, the problem is your target! You must REALLY trust your models to be so confident that a Fed Funds rate of two percent is worth defending in a liquidity crisis. I was about to chalk up the policy to mere incompetence and panicking in the fog of war when I came across this wonderful essay published by the Richmond Fed. It actually gives a fully honest account of what happened and why it was deemed urgent to start IOR:

This feature became important once the Fed began injecting liquidity into financial markets starting in December 2007 to ease credit conditions. In making these injections, the Fed created money to extend loans to financial institutions. Those institutions provided as collateral securities from their portfolio that had, as a result of the financial market turmoil, become difficult to trade and value. This action essentially replaced illiquid assets in their portfolio with a credit to their account at the Fed, which would add reserves to the banking system. Adding reserves to the system will, under usual circumstances, exert downward pressure on the fed funds rate. At the time the Fed was not yet facing the zero-lower-bound on interest rates that it faces today. Thus, the injections had the potential to push the fed funds rate below its target, increasing the overall supply of credit to the economy beyond a level consistent with the Fed’s macroeconomic policy goals, particularly concerning price stability. To avoid this outcome, the Fed “sterilized” the effect of liquidity injections on the overall economy: It sold an equal amount in Treasury securities from its own account to banks. Sterilization offset the injections’ effect on the monetary base and therefore the overall supply of credit, keeping the total supply of reserves largely unchanged and the fed funds rate at its target. Sterilization reduced the amount in Treasury securities that the Fed held on its balance sheet by roughly 40 percent in a year’s time, from over $790 billion in July 2007 to just under $480 billion by June 2008. However, following the failure of Lehman Brothers and the rescue of American International Group in September 2008, credit market dislocations intensified and lending through the Fed’s new lending facilities ballooned. The Fed no longer held enough Treasury securities to sterilize the lending.

This led the Fed to request authority to accelerate implementation of the IOR policy that had been approved in 2006. Once banks began earning interest on the excess reserves they held, they would be more willing to hold on to excess reserves instead of attempting to purge them from their balance sheets via loans made in the fed funds market, which would drive the fed funds rate below the Fed’s target for that rate. When the Fed stopped sterilizing its liquidity injections, the monetary base (which is comprised of total reserves in the banking system plus currency in circulation) ballooned in line with Fed lending, from about $847 billion in August 2008 to almost $2 trillion by October 2009. However, this did not result in a proportional increase in the overall money supply. This result is likely due largely to an undesirable lending environment: Banks likely found it more desirable to hold excess reserves in their accounts at the Fed, earning the IOR rate with zero risk, given that there were few attractive lending opportunities. That the liquidity injections did not result in a proportional increase in the money supply may also be due to banks’ increased demand to hold liquid reserves (as opposed to individually lending those excess reserves out) in the wake of the financial crisis.

So the truth is that when the subprime mortgage crisis blew-up in December, 2007 the Fed started SELLING hundreds of billions in treasuries to sterilize their credit facility that engaged in repo of MBS. Since this did not provide aggregate liquidity, this was not a lender of last resort function, this was a credit policy to support MBS. Then after Bear Stearns failed in March, 2008 the Fed sold more treasuries to make billions in direct loans to firms such as Bear (to aid in their purchase by JP Morgan) and AIG. At their peak, during the Lehman shock, their direct lending totaled well over $400 billion, or about half their balance sheet.

http://research.stlouisfed.org/fred2/graph/?g=16fS

http://research.stlouisfed.org/fred2/graph/?g=16fS

The damning truth is the Fed felt the urgent need to institute IOR because they were running low on treasuries but wanted to provide more liquidity. They were afraid to initially expand their balance sheet because in October, 2008 they were still concerned about inflation! Talk about missing the mark. They were concerned because the Fed Funds rate was below their target and they couldn’t control it. What they don’t seem to realize is that the Fed Funds is a barometer of liquidity. You don’t make the weather warmer by tricking your thermometer into not going below 70 degrees. I suspect it is the “Neo-Wicksellians” like Michael Woodford who took the money out of Wicksell who are to blame for this. This is a perfect example of Goodhart’s Law: “when a measure becomes a target, it ceases to be a good measure.” You can see in the chart below they tried, and failed, to create an interest rate channel by initially pegging the interest on excess reserves lower than the target rate. Eventually they gave up and harmonized all the rates at 25 bps. The effective Fed Funds remained below that because some institutions, such as the GSEs, have access to the Fed Funds market but not deposits at the Fed. This means there’s an arbitrage opportunity for banks to borrow on the Fed Funds market and deposit at the Fed. Since GSEs were nationalized, this might be considered another public subsidy. Either way, the primary dealer model and other differential treatment of institutions is broken.

http://research.stlouisfed.org/fred2/graph/?g=16fY

http://research.stlouisfed.org/fred2/graph/?g=16fY

We no longer have the initial conditions that justified interest on reserves. We are not above the ZLB and fearing inflation while wanting to increase the balance sheet. We are in the exact opposite. The Fed should normalize, including abandoning IOR. This is Bernanke’s legacy. The same man who promised, “We won’t do it again” got so caught up in the act of directing credit, experimenting with new tools and obeying his models that he forgot to listen to Bagehot’s advice or even professor Bernanke’s.

*Friedman, Milton. 1959. A Program for Monetary Stability.

Pushing market rationality too far

In a new post on Switzerland, Scott Sumner said (my emphasis):

The following graph shows that the SF has fallen from rough parity with the euro after the de-pegging, to about 1.08 SF to the euro today:

And this graph shows that the Swiss stock market, which crashed on the decision that some claimed was “inevitable” (hint, markets NEVER crash on news that is inevitable), has regained most of its losses.

I often enjoy what Scott Sumner writes, but this comment is from someone who doesn’t understand, or has no experience in, financial markets. We all know that Sumner strongly believes in rational expectations and the EMH. But this is pushing market efficiency and rationality too far.

According to Sumner, “markets never crash on news that is inevitable”. Really? Is he saying that markets believed the Euro peg would remain in place forever (which is the only necessary condition for the de-pegging not being ‘inevitable’)?

In reality many investors, if not most (though it can’t be said with certainty), were aware that the peg would be removed and of the resulting potential consequences for Swiss companies. So why the crash?

While investors surely knew that the peg wouldn’t last, they didn’t know when it would end. They were acting on incomplete information. However, this is perhaps what Sumner implies: the Swiss central bank should have provided markets with a more precise statement of when, and in what conditions, the peg would end. Markets would have revised their expectations and priced in the information. This reasoning underpins the rationale for monetary policy rules and forward guidance. But in practice, providing ‘guidance’ isn’t easy: central bankers are not omniscient, have imperfect access to information and cannot accurately forecast the future in an ever-changing world. See what happened to the BoE’s forward guidance policy, which ended up not being much guidance at all as central bankers changed their minds as the economic situation in the UK evolved*.

But the rational expectations argument itself can be used to describe many different situations. If investors believe the peg will end at some point, but don’t know exactly when, it is arguably as ‘rational’ for them to try to maximise gains as long as they could and to try to exit the market just before it crashes, as it is ‘rational’ to adapt their positions to minimise their risk exposure. When the market finally does crash, it often overshoots, for the same reason: benefiting from a short-term situation to maximise profits.

Taking advantage of monetary policy is what traders do. It is their job. Of course, many will fail in their attempt. But necessarily identifying rational expectations with strong short-term risk-aversion and immediate inclusion of external information into prices is abusive.

This latest Bloomberg article shows that close to 20% of traders expect the Fed to raise rates in June, and consequently have surely put in place trading strategies around this belief, and are likely to react negatively if their expectations aren’t fulfilled. However, who doubts that a rate rise is ‘inevitable’? This demonstrates the price-distorting ability of central banks. In order to limit extreme price fluctuations and crashes, the better central banks can do is to disappear from the marketplace entirely.

*Other practical restrictions on guidance include the fact that, while professional investors are likely to be aware of their significance, the rest of the population has no idea what the hell you’re talking about, if it has even heard of it. As a result, the efforts the BoE made to reassure UK borrowers that rates would not rise in the short-run seemed pointless, as virtually no average Joe got it, implying that most people didn’t change their borrowing behaviour/plan in consequence.

I have made a case for rule-based policies a while ago, which I do believe would limit distortions to an extent.

The Great Depression and the money multiplier

The money multiplier has collapsed following the introduction of new reserves as central banks engaged in quantitative easing. This has led many economic commentators to declare that the money multiplier did not exist.

While I have several times said that this wasn’t that straightforward, I stumbled upon a post by Mark Sadowski, on Marcus Nunes’ blog, which includes a very interesting graph of the M2 money multiplier (blue line below) from 1925 to 1970 (I have no idea how he obtained this dataset as I can’t seem to be able to go further back than 1959 on the FRED website).

The multiplier collapsed from 7 in 1930 to a low 2.5 in 1940 and banks that had not disappeared had plenty of excess reserves, which they maintained for a number of reasons (precautionary, lack of demand for lending, low interest rates, Hoover/FDR policies…). This situation looks very similar to what happened during our recent crisis. However, what’s interesting is that the multiplier did eventually increase. In 1970, 30 years after reaching the bottom, the multiplier was back at around 6, meaning a large increase in the money stock. This is what most people miss: it doesn’t just take a few years for new reserves to affect lending; it can take decades.

Unless the Fed takes specific actions to remove (or prevent the use of) current excess reserves, the money multiplier could well get back to its historical level within the next few decades.

Hummel vs. Haldane: the central bank as central planner

Recent speeches and articles from most central bankers are increasingly leaving a bad aftertaste. Take this latest article by Andrew Haldane, Executive Director at the BoE, published in Central Banking. Haldane describes (not entirely accurately…) the history and evolution of central banking since the 19th century and discusses two possible paths for the next 25 years.

His first scenario is that central banks and regulation will step backward and get back to their former, ‘business as usual’, stance, focusing on targeting inflation and leaving most of the capital allocation work to financial markets. He views this scenario as unlikely. He believes that the central banks will more tightly regulate and intervene in all types of asset markets (my emphasis):

In this world, it would be very difficult for monetary, regulatory and operational policy to beat an orderly retreat. It is likely that regulatory policy would need to be in a constant state of alert for risks emerging in the financial shadows, which could trip up regulators and the financial system. In other words, regulatory fine-tuning could become the rule, not the exception.

In this world, macro-prudential policy to lean against the financial cycle could become more, not less, important over time. With more risk residing on non-bank balance sheets that are marked-to-market, it is possible that cycles in financial assets would be amplified, not dampened, relative to the old world. Their transmission to the wider economy may also be more potent and frequent. The demands on macro-prudential policy, to stabilise these financial fluctuations and hence the macro-economy, could thereby grow.

In this world, central banks’ operational policies would be likely to remain expansive. Non-bank counterparties would grow in importance, not shrink. So too, potentially, would more exotic forms of collateral taken in central banks’ operations. Market-making, in a wider class of financial instruments, could become a more standard part of the central bank toolkit, to mitigate the effects of temporary market illiquidity droughts in the non-bank sector.

In this world, central banks’ words and actions would be unlikely to diminish in importance. Their role in shaping the fortunes of financial markets and financial firms more likely would rise. Central banks’ every word would remain forensically scrutinised. And there would be an accompanying demand for ever-greater amounts of central bank transparency. Central banks would rarely be far from the front pages.

He acknowledged that central banks’ actions have already considerably influenced (distorted?…) financial markets over the past few years, though he views it as a relatively good thing (my emphasis):

With monetary, regulatory and operational policies all working in overdrive, central banks have had plenty of explaining to do. During the crisis, their actions have shaped the behaviour of pretty much every financial market and institution on the planet. So central banks’ words resonate as never previously. Rarely a day passes without a forensic media and market dissection of some central bank comment. […]

Where does this leave central banks today? We are not in Kansas any more. On monetary policy, we have gone from setting short safe rates to shaping rates of return on longer-term and wider classes of assets. On regulation, central banks have gone from spectator to player, with some granted micro-prudential as well as macro-prudential regulatory responsibilities. On operational matters, central banks have gone from market-watcher to market-shaper and market-maker across a broad class of assets and counterparties. On transparency, we have gone from blushing introvert to blooming extrovert. In short, central banks are essentially unrecognisable from a quarter of a century ago.

This makes me feel slightly unconfortable and instantly remind me of the – now classic – 2010 article by Jeff Hummel: Ben Bernanke vs. Milton Friedman: The Federal Reserve’s Emergence as the U.S. Economy’s Central Planner. While I believe there are a few inaccuracies and omissions in Hummel’s description of the financial crisis, his article is really good and his conclusion even more valid today than at the time of his writing:

In the final analysis, central banking has become the new central planning. Under the old central planning—which performed so poorly in the Soviet Union, Communist China, and other command economies—the government attempted to manage production and the supply of goods and services. Under the new central planning, the Fed attempts to manage the financial system as well as the supply and allocation of credit. Contrast present-day attitudes with the Keynesian dark ages of the 1950s and 1960s, when almost no one paid much attention to the Fed, whose activities were fairly limited by today’s standard. […]

As the prolonged and incomplete recovery from the recent recession suggests, however, the Fed’s new central planning, like the old central planning, will ultimately prove an unfortunate and possibly disastrous failure.

The contrast between central bankers’ (including Haldane’s) beliefs of a tightly controlled financial sector to those of Hummel couldn’t be starker.

Where it indeed becomes really worrying is that Hummel was only referring to Bernanke’s decision to allocate credit and liquidity facilities to some particular institutions, as well as to the multiplicity of interest rates and tools implemented within the usual central banking framework. At the time of his writing, macro-prudential policies were not as discussed as they are now. Nevertheless, they considerably amplify the central banks’ central planner role: thanks to them, central bankers can decide to reduce or increase the allocation of loanable funds to one particular sector of the economy to correct what they view as financial imbalances.

Moreover, central banks are also increasingly taking over the role of banking regulator. In the UK, for instance, the two new regulatory agencies (FCA and PRA) are now departments of the Bank of England. Consequently, central banks are in charge of monetary policy (through an increasing number of tools), macro-prudential regulation, micro-prudential regulation, and financial conduct and competition. Absolutely all aspects of banking will be defined and shaped at the central bank level. Central banks can decide to ‘increase’ competition in the banking sector as well as favour or bail-out targeted firms. And it doesn’t stop here. Tighter regulatory oversight is also now being considered for insurance firms, investment managers, various shadow banking entities and… crowdfunding and peer-to-peer lending.

Hummel was right: there are strong similarities between today’s financial sector planning and post-WW2 economic planning. It remains to be seen how everything will unravel. Given that history seems to point to exogenous origins of financial imbalances (whereas central bankers, on the other hand, believe in endogenous explanations, motivating their policies), this might not end well… Perhaps this is the only solution though: once the whole financial system is under the tight grip of some supposedly-effective central planner, the blame for the next financial crisis cannot fall on laissez-faire…

Financial instability: Beckworth and output gap

I recently mentioned David Beckworth’s excellent new paper on inflation targeting, which, according to him, promotes financial instability by inadequately responding to supply shocks. Like free bankers and some other economists, Beckworth understands the effects of productivity growth on prices and the distorting economic effects of inflation targeting in a period of productivity improvements.

Nevertheless, I am a left a little surprised by a few of his claims (on his blog), some of which seem to be in contradiction with his paper: according to him, current US output gap demonstrates that the nominal natural rate of interest has been negative for a while. Consequently, the current Fed rate isn’t too low and raising it would be premature.

While I believe that the real natural interest rate (in terms of money) is very unlikely to ever be negative (though some dispute this), it is theoretically and empirically unclear whether or not the nominal natural rate could fall in negative territory, especially for such a long time.

Beckworth uses a measure of US output gap calculated by the CBO and derived from their potential GDP estimate. This is where I become very sceptical. GDP itself is already subject to calculation errors and multiple revisions. Furthermore, there are so many variables and methodologies involved in calculating ‘potential’ GDP, that any output gap estimate takes the risk of being meaningless due to extreme inaccuracy, if not completely flawed or misleading.

This is the US potential GDP, as estimated by the CBO:

Wait a minute. For most of the economic bubble of the 2000s, the US was below potential? This estimate seems to believe that credit-fuelled pre-crisis years were merely in line with ‘potential’. This is hardly believable, and this reminds me of the justification used by many Keynesian economists: we should have used more fiscal stimulus as we are below ‘trend’ (‘trend’ being calculated from 2007 of course, as if the bubble years had never happened). Does this also mean that the natural rate of interest has been negative or close to zero since 2001? This seems to contradict Beckworth’s own inflation targeting article, in which he says that the Fed rate was likely too low during the period.

Let’s have a look at a few examples of the wide range of potential GDP estimates (and hence output gap) that are available out there*. The Economic Report of the President estimates potential GDP as even higher than the CBO’s (source: Morgan Stanley):

The Fed of San Francisco, on the other hand, estimated very different output gap variations. According to some measures, the US is currently… above potential:

Some of the methodologies used to calculate some of those estimates might well be inaccurate, or simply wrong. Still, this clearly shows how hard it is to determine potential GDP and thus the output gap. Any conclusion or recommendation based on such dataset seems to me to reflect conjectures more than evidences.

This is where we get to my point.

In his very good article, Beckworth brilliantly declares that:

the productivity gains will also create deflationary pressures that an inflation-targeting central bank will try to offset. To do that, the central bank will have to lower its target interest rate even though the natural interest rate is going up. Monetary authorities, therefore, will be pushing short-term interest rates below the stable, market-clearing level. To the extent this interest rate gap is expected to persist, long-term interest rates will also be pushed below their natural rate level. These developments mean firms will see an inordinately low cost of capital, investors will see great arbitrage opportunities, and households will be incentivized to take on more debt. This opens the door for unwarranted capital accumulation, excessive reaching for yield, too much leverage, soaring asset prices, and ultimately a buildup of financial imbalances. By trying to promote price stability, then, the central bank will be fostering financial instability.

Please see the bold part (my emphasis): isn’t it what we are currently experiencing? It looks to me that the current state of financial markets exactly reflects Beckworth’s description of a situation in which the central bank rate is below the natural rate. This is also what the BIS warned against, explicitely rejected by Beckworth on the basis of this CBO output gap estimate. (see also this recent FT report on bubbles forming in credit markets)

I am asking here how much trust we should place in some potentially very inaccurate estimates.

Perhaps the risk-aversion suppression and search for yield of the system is not apparent to everyone, including Beckworth, not helping him diagnose our current excesses. But, his ‘indicators that don’t show asset price froth’ are arguable: the risk premium between Baa-rated yields and Treasuries are ‘elevated’ due to QE pushing yields on Treasuries lower, and it doesn’t mean much that households still hold more liquid assets than in the financial boom years of 1990-2007.

At the end of the day, we should perhaps start relying on actual** – rather than estimated and potentially flawed – indicators for policy-making purposes (that is, as long as discretion is in place). Had US GDP been considered as above potential in the pre-crisis years and the Fed stance adapted as a result, the impact of the financial crisis might have been far less devastating. I agree with Beckworth: time to end inflation targeting.

* The IMF estimate also shows that the US was merely in line with potential as of 2007. Others are more ‘realistic’ but as the charts below demonstrate, estimates vary widely, along with confidence intervals (link, as well as this full report for tons of other output gap charts from the same authors):

** I understand and agree that ‘actual’ market and economic data can also be subject to interpretation. I believe, however, that the range of interpretations is narrower: these datasets represents more ‘crude’ or ‘hard’ data that haven’t been digested through multiple, potentially biased, statistical computations.

Lars Christensen on Yellen and bubbles, and UK regulators at full speed

Lars Christensen published a sarcastic post on his blog, which coincidentally treats the monetary policy and bubbles problem as the same time as my previous post. I fully agree with him that Yellen’s comments are ridiculous.

This is Lars:

it seems to part of a growing tendency among central bankers globally to be obsessing about “financial stability” and “bubbles”, while at the same time increasingly pushing their primary nominal targets in the background.

While I agree with Lars that central banks should provide ‘nominal stability’, I don’t think inflation targeting provides such framework (and I believe Lars agrees). Inflation is very hard to measure, let alone to define, and can be very misleading (Scott Sumner believes that inflation indicators are meaningless). According to a Wicksellian framework, it does look like something’s wrong with interest rates at the moment. Banking regulation, due to its roles in ‘channelling’ interest rates, surely also plays a big role that monetary policy cannot influence. In the end, maintaining inflation right on target is in no way insurance of actual nominal (and financial) stability.

David Beckworth, in a new paper published a few days ago, also criticised inflation targeting on the ground that it contributes to financial instability. I agree with Market Monetarists that a policy stabilising NGDP growth would provide a more robust economy and financial system, though it is in my view still imperfect (I’ll come back to that in another post).

Totally unrelated: in the UK, regulators are working at full speed. Here is a summary of some of the latest regulatory announcements:

- Regulators believe that asset managers ‘waste’ too much client money on sell-side analysts research and want to regulate the process, risking to transform the market into an oligopoly as smaller research providers may not be able to cope with the reduced fee-generation (see here and here)

- HMRC wants to get the power to access your bank account and check your spending habits without going through court to make sure that you are able to pay the taxes they claim you owe them (even if they are wrong). I have personally dealt many times with HMRC (I didn’t owe them money, they did) and the least I can say is that it wasn’t necessarily a pleasant experience: waiting 45min on the phone to end up speaking to someone who sounds very suspicious that you are trying to trick tax authorities… (to be fair, I also ended up speaking to competent and pleasant people) HMRC makes mistakes all the time and I would be very cautious in granting them such powers… (see here and here)

- New rules capping the fees payday lenders can charge are effectively about to kill a large number of them… It probably won’t help much (see here)

- Bank account holders aren’t taking advantage of the best offers available to them and don’t spend their time constantly changing bank to get the best pricing and as a result earn poor returns? The regulator also wants to change that, though I submit that it should tell his boss (the BoE) that, if savers indeed earn poor returns, it possibly is because rates aren’t very high… (see here)

- The BoE and PRA want global banking regulators to reduce RWAs or capital requirements for small banks. Not saying this is a bad thing, but this sounds kind of contradictory to me, given everything we’ve been hearing for years from the same regulators… (see here)

New research on banking

New York Fed researchers published new papers on banking over the past few months on the Fed’s blog Liberty Street Economics.

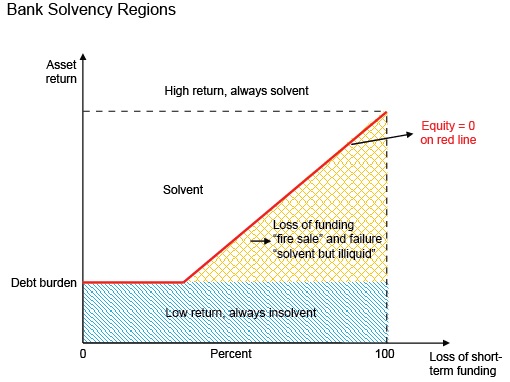

The first one, titled Stability of Funding Models: an Analytical Framework, is summarised through two different blog posts (here and here). The researchers present a banking model that graphically illustrates the factors that influence the risk of a bank becoming insolvent or illiquid (namely: low asset returns, high leverage, loss of funding (short-term debt maturity profile), asset encumbrance…).

Nothing ground breaking. The model simply graphically represents what all banks’ analysts already know. But the principle is interesting. They also published an interactive model you can play with to simulate your own bank (here). I think the internal microeconomic impacts of the firm are also downplayed here: cost efficiency also plays a crucial role, ceteris paribus. Two banks’ asset returns (and in turn revenues), funding profile (and in turn net interest margin) and leverage could be the same, but the bank with the higher cost/income will have a lot less financial flexibility to absorb the exact same asset impairments when they arise and as a result presents a higher risk of insolvency.

The second piece of research, titled Do “Too-Big-to-Fail” Banks Take On More Risk? (see related blog post here), aims at analysing the influence of being classified as ‘systemically important’ on risk-taking. The report concludes that:

The results of our investigation show that a greater likelihood of government support leads to a rise in bank risk-taking. Following an increase in government support, we see a larger volume of bank lending becoming impaired. Further, and in line with this finding, our results show that stronger government support translates into an increase in net charge-offs. Additionally, we find that the effect of government support on impaired loans is stronger for riskier banks than safer ones, as measured by their issuer default ratings. Our findings offer novel evidence that government support does play a role in bank risk-taking incentives.

Fed researchers decided to use the rating agency Fitch’s Support Rating Floor as an indication of sovereign support, as most other rating agencies do not distinguish between institutional/parental and sovereign supports in their rating uplift. This is Fitch’s methodology, which you can find in their financial institutions rating criteria here (gated but free registration):

Nothing very surprising here either, but this research adds to the increasingly large literature that underlines the benefits (and the risks) of being a large (and possibly government-linked) bank. Artificially cheaper funding and riskier behaviour pushes the banking system away from its equilibrium state, which is supposed to reflect savers’ intertemporal preferences. This, combined with inaccurate central bank monetary policy and regulatory-distorted interest rates, is a definitive recipe for the misallocation of capital on a massive scale. No surprise financial and economic crises are so recurrent.

Finally, other Fed employees developed yet another liquidity measure, the liquidity stress ratio. I’m not sure about its usefulness to be honest as well as some of the conclusions that the authors draw from some of the spurious correlations they calculate. Take the following chart for example:

From this, the authors conclude:

The positive relationship [between capitalisation and liquidity stress ratio] may indicate that when banks are less vulnerable to undercapitalization, they take more liquidity risk. In other words, capital and liquidity may act as substitutes.

Really? Take the red line off the chart above and you end up with no clear pattern at all. Some banks play it safe; some others are willing to take on more risk; some are in between. This seems to me to be a clear case of mathematical regression interpretation abuse.

On another platform, Vox, a group of economists have come up with an interesting experiment. They found that

Economic linkages between banks give rise to contagion of deposit withdrawals across banks, especially when depositors are aware of these economic linkages. Systemic risk due to the contagion of panic-based deposit withdrawals is thus likely to be more acute for banking systems characterised by clusters of domestic banks which share the same business model (e.g. cajas in Spain or Sparkassen/Volksbanken in Germany).

This is very interesting. However, their recommendation is way off:

For regulators this accentuates the question of how to monitor and regulate economic linkages between banks stemming from similar exposures, in order to mitigate financial fragility and to encourage greater diversity in the financial system.

Are they aware that regulators have been doing the exact opposite of their recommendation for many, many years? Regulations have been trying to harmonise business models since the 1980s, when Basel regulations were first implemented. Moreover, regulators now try to influence banks’ internal organisation and structure to comply with what they see as adequate. The result of all those policies is an increasing lack of diversification between banks. You want more diversity in the financial system? Then tell regulators to back away.

PS: Martin Wolf had a piece in the FT this week in which he came on favour of… 100% reserve banking. That’s right. That was a little bit of a surprise to say the least. Izabella Kaminska discussed it here, though she seems again to get mixed up between various terms and definitions, and Frances Coppola had a good article criticising Wolf’s idea (though I don’t entirely agree with everything she says).

Greenspan put, Draghi call? (guest post by Vaidas Urba)

(This is a monetary economics guest post by Vaidas Urba, a market monetarist from Lithuania. He has previously appeared at The Insecurity Analyst blog and TheMoneyIllusion. You can follow him on Twitter here)

Greenspan put, Bernanke put – everybody uses these expressions half-jokingly to describe monetary policy and asset prices. Ricardo Caballero and Emmanuel Farhi have proposed a very serious classification of policy tools, distinguishing between monetary puts and calls. According to Caballero and Farhi, policy puts support the economy in bad states of the world, while policy calls support the economy in good states of world. There is much to disagree with in their “Safety Traps and Economic Policy” paper, but their definition of policy puts and calls is very useful.

QE1 and ARRA stimulus in 2009 are examples of policy puts. On the other hand, QE3 and Evans rule are primarily policy calls. Evans rule supported expectations of low interest rates in good states of the world, while QE3 compressed the term premium by reducing the risk of bond market volatility during the recovery. Policy calls are riskier than policy puts. Evan’s rule increased the risk of suboptimally low interest rates during late stages of recovery, while QE3 increased the risk of losses in Fed’s portfolio. Indeed, on March 1, 2013 Bernanke indicated that the estimated treasury term premium is negative. The Fed has walked back from policy calls. Tapering has restored the bond term premium to more normal levels, and the Fed has replaced the Evans rule with a more vague guidance. Bernanke call was replaced by Yellen put.

The Fed has used both monetary puts and calls, but the ECB has never used policy calls, and is not planning to use them. The policy of the ECB was a succession of impressive policy puts. Temporary liquidity injection in August 2007 has addressed the liquidity panic. Full allotment in October 2008 has placed a floor on the functioning of euro and dollar money markets. Three year LTROs in 2011 have prevented Greece’s default from becoming Lehman II. OMTs are out-of the money policy puts – they were never activated. Forward guidance is a policy put too, the ECB describes it as being all about “subdued outlook for inflation and broad-based weakness of the economy”, and low rates are signalled in bad states of the world without affecting interest rate expectations in good states of the world.

On further weakness the ECB is likely to start QE. Executive Board member Benoit Coeure has recently given us a glimpse of likely modalities of QE in his “Asset purchases as an instrument of monetary policy” speech. Coeure has stressed the continuity of ECB’s approach, he also said that “asset purchases in the euro area would not be about quantity, but about price”, and the ECB will use the yardstick of “the observable effect of our operations on term premia”. Presumably, the intent of QE will be to reduce term premia that are unduly high (policy put), and not to recreate boom conditions in financial markets by driving term premia to excessively low levels (policy call).

The Eurozone economy is very far away from any sensible macro equilibrium, and monetary call would be a very sensible step to take. Unfortunately, a blocking minority exists for any explicit decision. However, Draghi could communicate an implicit policy call by signalling the existence of majority coalition which would block a premature interest rate increase. The rate hike of 2011 was unanimous, so the bar is high for any such communication. Draghi’s talk of “plenty of slack” is a step to the right direction, but stronger and clearer words are needed to persuade the markets that ECB’s reaction function has changed unrecognizably since 2011.

A central banker contradiction?

Last week, Mark Carney, the governor of the Bank of England, was at Cass Business School in London for the annual ‘Mais Lecture’. Coincidentally, I am an alumnus of this school. And I forgot to attend… Yes, I regret it.

Carney’s speech was focused on past, current, and future roles of the BoE. In particular, Carney mentioned the now famous monetary and macroprudential policies combination. It’s a classic for central bankers nowadays. They all have to talk about that.

In January, Andrew Haldane, a very wise guy and one my ‘favourite’ regulators, also from the BoE, made a whole speech about the topic. As Jens Weidmann, president of the Bundesbank, did in February.

I am not going to come back to the all the various possible problems caused and faced by macroprudential policies (see here and here). However, there seems to be a recurrent contradiction in their reasoning.

This is Carney:

The transmission channels of monetary and prudential policy overlap, particularly in their impact on banks’ balance sheets and credit supply and demand – and hence the wider economy. Monetary policy affects the resilience of the financial system, and macroprudential policy tools that affect leverage influence credit growth and the wider economy. […]

The use of macroprudential tools can decrease the need for monetary policy to be diverted from managing the business cycle towards managing the credit cycle. […]

That co-ordination, the shared monitoring of risks, and clarity over the FPC’s tools allows monetary policy to keep Bank Rate as low as necessary for as long as appropriate in order to support the recovery and maintain price stability. For example expectations of the future path of interest rates – and hence longer-term borrowing costs – have not risen as the housing market has begun to recover quickly.

First, it is very unclear from Carney’s speech what the respective roles of monetary policy and macroprudential policies are. He starts by saying (above) that “monetary policy affects the resilience of the financial system”, then later declares “macroprudential policy seeks to reduce systemic risks”, which is effectively the same thing. At least, he is right: both policy frameworks overlap. And this is the problem.

This is Haldane:

In the UK, the Bank of England’s Monetary Policy Committee (MPC) has been pursuing a policy of extra-ordinary monetary accommodation. Recently, there have been signs of renewed risk-taking in some asset markets, including the housing market. The MPC’s macro-prudential sister committee, the Financial Policy Committee (FPC), has been tasked with countering these risks. Through this dual committee structure, the joint needs of the economy and financial system are hopefully being satisfied.

Some have suggested that having monetary and macro-prudential policy act in opposite directions – one loose, the other tight – somehow puts the two in conflict [De Paoli and Paustian, 2013]. That is odd. The right mix of monetary and macro-prudential measures depends on the state of the economy and the financial system. In the current environment in many advanced economies – sluggish growth but advancing risk-taking – it seems like precisely the right mix. And, of course, it is a mix that is only possible if policy is ambidextrous.

Contrary to Haldane, this does absolutely not look odd to me…

Let’s imagine that the central bank wishes to maintain interest rates at a low level in order to boost economic activity after a crisis. After a little while, some asset markets start looking ‘frothy’ or, as Haldane says, there are “renewed signs of risk-taking.” Discretionary macroprudential policy (such as increased capital requirements) is therefore utilised to counteract the lending growth that drives those asset markets. But there is an inherent contradiction here: one of the goals that low interest rates try to achieve is to boost lending growth to stimulate the economy…whereas macroprudential policy aims at…reducing it. Another contradiction: while low interest rates tries to prevent deflation from occurring by promoting lending and thus money supply growth, macroprudential policy attempts to reduce lending, with evident adverse effects on money supply and inflation…

Central bankers remain very evasive about how to reconcile such goals without entirely micromanaging the banking system.

I guess that the growing power of central bankers and regulators means that, at some point, each bank will have an in-house central bank representative that tells the bank who to lend to. For social benefits of course. All very reminiscent of some regions of the world during the 20th century…

Weidman is slightly more realistic:

We have to acknowledge that in the world we live in, macroprudential policy can never be perfectly effective – for instance because safeguarding financial stability is complicated by having to achieve multiple targets all at the same time.

Indeed.

Photograph: Intermonk

Bundesbank’s Dombret has strange free market principles

Andreas Dombret, member of the executive board of the Bundesbank, made two very similar speeches last week (The State as a Banker? and Striving to achieve stability – regulations and markets in the light of the crisis). When I started to read them, I was delighted. Take a look:

If one were to ask the question whether or not the market economy merits our trust, another question has to be added immediately: “Does the state merit our trust?”

[…]

Sometimes it seems as if we are witnessing a transformation of values and a redefinition of fundamental concepts. The close connection between risk-taking and liability, which is an important element of a market economy, has weakened.

Conservative and risk-averse business models have become somewhat old-fashioned. If the state is bearing a significant part of the losses in the case of a default of a bank, banks are encouraged to take on more risks.

[…]

[High bonuses and short-termism] are the result of violated market principles and blurred lines between the state and the banks. They are not the result of a well-designed market economy but rather indicative of deformed economies. However, the market economy stands accused of these faults.

Brilliant. I was just about to become a Dombret fan when…I read the rest:

In my view, the solution is to be found in returning the state to its role of providing a framework in which the private sector can operate. This means a return to the role the founding fathers of the social market economy had in mind.

They knew that good banking regulation is a key element of a well-designed framework for a well-functioning banking industry and a proper market economy in general.

[…]

This is where good bank capitalisation comes into play. It is the other side of the coin. Good regulation should directly address the key problem. If the system is too fragile, an important and direct measure to reduce fragility is to have enough capital.

[…]

Good capitalisation will have the positive side effect of reducing many of the wrong incentives and distortions created by taxpayers’ implicit guarantees and therefore making the bail-in threat more credible ex ante.

And from the second article:

In view of all this, I believe that two elements will be especially important in making banks more stable: capital and liquidity. Deficits in both of these things were factors which contributed significantly to the financial crisis. The state can bring in regulation to address these deficits, and has done so very successfully.

And on shadow banking:

In terms of financial stability, the crux of the matter is that these entities can cause similar risks to banks but are not subject to bank regulation.And the shadow banking system can certainly generate systemic risks which pose a threat to the entire financial system.

Much the same applies to insurance companies. Although they aren’t a direct component of the shadow banking system, they can also be a source of systemic risk. All of this makes it appropriate to extend the reach of regulation.

Sorry but I will postpone joining the fan club…

Mr. Dombret correctly identifies the issue with the financial system: too much state involvement. What is his solution? More state involvement. It is hard to believe that one person could come up with the exact same solution that had not worked in the past. Were the banks not already subject to capital requirements before the crisis? Even if not ‘high’ enough they were still higher than no capital requirement at all. So in theory they should have at least mitigated the crisis. But the crisis was the worst one since 1929, and much worse than previous ones during which there were no capital requirements. Efficient regulation indeed…

Like 95% of regulators, he makes such mistakes because of his (voluntary?) ignorance of banking history. A quick look at a few books or papers such as this one, comparing US and Canadian banking systems historically, would have shown him that Canadian banks were more leveraged than US banks on average since the early 19th century, yet experienced a lot fewer bank failures. There is clearly so much more at play than capital buffers in banking crises…

Moreover, he views formerly ‘low’ capital requirements as a justification for bankers to take on more risks to generate high return on equity. This doesn’t make sense. For one thing, the higher the capital requirements the higher the risks that need to be taken on to generate the same RoE. It also encourages gaming the rules. This is what is currently happening, as banks are magically managing to reduce their risk-weighted assets so that their regulatory-defined capital ratios look healthier without having to increase their capital.

Mr. Dombret starts by seriously questioning the state’s ability to manage the system and highlights the very harmful and distortive effects of state regulation to eventually… back further and deeper state regulation.

A question Mr. Dombret: what are we going to do following the next crisis? Continue down the same road?

Can please someone remind Mr. Dombret of what a free market economy, which he seems to cherish, means?

Picture: Marius Becker

Recent Comments