Frances Coppola on regulatory arbitrage

Frances Coppola recently wrote an interesting article on the origins of the financial crisis, which reflects several of the points that I have made on this blog time and time again: the crisis is the resulting product of the combination of regulatory arbitrage and interest rates below their natural level (as well as a few other things). I encourage you to read her article (which is at least necessary to follow my own post).

Yet I believe her story isn’t fully accurate. While US banks were subject to a leverage ratio, they were also subject to Basel 1 rules. As I have demonstrated, Basel 1 caused a surge in real estate and sovereign lending, and boosted the use of securitization, through regulatory arbitrage as Basel applied low risk-weights to those asset classes (for the most recent evidence, see here). Unlike what Hyun Song Shin believes, banks were already circumventing the ‘spirit’ of Basel 1 as soon as it was published in 1988… Basel 2 didn’t change much, and its implementation in Europe was anyway too late to have much of an influence on the crisis storyline (which had been building up since the late 1980s).

As a result, I don’t believe that, if European banks had been subject to a leverage ratio, they would not have been able to invest in American securitized products. They would still have done it, and perhaps sacrificed other type of lending or investments in other securities instead. Why? Because RMBSs and other CDOs offered higher yields for lower capital requirements, ceteris paribus. Risk-adjusted profit-maximising banks quickly figure it out.

She concludes:

The story of the financial crisis is a story of the failure of safe assets. That is why it was so traumatic. People expect to take losses on risky investments. They don’t expect to take losses on safe ones. Yet we are still trying to make the financial system “safer” and encourage investors to invest in “safe” assets. When will we learn that the safest investment is a risky one, and the most dangerous investments are those that are believed to be completely safe?

And it is also a warning of the consequences of regulatory arbitrage. The fact that the US and European banks had different regulatory regimes created a golden opportunity for unregulated institutions to exploit, with catastrophic consequences. Yet the US, the UK and the EU are still devising their own systems of regulation with scant regard for international consistency. When will we learn that an international industry requires international regulation?

I would say that the crisis wasn’t a failure of safe assets per se. It was a failure of regulation that wanted us (or actually, forced us) to believe that some assets were safe, creating a vicious spiral as banks piled into those asset classes to maximise their return on regulatory capital.

Moreover, regulatory arbitrage isn’t a cross-border issue. Most countries experienced the same symptoms: increasing real estate prices and securitization-issuance volumes, and lower sovereign debt yields. This points to intra-Basel distortions within countries, not to extra-Basel arbitrage across countries. Regulatory arbitrage-driven financial imbalances are endogenous to Basel regulations. Cross-border arbitrage, the Euro, populist politics (which never dies, as US politicians – incredibly – want to revive Fannie and Freddie…), also played a secondary (and surely exacerbating) role, but they were not at the very root of the crisis.

PS: Frances just published a new article on the ECB stress tests. I don’t disagree with her, but I believe that it is easy to criticise the test in hindsight, once we found out the number of banks that failed: she could have attacked the methodology at the time it was published. She also missed that, if banks don’t increase lending post-result announcements, it isn’t necessarily because they are zombies (some may well be). But the test was run on phased-in Basel 3 CET1 figures, not fully-loaded ones. Many banks still have large capital adjustments/deleveraging to make before complying with fully-loaded Basel 3 requirements, which isn’t going to help lending growth, especially given that banks currently don’t cover their cost of capital. (Another inconsistency of the test is that some banks were tested against fully-loaded ratios, and in the end obviously appeared uglier than if they had been tested against the same standards as other banks. If all banks had been tested against fully-loaded capital ratios, 36 would have failed)

The Economist on mobile payments and market liquidity

The Economist recently published an article on mobile payment, which is suspicious of its success to say the least:

The fragmentation [of mobile payment systems] confuses merchants and consumers, who have yet to see what is in it for them. From their perspective, the current system works well. Swiping a credit card is not much harder than tapping a phone. Nor is it too risky, especially in America, since credit cards are protected against fraud. Upgrading to a new system is a hassle. Merchants have to install new terminals. Consumers need to store their card details on their phones, but still carry their cards around, since most stores are not yet properly equipped.

I believe the newspaper is too pessimistic. Yes, swapping credit cards is easy. But then it involves signing a bill (not the fastest and most modern system ever) and the card can be replicated. Hence why most of the rest of the developed world has moved to a ‘chip and pin’ form of card payment, which is only slightly more burdensome (and not very fast either). The US is also taking the same direction.

Most people who have recently swapped their ‘chip and pin’ card for a contactless one can witness how convenient and quick the new system is. Yet, they also believed that the previous system “worked well”. Following the same argument, it would have been hard to convince people to switch to cards since carrying cash also “worked well” (ok, it’s not as strong an argument). Switching to smartphone-based contactless payment would make the system as fast, yet reduce the number of cards and devices one carries.

The Economist continues:

But even Apple’s magic may not be enough to make mobile payments fly. It is not clear how merchants will benefit from Apple’s new ecosystem: it does not offer them lower fees for processing payments or useful data about their customers, as CurrentC does. As a result, they may refuse to sign up for Apple Pay or discourage its use.

Yet, as described above, speed is mobile payment’s major asset. Any retailer regularly experiencing long queues is likely to lose customers. Contactless cards already speed up the checkout process considerably. Unfortunately, they are usually capped to pay small amounts (GBP20 in the UK). Contactless mobile payment/NFC systems would remove that cap.

In another article, The Economist once again highlights its ambivalent stance towards regulation:

But the illiquidity problem will still be there when the next crisis occurs. In a sense, it is a problem caused by regulators; they wanted banks to be less exposed to the vicissitudes of markets. But you cannot make risk disappear altogether; you can only shift it to another place. Get ready for more moments of sheer market terror.

The article refers to the recent market turbulence and points to regulatory requirements that have made lack of liquidity a rather new problem:

Due to new regulatory restrictions and capital rules that make bond-trading less profitable, banks have cut back their inventories to the level of 2002, even though the value of bonds outstanding has doubled since then (see chart).

That is a problem when trading surges, as it did between October 10th and 16th, when volumes rose by 67%. “Credit is not a continuously priced market,” says Richard Ryan of M&G Investments, a fund manager. “When a bond price falls from 100 to 90, it won’t do so smoothly, but in big drops.”

This is correct. Market-making (mostly fixed income) is becoming trickier because harsher capital requirements make it more expensive to carry a large inventory of bonds through three channels: 1. deleveraging, as banks are pushed towards higher regulatory capital ratios (and as the new leverage ratio is introduced), 2. credit risk, as credit risk-weights are on upward trend, 3. market risk, as holding larger inventories penalise banks through higher market RWAs than before. I may write a whole post on this topic soon.

But the newspaper forgets liquidity requirements: banks are required to hold enough very liquid assets on their balance sheet (‘liquidity coverage ratio’). Given the combination of leverage and liquidity constraints, banks have to sacrifice other asset classes: the riskier bonds. This leads to the following very good chart, from a Citigroup report and reported by Felix Salmon at Reuters:

This has been an issue with The Economist since the start of the crisis: the same newspaper declares that banks needs to be regulated and safer and complains about the negative effects of regulation at the same time. Perhaps time to be less contradictory?

PS: The ECB published its stress test results yesterday. I won’t comment on them. I just thought the AQR was an interesting exercise, but its consequences must be carefully weighted and it is crucial not to over-interpret them (I’ve already written about the danger of ‘harmonizing’ assessments across multiple jurisdictions and cultures).

Blurry banks’ future is

A lot of articles on financial innovation and disruption in the FT over the last few days. Here, John Gapper argues that tech firms aim at using the existing financial system rather than challenge it. Here, Martin Arnold argues that banks shouldn’t forget their traditional branch network as this is how they make money through their oldest and wealthiest clients. Here, Luke Johnson argues that crowdfunding is riskier but also more exciting and, in a way, is the future.

John Gapper is right to point out that the regulatory and capital costs of setting up new bank-alike lending entities are very high. Yet he probably overstates his case. P2P lenders do not provide bank-type services: technology has enabled disintermediation by allowing investors to lend money (almost) directly to borrowers, but the money invested is stuck and does not represent a means of payment, unlike bank deposits. P2P lenders have the ability to take over a large market share of the lending market; and their business model does not require a high operating, regulatory and capital costs base (at least for now…). This is where the traditional intermediated lending channel could effectively approach death. On the other hand, P2P lender cannot handle deposits and banks still have a near-monopoly in this area.

Of course, we could imagine a 100%-reserve banking world in which the lending channel has moved entirely to P2P lenders, mutual and hedge funds and equivalent, whereas the deposit and payment system has moved entirely to Paypal-like payment firms. And this excludes alternative options offered by cryptocurrencies. In this world, banks are effectively dead.

Still, I am far from sure this would be the best solution: banks provide an elastic supply of currency (fractional reserve banking) that can adapt to the demand for money. (We could imagine a world without banks but still an elastic currency supply, if for instance the whole money supply only comprised competing cryptocurrencies. Let’s say this is highly unlikely to happen in the foreseeable future)

Banks can also survive by benefiting from those technologies (if ever they dare touching their antique IT systems…). As I’ve been saying for a while, banks can leverage their huge customer base to set up their own P2P/crowdfunding platform. This has already started to happen: RBS just announced the creation of its own P2P lending platform, Santander announced a partnership with Funding Circle, Lending Club is developing partnerships with many US banks. Banks could earn a fee from referring customers to their own (or third-party) platform, while deleveraging and reducing their on-balance sheet credit risk. Investors would earn more on those investments than on time deposits, but bear some risk.

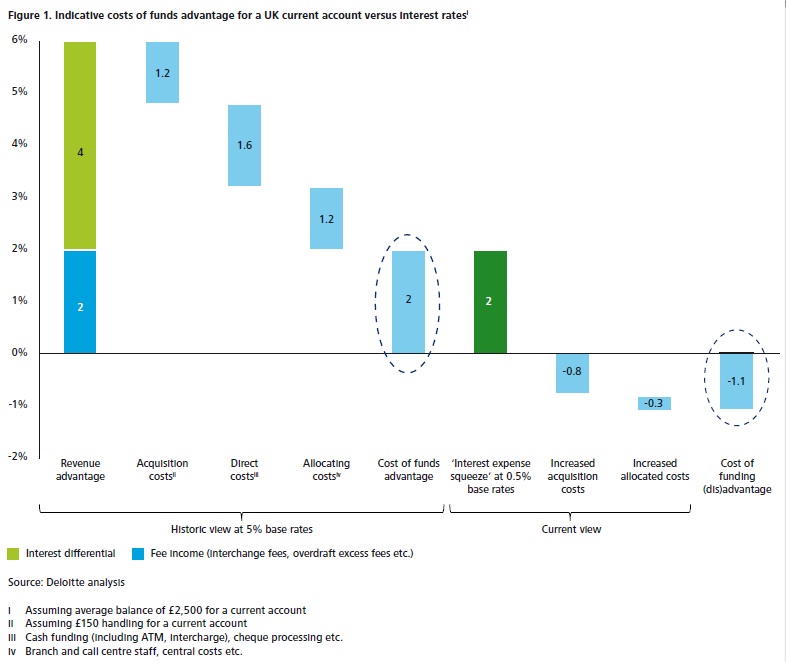

Whatever they decide to do, banks will have to adapt. But timing is key. Gapper referred to this recent, excellent, Deloitte report. They explain the margin compression effect (due to low base rates)*, which depresses banks’ profitability and adds another challenge on top of those that tech-enabled competitors and regulation already represent. According to them, closing down branches and moving online does not sufficiently slash cost to offset the decrease in net interest income. Closing down branches too quickly could also hurt banks by alienating the part of their client base born before the internet age. Deloitte provides evidence that a radical restructuring of IT systems could significantly improve returns, but this requires investments, which banks aren’t necessarily willing to undertake in a period of below-cost of capital RoE.

As the internet makes it easier for customers to compare pricing through aggregators and hence more difficult for banks to ‘extract value’ from them (what they call ’privileged access’), they recommend banks enhance ‘customer proposition’ (i.e. use ‘big data’) and focus on SME lending. As I’ve argued on this blog, capital regulation makes this difficult. They also indeed support the idea of in-house P2P platform, mostly to focus on local SMEs. This would help with capital requirements by maintaining SME exposures off-balance sheet, the risk borne by customers. Banks could effectively become risk assessment providers: rating lending opportunities to help customers (which include investment funds that don’t have such in-house capabilities) make their investment choices.

At the end of the day, banks are indeed likely to die if they don’t adapt. But also if they adapt too quickly. We could however see in the future surviving banks increasingly becoming like non-banks and non-banks increasingly providing banking services. The distinction between both types of institutions is likely to get very blurry. (That is, if regulation doesn’t kill non-banks first)

* Ben Southwood reiterated that interest rates are determined by markets and not by central banks. I already wrote responses to those claims here and here. Scott Sumner just mentioned his latest post, so I thought it would be a good idea to share Deloitte’s insight and own explanation of the margin compression effect and why “the spreads between Bank Rate and market rates seem to be narrow and fairly consistent—until they’re not.” In reality, lending spreads fluctuate only slightly when rates are above a certain threshold (i.e. banks’ risk-adjusted operating costs) and widen when they drop below it (explaining the “until they’re not”; see my previous posts). The fact that the “until they’re not” occurs does not imply that lending rates are “determined by the market”.

Here’s Deloitte own version:

The interest rate paid by banks on current accounts is typically lower than those paid for lump sum deposits (and the rates paid to borrow in the wholesale markets). However, this interest rate does not reflect the full cost of acquiring and servicing these current accounts. In the past, these acquisitions and servicing costs were offset by the fact that banks did not have to pay very high interest rates on current accounts.

Until the financial crisis, central bank interest rates (the ‘base rate’) were traditionally much higher. This meant that current account rates could easily be 500 or more basis points (hundredths of a percentage point) below lump-sum deposit rates.

Because base rates are at unprecedented lows, that maths does not work. Base rates have been low since 2009, and central bankers have signalled that they are likely to stay that way for some time yet. Figure 1 shows the economics of current accounts in the UK, where banks typically do not charge for them. A 200 basis point margin generated by current accounts when base rates are at 5 per cent turns into a 110 basis point loss at a 0.5 per cent base rate.

New research confirms the role of regulation and housing in modern business cycles

I think readers will find it hard to imagine how excited I was yesterday when I discovered (through an Amir Sufi piece in the FT) a brand new piece of research called: The Great Mortgaging: Housing Finance, Crises, and Business Cycles

(The authors, Jordà, Schularick and Taylor (JST), also published a free version here, and a summary on VOX)

I wish the authors had read my blog before writing their paper as it confirms many of my theses (unless they had?). It’s so interesting that I could almost quote two thirds of the paper here. I obviously encourage you to read it all and I will selectively copy and paste a few pieces below.

In my recent piece on updating the Austrian business cycle theory (ABCT), I pointed out that the nature of lending (and banks’ balance sheets) had changed over time since the 19th century (and particularly post-WW2), mainly due to banking regulation and government schemes. I had already provided a revealing post-WW2 chart for the US to demonstrate the effects of Basel 1 on business and real estate lending volumes.

JST went further. They went further back in time and gathered a dataset of disaggregated lending figures covering 17 developed countries over close to 140 years. Their conclusions confirm my views. Regulations – and in particular Basel – changed everything.

Here is their aggregate credit to GDP chart across all covered countries, to which I added the introduction of Basel 1 as well as pre-Basel trends:

I don’t think there is anything clearer than this chart (I’m not sure that securitized mortgages are included, in which case those figures are understated). Since the 1870s, non-mortgage lending had been the main vector of credit and money supply growth, and mortgage lending represented a relatively modest share of banks’ balance sheet. Basel turned this logic upside-down. How? I have already described the process countless times (risk-weights and capital regulation), so let see what JST say about it:

Over a period of 140 years the level of non-mortgage lending to GDP has risen by a factor of about 3, while mortgage lending to GDP has risen by a factor of 8, with a big surge in the last 40 years. Virtually the entire increase in the bank lending to GDP ratios in our sample of 17 advanced economies has been driven by the rapid rise in mortgage lending relative to output since the 1970s. […]

In addition to country-specific housing policies, international banking regulation also contributed to the growing attractiveness of mortgage lending from the perspective of the banks. The Basel Committee on Bank Supervision (BCBS) was founded in 1974 in reaction to the collapse of Herstatt Bank in Germany. The Committee served as a forum to discuss international harmonization of international banking regulation. Its work led to the 1988 Basle Accord (Basel I) that introduced minimum capital requirements and, importantly, different risk weights for assets on banks’ balance sheets. Loans secured by mortgages on residential properties only carried half the risk weight of loans to companies. This provided another incentive for banks to expand their mortgage business which could be run with higher leverage. As Figure 1 shows, a significant share of the global growth of mortgage lending occurred in recent years following the first Basel Accord.

I wish they had expanded on this topic and made the logical next step: Basel helped set up the largest financial crisis in our lifetime through regulatory arbitrage. Nevertheless, the implications are crystal clear.

To JST, this growth in real estate lending is the reason underlying our most recent financial crises:

We document the rising share of real estate lending (i.e., bank loans secured against real estate) in total bank credit and the declining share of unsecured credit to businesses and households. We also document long-run sectoral trends in lending to companies and households (albeit for a somewhat shorter time span), which suggest that the growth of finance has been closely linked to an explosion of mortgage lending to households in the last quarter of the 20th century. […]

Since WWII, it is only the aftermaths of mortgage booms that are marked by deeper recessions and slower recoveries. This is true both in normal cycles and those associated with financial crises. […]

The type of credit does seem to matter, and we find evidence that the changing nature of financial intermediation has shifted the locus of crisis risks increasingly toward real estate lending cycles. Whereas in the pre-WWII period mortgage lending is not statistically significant, either individually or when used jointly with unsecured credit, it becomes highly significant as a crisis predictor in the post-WWII period.

JST confirm what I was describing in my post on updating the ABCT: that is, that banks don’t play the same role as in early 20th century, when the theory was first outlined:

The intermediation of household savings for productive investment in the business sector—the standard textbook role of the financial sector—constitutes only a minor share of the business of banking today, even though it was a central part of that business in the 19th and early 20th centuries.

JST describe the post-WW2 changes in mortgage lending originally as a result of government schemes to favour home building and ownership, followed by international regulatory arrangements (Basel) from the 1980s onward. Those measures and rules led to a massive restructuring of banks’ balance sheet, as demonstrated by this chart:

While the empirical findings of this paper will be of no surprise to readers of this blog, this research paper deserves praise: its data gathering and empirical analysis are simply brilliant, and it at last offers us the opportunity to make other mainstream academics and regulators aware of the damages their ideas and policies have made to our economy over the past decades. It also puts the idea of ‘secular stagnation’ into perspective: our societies are condemned to stagnate if regulatory arbitrage starve our productive businesses of funds and the only way to generate wealth is through housing bubbles.

While the empirical findings of this paper will be of no surprise to readers of this blog, this research paper deserves praise: its data gathering and empirical analysis are simply brilliant, and it at last offers us the opportunity to make other mainstream academics and regulators aware of the damages their ideas and policies have made to our economy over the past decades. It also puts the idea of ‘secular stagnation’ into perspective: our societies are condemned to stagnate if regulatory arbitrage starve our productive businesses of funds and the only way to generate wealth is through housing bubbles.

China’s Frankenstein banking system keeps growing

Financial regulation in China is quite a mess. China seems to be the world testing ground for some of the most ridiculous banking rules. With all their related unexpected consequences.

Take this recent story: some time ago, Chinese regulators found it clever to cap Chinese banks’ loans/deposits ratios at 75% by the end of each quarter (it isn’t). The goal was to ensure that banks have enough liquidity to face large cash withdrawals. Nevermind that loans/deposits only take into account loans from the asset side of the balance sheet and that banks can use depositors cash to invest in many different sorts of assets (from liquid sovereign bonds and short-term repos to very illiquid securities). Perhaps Chinese banking rules forbid some of those investments (I am not an expert on the Chinese banking system). The fact that the rule was only enforced at quarter-end seemed not to be a problem either (arbitrage anyone?), or that the news that a bank hadn’t complied with the rule could trigger a panic.

Nevertheless, as usual with China, the spontaneous financial order reacts. As the FT reports:

In recent years, the final few days of each quarter have become a nervous time for banks. As liquidity has tightened and many depositors have shifted their savings into higher-yielding substitutes such as Alibaba’s online money-market fund, Yu’E Bao, many lenders have struggled to attract enough traditional deposits to stay below the maximum 75 per cent loan-to-deposit ratio.

That regulation, intended to ensure banks keep enough cash on hand to meet withdrawal demand, is enforced at the end of each quarter – providing an incentive to window-dress deposit totals. This was exacerbated by the desire to prettify quarterly reports to shareholders.

To meet the deposit challenge, many banks resorted to an all-hands-on-deck approach, requiring employees to meet a deposit target. That meant urging clients – and even family and friends – to transfer funds into the bank, typically only for a few days covering the quarter-end period.

Typical example of a rule that, not only introduces opacity, but also creates unintended consequences.

But the story isn’t over.

Chinese regulators didn’t really appreciate that bankers were trying to bypass their well-thought-out rule. They came up with another very ‘clever’ rule to fix the flawed rule:

Regulators will suspend business approvals to banks whose month-end deposit total deviates by more than 3 per cent from the daily average over the previous month.

Problem solved. Not.

To the uncertainty and unintended consequences of the previous rule, they added further uncertainty and unintended consequences. Nevermind that such a rule would limit competition for deposits (Chinese banks are for now forbidden to compete on price – this is about to change –, but can well use other means and advantages). A larger deposit inflow could well happen for any reason (run on a competitor, or simply good news about the financial strength of a bank leading to an inflow of new customers). Penalising banks for such reason sounds rather dubious to say the least.

One of the consequences is that banks now turn away deposits…

The rule can also easily trigger instability, as the FT adds:

A light-hearted commentary circulated among bankers on social media on Wednesday, carrying the headline “If there’s a bank you hate, send them all your money before 12 tonight”.

I’m sure Chinese people, with their usual banking rule-avoiding ingenuity, will soon enough find a way to use all the loopholes created by this combination of definitely very clever regulations. And that regulators, in turn, will come up with another rule to patch the rule that patched the rule. The Frankenstein experiment continues.

MC Klein and central bankers struggle to understand banking mechanics

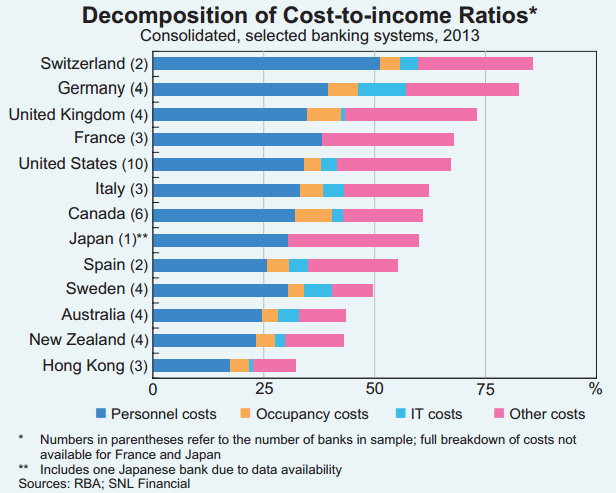

I recently pointed out that many central bankers actually did not understand banks’ internal mechanics. We now have further evidence. In an FT Alphaville blog post, Matthew Klein quoted a recent report from the Reserve Bank of Australia, which usefully compared banking metrics across countries.

MCK points out that Australian banks have some of the lowest cost/income ratios in the world, whereas Swiss, German and British banks have some of the highest ones. According to the report, the difference mostly comes from the lower income paid to Australian bankers, which (apparently) originates in the ‘simplicity’ of Australian banks, whose investment banking activities are relatively small.

Indeed, as the following chart demonstrates, Australian banks do generate a larger share of their revenues from net interest income than banks in other countries. MCK concludes:

In other words, the more a bank focuses on taking in deposits and making loans to households and businesses, the cheaper it is to run and the less money its employees make.

And he then quotes the Australian central bank:

The Australian major banks’ focus on commercial banking – that is, lending to households and businesses – appears to be a contributor to their relatively low CI ratio. In 2013, those large banks that earned a greater share of their income from net interest income (a proxy for a bank’s focus on lending activities) tended to have lower CI ratios than ‘universal’ banks, which earned a larger share of their income through non-interest sources such as investment banking or wealth management.

The above analysis suggests that there may be diseconomies of scope for some large banks – that is, average costs increase as they diversify outside of commercial banking services. This is consistent with some literature which points to negative returns to scope when banks move into market-based activities. While market-based activities can provide a more diversified revenue stream for banks, they are typically a more volatile source of income and can expose banks to additional risks and complexity.

As simple as that.

But… wait. Are things really that simple?

Let’s take a look at some of the largest banks’ reported segmental cost/income ratios in 2013*. The segments in bold are the ones that include ‘simple’ retail banking:

- UBS: its reported segmental cost/income ratios were the following in 2013: Wealth Management 70%, Wealth Management Americas 87%, Retail & Corporate 61%, Global Asset Management 70%, Investment Bank 73%

- Credit Suisse: Wealth Management 75%, Corporate & Institutionals 51%, Asset Management 69%, Investment Banking 71%

- Deutsche Bank: Corporate Banking & Securities 76%, Global Transaction Banking 65%, Asset & Wealth Management 83%, Private & Business Clients 76%

- Commerzbank: Private Customers 90%, Mittlestandbank 46%, Central & Eastern Europe 54%, Corporates & Markets 65%, Non-Core Assets 98%

- Barclays: UK RBB 67%, Barclaycard 43%, Africa RBB 71%, Europe RBB 126%, Wealth 87%, Investment Bank 72%, Corporate 58%

It is really not clear that straightforward retail banking boasts low cost/incomes. And if one thing is clear, it is that, even in their retail banking divisions, banks in Europe do not boast the same sort of cost/income as in Australia, far from that. Around 20 percentage points higher in fact. Small, retail-only, European banks’ cost/income ratios also reach the 60 to 75% level.

Perhaps the complexity/simple story isn’t that straightforward after all.

While it is true that investment banking, in theory, can lead to higher cost/income ratios (as can private banking), and that banking systems that rely on such activities inherently have bigger cost bases, this does not mean that those banking systems are necessarily unprofitable. Switzerland for instance has a very large number of private banks. The private banking business model leads to high level of costs… and low level of risk. In a bank’s income statement, loan impairment charges follow operating costs. A bank whose asset quality is low needs the financial flexibility to absorb losses on its loan portfolio. Hence the importance of a low cost/income. Many emerging markets banks indeed have low cost/income ratios.

That was the first point: cost/income by itself doesn’t mean much.

Second point is… by focusing on the cost side of the equation, both MCK and the Australian central bankers forgot the income side.

The income side comprises net interest income. This net interest income is partly dependent on the level of interest rates. When rates are set at a low level by central banks, margin compression appears. I have already described this phenomenon here. Unfortunately this concept seems to be foreign to most people.

Banks in the UK and Europe have been suffering from margin compression for many years, as interest rates have dropped near their zero lower bound, leading lending rates to fall while (deposit) funding rates were already stuck at the bottom. Many banks in the UK and the Eurozone now only have net interest margins of 1% or less. When margins are low, net interest income suffers and accounts for a lower share of total income.

What happened in Australia in the meantime? Well, interest rates are now at a record low of…2.5%. What are banks’ net interest margins? 2% to 2.25%… Given how strong those margins are, it is natural that Australian banks will also boast higher net interest incomes, and in turn higher incomes and lower cost/income ratios…

We now have a more comprehensive answer than the ‘simple’ (if not simplistic) explanation offered in this FT Alphaville column: low rates are partly responsible for European and American banks’ high cost/income ratio. ‘Complexity’, on the other hand, is an easy and convenient target for regulators. It fits the story they’ve been trying to sell since the crisis. Facts, unfortunately, are a little more stubborn.

* Segments aren’t fully comparable. Some include corporate/SME lending or wealth management, others not. Some one-offs could distort some of the figures somewhat. I didn’t correct for that. Some banks already exclude them from their reported segmental cost/income or include them in ‘non-core’ or ‘non-strategic’ units.

Why the Austrian business cycle theory needs an update

I have been thinking about this topic for a little while, even though it might be controversial in some circles. By providing me with a recent paper empirically testing the ABCT, Ben Southwood, from ASI, unconsciously forced my hand.

I really do believe that a lot more work must be done on the ABCT to convince the broader public of its validity. This does not necessarily mean proving it empirically, which is always going to be hard given the lack of appropriate disaggregated data and the difficulty of disentangling other variables.

However, what it does mean is that the theoretical foundations of the ABCT must be complemented. The ABCT is an old theory, originally devised by Mises a century ago and to which Hayek provided a major update around two decades later. The ABCT explains how an ‘unnatural’ expansion of credit (and hence the money supply) by the banking system brings about unsustainable distortions in the intertemporal structure of production by lowering the interest rate below its Wicksellian natural level. As a result, the theory is fully reliant on the mechanics of the banking sector.

The theory is fundamentally sound, but its current narrative describes what would happen in a relatively free market with a relatively free banking system. At the time of Mises and Hayek, the banking system indeed was subject to much lighter regulations than it is now and operated differently: banks’ primary credit channel was commercial loans to corporations. The Mises/Hayek narrative of the ABCT perfectly illustrates what happens to the economy in such circumstances. Following WW2, the channel changed: initiative to encourage home building and ownership resulted in banks’ lending approximately split between retail/mortgage lending and commercial lending. Over time, retail lending developed further to include an increasingly larger share of consumer and credit card loans.

Then came Basel. When Basel 1 banking regulations were passed in 1988, lending channels completely changed (see the chart below, which I have now used several times given its significance). Basel encouraged banks’ real estate lending activities and discouraged banks’ commercial lending ones. This has obvious impacts on the flow of loanable funds and on the interest rate charged to various types of customers.

In the meantime, banking regulations have multiplied, affecting almost all sort of banking activities, sometimes fundamentally altering banks’ behaviour. Yet the ABCT narrative has roughly remained the same. Some economists, such as Garrison, have come up with extra details on the traditional ABCT story. Others, such as Horwitz, have mixed the ABCT with Yeager’s monetary disequilibrium theory (which is rejected by some other Austrian economists).

While those pieces of academic work, which make the ABCT a more comprehensive theory, are welcome, I argue here that this is not enough, and that, if the ABCT is to convince outside of Austrian circles, it also needs more practical, down to Earth-type descriptions. Indeed, what happens to the distortions in the structures of production when lending channels are influenced by regulations? This requires one to get their hands dirty in order to tweak the original narrative of the theory to apply it to temporary conditions. Yet this is necessary.

Take the paper mentioned at the beginning of this post. The authors find “little empirical support for the Austrian business cycle theory.” The paper is interesting but misguided and doesn’t disprove anything. Putting aside its other weaknesses (see a critique at the bottom of this post*), the paper observes changes in prices and industrial production following changes in the differential between the market rate of interest and their estimate of the natural rate. The authors find no statistically significant relationship.

Wait a minute. What did we just describe above? That lending channels had been altered by regulation and political incentives over the past decades. What data does the paper rely on? 1972 to 2011 aggregate data. As a result, the paper applies the wrong ABCT narrative to its dataset. Given that lending to corporations has been depressed since the introduction of Basel, it is evident that widening Wicksellian differentials won’t affect industrial structures of production that much. Since regulation favour a mortgage channel of credit and money creation, this is where they should have looked.

But if they did use the traditional ABCT narrative, it is because no real alternative was available. I have tried to introduce an RWA-based ABCT to account for the effects of regulatory capital regulation on the economy. My approach might be flawed or incomplete, but I think it goes in the right direction. Now that the ABCT benefits from a solid story in a mostly unhampered market, one of the current challenges for Austrian academics is to tweak it to account for temporary regulatory-incentivised banking behaviour, from capital and liquidity regulations to collateral rules. This is dirty work. But imperative.

Major update here: new research seems to confirm much of what I’ve been saying about RWAs and the changing nature of financial intermediation.

* I have already described above the issue with the traditional description of the ABCT in this paper, as well as the dataset used. But there are other mistakes (which also concern the paper they rely on, available here):

– It still uses aggregate prices and production data (albeit more granular): the ABCT talks about malinvestments, not necessarily of overinvestment. The (traditional) ABCT does not imply a general increase in demand across all sectors and products. Meaning some lines of production could see demand surge whereas other could see demand fall. Those movements can offset each other and are not necessarily reflected in the data used by this study.

– It seems to consider that aggregate price increases are a necessary feature of the ABCT. But inflation can be hidden. The ABCT relies on changes in relative prices. Moreover, as the structure of production becomes more productive, price per unit should fall, not increase.

Kupiec on central banking/planning

In the WSJ a couple of days ago, Paul Kupiec wrote an article that looks so similar to my blog that I had to quote it here.

Macroprudential regulation, macro-pru for short, is the newest regulatory fad. It refers to policies that raise and lower regulatory requirements for financial institutions in an attempt to control their lending to prevent financial bubbles. […]

There is also the very real risk that macroprudential regulators will misjudge the market. Banks must cover their costs to stay in business, and in the end bank customers will pay the cost banks incur to comply with regulatory adjustments, regardless of their merit. By the way, when was the last time regulators correctly saw a coming crisis?

He concludes with:

With Mr. Fischer now heading the Fed’s new financial stability committee, might we soon see regulations requiring product-specific minimum interest rates? Or maybe rules that single out new loan products and set maximum loan maturities and debt-to-income limits to stop banks from lending on activities the Fed decides are too “risky”? None of these worries is an unimaginable stretch.

Since the 2008 financial crisis, U.S. bank regulators have put in place new supervisory rules that limit banks’ ability to make specific types of loans in the so-called leverage-lending market—loans to lower-rated corporations—and for home mortgages. Since there is no scientific means to definitively identify bubbles before they break, the list of specific lending activities that could be construed as “potentially systemic” is only limited by the imagination of financial regulators.

Few if any centrally planned economies have provided their citizens with a standard of living equal to the standard achieved in market economies. Unfortunately the financial crisis has shaken belief in the benefits of allowing markets to work. Instead we seem to have adopted a blind faith in the risk-management and credit-allocation skills of a few central bank officials.

Government regulators are no better than private investors at predicting which individual investments are justified and which are folly. The cost of macroprudential regulation in the name of financial stability is almost certainly even slower economic growth than the anemic recovery has so far yielded.

This is very good, and I can’t agree more.

He points to his own research on macro-prudential policies. In a paper published in June 2014, Kupiec, Lee and Rosenfeld declare that

Compared to the magnitude of loan growth effects attributable to [increase in supervisory scrutiny or losses on loan/securities], the strength of macroprudential capital and liquidity effects are weak. This data suggest that traditional monetary policy (lowering banks’ cost of funding) is likely to be a much more potent tool for stimulating bank loan growth following widespread bank losses than modifying regulatory capital or liquidity requirements.

(note: they also say that the opposite logic applies)

While it doesn’t mean that they are wrong, I am not fully convinced by their arguments, especially given the dataset they base their analysis on (an economic and credit boom period, with less than tight monetary policy and many variables that could have been distorted as a result). In another paper, Aiyar, Calomiris and Wieladek point to the fact that macro-prudential policy can be effective at reducing banks’ lending, but that alternative sources of credit (i.e. shadow banking) grow as a result (they say that macro-prudential policies ‘leak’).

What is clear is that the effects of macro-prudential policies are unclear. What is also clear is that, whatever the effects of those policies, none are necessarily desirable. If macropru is indeed effective, then the resulting distorted capital allocation may be harmful. If macropru isn’t effective, then it may lead central bankers to (wrongly) believe they can maintain interest rates below/above their natural level while controlling the collateral damages this creates. In both cases the economy ends up suffering.

Recent Comments