You thought Davos was a laissez-faire forum? Think again

![]() Business Insider reported that Mark Carney, the BoE Governor, said last week at the World Economic Forum in Davos that IT and online-enabled new financial business models could lead to “an Uber-type situation” in financial services, unless government acted fast to regulate those new firms. Carney worries that those financial entrepreneurs will damage banks’ established model.

Business Insider reported that Mark Carney, the BoE Governor, said last week at the World Economic Forum in Davos that IT and online-enabled new financial business models could lead to “an Uber-type situation” in financial services, unless government acted fast to regulate those new firms. Carney worries that those financial entrepreneurs will damage banks’ established model.

I am a little shocked by Carney’s remark. To be fair, it is possible that BI reported those comments out of context, so I’ll give Carney the benefit of the doubt. But I find it hard to understand why Carney would intervene, or simply comment, on the normal laissez-faire Schumpeterian creative destruction process. If banks are to be superseded by more efficient business models (and potentially more stable?), why objecting to that? Why protecting banks? Unless protecting banks is a way of maintaining central banks’ powers (which could also potentially be affected by technological disruptions)?

A further divide between Carney and the private sector (here: banks) appeared in Davos. Carney appeared worried that there used to be an “illusion of liquidity” in financial markets, which is now “gradually being disabused.” This contrasts with what private banks and fund managers believe, as exemplified by Deutsche Bank’s co-CEO Jain, who reportedly clashed with Carney and Jack Lew (US Treasury Secretary) behind closed doors “over whether recent violent market swings were caused by a liquidity crisis fuelled by onerous regulation”, as reported by the FT. Both officials rejected this conclusion.

Carney may well be right when he says that there used to exist an illusion of liquidity. But perhaps not for the reasons he thinks. ‘Excess’ liquidity in markets in the pre-crisis era is likely to have emanated from central banks’ actions. In a free market, liquidity might have indeed been scarcer and markets a little more volatile, reflecting a rougher price discovery process (rather than a one way bet). But, as I have also described in a relatively recent post, regulation is definitely responsible for the liquidity deficiency that we now experience. Regulation created silos that effectively entrapped vast amounts of liquid assets. There isn’t much point denying it really. Regulation has drawbacks and regulators should instead acknowledge them and announce what they can do to alleviate the situation. If they don’t, we are likely to see an increasing number of clashes between the private sectors and regulators, which aren’t going to help our economic recovery much.

Easy money is secondary to bank regulation in triggering housing booms

I’ve already reported on the excellent piece of research that Jordà et al published last year. Last month, they elaborated on their previous research to publish another good paper, titled Betting the House. While their previous paper focused on gathering and aggregating real estate and business lending data across most major economies since the second half of the 19th century, their new paper built on this great database to try to extract correlations between ‘easy’ monetary conditions and housing bubbles.

Remember their remarkable chart, to which I had added Basel and trend lines:

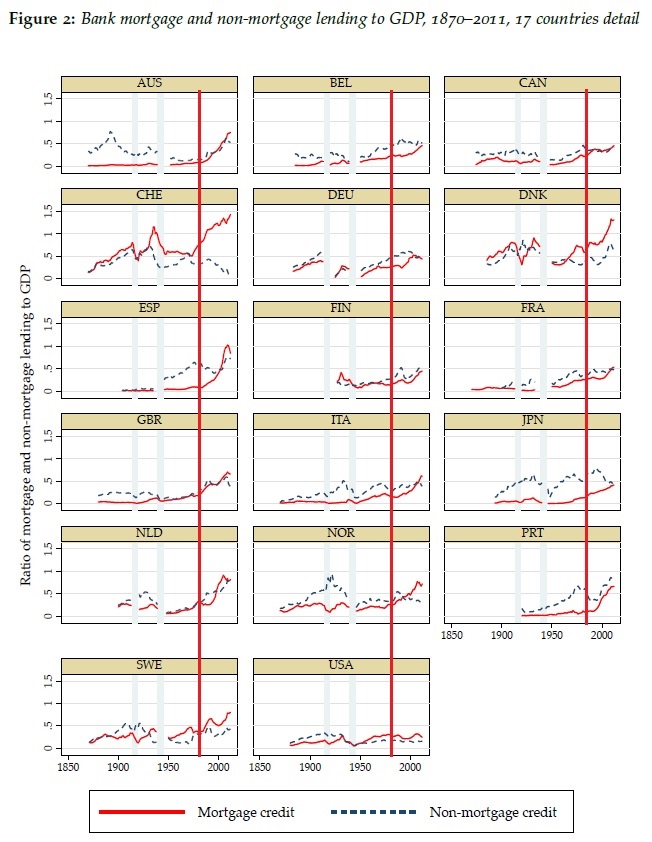

They also produced the following chart, which shows disaggregated data across countries (click on it to zoom in). I added red vertical bars that show the introduction of Basel 1 regulations (roughly… it’s not very precise). What’s striking is that, almost everywhere, mortgage debt boomed as a share of GDP and overtook business lending. It was a simultaneous paradigm change that can hardly be separated from the major changes in banking regulation and supervision that occurred at that time.

They also produced the following chart, which shows disaggregated data across countries (click on it to zoom in). I added red vertical bars that show the introduction of Basel 1 regulations (roughly… it’s not very precise). What’s striking is that, almost everywhere, mortgage debt boomed as a share of GDP and overtook business lending. It was a simultaneous paradigm change that can hardly be separated from the major changes in banking regulation and supervision that occurred at that time.

Their new study repeats most of what had been said in their previous one (i.e. that mortgage credit had been the primary driver of post-WW2 bank lending) and then compares real estate lending cycles with monetary policy. And they conclude that:

Their new study repeats most of what had been said in their previous one (i.e. that mortgage credit had been the primary driver of post-WW2 bank lending) and then compares real estate lending cycles with monetary policy. And they conclude that:

loose monetary conditions lead to booms in real estate lending and house prices bubbles; these, in turn, materially heighten the risk of financial crises. Both effects have become stronger in the postwar era.

As I said in my post on Jordà et al’s previous research, most (if not all) of what they identify as post-WW2 housing cycles actually happened post-Basel implementation. I wish they had differentiated pre- and post-Basel cycles.

They start by assessing the stance of monetary policy in the Eurozone over the past 15 years, using the Taylor rule as an indicator of easy/tight monetary policy. While the Taylor rule is possibly not fully adequate to measure the natural rate of interest, it remains better than the simplistic reasoning that low rates equal ‘easy’ money and high rates equal ‘tight’ money. According to their Taylor rule calculation, the stance of monetary policy in the Eurozone before the crisis was too tight in Germany and too loose in Ireland and Spain. In turn they say, this correlated well with booms in mortgage lending and house prices (see chart below).

At first sight, this seems to confirm the insight provided by the Austrian business cycle theory: Spain and Ireland benefited from interest rates that were lower than their domestic natural rates, launching a boom/bust cycle driven by the housing market. (While Germany was the ‘sick’ man of Europe as the ECB policy was too tight in its case)

At first sight, this seems to confirm the insight provided by the Austrian business cycle theory: Spain and Ireland benefited from interest rates that were lower than their domestic natural rates, launching a boom/bust cycle driven by the housing market. (While Germany was the ‘sick’ man of Europe as the ECB policy was too tight in its case)

And while this is probably right, this is far from being the whole story. In fact, I would say that ‘easy’ monetary policy is only secondary to banking regulation in causing financial crises through real estate booms. As I have attempted to describe a little more technically here, Basel reorganised the allocation of loanable funds towards real estate, at the expense of business lending. This effectively lowered the market rate of interest on real estate lending below its natural rate, triggering the unsustainable housing cycle, and preventing a number of corporations to access funds to grow their business. By itself, Basel causes the discoordination in the market for loanable funds: usage of the newly extended credit does not reflect the real intertemporal preference of the population. No need for any central bank action.

What ‘easy’ monetary policy does is to amplify the downward movement of interest rates, boosting real estate lending further. But it is not the initial cause. In a world without Basel rules, the real estate boom would certainly have occurred in those proportions, and quick lending growth would have been witnessed across sectors and asset classes. The disproportion between real estate and business lending in the pre-crisis years suggests otherwise.

* They continue by building a model that tries to identify the stance of monetary policy throughout the more complex pre-WW2 and pre-1971 monetary arrangements. I cannot guarantee the accuracy of their model (I haven’t spent that much time on their paper) but as described above, everything changed from the 1980s onward anyway.

PS: The ‘RWA-based ABCT’ that I described above is one of the reasons why I recently wrote a post arguing that the original ABCT needed new research to be adapted to our modern financial system and be of interest to policymakers and the wider public.

Worrying inconsistency at the heart of policymaking

Imagine you read a book* stating that:

Banks do not lend out their reserves at the central bank. Banks create loans on their own, as already explained above. They do not need reserves to do so and, indeed, in most periods, their holdings of reserves are negligible.

Fine. I deeply disagree with this statement, but that person has the right to say it. Free speech is back in fashion nowadays.

The author of that book had actually said a few months earlier something similar in an FT article**:

Second, the “money multiplier” linking lending to bank reserves is a myth. In the past when bank notes could be freely exchanged for gold, that relationship might have been close. Strict reserve ratios could yet re-establish it. But that is not how banking operates today. In a fiat (or government-made) monetary system, the central bank creates reserves at will. It will then supply the banks with the reserves they need (at a price) to settle payments obligations.

So far so good.

Now, imagine that, for some reason, you ended up on another FT article***, dating back five years, declaring this:

Indeed, the Fed explained precisely what it would do in its monetary report to Congress last July. If the worst came to the worst, it could just raise reserve requirements.

Point reiterated just two days ago**** by the same economist, commenting on the Swiss central bank euro unpegging:

Furthermore, the Swiss could have curbed inflationary dangers without abandoning the peg, for instance by increasing reserve requirements on banks.

‘Foolish’ you would say. This person should read the other author above, who said that reserve requirements were useless because banks did not ‘lend out’ their reserves and that central banks would provide those reserves on demand anyway. So how could a reserve requirement increase by the SNB prevent money creation and inflationary danger? These two economists clearly disagree with each other.

But………..

Ironically, this person also declared that other people “failed to understand how the monetary system works” and that this issue wasn’t “just academic” but that “understanding the monetary system [was] essential.” But has no problem switching from one side of the endogenous outside money debate to the other whenever it suits his argument.

More worryingly, this economist was also a member of the UK’s Independent Commission on Banking, which came up with the idea of ‘ringfencing’. I suddenly find it even harder than before to really trust his views on banking issues. I also find it bewildering that an economist of such reputation could be so internally inconsistent and blatantly contradict himself article after article. This isn’t very reassuring.

Oh, I forgot to say who this economist was. He’s called Martin Wolf.

* See my review of the book, published September 2014, here.

** See article here, dated April 2014

*** See article here, dated November 2010

**** See article here, dated January 2015

The end of banking? Not like this please

I recently read Jonathan McMillan’s The End of Banking, which I first heard of through FT Alphaville here (McMillan is actually a pseudonym to cover it two authors: an academic and a banker). I have mixed feelings about this book. I really wanted to agree with it. And I do, to some extent. But I simply cannot agree with a number of other points they make.

Their proposal to reform banking is as follows (see the book for details): lending can be disintermediated through P2P lending platforms (and equivalent), which both monitor potential borrowers through credit scoring and allocate savers’ funds to minimise the probability of losses. Marketplaces set up by platforms would enable savers to sell their investments to generate cash if needed. What about the payment system? Their solution is for non-bank FIs to continuously provide market liquidity a number of financial instruments using algorithmic trading. Current accounts would in fact be invested like mutual funds, which would instantly convert those investments into cash when required for payment. They also propose accounting rule changes to prevent corporations from creating money-like instruments.

As such, they propose to end banks’ inside money and have a financial system exclusively based on digital outside money controlled by a monetary authority. While they don’t classify it this way, it does seem to me to be some sort of 100%-reserve banking proposal: the money supply is fixed in the very-short term and exogenously-defined by the monetary authority.

What I agree with:

- The main thesis of the book is completely valid and is something I have also argued for a little while: technological disruptions are now allowing us to go beyond banking and disintermediate it. P2P lending, non-banking payment systems, decentralised payment frameworks and currencies, algorithm-driven credit scoring… In many areas, banks have almost become redundant. I totally adhere to the authors’ thesis (although credit scoring does have real limitations).

- Technological developments have facilitated regulatory arbitrage, if not enabled it. Computing power now allow banks to optimise their capital requirements through the use of complex models which, it is important to point out, are validated by regulators.

What I disagree with:

- The authors seem to believe that banking regulation is usually a good thing and cannot seem to understand the various distortions, bubbles and inefficiencies those regulations create. According to them, if only technology hadn’t boomed over the past three decades, the banking system would be more stable. I strongly disagree.

- I dislike the top-down banking reform approach taken by their thesis. Free markets, driven by technology, should decide under what form the next iteration of banking should arise.

- I also see weaknesses in their proposal. First, I cannot agree with their view that money belongs to the public sphere, and that IOUs must benefit from a state guarantee to qualify as money. This has been disproved by history over and over again. Second, I see their proposal to have algorithmic trading manage the payment system as not only unworkable, but also dangerous. As already witnessed, algorithmic trading is imperfect and can amplify crashes rather than prevent them. How their payment system would react during a crisis, when everyone tries to exit most investments and pile into a few others, is anyone’s guess. Mine is that the payment system would suddenly be down, paralysing the entire economy. To be fair, their treatment of cash is unclear: could we maintain a custody account comprising only digital cash in their framework?

- Their 100%-reserve banking reform does not address fluctuations in the demand for money. Centralised monetary authorities do neither have access to the right information, nor within the right timeframe, to accurately provide extra media of exchange when needed by the public. Private entities, in direct contact with the public, can.

- Finally, though this is a minor point, I disagree with their monetary policy stance. It is inaccurate to present price stability as ideal to avoid economic distortions: productivity increases should lead to mild deflation in a growing economy (see Selgin’s Less than Zero or any market monetarist or Austrian blog and research paper). I also reject their physical cash ban, from a libertarian standpoint: people should be able to withdraw cash if ever they wish to*. This would seriously limit their negative interest rates policy proposal.

Overall, it is a thought-provoking and interesting book, which also quite accurately describes our current banking system in its first part (mostly aimed at people who don’t know that much about banking). Its two authors are also right to point out the defects of regulation in an IT-intensive era. But, in my opinion, they draw the wrong conclusions and the wrong reform proposals from their original assessment.

* Here again, their treatment of cash is unclear: can cash be withdrawn in a digital form and maintain in a digital wallet outside the financial system? I doesn’t look so from their book but I cannot say for sure.

Are ETFs making markets less efficient?

I don’t have an answer to that question. But I have been wondering for a little while.

Noah Smith, on Bloomberg, and John Authers, in the FT, are pointing out that passive funds keep witnessing inflows at the expense of actively managed funds (which still represent the large majority of assets under management). Smith adds that academic research overwhelmingly demonstrates that active fund management (whether hedge funds or more traditional, and cheaper, mutual funds) is a ‘waste’ of money.

Market efficiency requires that many different individuals make their own investment assessment and decisions, in accordance with their limited means, knowledge and preferences. Some will gain, some will lose, market prices will continuously fluctuate one way or another in a permanent state of disequilibrium that reflects investors’ evolving views of what constitutes an efficient allocation of resources. In turn market price movements in themselves lead investors to reassess their opinions, bringing about further fluctuations but eventually producing something that resemble a near-equilibrium market, which almost accurately reflects investors’ preferences… for a few instants… after which other investors’ reactions are triggered. This is confusing; this is perpetual discovery and adaptation; this is the market process*.

Hence the importance of prices. And in particular, of relative prices. Investors can pick investments among a very wide range of securities. Such market granularity eases the market process: when one particular security looks underpriced relative to its peers, investors might start buying (until its price has gone up).

ETFs, index funds, on the other hand, allow investors to buy the whole market, or a large part of it, or a whole sector. They merely replicate market movements. As such, granularity, relative prices, and intra-market fluctuations disappear. Consequently, if everyone starts buying the whole market, there is no room left to pick winners within the market. Efficient firms and investments benefit as much from the inflow of capital as bad ones. Once a majority of investors start buying the whole market through index funds, stock pickers will have very limited choice to pick winners. Resources allocation, and in the end economic efficiency, becomes impaired**.

All this remains very theoretical. I haven’t been able to find any theoretical or empirical paper that researched this particular topic (please let me know if you know any). 2013 Nobel-winner Eugene Fama recently dismissed those concerns:

There’s this fallacy that you need active managers to make the market efficient. That’s true to some extent, but you need informed active managers to make it more efficient. Bad active managers make it less efficient.

Basically, he hasn’t answered the question. According to him, no, ETFs don’t make markets less efficient, but yes that’s true to an extent but no if you have bad active managers. Not that helpful to say the least. He is the father of the efficient market hypothesis so probably a little biased to start with.

Smith has another answer: he believes that asset-class picking could become the new stock-picking and that active management could shift from relative intra-market prices to relative inter-market prices. Basically, investors would take positions on, let’s say, the German stock market vs. the British one, instead of picking companies or securities within each of those markets. This is a possibility, albeit one that doesn’t really solve the economic resources allocation efficiency problem described above. Investors also don’t always have the option to invest outside of their domestic market, for contractual or FX fluctuation reasons.

It is likely that stock picking won’t disappear. Investors will always want to buy promising or sell disappointing individual securities. Still, the rise of index investing could have some interesting (and possibly far-reaching) implications for the market process and resource allocations. It is, as yet, unclear what form these implications may take.

* This ‘market efficiency’ definition is very close to the one defined by Austrian school scholars (which I prefer), as opposed to the more common market efficiency as defined under the equilibrium neo/new classical and Keynesian frameworks. See summaries here, as well as a more detailed description of the New classical efficient market hypothesis here.

** A real life comparison would be: instead of purchasing one TV, after carefully weighing the pros and cons of each option out there, everyone starts buying all possible models from all manufacturers, independently of their respective qualities. The company offering the worst product would benefit as much as the one offering the best product. Needless to say, this isn’t the best way of maximising economic resources.

Why can’t economists understand margin compression?

Are basic accounting statements so difficult to interpret? According to Viennacapitalist, who commented on my previous post, it does seem so. At least for macroeconomists. Indeed, Werner seemed to imply that most economists did not know that deposits sat on the liability side of a bank’s balance sheet (he’s surely wrong), and I have many times pointed out the central bankers’ and policymakers’ misunderstanding of banking mechanics.

Three researchers from the BIS just confirmed the trend. In a new working paper called ‘Has the transmission of policy rates to lending rates been impaired by the Global Financial Crisis?’, they wonder, and try to find out, why spreads between central banks’ base rates and lending rates have jumped once base rates reached the zero-lower bound.

It’s a debate I’ve already had almost a year ago, when I tried to explain that, due to the margin compression effect (an accounting phenomenon), spreads would have to increase in order allow banks to generate sufficient earnings to report (at least) positive accounting net incomes (see here and here).

Those BIS researchers have come up with the same sort of dataset and charts I did over the past year, although they also looked at the US (but didn’t look as other European countries, unlike what I did in this post). This is what they got:

This looks very very similar to my own charts. Clearly, spreads jumped across the board: pre-crisis, they were around 1.5% in the US, 1.5% in the UK and 1.25/1.5% in Spain and Italy. In 2009/2010, with base rate dropping to the zero-lower bound, things changed completely: spreads were of 3% in the US, 2.25% in the UK, 2% in Spain and 1.5% in Italy. Rates had not dropped as much as base rates. Worse, spreads on average increased afterwards: by 2013, spreads were around 2.5% in all countries.

This looks very very similar to my own charts. Clearly, spreads jumped across the board: pre-crisis, they were around 1.5% in the US, 1.5% in the UK and 1.25/1.5% in Spain and Italy. In 2009/2010, with base rate dropping to the zero-lower bound, things changed completely: spreads were of 3% in the US, 2.25% in the UK, 2% in Spain and 1.5% in Italy. Rates had not dropped as much as base rates. Worse, spreads on average increased afterwards: by 2013, spreads were around 2.5% in all countries.

The BIS researchers tried to understand why. Unfortunately, they focused on the wrong factors. They built a model that concluded that the “less pass-through seems to be related in part to higher premium for risk required by banks and by worsening of their financial conditions as well.” They are probably right that some of these factors did play a role. But they cannot explain why the spread remains so elevated even in economies that have experienced strong recoveries such as the US or, more recently the UK.

But their study also has a number of other problems. First, they used new lending data only. It is extremely tricky to extract credit risk information from new lending rate figures. Why? Because new lending rates only show credit actually extended. Many borrowers cannot access credit altogether or simply refuse to do so at high rates. Consequently, the figures could well only reflect borrowers that have relatively good credit risk in the first place as banks try to eliminate credit risk from their portfolio. Second, they never ever discuss operating costs and margin compression, as if banks could simply lower interest income to close to 0 and get away with it.

But for this, they should have looked at two things: deposit rates and banks’ back books (i.e. legacy lending). Not new lending only. When the margin between deposit rates and lending rates on back books fall below banks’ operating costs, banks have to offset that decline by increasing spreads. This is why I suggested that the actual lowering base rates ceased to be effective from around 1.5 to 2% downward as a means of reducing household and companies’ borrowing rates.

Problem is, very few researchers and policymakers seem to get it. Patrick Honohan, of the Irish Central Bank, and Benoit Coeuré, of the ECB, do seem to understand what the issue is. Bankers and consultants have for a while (see Deloitte at the end of this post). Some economic commentators assert that it is hard to figure out why bankers keep complaining about low rates. This dichotomy between theorists and practitioners is leading to misguided, and potentially harmful, policies.

But let me ask a simple question. How hard is it to understand bank accounting really?

More, more, more money endogeneity confusion

First of all, happy new year everyone! We are now in 2015, so keep your eyes open for Marty McFly on the 21st of October.

Let’s start the year with one of my favourite topics: money endogeneity. I’ve covered the subject a number of times, but it keeps coming back. On Mises Canada, Bob Murphy wrote a good post on the differences in reserve management between individual banks and the banking system as a whole (and describes very well the first step of Yeager’s ‘hot potato’ effect, that is, the increase in goods’ nominal prices). Murphy was replying to Nick Freiling’s post, who accused him of making a common mistake. Bob is right and Nick is wrong. In another ‘banks create money out of thin air’ post, Lord Keynes comments on (and, surprisingly, likes) a rather weird new piece of research by Richard Werner.

First, this is Nick:

Banks might decide to increase lending, but not at the expense of losing interest on reserves at the Fed. In fact, banks would rather earn interest on both new loans and reserves at the Fed (which is possible because new loans don’t require an outflow of reserves). Ideally, Bob would write a check against his loaned funds account that is addressed to another customer of that bank. Then the bank sees no loss in reserves (and so earns the same interest on the reserves as before) plus an increase in loaned funds which, of course, earns interest.

This is a very subtle point, but has huge implications for predicting inflation and gauging the effects of QE and growth in the monetary base. For example, there is no threat of sky-high levels of reserves “turning into” loans funds and thereby launching us into hyperinflation. Sure, a higher level of reserves pushes banks further from being constrained by their reserve-requirement ratio, which means they can increase lending. But banks are normally not reserve-constrained, so the relationship between reserves and loans is not direct, and might be hardly related at all.

There are some confusions here. Reserves can be in excess as long as banks aren’t fully ‘loaned up’ to the maximum allowed by reserve requirements. For instance, if the banking system has an aggregate $1,000 of reserves, and assuming a 10% reserve requirement, total lending can be expanded to $10,000. If overnight, reserves increase to $1,500 but lending remains at $10,000, the system holds $1,000 of ‘required’ reserves and $500 of ‘excess’ reserves. The Fed has been paying interest on this ‘excess’ for several years now (which wasn’t the case before). What happens if banks decide to increase lending following this reserves injection? $1,500 in reserves allows banks to lend an extra £5000. When lending reaches $15,000, there are no reserves in ‘excess’ anymore. Reserves have all become ‘required’. This is what many people mean by ‘lending out’.

Murphy’s point was that, at the individual bank level, the risk-adjusted yield on the ‘excess’ portion of reserves is compared to the risk-adjusted yield that the bank can make by expanding its loan book. Sure, the Fed still pays interest on required reserves, but it’s the excess reserves portion that is a monetary policy tool. Moreover, it is highly likely that the expanding bank is going to be subject to adverse clearing, thereby losing reserves to a competitor during the interbank settlement process, and hence the associated interests on reserves. Consequently, extending credit often leads to reserve outflows. The lower the market share of the bank, the more likely it is to suffer outflows. The system as a whole, on the other hand, does not lose reserves (unless withdrawn by depositors), and the interests on reserves lost by the first bank are now earned by another one.

The second point is trickier. There was indeed no inflation over the past few years despite the huge increase in reserves. And doomsayers (including Bob) have been wrong in predicting hyperinflation in the short-term. However, as I have recently pointed out, US excess reserves also massively increased during the Great Depression and the money multiplier collapsed. It took between 30 to 40 years for the multiplier to increase again, and guess what, this happened just before inflation levels jumped in the US (in the 1970s and 1980s). Coincidence? Maybe.

The problem is that Nick relies on a flawed banking theoretical framework. He quotes economist Paul Sheard as saying:

This is possible, again, because loans do not “come from” excess reserves. As Sheard explains:

…banks do not need excess reserves to be able to lend. They need willing borrowers and enough capital – the central bank will always supply the necessary amount of reserves, given its monetary stance (policy rate and reserve requirements).

This is the ‘endogenous money’ view (or, to be more precise, the ‘endogenous outside money’ view, as the fractional reserve banking theory necessary implies an endogenous inside money framework), also adopted by MMT-proponents (as well as Frances Coppola, though she says she doesn’t believe in MMT). It’s a nice theoretical construction. Just wrong. I have extensively written about this (see here, here, here and here). To be brief, there is no way an individual bank could continuously extend credit through central bank funding. This bank would suffer from central bank funding stigma (see also this recent paper) and be violently punished by the financial markets, forcing the contraction of its loan book (and of the money supply) in the medium-term. I advise Paul Sheard, who works for the rating agency S&P, to spend some time with his bank analyst colleagues, and ask them how they view a bank that increasingly relies on central banks for funding and liquidity. He might be surprised. In reality, banks’ inside money is endogenous but constrained by exogenous limits defined by the outside money supply (i.e. reserves).

At least, the MMT view is nicely-constructed, on a relatively sound theoretical basis. This isn’t the case of Richard Werner’s latest paper, titled ‘Can banks individually create money out of nothing? – The theories and the empirical evidence’.

I really don’t know what to think of it. It accumulates so many mistakes and misunderstandings that it becomes hard to take seriously. Its author seems to identify three banking theories: the credit creation theory of banking, the fractional reserve banking theory (FRB) and the financial intermediation theory of banking. The first one implies that banks are not constrained by reserves to extend credit, but not MMT-style: according to the theory (Werner has been a long-time proponent), banks apparently never need reserves (whereas MMT/endogenous theory says that banks can just borrow them from the central bank without limit). The last theory of the list emanates from Tobin’s work ‘Commercial Banks as Creators of Money’, which Werner considers the most dominant theory of banking nowadays. He makes a curious distinction between this view and FRB, as if they were unrelated. But Tobin’s ‘new view’ is based on FRB and the distinctions remain relatively minor.

Nevertheless, Werner manages to make the following (amazing) claim (my emphasis):

Starting by analysing the liability side information, we find that customer deposits are considered part of the financial institution’s balance sheet. This contradicts the financial intermediation theory, which assumes that banks are not special and are virtually indistinguishable from non-bank financial institutions that have to keep customer deposits off balance sheet. In actual fact, a bank considers a customers’ deposits starkly differently from non-bank financial institutions, who record customer deposits off their balance sheet. Instead we find that the bank treats customer deposits as a loan to the bank, recorded under rubric ‘claims by customers’, who in turn receive as record of their loans to the bank (called ‘deposits’) what is known as their ‘account statement’. This can only be reconciled with the credit creation or fractional reserve theories of banking.

Wait… really? So you mean that most economists did not know that deposits were sitting on the liability side of banks’ balance sheet?… Or perhaps they did, and the author simply completely misunderstood the ‘financial intermediation’ theory.

Furthermore, Werner also misunderstands the FRB theory:

Since the fractional reserve hypothesis requires such an increase in deposits as a precondition for being able to grant the bank loan, i.e. it must precede the bank loan, it is difficult to reconcile this observation with the fractional reserve theory.

This is also wrong. The FRB theory never states that a bank needs to get hold of reserves before extending credit. Indeed, the FRB states that a monopoly bank can extend credit up to several times its reserve base, because it is not subject to adverse interbank clearing. In a competitive market however, banks are likely to suffer from reserve outflows at some point. This implies that an individual bank needs to find extra reserves before the outflow occurs (in case it doesn’t already have some in excess) in order not to default on its interbank settlement. But this also implies that the bank can extend credit before finding those reserves*.

This leads Werner’s empirical evidence to completely miss the point: of course the bank can extend credit out of nowhere. But in this case the bank also knows that no cash is going to leave its vaults as the result of the transaction (which the researchers agreed to repay on the following day)**. But here we go: the paper ‘rejects’ the FRB theory on the ground that (brace yourself) “there seems no evidence that reserves (cash and claims on other financial institutions) declined in an amount commensurate with the loan taken out.”

There is evidently no discussion whatsoever in the paper of adverse clearing or evidences in banking history. No, instead, the paper concludes that

it can now be said with confidence for the first time – possibly in the 5000 years’ history of banking – that it has been empirically demonstrated that each individual bank creates credit and money out of nothing, when it extends what is called a ‘bank loan’. The bank does not loan any existing money, but instead creates new money. The money supply is created as ‘fairy dust’ produced by the banks out of thin air. The implications are far-reaching.

Nothing less.

According to the paper, Keynes:

was perhaps even more dismissive of supporters of the credit creation theory, who he referred to as being part of the “Army of Heretics and Cranks, whose numbers and enthusiasm are extraordinary”, and who seem to believe in “magic” and some kind of “Utopia” (Keynes, 1930, vol. 2, p. 215)

I am no fan of Keynes. But it does seem he got that right.

Ironically, Lord Keynes (the blogger) found this paper ‘excellent’, and seems not to be able to spot the many differences between Werner’s theory and post-Keynesian’s (and ‘endogenous money’) views.

* For a single transaction, it may not even have to look for extra reserves if the funds are transferred to one of its own customers.

** There are also plenty of other reasons why this bank, a member of the German cooperative banking group, would not seek extra reserves. The operational arrangements of this group (and of the German savings banks group too) are very specific and relatively unique in the world. Werner’s whole experiment is thus flawed. His accounting analysis is also far from clear and seems to mix up reserves and money market claims on intragroup banks and other financial institutions.

Recent Comments