TLTRO, a predictable failure

Almost a year and a half ago, I predicted the failure of the ECB’s TLTRO measure:

Finally, the ECB has launched its own-FLS style ‘TLTRO’, a scheme that provides cheap funding to banks if they channel the funds to businesses. Similarly to the BoE’s FLS, I believe such scheme suffers from delusion. Banks are currently deleveraging to lower their RWAs in order to comply with the harsher capital requirements of Basel 3. If there is one thing banks want to avoid, it is to lend to RWA-dense customers such as SMEs… (and instead focus on better RWA/risk-adjusted profitable lending such as… mortgages). Banks can also already extract relatively low wholesale funding rates by issuing secured funding instruments such as covered bonds.

Now Fitch, the rating agency, just published a piece confirming that the TLTRO effects were ‘modest’ at best. I don’t have access to their whole report, but the FT, commenting on the same piece of research, reported that:

A total of €400bn has been injected into the banking system through five TLTRO auctions since September 2014, with demand predominantly from Spanish and Italian institutions. By contrast, bank corporate lending grew by just €4bn between September 2014 and August 2015.

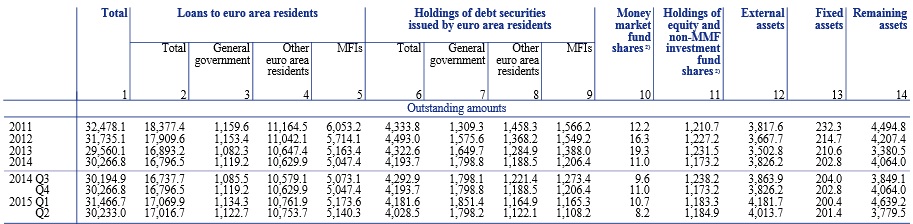

Now compares this €4bn with stats from the ECB (see table below) that show that total lending grew by €279bn in the Eurozone over the same time period, of which €175bn was extended to non-financial private individuals and businesses.

Fitch reports that corporate lending grew in a few northern European countries, and that lack of demand is likely a cause of the slow lending growth across most Eurozone countries. While there is definitely some truth to this, we have to keep in mind that the causation in this case may well go the other way around: demand may be low because rates on business loans are too high to justify borrowing.

TLTRO (as well as the British FLS) is a prime example of how deluded central bankers and policymakers are if they expect monetary policy and unconventional bank funding measures to bypass the negative effects that banking regulation has at the microeconomic level on the banking channel of monetary policy. Throw in as much stimulus as you wish, the money will always flow towards points of the economic system where micro resistance is the weakest. And, that is, money will flow to low-RWA asset classes (ahem…mortgages…ahem).

PS: I really have little time for blogging at the moment. Doing what I can to post updates!

Will Switzerland reveal the lower bound?

Given that a number of central banks have moved some of their monetary policy tools into negative territory for the first time in their history, many people have questioned the assumption that the zero lower bound is effectively the lower bound that conventional economic theory describes. However, most economists do think that the lower bound exists; it is simply negative (as storing cash also involves a cost) and nobody really knows what its precise level is.

Hence the interesting experiment now happening in Switzerland, which seems to provide us with some indications. The SNB target range has now been in negative territory for a little while, and demand deposits at the central bank are currently charged a negative rate of 0.75%:

This is causing some issues for Swiss banks, in particular those that don’t have any international presence. SNL (link) reports that overall Swiss net interest income is declining by 6% this year and net interest margin is down from 1.8% in 2007 to less than 1.3% in 2014. Including the two largest and international Swiss lenders, NIM drops to 60pb, lower than in Japan. Between 2013 and 2015, NIM is forecasted to fall by 11%. Unsurprisingly, profitability is low. Add the harsh Swiss banking regulation and SNL now calls Swiss banks ‘low-return low-risk utilities’. This is a typical effect of the margin compression effect I keep mentioning on this blog.

Evidently, many Swiss banks are private entities that don’t really enjoy this situation. First, despite the lowest interest rates ever, banks have increased rates on mortgages; a phenomenon I had predicted in a margin compression period (see my discussion with Ben Southwood, who believes that competitive pressure cannot allow banks to raise rates). Second, a number of Swiss banks have been charging negative rates on large corporate deposits for several months already. Recently. a small Swiss bank revealed it would charge 0.125% on slightly less than a third of its clients’ accounts.

SNL reports that a large pension fund attempted to withdraw physical cash earlier in the year. Attempt that failed. But there is apparently growing demand for safe deposit boxes in the country, although demand remains limited as negative rates are only charged on corporate, and now some large retail, deposits.

While those are early signs, they remain important signs that we are getting closer to the actual lower bound. Various types of customers can also have different lower bound tolerance, and small retail depositors, for now unconcerned by negative rates, may be less tolerant of such charges. Once negative rates generalise, we’ll find out how deep the lower bound really is.

Central bankers, who believe they can stabilise the economy by imposing negative rates, might well endanger it in reality. If negative rates generalise, the banking sector will be weakened: not only its profitability will get depressed (and you need a healthy banking system to extend credit for productive purposes), but also its funding structure will become much more unstable. Indeed, depositors will be more likely to withdraw their deposits and avoid getting locked in longer maturity saving products, exacerbating banks’ maturity mismatches. Eventually, the net effect of negative rates might not be that positive.

PS: I’d like to know what the proponents of ‘the Wicksellian natural rate of interest is negative because of our depressed economy’ think in the case of Switzerland. Its economy doesn’t look particularly under stress, yet it is imposed negative rates by its central bank to control FX fluctuations. George Selgin also has a nice post on deflation in Switzerland, which, unlike conventional wisdom, doesn’t seem to be damaging.

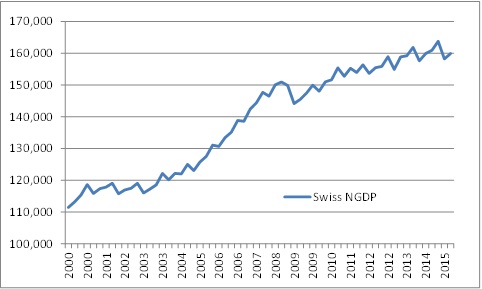

This is the quarterly Swiss NGDP since 2000, extracted from the SNB website:

Note that the post-crisis NGDP trend has not caught up with pre-crisis trend. Very far from that (also note that the growth trend changed twice over the past 15 years). I suspect that some would advocate a much larger SNB stimulus to cause inflation to get NGDP back on track (but on which track?). Despite this ‘output gap’, the Swiss economy seems to be relatively healthy, at least for European standards.

PPS: an analyst, interviewed by SNL on the topic of the abolition of cash cherished by Kimball or Buiter, perfectly answered:

“That,” said Maier, “would be my definition of hell.”

Wicksell is hiding; the real estate boom isn’t

The Wicksellian natural rate of interest remains an economic mystery. No one knows what its level is. That wouldn’t be a problem if no one tried to emulate (or voluntarily tried to manipulate it downward or upward), that is, if we had a free market for money. But we don’t and a number of central banks attempt to estimate what this interest rate is so they can play with their own monetary policy tools.

Problem is, no one has a proper definition, and we often hear about a ‘neutral’ rate of interest, or a ‘natural’ rate that would maintain CPI stable or on a stable growth trend, and/or a rate that would be consistent with ‘full employment’ or that would allow GDP growth in line with an often ill-defined ‘potential output’. This is all very confusing, and doesn’t seem to accurately represent what Wicksell originally called the ‘natural rate of interest’, that is, the rate whose level would not affect ‘commodity prices’ and is similar to the rate of interest of a money free world (see Interest and Prices). Some believe the natural rate to be relatively stable; others believe it to fluctuate in line with business cycles. This Bruegel post sums up quite well the differing views that a number of current economists hold.

A common view today is that the natural rate has turned negative in most of the Western world since the financial crisis. It’s a view held by a wide range of economists, from Keynesians to Market Monetarists. Scott Sumner believes that the rate is firmly negative (David Beckworth too, and he denies that central banks affect interest rates – see also my response to Ben Southwood on the same topic) because

Since 2008, the inflation rate has usually been below the Fed’s 2% target, and if you add in employment (part of their dual mandate) they’ve consistently fallen short. This means that money has been too tight, i.e. the actual interest rate has clearly been above the Wicksellian equilibrium rate.

He is therefore surprised by a new piece of research by two Richmond Fed economists, who came up with very different conclusions.

First, they remind us of an estimate of the natural rate made by Laubach and Williams, which shows the nominal rate to have fallen into negative territory since the crisis, but also that the real rate is too loose:

Using a different methodology, which they believe more accurately reflects Wicksell’s original vision, the authors estimate the natural rate of interest to be higher than that estimated by LW. They also point out that it never turns negative.

This demonstrates how tricky it can be to estimate this rate (see their lower/upper bound estimates…), and how easily central bankers could make policy mistakes as a result. (See also estimates from Thomas Aubrey’s methodology, i.e. ‘Wicksellian differential’)

Interestingly, all Fed economists above estimate the natural rate to be below the real money rate of interest from around 1994 to 2002, that is, money was too tight during the period. Thomas Aubrey, by contrast, finds the opposite result, with a positive Wicksellian differential over the period, meaning that money was too loose. Similarly, Anthony Evans writes on Kaleidic Economics that his own estimate of the UK natural rate is 2.3%; much higher than the current BoE rate.

If the Fed economists are right, it means that the classic Austrian Business Cycle theory (i.e. malinvestments originating in economic discoordination due to money rate of interest below the natural rate) cannot apply to most of the two decades preceding the crisis (it can in the case of Aubrey’s theory however).

As some readers already know, malinvestments and economic discoordination can still happen independently of the level of the risk-free natural rate of interest. This is what I theorised in my RWA-based ABCT: Basel banking regulations add another layer of distortion to the credit allocation process.

Where it gets scary is that, according to the same Fed economists, the current monetary policy stance is too loose. I find it hard to understand the outright dismissal of those estimates by a number of economic commentators and professors. Some commenters on Sumner’s post don’t even try to discuss the theoretical basis of this Richmond Fed paper. They see some sort of conspiracy or whatever. Not really the highest sort of intellectual debate to say the least. When some ‘evidence’ seems to challenge your theoretical framework, don’t dismiss it outright. Address it.

Personally, I have repeated a number of times that I find it hard to believe that our recent economic woes were so severe that they led to a market clearing, natural, Wicksellian rate below zero for the first time in the history of mankind. I have also tried to show elsewhere that a free banking system would be highly unlikely to drop rates below the zero-lower bound.

Now, if the estimates highlighted above are right, I fear possibly huge distortions in the real estate market. Let’s define a simplified free-market mortgage interest rate as

MR = RFR + IP + CRP – C,

where MR is the mortgage rate, RFR is the applicable, same maturity, risk-free rate, IP the expected inflation premium, CRP the credit risk premium that applies to that particular customer and C the protection provided by the collateral (that is, house value, with lower LTV loans leading to higher C).

Ceteris paribus, if the RFR is pushed downward, MR goes down, likely stimulating the demand for real estate credit. But this can also apply to all sort of lending. Enter Basel.

In a Basel world, the favourable capital treatment of such loans increases the supply of loanable funds towards the real estate sector. MR is pushed down even further, leading to an increase in demand for mortgages, in turn pushing house prices up, which raises the value of collateral C, which lowers MR further. It’s a virtuous (or rather vicious) circle. On the other hand, the stimulating effect of the lower RFR applied to SME lending gets ‘suppressed’ by the reduced supply of loanable funds for that type of credit. (and there are many other impacts on the RFR emanating from Basel)

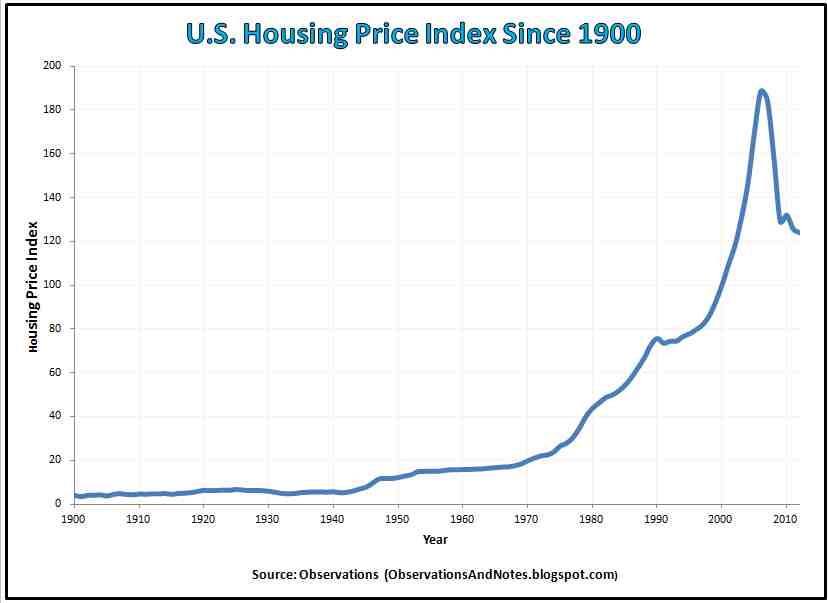

I warned more than two years ago that this situation would continue. And this is precisely what has been happening. While the media complain on a weekly basis that SMEs are starved of bank credit and turn to alternative lenders (while regulators attempt to revive the market for securitised corporate loans), the Economist reports that housing markets are either strongly recovering or even way overvalued in most advanced economies. This sort of continuous and rapid house prices booms and busts was unknown in history before the 80s/90s (see also here).

It is unclear what the exact contribution of low risk-free rates is, relative to Basel’s. What is certain is that, if Richmond Fed economists are right, we’re in for another housing disaster as Basel’s effects get amplified by monetary policy (which doesn’t necessarily imply that the effects would be similar to those of the 2008/9 crisis, although historical evidence shows that housing bubble are the most damaging types of ‘bubbles’).

Hillary Clinton gets everything wrong about banking

In a column published last Friday on Bloomberg, Hillary Clinton is trying to build her credentials for the US presidential election. Sadly, her quite populist tone is let down by the quality of her arguments and the accuracy of her facts.

Let’s deconstruct her piece step by step.

She starts with a comment that could be interpreted as ironic if it were not in fact serious:

Before the crisis hit, as a senator from New York, I was alarmed by this gathering storm, and called for addressing the risks of derivatives, cracking down on abusive subprime mortgages and improving financial oversight. Unfortunately, the Bush administration and Republicans in Congress largely ignored calls for reform.

Interestingly ‘abusive subprime mortgages’ were in fact first pushed by the…..Clinton administration in 1990s (and then continued under Bush), and banks were literally forced to maintain a quota of such mortgages to obtain various regulatory approvals (including merging with other banks, during the consolidation period that followed the end of interstate banking restriction). This whole very political process was clearly outlined and very well documented in Calomiris and Haber’s Fragile by Design (see my review here).

But don’t get my word (or Calomiris and Haber’s) for it. See this 1999 NYT article, a newspaper that hardly qualifies as banking and free market lover (my emphasis):

Fannie Mae, the nation’s biggest underwriter of home mortgages, has been under increasing pressure from the Clinton Administration to expand mortgage loans among low and moderate income people and felt pressure from stock holders to maintain its phenomenal growth in profits.

When politics trumps economics. (and then blames ‘irrational’ economic actors for the catastrophic outcome)

She later attacks high-frequency trading and shadow banking (she wants more ‘oversight’ – how? – and she forgets that regulators still have no idea how to follow a continuously morphing shadow banking sector), apparently without realising that HFT and shadow banking were reactions to government regulations (the so-called Reg NMS in the case of HFT) and not free market creatures.

Clinton wants to ‘rein in the complexity and riskiness’ of financial institutions. Good. Surely this means getting rid of the tens of thousands pages of complex rules that banks have had to accommodate and that fundamentally reshaped their business model? No, she actually means adding another layer of rules, as she seems to consider Dodd-Frank as ineffective (how ironic).

Consequently, she wishes to reinstate the Glass-Steagall act (which was repealed under her husband’s watch) (and strengthen the Volcker rule – how?), even though there is now no real clear boundary between commercial and investment banking (hence why it was repealed: when the small business, to which you just extended credit to purchase inventory from abroad, seeks to hedge its future expenses by entering into an FX derivative contract with you, or simply when you lent in another currency and wish to hedge FX fluctuations, well, you need a trading book and trading counterparties to take the other side of the trades…).

But Glass-Steagall just misses the whole point: the financial crisis wasn’t an investment banking crisis; it was originally a plain vanilla mortgage lending crisis. Many banks that had no real IB activity suffered or collapsed due to the bad loans they are extended or the fall in value of the securitised products based on bad quality mortgages they had purchased. In short, IB wasn’t the root cause of the crisis.

Where it gets really dangerous is when she wants to give regulators even more authority and power than they already have. The opacity and the lack of respect for the rule of law is already a characteristic of our regulatory system. More discretion is not welcome unless we wish to build a world led by all-powerful but flawed economic administrators that need to get ‘pleased’ if one desires to avoid negative consequences. This would be the end of the Law, and the end of economic efficiency. And this is what happens in a number of developing countries that struggle to develop the sort of solid institutional framework and rules that would allow them to finally thrive. And this is what Clinton is suggesting.

As usual with such wishful political thinking, it ignores all public choice issues: give them all powers, and they’ll work for the greater good:

We need to find the best, most independent-minded people for these important regulatory jobs — people who will put consumers and everyday investors ahead of the industries and institutions they’re supposed to oversee.

Regulatory capture? Personal utility maximisation? Human ignorance/lack of omniscience? Unknown concepts. As Milton Friedman adequately remarked: “and where in the world do you find these angels who are going to organise society for us?”

The only thing I agree with is that financial crimes/frauds should be punished, although in order to respect the rule of law, financial services employees should be judged on the same basis as the employees of any other sector.

Granted, she’s a politician in campaign and not a banking/economic expert. But a more moderate tone and a little more fact-checking would help the US economy more in the long-run than vengeful finger-pointing that will only result in more distrust.

The inherent contradiction of regulation exposed (again)

A few weeks ago, Reuters reported that a new research report (I can’t seem to find the original paper, which is still a work in progress) published by two German academics (Wolfgang Gick and Thilo Pausch) recommended that bank supervisors “withhold some information when they publish stress test results to prevent both bank runs and excessive risk taking by lenders”.

I have pointed out multiple times that this was an intrinsic problem to bank regulation, and that Bagehot had correctly identified the issue already in his time. Our societies have, since then, tried to conveniently forget Bagehot’s wise remarks.

Reuters continues:

If depositors know from the watchdog that banks are in trouble, they will withdraw their cash, threatening lenders’ survival and causing the panic the supervisor is trying to avoid, the paper said.

Exactly. And wholesale markets are even more at risk. The authors then recommend that “the amount of information disclosed by supervisors should decrease the more vulnerable the banking sector is expected to be.” Is this going to correct the problem? Evidently not. As the public starts to understand that ‘less information about a given bank’ equals ‘riskier bank’, withholding information from the public domain will become self-defeating.

The authors also correctly highlight that

giving banks a clean bill of health also carries risks, according to Gick and Pausch, by encouraging depositors to leave their money in banks. That would undermine market discipline and lead lenders to take excessive risks, they wrote.

In the end, whatever regulators do, negative consequences follow.

Another contradiction was exposed last month when Ewald Nowotny, Governor of the Austrian central bank, warned that proposed changes to the Basel regulatory regime were “dangerous” because borrowing “could become harder for SMEs.” He added that the revised Basel framework had “a sort of bias against bank lending”, and that “banking regulators should analyze the combined effect on the real economy of the multitude of rules that are due to come into force.”

He is both right and wrong. Wrong because the Basel rules have not been loose for corporate lending since Basel was put in place in the 1980s. It’s precisely the opposite. Rules were stricter than for many other lending types, such as real estate lending, leading to the great credit distortion we have experienced over the past couple of decades, and the slow recovery as corporations were starved of credit (see many many of my previous blog posts for details).

But he’s right that the revised Basel framework will perhaps exacerbate this situation by widening the spread between the capital cost of SME lending and that of real estate lending.

This is where the great contradiction lies. Nowotny is one of the first top regulators to underline a part of the credit allocation distortion. Yet most regulators believe that higher capital costs are justified on the basis that SME/corporate lending is inherently riskier. They never admit that the Basel framework played a major role in creating the great real estate credit bubble that led to the crisis. They constantly, and stubbornly, deny that Basel’s risk-weights could have any impact on the credit supply (and hence the sectorial interest rate). Yet, they contradict themselves when, at the same time, they consider lowering those same risk-weights on a number of products (such as securitisations) to boost…their supply and demand!

Let me get this straight: risk-weights are an instance of price control (in this case, capital cost control). And economic theory clearly demonstrates that price controls are both inefficient and leads to economic distortions. You can’t stabilise the financial system using price control tools, and then blame financial institutions and economic agents for rationally reacting to your measures. You just can’t.

Update: I originally used the term ‘price-fixing’ above. I then thought ‘price control’ was more appropriate, so I modified the post.

Economists and banking: why such misunderstanding?

I had a curiously contrasting week. A few days ago, I attended a private conference organised by the Adam Smith Institute with Bob Hetzel, of the Richmond Fed. The following day I attended the annual Moody’s banking conference. Both events talked about the financial crisis and low interest rate environment, yet illustrated the huge gap between both worlds.

In his explanation of what went wrong in 2008/9, Bob Hetzel never mentioned the words ‘banks’ or ‘financial system’ even once (at least from what I can remember). Consumer demand, investment, liquidity, monetary policy, central banks were the terms used. This is typical. Too many economists nowadays seem to have forgotten that banks exist and that the traditional way of implementing monetary policy has been for central banks to deal with commercial banks (primary dealers, lending facilities…). Of course, the financial crisis also saw central banks use extraordinary measures by buying other types of assets resulting in the impact of the asset price channel of monetary policy grow.

Still, over the last couple of weeks, a number of famous economists and economic commentators have written articles showing their limited understanding of how banks really work.

First in line is Scott Sumner. While Scott is one of my favourite economists, who opened my eyes on a number of things over the past few years, his stubborn dismissal of the importance of banks is unfortunate. In an Econlog column published a few days ago, Scott urges us to “stop talking about banking”. Monetary policy is independent he says, a separate phenomenon.

He gives the following example:

You print more currency than the public wants to hold, and they’ll bid up prices. How do you inject it without banks? Simple, pay government worker salaries in cash. Or buy T-bonds for cash. Cantillon effects don’t matter, unless the central bank is doing something bizarre, like buying bananas.

This is an unrealistic story. Does any central bank print money and pay government salaries? No. At least not in the developed world. From whom do central banks buy T-bond? From…banks, and from funds, which then leave the newly acquired cash in…banks. Or which purchase other assets to replace those T-bonds, in which case this cash also ends up in banks. And in truth, the hot potato effect described by Leland Yeager can easily get interrupted by the operational realities of the financial sector. In short, financial institutions can wear heat protection gloves. There is no need for IOR for excess reserves to build up. The implementation of monetary policy remains subject to strong structural rigidities (it isn’t the goal of this post to list such rigidities, although it may be the topic of a later one).

Against all evidence, Sumner keeps denying that banks, their business models, their regulation, and their accounting standards, play a role in transmitting monetary policy, booms and busts. He (as well as Hetzel) considers himself a follower of Milton Friedman’s monetarism. Yet Friedman seemed to understand more about banks than Sumner does. Indeed, Friedman and Schwartz partly blamed bank accounting standards (in particular mark-to-market accounting) for the catastrophic banking collapse (and money supply collapse) of the Great Depression.

In A Monetary History of the United States, he explains that due to tight liquidity levels, and “whatever the quality of assets held by banks”,

banks had to dump their assets on the market, which inevitably forced a decline in the market value of those assets and hence of the remaining assets they held. The impairment in the market value of assets held by banks, particularly in their bond portfolios, was the most important source of impairment of capital leading to bank suspensions, rather than default of specific loans or of specific bond issues.

Hence Friedman describes a self-reinforcing insolvency issue that originates in a liquidity problem, and which led to a contraction of the money supply. He also thinks that outright defaults of bad loans made in the 1920s, while limited, could have been the trigger that led to the tight liquidity situation. He adds that large open market purchases of those assets could have maintained their market value and prevented a number of bank failures (although I have to object that this is akin to a bailout of the system, with strong associated moral hazard).

Now, Friedman may have understated the extent of the solvency crisis during the Great Depression. What is certain is that the Great Recession involved a larger insolvency component. In the US, default rates started to increase by end-2006, and house prices by end-2005 (see charts below), way before liquidity conditions tightened as a result of this large-scale solvency issue. But overall, Friedman was wiser than many of his followers as he understood the role of banking in amplifying (if not creating) crises.

Against this background, it is unsurprising that many other economists seem clueless about banking. Krugman is bewildered that banks demand higher rates (see also here). He understands that banks experience margin compression (a rarity among economists though…), but doesn’t seem to get that a healthy economy needs healthy banks and that unhealthy banks disrupt the money creation process (and hence the inflation that he wants to see appear). He also misses the fact that low central bank base rates could simply just stop being transmitted to the economy.

Instead, he uses his usual personal attacks (‘permahawkery’, ‘interest group’, easily influenceable Fed and BIS officials – really? After all the regulatory rounds of those past few years? – ‘lobbyists’, ‘corrupt’…). Of course banks are going to lobby. This doesn’t imply that we should simply dismiss those claims without even attempting to analyse their substance.

The same effect is occurring in Europe. Bundesbank’s Andreas Dombret declared that the impact of low interest rates on German banks was “truly worrying” following a Bundesbank stress test. SNL (gated link) reports that:

According to the worst-case scenario involving a 100-basis-point reduction in the interest rate, these German banks could see a 75% drop in pretax profit by 2019. Even if they adjusted their balance sheet structure, the decline would still be 60%.

Under assumptions based on 2014-end rates and business plans, the cohort of German banks expects its pretax profits to decline by 25% by 2019 despite the solid economy and current cost-cutting targets. Remarkably, profits would fall even in the event of a 200-basis-point rate rise. […]

“I found results of the survey alarming for the large banks,” Kepler Cheuvreux bank analyst Dirk Becker told SNL Financial. “The effect of low interest rates will kill the banks at some stage if this continues. The study said that so much money is lost on the deposit margins that cannot be made good on lending margins. That is truly dramatic.”

Surely Krugman could explain to us how an economy can thrive with a dying banking system. Dombret, while worried, nevertheless warned banks that low rates in Europe were here to stay.

And what about Noah Smith? After a misguided article some time ago on the same topic, he now points out that some “commentators say they believe that they have hit upon the answer — it’s all about net interest margins, or the spread between a bank’s borrowing costs and lending rates.” Good to know that ‘commentators’ have to teach economists about banking mechanics… (and I might well be one of those, given my reply and interactions with Smith after his first article)

Unfortunately, he keeps misunderstanding the drivers of margin compression. He states that:

Then there’s the lack of a good theory for why lower interest rates should compress banks’ margins. Changes in the fed funds rate should affect both long-term and short-term rates equally. If the Fed tightens, depositors will demand higher deposit rates from banks, and banks will demand higher interest from borrowers. After an initial period of adjustment (to allow for existing loans to roll over), the effect of rate changes on spreads shouldn’t be substantial.

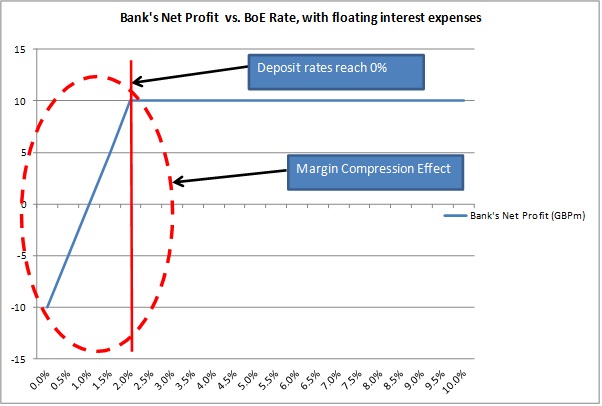

Really? As I explained now some time ago (see chart below from this old post), above a certain threshold the nominal level of interest rates is irrelevant (the real level might be to an extent). It is when deposit funding reaches the zero lower bound that banks start experiencing troubles, in particular if their loan books are composed of a lot of variable-interest loans (the worst case scenario being loans contractually based on the central bank base rate, such as what happens in the UK mortgage industry with loans being priced at BoE base rate + spread).

The result of this is that the spreads between deposit rates and lending rates narrow while banks’ cost structure doesn’t change. A simple P&L analysis shows why this is an issue. In the absence of other major sources of revenue growth, and independently of credit risk considerations**, banks (which are stuck with portfolios of multi-decade maturities low rate variable mortgages) have to start increasing the spreads on new lending to rebalance their revenue stream in line with their cost of intermediation. Which defeats the purpose of lowering the central bank base rate to stimulate lending.

Smith adds that a Fed tightening would increase banks’ interest expense. This is inaccurate. Deposit-funded banks don’t have to raise deposit rates unless under competitive pressure if and when they try to attract more funds to grow their lending business. But on the other hand variable rate lending automatically generates higher interest income***.

There is indeed an argument that monetary easing helps banks by lowering default rates, and hence banks’ cost of risk, which boosts their bottom line. But the net effect is far from clear, especially in the long run when banks have fully repriced their books to factor in wider credit risk spreads.

And in the end, it all demonstrates that understanding banking mechanics is crucial to monetary policy.

*Or banks can lend to capital light sectors, such as real estate, which isn’t included in inflation measures such as the CPI, while avoiding capital intensive asset classes, such as SME lending. Consequently, new money keeps being recycled in housing, and never shows up in CPI figures.

**Don’t get fooled by sudden changes upwards in net interest margins. NIMs aren’t risk-adjusted. When credit risk rises, banks increase the cost of credit to offset the increased cost of risk and likely loan impairment charges. NIMs then look like they improved. But ‘real NIMs’ (ie, risk-adjusted NIMs) didn’t. Compare Germany and Spain for instance: German NIMs have fallen as credit risk has remained low, whereas Spanish NIMs seem to hold up well, but this hides a decline in risk-adjusted margins.

***He also referred to Japan as a counter example of a rate rise that did not help banks. But in this case, rates didn’t rise above the threshold I was talking about above, so the example is still irrelevant.

Update: Scott Sumner’s reponse at Econlog. I think I really have to write a post on the structural rigidities at the micro level that I mention above (when I find the time…).

{kind=link}

{kind=link}

Recent Comments