Continuously ignoring and misinterpreting history

This recent speech by the Vice President of the ECB, Vítor Constâncio, is in my opinion one of the foremost examples of how a partial reading or misinterpretation of history that becomes accepted as mainstream can lead to bad policy-making.

This speech is typical. Constâncio argues that

the build-up of systemic risk over the financial cycle is an endogenous outcome – a man-made construct – and the job of macro-prudential policy is to try to smoothen this cycle as much as possible. […]

The […] most important source of systemic risk is the risk of the unravelling of financial imbalances. These imbalances may build up gradually, mostly endogenously, and can then unravel abruptly. They form part of the inherent pro-cyclicality of the financial system.

It is crucial to recognise that the financial cycle has an important endogenous component which arises because banks take too much solvency and liquidity risk. The aim of macro-prudential policy should be to temper the financial cycle rather than to merely enhance the resilience of the financial sector ahead of crises.

While Constâncio is right that there is some truth in the pro-cyclicality of financial systems as a long economic boom impairs risk perception, risk assessment and risk premiums, he never highlights why such booms and busts occur in the first place. Outside of negative supply shocks, are they a ‘natural’ consequence of the activity of the economic system? Or are they exogenously triggered by bad government or monetary policies?

Several economic schools of thought have different explanations and theories. Yet, there is one thing that cannot be denied: historical experiences of financial stability.

This is where the flaw of Constâncio’s (and of most central bankers’ and mainstream economists’) thinking resides: history proves that, when the banking sector is left to itself, systemic endogenous accumulation of financial imbalances is minimal, if not non-existent…

According to Larry White in a recent article summing up the history of thought and historical occurrences of free banking, Kurt Schuler identified sixty banking episodes to some extent akin to free banking. White’s paper describes 11 of them, many of which had very few institutional and regulatory restrictions on banking. He quotes Kevin Dowd:

As Kevin Dowd fairly summarizes the record of these historical free banking systems, “most if not all can be considered as reasonably successful, sometimes quite remarkably so.” In particular, he notes that they “were not prone to inflation,” did not show signs of natural monopoly, and boosted economic growth by delivering efficiency in payment practices and in intermediation between savers and borrowers. Those systems of plural note-issue that were panic-prone, like the pre-1913 United States and pre-1832 England, were not so because of competition but because of legal restrictions that significantly weakened banks.

Yet, there is no trace of such events in conventional/mainstream financial history. Central bankers seem to be completely oblivious to those facts (this is surely self-serving) and economists only partially aware of the causes of financial crises. Moreover, free banking episodes also proved that banks were not inherently prone to take “too much solvency and liquidity risk”: indeed, historical records show that banks in such periods were actually well capitalised and rarely suffered liquidity crises. In short, laissez-faire banking’s robustness was far superior to our overly-designed ones’. Consequently we keep making the same mistakes over and over again in believing that a crisis occurred because the previous round of regulation was inadequate…

What we end up with is a banking system shaped by layers and layers of regulations and central banks’ policies. Every financial product, every financial activity, was awarded its own regulation as well as multiple ‘corrective’ rules and patches, was influenced by regulators’ ‘recommendations’, was limited by macro-prudential tools and manipulated through various interest rates under the control by a small central authority. On top of such regulatory intervention, short-term political interference compounds the problem by purposely designing and adjusting financial systems for short-term electoral gains. Markets are distorted in all possible ways as the price system ceases to work adequately, defeating their capital allocation purposes and creating bubbles after bubbles.

Studying banking and financial history demonstrates that it is quite ludicrous to pretend that banking systems are inherently subject to failure through endogenous accumulation of risk. In the quest for an explanation of the crisis, better look at the intersection of moral hazard, political incentives, and the regulatory-originated risk opacity. It might turn out that imbalances are, well, mostly… exogenous.

Please let finance organise itself spontaneously.

Photo: José Carlos Pratas

Financial instability: Beckworth and output gap

I recently mentioned David Beckworth’s excellent new paper on inflation targeting, which, according to him, promotes financial instability by inadequately responding to supply shocks. Like free bankers and some other economists, Beckworth understands the effects of productivity growth on prices and the distorting economic effects of inflation targeting in a period of productivity improvements.

Nevertheless, I am a left a little surprised by a few of his claims (on his blog), some of which seem to be in contradiction with his paper: according to him, current US output gap demonstrates that the nominal natural rate of interest has been negative for a while. Consequently, the current Fed rate isn’t too low and raising it would be premature.

While I believe that the real natural interest rate (in terms of money) is very unlikely to ever be negative (though some dispute this), it is theoretically and empirically unclear whether or not the nominal natural rate could fall in negative territory, especially for such a long time.

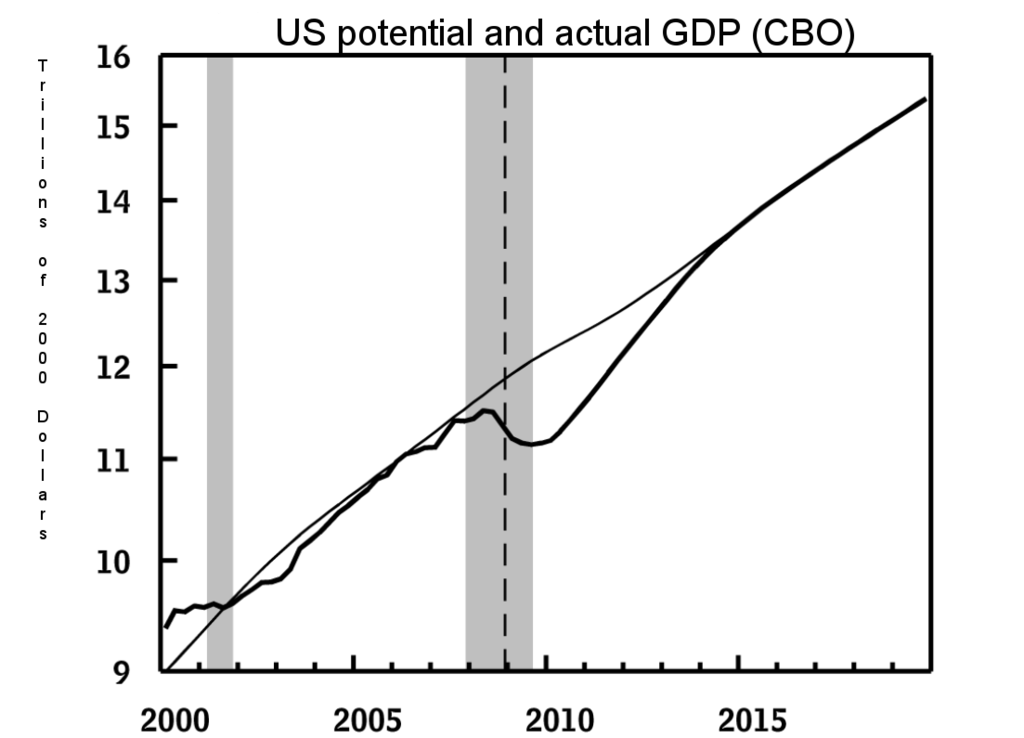

Beckworth uses a measure of US output gap calculated by the CBO and derived from their potential GDP estimate. This is where I become very sceptical. GDP itself is already subject to calculation errors and multiple revisions. Furthermore, there are so many variables and methodologies involved in calculating ‘potential’ GDP, that any output gap estimate takes the risk of being meaningless due to extreme inaccuracy, if not completely flawed or misleading.

This is the US potential GDP, as estimated by the CBO:

Wait a minute. For most of the economic bubble of the 2000s, the US was below potential? This estimate seems to believe that credit-fuelled pre-crisis years were merely in line with ‘potential’. This is hardly believable, and this reminds me of the justification used by many Keynesian economists: we should have used more fiscal stimulus as we are below ‘trend’ (‘trend’ being calculated from 2007 of course, as if the bubble years had never happened). Does this also mean that the natural rate of interest has been negative or close to zero since 2001? This seems to contradict Beckworth’s own inflation targeting article, in which he says that the Fed rate was likely too low during the period.

Let’s have a look at a few examples of the wide range of potential GDP estimates (and hence output gap) that are available out there*. The Economic Report of the President estimates potential GDP as even higher than the CBO’s (source: Morgan Stanley):

The Fed of San Francisco, on the other hand, estimated very different output gap variations. According to some measures, the US is currently… above potential:

Some of the methodologies used to calculate some of those estimates might well be inaccurate, or simply wrong. Still, this clearly shows how hard it is to determine potential GDP and thus the output gap. Any conclusion or recommendation based on such dataset seems to me to reflect conjectures more than evidences.

This is where we get to my point.

In his very good article, Beckworth brilliantly declares that:

the productivity gains will also create deflationary pressures that an inflation-targeting central bank will try to offset. To do that, the central bank will have to lower its target interest rate even though the natural interest rate is going up. Monetary authorities, therefore, will be pushing short-term interest rates below the stable, market-clearing level. To the extent this interest rate gap is expected to persist, long-term interest rates will also be pushed below their natural rate level. These developments mean firms will see an inordinately low cost of capital, investors will see great arbitrage opportunities, and households will be incentivized to take on more debt. This opens the door for unwarranted capital accumulation, excessive reaching for yield, too much leverage, soaring asset prices, and ultimately a buildup of financial imbalances. By trying to promote price stability, then, the central bank will be fostering financial instability.

Please see the bold part (my emphasis): isn’t it what we are currently experiencing? It looks to me that the current state of financial markets exactly reflects Beckworth’s description of a situation in which the central bank rate is below the natural rate. This is also what the BIS warned against, explicitely rejected by Beckworth on the basis of this CBO output gap estimate. (see also this recent FT report on bubbles forming in credit markets)

I am asking here how much trust we should place in some potentially very inaccurate estimates.

Perhaps the risk-aversion suppression and search for yield of the system is not apparent to everyone, including Beckworth, not helping him diagnose our current excesses. But, his ‘indicators that don’t show asset price froth’ are arguable: the risk premium between Baa-rated yields and Treasuries are ‘elevated’ due to QE pushing yields on Treasuries lower, and it doesn’t mean much that households still hold more liquid assets than in the financial boom years of 1990-2007.

At the end of the day, we should perhaps start relying on actual** – rather than estimated and potentially flawed – indicators for policy-making purposes (that is, as long as discretion is in place). Had US GDP been considered as above potential in the pre-crisis years and the Fed stance adapted as a result, the impact of the financial crisis might have been far less devastating. I agree with Beckworth: time to end inflation targeting.

* The IMF estimate also shows that the US was merely in line with potential as of 2007. Others are more ‘realistic’ but as the charts below demonstrate, estimates vary widely, along with confidence intervals (link, as well as this full report for tons of other output gap charts from the same authors):

** I understand and agree that ‘actual’ market and economic data can also be subject to interpretation. I believe, however, that the range of interpretations is narrower: these datasets represents more ‘crude’ or ‘hard’ data that haven’t been digested through multiple, potentially biased, statistical computations.

What’s wrong with Bloomberg?

Bloomberg was created to report financial and economic events to financiers. Yet it seems that it has drawn the wrong conclusions from the crisis and fallen into the interventionist trap. Repeating usual basic statist/interventionist misconceptions isn’t what we expect from such a respectable company. The editorial line of the Financial Times or The Economist seems to be much more balanced in comparison, even if I don’t agree with everything they say.

Last week, Bloomberg reported that:

Four years after President Barack Obama signed the Dodd-Frank Wall Street Reform and Consumer Protection Act into law, polling suggests that most Americans think it hasn’t done enough to protect them from a repeat of the 2008 financial crisis, a disaster from which the global economy has yet to fully recover.

Unfortunately, they’re right.

According to Bloomberg, Dodd-Frank is the ultimate tool that regulators need to make the system ‘safe’:

Dodd-Frank provides regulators with all the powers they need to prevent the financial sector from leaning on taxpayers and putting the economy in danger. All that’s wanting, four years on, is the will to use them.

This goes against all evidences so far. Dodd-Frank has many issues (too many links to provide… I let you google it). Just don’t tell Bloomberg.

Today, Bloomberg announced its support of tighter regulatory oversight for insurers and… Berkshire Hathaway:

Could Warren Buffett’s Berkshire Hathaway Inc. threaten the stability of the financial system? The U.S.’s top regulators are asking themselves this question as they consider whether Berkshire and other large insurers should come under Federal Reserve oversight.

The answer is yes.

While many of Bloomberg’s contributors publish interesting and intellectually-stimulating articles, and many of its financial facts-reporting articles are useful sources of information, Bloomberg ‘Editors’ have taken a very narrow view of what happened during the crisis based on platitudes, partial understandings and other misconceptions, and keep lamenting about the lack of regulatory pressure/intrusion/control. According to the website, it looks like regulation is the alpha and the omega: if only regulators and politicians were more tightly controlling the financial system, there would be no crisis. Criticisms and challenges (or at least discussions) of regulatory failures and regulatory distortions seem to be pretty much non-existent in editorials. Is this really the type of balanced reporting we expect from such a serious financial publication?

Sovereign debt crisis: another Basel creature?

I often refer to the distortive effects of RWA on the housing and business/SME lending channels. What I don’t say that often is that Basel’s regulations have also other distortive effects, perhaps slightly less obvious at first sight.

Basel is highly likely to be partially responsible for sovereign states’ over-indebtedness, by artificially maintaining interest rates paid by governments below their ‘natural’ level.

How? Through one particular mechanism historically, that you probably start knowing quite well: risk-weighted assets (RWA). Basel 1 indeed applied a 0% risk-weight on OECD countries’ sovereign debt*, meaning banks could load up their balance sheet with such instruments without negatively impacting their regulatory capital ratios at all. Interest income earned on sovereign debt was thus almost ‘free’: banks were incentivised to accumulate them to maximise capital-efficiency and RoE.

This extra demand is likely to have had the effect of pushing interest rates down for a number of countries, whose governments found it therefore much easier to fund their electoral promises. In the end, the financial and economic crisis was triggered by the over-issuance of very specific types of debt: housing/mortgage, sovereign and some structured products. All those asset classes had one thing in common: a preferential capital treatment under Basel’s banking regulations.

Basel 2 introduced some granularity but fundamentally didn’t change anything. Basel 3 doesn’t really help either, although local and Basel regulators have recently announced possible alterations to this latest set of rules in order to force banks to apply risk-weights to sovereign bonds (one option is to introduce a floor). Some banks have already implemented such changes (which cost billions in extra capital requirements).

While those measures go in the right direction, Basel 3 has also introduced a regulatory tool that goes precisely the opposite way: the liquidity coverage ratio (LCR). The LCR requires banks to maintain a large enough liquidity buffer (made of highly-liquid and high quality assets) to cover a 30-day cash outflow. As you may have already guessed, eligible assets include mostly… government securities**.

Here again, Basel artificially elevates the demand for sovereign debt in order to comply with regulatory requirements, pushing yields down in the process. This has two consequences: 1. governments could find a lot easier to raise cash than in free market conditions (with all the perverse incentives this has on a democratic process unconstrained by economic reality) and 2. as sovereign yields are used as risk-free rate benchmarks in the valuation of all other asset classes, the fall in yield due to the artificially-increased demand could well play the role of a mini-QE, boosting asset prices across the board ceteris paribus.

We end up with a policy mix that contaminates both central banks’ monetary policies and domestic political debates. But, worst of all, it is a real malinvestment engine, which trades short-term financial solidity for long-term instability.

* Some non-OECD regions of the world also allow their domestic banks to use 0% risk-weight on domestic sovereign debt. For instance, many African countries are allowed to apply 0% weighing on the sovereign debt of their local governments despite the obvious credit risk it represents as well as its poor marketability (this is partly mitigated as this debt is often repoable at the regional central bank). Moreover, the same regulators prevent their domestic banks from investing their liquidity in Treasuries or European debt, with the obvious goal of benefiting those African states. Consequently, illiquid and risky sovereign bonds comprise most of those banks’ “liquidity” buffers, evidently not making those banking systems much safer…

** The LCR is partly responsible for the ‘shortage of safe assets’ story.

Lars Christensen on Yellen and bubbles, and UK regulators at full speed

Lars Christensen published a sarcastic post on his blog, which coincidentally treats the monetary policy and bubbles problem as the same time as my previous post. I fully agree with him that Yellen’s comments are ridiculous.

This is Lars:

it seems to part of a growing tendency among central bankers globally to be obsessing about “financial stability” and “bubbles”, while at the same time increasingly pushing their primary nominal targets in the background.

While I agree with Lars that central banks should provide ‘nominal stability’, I don’t think inflation targeting provides such framework (and I believe Lars agrees). Inflation is very hard to measure, let alone to define, and can be very misleading (Scott Sumner believes that inflation indicators are meaningless). According to a Wicksellian framework, it does look like something’s wrong with interest rates at the moment. Banking regulation, due to its roles in ‘channelling’ interest rates, surely also plays a big role that monetary policy cannot influence. In the end, maintaining inflation right on target is in no way insurance of actual nominal (and financial) stability.

David Beckworth, in a new paper published a few days ago, also criticised inflation targeting on the ground that it contributes to financial instability. I agree with Market Monetarists that a policy stabilising NGDP growth would provide a more robust economy and financial system, though it is in my view still imperfect (I’ll come back to that in another post).

Totally unrelated: in the UK, regulators are working at full speed. Here is a summary of some of the latest regulatory announcements:

- Regulators believe that asset managers ‘waste’ too much client money on sell-side analysts research and want to regulate the process, risking to transform the market into an oligopoly as smaller research providers may not be able to cope with the reduced fee-generation (see here and here)

- HMRC wants to get the power to access your bank account and check your spending habits without going through court to make sure that you are able to pay the taxes they claim you owe them (even if they are wrong). I have personally dealt many times with HMRC (I didn’t owe them money, they did) and the least I can say is that it wasn’t necessarily a pleasant experience: waiting 45min on the phone to end up speaking to someone who sounds very suspicious that you are trying to trick tax authorities… (to be fair, I also ended up speaking to competent and pleasant people) HMRC makes mistakes all the time and I would be very cautious in granting them such powers… (see here and here)

- New rules capping the fees payday lenders can charge are effectively about to kill a large number of them… It probably won’t help much (see here)

- Bank account holders aren’t taking advantage of the best offers available to them and don’t spend their time constantly changing bank to get the best pricing and as a result earn poor returns? The regulator also wants to change that, though I submit that it should tell his boss (the BoE) that, if savers indeed earn poor returns, it possibly is because rates aren’t very high… (see here)

- The BoE and PRA want global banking regulators to reduce RWAs or capital requirements for small banks. Not saying this is a bad thing, but this sounds kind of contradictory to me, given everything we’ve been hearing for years from the same regulators… (see here)

Is the BIS on the Dark Side of macroeconomics?

The BIS has got a hobby: to annoy other economists and central bankers. It’s a good thing. It published its annual report about two weeks ago, and the least we can say is that it didn’t please many.

Gavin Davies wrote a very good piece in the FT last week, summarising current opposite views: “Keynesian Yellen versus Wicksellian BIS”. What’s interesting is that Davies views the BIS as representing the ‘Wicksellian’ view of interest rates: that current interest rates are lower than their natural level (i.e. monetary policy is ‘loose’ or ‘easy’). On the other hand, Scott Sumner and Ryan Avent seem to precisely believe the opposite: that current rates are higher than their natural level and that the BIS is mistaken in believing that low nominal rates mean easy money. This is hard to reconcile both views.

Neither is the BIS particularly explicit. Why does it believe that interest rates are low? Because their headline nominal level is low? Because their real level is low? Or because its own natural rates estimates show that central banks’ rates are low?

It is hard to estimate the Wicksellian ‘natural rate’ of interest. Some people, such as Thomas Aubrey, attempt to estimate the natural rate using the marginal product of capital theory. There are many theories of the rate of interest. Fisher (described by Milton Friedman as America’s best ever economist), Bohm-Bawerk, and Mises would argue that the natural interest rate is defined by time preference (even though they differ on details), and Keynes liquidity preference. Some economists, such as Miles Kimball, currently argue that the natural rate of interest is negative. This view is hard to reconcile with any of the theories listed above. Fisher himself declared in The Rate of Interest that interest rates in money terms cannot be negative (they can in commodity terms).

Unfortunately, and as I have been witnessing for a while now, Wicksell is very often misinterpreted, even by senior economists. The latest example is Paul Krugman, evidently not a BIS fan. Apart from his misinterpretation of Wicksell (see below), he shot himself in the foot by declaring (my emphasis):

Now, what about the BIS? It is arguing that central banks have consistently kept rates too low for the past couple of decades. But this is not a statement about the Wicksellian natural rate. After all, inflation is lower now than it was 20 years ago.

Given that we indeed got two decades of asset bubbles and crashes, it looks to me that the BIS view was vindicated…

Furthermore, in a very good post, Thomas Aubrey corrects some of those misconceptions:

The second issue to note is that when the natural rate is higher than the money rate there is no necessary impact on the general price level. As the Swedish economist Bertie Ohlin pointed in the 1930s, excess liquidity created during a Wicksellian cumulative process can flow into financial assets instead of the real economy. Hence a Wicksellian cumulative process can have almost no discernible impact on the general price level as was seen during the 1920s in the US, the 1980s in Japan and more recently in the credit bubble between 2002-2007.

(Bob Murphy also wrote a very good post here on Krugman vs. Wicksell)

But there are other problematic issues. First, inflation (as defined by CPI/RPI/general increase in the price level) itself is hard to measure, and can be misleading. Second, as I highlighted in an earlier post, wealthy people, who are the ones who own most investible assets, experience higher inflation rates. In order to protect their wealth from declining through negative real returns (what Keynes called the ‘euthanasia of the rentiers’), they have to invest it in higher-yielding (and higher-risk) assets, causing bubbles is some asset classes (while expectations that central bank support to asset prices will remain and allow them to earn a free lunch, effectively suppressing risk-aversion).

If natural rates were negative – or at least very low – and the environment deflationary, it is unlikely that we would witness such hunt for yield: people care about real rates, not nominal ones (though in the short-run, money illusion can indeed prevail). But this is not only an ultra-rich problem: there are plenty of stories of less well-off savers complaining of reduced purchasing power.

Meanwhile, the rest of the population and overleveraged companies, supposedly helped by lower interest rates, seem not to deleverage much: overall debt levels either stagnate or even increase in most economies, as the BIS pointed out.

Banks also suffer from the combination of low rates* and higher regulatory requirements that continue to pressurise their bottom line, and have ceased to pass lower rates on to their customers.

In this context, the BIS seems to have a point: rates may well be too low. Current interest rate levels seem to only prevent the reallocation of capital towards more economically efficient uses, while struggling banks are not able to channel funds to productive companies.

Critics of the BIS point to their call to rise rates to counter inflation back in 2011. Inflation, as conventionally measured, indeed hasn’t stricken in many countries. In the UK and some other European countries though, complaints about quickly rising prices and falling purchasing power have been more than common (and I’m not even referring to house price inflation). This mismatch between aggregate inflation indicators and widespread perception is a big issue, which underlies financial risk-taking.

In the end, Keynes’ euthanasia of the rentiers only seem to prop up dying overleveraged businesses and promote asset bubbles (and financial instability) as those rentiers pile in the same asset classes. I side with the BIS in believing this is not a good and sustainable policy.

I also side with the BIS and with Mohamed El-Erian in believing in the poor forecasting ability of most central bankers, who seem to constantly display a dovish view of the economy, which apparently experiences never-ending ‘slack’, as well as the very uncertain effect of macro-prudential policies, which cannot and will not get in all the cracks. Nevertheless, many mainstream economists and economic publications seem to be overconfident in the effectiveness of macro-prudential policies (see The Economist here, Yellen here, Haldane here, who calls macropru policies “targeted lightning strikes”…).

While central banks’ rates should probably already have risen in several countries (and remain low in others, hence the absurdity of having a single monetary policy for the whole Eurozone), everybody should keep the BIS warnings in mind: after all, they were already warning us before the financial crisis, yet few people listened and many laughed at them.

Unfortunately, politicians and regulators have repeated some of the mistakes made during the Great Depression: they increased regulation of business and banking while the economy was struggling. I have many times referred to the concept of regulatory uncertainty, as well as the over-regulation that most businesses are now subject to (in the US at least, though this is also valid in most European countries). Businesses complaints have been increasing and The Economist reported on that issue last week.

In the meantime, while monetary policy has done (almost) everything it could to boost credit growth and to prevent the money supply from collapsing, harsher banking regulation has been telling banks to do the exact opposite: raise capital, deleverage, and don’t take too much risk.

In the end, monetary policy cannot fix those micro-level issues. It is time to admit that we do not live in the same microeconomic environment as before the crisis. What about cutting red tape to unleash growth rather than risk another financial crisis?

* Yes, for banks, rates are low, whichever way you look at them. Banks can simply not function by earning zero income on their interest-earning assets (loan book and securities portfolio).

PS: Noah Smith, another member of the anti-BIS crowd, has a nonsense ‘let’s keep interest rate low forever’-type article here: raising interest rates would lead to an asset price crash, so we should keep them low to have a crash later. Thanks Noah. The way he describes a speculative bubble is also wrong (my emphasis):

The theory of speculation tells us that bubbles form when people think they can find some greater fool to sell to. But when practically everyone is convinced that asset prices are relatively high, like now, it’s pretty obvious that there aren’t many greater fools out there.

Really? No, speculation involved buying as long as you believe you can get the right timing to exit the position. Even if everyone believed that asset prices were overvalued, as long as investors expect prices to continue to increase, speculation would continue: profits can still be made by exiting on time, even if you join the party late.

PPS: A particularly interesting chart from the BIS report was the one below:

It is interesting to see how coordinated financial cycles have become. Yet the BIS seems not to be able to figure out that its own work (i.e. Basel banking rules) could well be the common denominator of those cycles (which were rarely that synchronised in the past).

It is interesting to see how coordinated financial cycles have become. Yet the BIS seems not to be able to figure out that its own work (i.e. Basel banking rules) could well be the common denominator of those cycles (which were rarely that synchronised in the past).

A tale of two US lending curves

I was a little bit intrigued by my previous chart and decided to take a second look at it. Here it is, using a log scale (as this is a chart covering 47 years, please keep in mind that what looks like small temporary fluctuations actually represent large ones…):

The two dotted lines represent the 1950-1980 trend for each curve. Why did I pick 1980? As it takes many years to develop new international Basel regulations, numerous drafts and proposals are circulated over a few years. This raises expectations of what future regulatory requirements will look like and banks progressively adapt the shape of their balance sheet to be in compliance once the rules effectively kick in. For instance, current Basel 3 regulations consultations started in 2009, with almost final proposals published between 2010 and 2011, and planned to be enforced by 2019, although most banks already comply with many of its features.

A draft of Basel 1 rules was published in 1987, following years of consultations (I am unsure exactly when those started, hence the choice of 1980), followed by a final agreement in 1988 and an official enforcement from 1992 onwards. In the US, Basel 1 was in place until well into the 2000s, and only a few banks had started applying Basel 2 before the crisis.

The first shocking feature of this chart is the differential between trend and actual business lending volume. Business lending completely collapsed relative to trend from the end of the 1980s, coinciding pretty much exactly with the implementation of Basel 1, and despite real interest rates falling (see chart below). Can any other (macro or micro) economic event explain this very sudden change? Did we overnight move into a low-growth/secular stagnation/economic ‘abundance’ paradigm? This looks highly unlikely.

The second remarkable feature is that real estate lending volume did not offset the fall in business lending. For a long period, real estate lending seemed to be above pre-1980 trend, before getting back to trend level and then departing from it again from the early 2000s. Never real estate lending fell below trend following the introduction of Basel 1, except during the Great Recession.

Now, this chart is very hard to interpret by itself, and it will take much more analysis to come to any meaningful conclusion. Pre-1980 lending trend perhaps was too rapid (remember post-WW2 boom and stagflation)? This would have two possible consequences: 1. real estate lending growth would therefore have been way too fast post-1980 and 2. business lending was perhaps in line with the actual trend?

My guess is that the truth lies in between: pre-1980 trend was perhaps too rapid, but post-1980 business lending growth was too low. Remember that household debt to income kept increasing over the period, signalling that real estate lending growth was surely too fast.

There is another possible explanation: that my chart does not cover all possible lending instruments. We know that Basel rules strongly encouraged the use of securitised products (which benefited from better capital treatment), in particular securitised mortgage instruments such as CMBS and RMBS. Banks that originate those mortgages originally reported them on their balance sheet, before taking them off-balance sheet. Does the FRED real estate lending data include those products (off-balance sheet or purchased by other institutional investors)? I have no idea and will have to do a lot more research on the FRED database before coming up with a satisfying description of the chain of events.

Is the US dissociating from Basel banking rules?

I was left a little bewildered by this recent FT article:

US lending to businesses is reaching record levels but banks are privately warning that the activity should not be seen as evidence of an economic recovery.

Despite Basel rules that favour mortgage lending over business lending, and business lending struggling in Europe and the UK as a result, have US banks found the trick to bypass those rules or decided not to maximise their profitability? Is the US special?

First, let’s look at the data:

The first thing that comes out of this chart is the massive trend change from the end of the 1980s onwards. What happened at that time? Basel 1 rules were introduced, making it more expensive in terms of capital utilisation to lend to corporates than for real estate-related purposes. Basel is the turning point. Ex-ante, corporate lending volume used to be slightly larger than mortgage lending for decades. Ex-post, house lending became the primary channel of credit growth, by far.

The first thing that comes out of this chart is the massive trend change from the end of the 1980s onwards. What happened at that time? Basel 1 rules were introduced, making it more expensive in terms of capital utilisation to lend to corporates than for real estate-related purposes. Basel is the turning point. Ex-ante, corporate lending volume used to be slightly larger than mortgage lending for decades. Ex-post, house lending became the primary channel of credit growth, by far.

Something happened during the crisis: from end-2010 until now, the differential between the total volume of mortgage lending and the total volume of corporate lending tightened to USD1.9Tr. Surely this doesn’t fit my story that Basel rules introduce massive distortions of the lending channel. I have to admit that my knowledge of the US market is limited. Nevertheless, there is a possible explanation.

First, the tightening remains moderate: ‘only’ USD200Bn, or 9.5% of the original differential. The tightening arose from a strong recovery of business lending from early-2011 onwards (following a sharp fall during which the differential actually widened), whereas mortgage lending remained flat.

Second, risk-weights on residential and commercial real estate lending actually increase when the sector suffers and property prices collapse. The US experienced a large fall in both residential and commercial real estate prices. As defaults on those mortgages and foreclosures soared, risk-weights increased.

It is then very likely that, from a capital utilisation point of view, lending to businesses was as profit-maximising – if not more – as extending credit for real estate purposes. Indeed, daily corporate bankruptcies started normalising from early 2010, whereas house prices continued declining until mid-2012.

It also looks like much of this new corporate lending has been driven by large corporations (for acquisitions and share buybacks), which are less capital intensive for banks (especially at the moment, as many of them are sitting on large piles of cash, USD1.6Tr according to Moody’s, and growing at rapid pace – 12% p.a.). Moreover, the latest data seems to indicate that real estate lending is making a comeback.

At the end of the day, it looks a little premature to say that US banks have found the way to bypass Basel to fund industrial companies and SMEs…

Nevertheless, there is some glitter of hope. The UK regulator PRA warned banks that they may have to increase risk-weights on mortgage lending, hence increasing the amount of capital necessary to fund those loans and making them slightly less attractive to maximise profitability, relatively to other asset classes. This is ironic though. Risk-weights have been introduced and encouraged by regulators over the last twenty years, and still very few of them seem to understand the inherent capital allocation distortion they lead to…

I had a dream: that RWAs and Basel’s economically distortive rules were abolished and we were going back to the pre-1988 consensus of similar industrial and mortgage lending volume. Perhaps we would witness fewer housing bubbles and more economic growth*… But that’s just a dream.

* And be spared of ignorant ‘secular stagnation’ ideas that ignore the economic dynamics at the micro level…

PS: reduced blogging activity over the past 10 days due to work and travel… I’ll try to catch up soon.

A brief comment on Piketty

Thomas Piketty’s new book, Capital in the 21st Century, is both controversial and a great success. Despite its flaws, its success reflects growing concerns that need to be addressed. I finished reading the book a few weeks ago and actually found it quite interesting (apart from its nonsensical last section) and easy to read. I am not going to review it here: there are already possibly 1,000 reviews available online, focusing on the underlying economic theory or on the data-picking of the book.

One thing struck me though: the lack of explanation as to why the data evolves the way it does. Piketty seems to believe that this is the result of a ‘fundamental and inherent’ characteristic of capitalism (‘r > g’). Fair enough, but despite all his expertise in the unequality area, Prof Piketty seems to lack the necessary knowledge in other economic and finance areas to reach the right conclusions.

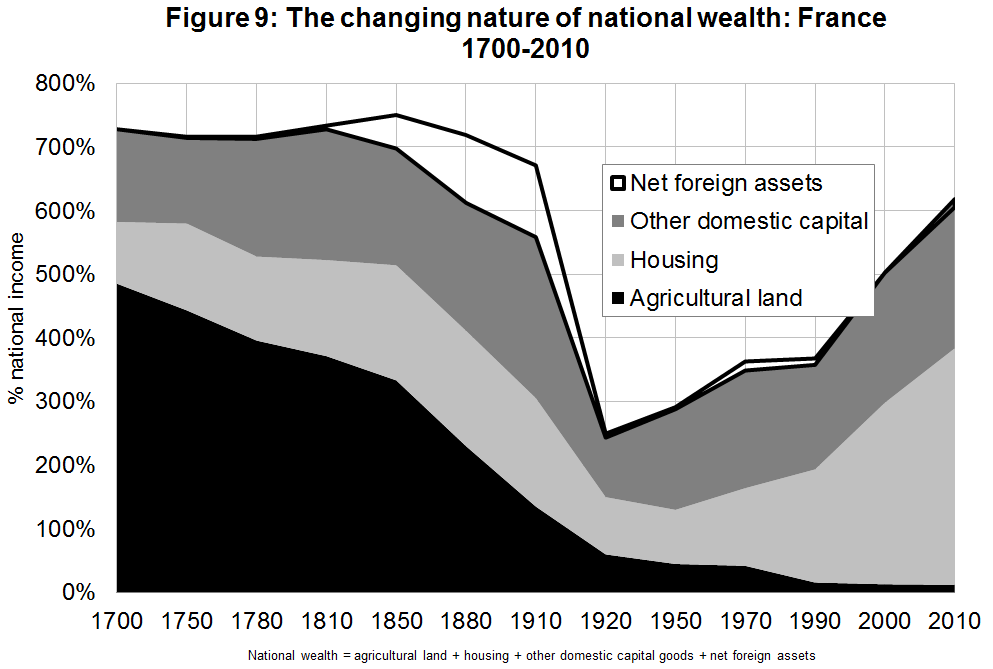

He uses the three following charts to demonstrate the evolution of wealth as a share of national income throughout the last few centuries.

In the US:

In Britain:

In France:

Now compare with the following charts:

A lot of people have already pointed out that most of what Piketty sees as ‘rise’ in inequality in fact emanates almost entirely from housing bubbles… This is obvious for Britain and France, though I am surprised by Piketty’s US chart as the US clearly experienced a housing bubble as well, which seems not to be reflected in in his wealth data: US housing roughly represented the same share of wealth in 2010 as in 1990. This may be due to the fact that, in 2010, US housing prices had collapsed, which is not captured by Piketty’s chart (which isn’t smooth enough, i.e. one data point every 20 years).

Piketty admits several times in his book that ‘bubbles’ were partly the underlying cause of those rises. Yet, to him, those bubbles seem to be fundamental features of capitalism and government must intervene by redistributing the increased capital stock. As I mentioned a couple of weeks ago, I encourage him to dig into Basel banking regulations, which distort lending by benefiting housing and were implemented almost exactly when housing wealth started rising. He would probably notice that a large part of the increase in pre-crisis wealth inequality was due to a combination of banking regulation and interest rates below their ‘natural’ level*, both creatures of government intervention, not of free market capitalism…

* Planning restrictions in places like London and Paris also are to blame, I know, though they can’t explain everything. And, anyway, they also reflect government measures…

Recent Comments