It wasn’t a subprime crisis

The term ‘subprime crisis’ is still widely used to describe the recent financial crisis. Yet it gives the impression that the crisis emanated from a very narrow asset class (i.e. subprime mortgage lending) that somehow managed to spread throughout the US economy and the wider world and knock down most Western economies. The narrative is that financial innovation and engineering fuelled this process by creating products like RMBS and CDOs.

On closer examination, this story cannot hold. Real estate markets boomed and fell simultaneously around the world despite no subprime lending going on in these other markets. Mortgage lenders in countries such as Spain, Ireland and the UK suffered or even collapsed when falling house prices forced them to provision huge amounts, damaging their balance sheet and ability to lend.

Even in the US, the crisis wasn’t triggered by subprime but by an unsustainable allocation of resources towards the entire real estate sector. New research adds further evidence to this view (Loan Origination and Defaults in the Mortgage Crisis: The Role of the Middle Class). In this paper, Adelino, Schoar and Severino demonstrate that “mortgage originations increased for borrowers across all income levels and FICO scores” and that “middle-income, high-income, and prime borrowers all sharply increased their share of delinquencies in the crisis.” This conclusion is in stark contrast with that of Mian and Sufi’s famous 2009 article (which they reformulated in their book House of Debt), which had fuelled the theory of a subprime origin to the crisis (I had already voiced doubts about their theory here).

More precisely, Adelina et al find that credit flowed towards all sorts of borrowers in the years preceding the crisis, and not just disproportionately towards subprime ones:

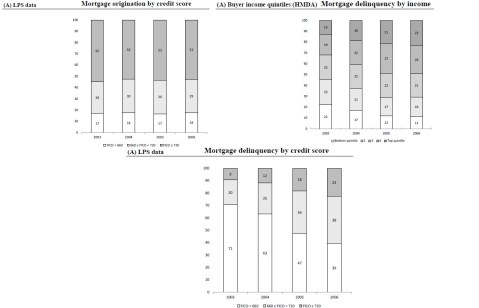

between 2002 and 2006 mortgage origination increased for borrowers across the whole income distribution, not just for low-income or subprime borrowers. In line with previous years, the majority of new mortgages by value were originated to middle-class and high-income segments of the population even at the peak of the boom. Similarly, the share of originations to subprime borrowers (those with a credit score below 660) relative to high credit score borrowers remained stable across the pre-crisis period. Although the pace of origination rose in low-income ZIP codes, this increase did not translate into significant changes in the overall distribution of credit, given that it started from a low base (borrowers in low-income and subprime ZIP codes obtain fewer and significantly smaller mortgages on average).

They also find that non-performing loans rose across the board, implying that losses were triggered by all sorts of real estate loans:

We show that the share of mortgage dollars in delinquency stemming from the lowest income groups decreased during the financial crisis. In contrast, middle- and high-income borrowers constituted a larger share of mortgage dollars in delinquency than in any prior year. The magnitudes are large: for the 2003 mortgage cohort, the top quintile of the income distribution constituted only 13% of mortgage dollars in delinquency three years later, whereas for the 2006 cohort, the top income quintile made up 23% of the delinquencies three years out. In contrast, over the same period, the contribution to delinquencies from the ZIP codes in the lowest 20% of the income distribution fell from 22% to only 11%.

We find a similar pattern when we look at credit scores: the share of mortgage defaults from borrowers with high credit scores increased during the crisis, whereas the share for subprime borrowers dropped.

Adelina et al therefore provide evidence that links the US real estate crisis with that of other countries: same roots, same consequences. The US did not experience a crisis because of a sudden and sharp increase in subprime borrowing. Subprime merely was a bystander; a symptom of deeper economic problems. Rather, the US experienced the same sort of crisis as its European counterparts: an overall debt-fuelled rise in real estate prices.

And this makes perfect sense: I keep emphasising the role played by Basel’s capital regulation in inflating the housing bubble. Low capital requirements on real estate loans provided bankers an incentive to maximise profitability within regulatory boundaries, directing the flow of credit towards housing, inflating the bubble. A purely subprime story with relatively low or no effect on other types of borrowers would not really fit this theory and would not match the experience of other countries.

Do not get me wrong though: subprime lending probably amplified the losses that some banks experienced, and did spread the crisis abroad to some extent. While the German real estate market remained roughly stable throughout the period, a number of German Landesbanks that had invested in tranches of structured products based on US subprime or near-subprime mortgages did suffer quite badly when the market price of those products radically fell.

Another very recent publication (The effect of bank shocks on firm-level and aggregate investment, by Amador and Nagengast) looks at what happened to lending and investment in the Portuguese economy following bank shocks during the 2005 to 2013 period. While I am not aware of similarly-structured studies of bank shocks in the US economy, this paper does seem to be in line with empirical results obtained by other researchers focusing on countries as diverse as Japan, Germany and emerging markets. They found that

credit supply shocks have a strong impact on firm-level investment in the Portuguese economy over and above aggregate demand conditions and firm-specific investment opportunities. In addition, we also consider how the effect of credit supply shocks on investment varies with the capital structure and size of firms. We find that firms with access to alternative financing sources are generally less vulnerable to the adverse effect of bank shocks on investment and partially manage to offset their shortfall of bank credit by increasing their financing from other sources. Larger firms also appear to be in a better position to cope with the unfavourable effects of bank shocks mainly since their banks do not curtail their credit supply as much as for small firms.

Those results look unsurprising to me and surely amplified by Basel rules that stipulate that small firms require proportionally more capital than large ones (a requirement that is hardly justified).

But combined with the empirical evidence provided above by Adelina et al, they allow me to reiterate my doubts regarding the claim that NGDP targeting would have merely led to a mild recession. This is a view of the crisis that some market monetarists accept, and which was summarised by Beckworth and Ponnuru in an NYT column earlier this year:

In retrospect, economists have concluded that a recession began in December 2007. But this recession started very mildly. Through early 2008, even as investors kept pulling money out of the shadow banks, key economic indicators such as inflation and nominal spending — the total amount of dollars being spent throughout the economy — barely budged. It looked as if the economy would be relatively unscathed, as many forecasters were saying at the time. The problem was manageable: According to Gary Gorton, an economist at Yale, roughly 6 percent of banking assets were tied to subprime mortgages in 2007.

I wrote elsewhere why I believe this view is inaccurate. But this new evidence provided by Adelina et al adds strength to my previous arguments by showing that the crisis was a full-scale real estate collapse rather than a mere and ‘manageable’ subprime-focused crisis. It should also make us think twice about the ability of NGDP targeting to cope with a situation during which banks’ balance sheets are highly damaged, leading to reduced lending and aggregate private investments throughout the economy.

That said, I do view NGDPT as a much better alternative to our current monetary arrangement. While it could potentially have alleviated the worst symptoms of the crash, I believe it is quite a stretch to think it could have led to a merely ‘mild’ recession. Please bear in mind however, that my reasoning only applies within the current institutional constraints on the implementation of monetary policy.

Were those constraints lifted, NGDP targeting could be more effective in stimulating the economy post-crash. Whether this is desirable is another issue altogether, and I tend to adhere to Salter and Cachanosky’s view that the composition of NGDP also matters*. After all, NGDP growth was roughly stable for the decade preceding the crisis, yet hid some unsustainable allocation of resources. Consequently, it seems to me that distortionary regulatory frameworks limit the effectiveness of a stable NGDP path. But would we even need NGDP targeting in a free market?

*As a side note, an interesting paper published last year seems to provide some evidence of the distortionary effect on relative prices of the usual monetary injection channel of monetary policy (i.e. Cantillon effect). This is only a lab experiment, but its conclusions are clear:

Although the theoretical model predicts, in line with mainstream economics, that the process of monetary injection is irrelevant and neutral, the experiment shows that credit expansion exerts a significant distortionary effect on resource allocation. Credit expansion also has a redistributive effect across subjects in favor of those who have a high consumption preference for the good whose production is stimulated by credit. The allocative effect of credit expansion comes from the fact that the increase in money is injected into the credit market, whereas lump-sum transfers affect all sectors evenly.

This finding is reminiscent of the insights of Cantillon (1755), who emphasised that an increase in money primarily affects relative prices rather than all prices to the same extent because money enters the economy at a certain point. This suggests that the process of monetary injection and its economic consequences should be addressed in implementing specific monetary policy measures or, more importantly, in designing the monetary system as a whole.

PS: This is my first blog post in a while. I am currently transitioning between jobs, and am pretty busy as a result.

Recent Comments