The limitations of the market monetarist story of the recession

The market monetarist story of the ‘Great Recession’ got published in the NYT two days ago in a column written by Beckworth and Ponnuru. I’m happy to see market monetarist ideas spread in the mainstream, but not fully happy because they still give a narrow view of what happened during the crisis, in my opinion.

And this column is no exception to the rule: market monetarism can explain a large part of the bust, but cannot explain the boom that led to the bust. Unfortunately, they are intrinsically linked and forgetting the mechanism that led to the economic implosion also lead them to draw partly wrong conclusions about what the Fed and other central banks could have done to ‘save the economy’.

This is Beckworth and Ponnuru:

What the housing-centric view underemphasizes is that the housing bust started in early 2006, more than two years before the economic crisis.

This is not what I saw. To me, the crisis started during the 2007 summer as the increasing level of defaults in the real economy triggered a number of funds to collapse (BNP Paribas and Bearn Stearns come to mind). The fact that events did not happen simultaneously does not imply that they were not linked. Indeed, as I describe below, it is extremely unlikely that financial stress would trigger a sudden economic collapse. Financial problems are usually a symptom that can turn into an amplifier. But rarely a root cause.

Then:

This housing decline caused financial stress by sowing uncertainty about the value of bonds backed by subprime mortgages. These bonds served as collateral for institutional investors who parked their money overnight with financial firms on Wall Street in the “shadow banking” system. As their concerns about the bonds grew, investors began to pull money out of this system.

This is the Gary Gorton ‘run on repo’ story. But this is not the only account of the financial crisis. Indeed, it is a very US-centric and incomplete theory, which forgets that housing booms occurred all around the world and that the primary driver of financial stress was not a withdrawing of wholesale (short-term repo in particular) funding from banks and other shadow banks, but a fear that the housing bust would make the banking system insolvent. The collateral story is only a part of this: most Spanish, Irish or German banks had nothing to do with the large wholesale-funded Wall Street broker-dealers that used some RMBSs as collateral in a number of trades. ‘Normal’ banks did not make extensive use of repos. They considered RMBSs, CMBSs and CDOs as higher-yielding investments, which they mostly held on balance sheet, sometimes as part of their liquidity portfolio.

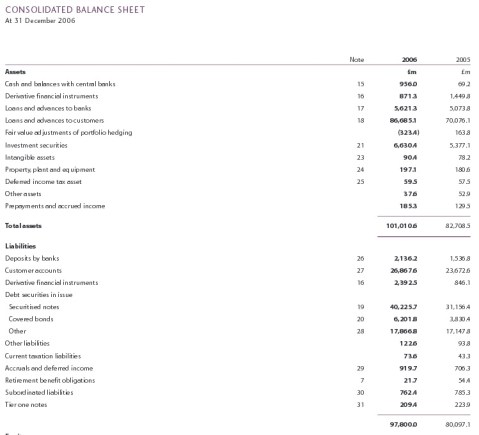

Moreover, remember UK-based Northern Rock. It suffered a bank run because depositors feared it could collapse. Why did they fear it could collapse? Because it was running out of liquidity as it was mostly wholesale-funded (but wasn’t using exotic securities as collateral for trades and wasn’t funded much with repos – see its end-2006 balance sheet below; this was a pretty straightforward retail bank, apart from the fact that it had a very high loans/deposit ratio of about 320%).

And why did its wholesale funding evaporated? For two reasons: 1. it had large exposures to the falling British housing market, and investors feared that it would fall into bankruptcy, and 2. some of the wholesale funding the bank was relying on was based on selling RMBS and CMBS to the market, which were not based on US subprime mortgages, but were still viewed as risky as house prices were on a downward path. Other British banks, which were seen as more diversified and safer by the market, such as HSBC, did not suffer such fate. So the ‘run on repo’ story of the financial crisis cannot comprehensively explain what happened.

They continue:

In retrospect, economists have concluded that a recession began in December 2007. But this recession started very mildly. Through early 2008, even as investors kept pulling money out of the shadow banks, key economic indicators such as inflation and nominal spending — the total amount of dollars being spent throughout the economy — barely budged. It looked as if the economy would be relatively unscathed, as many forecasters were saying at the time. The problem was manageable: According to Gary Gorton, an economist at Yale, roughly 6 percent of banking assets were tied to subprime mortgages in 2007.

Here, they assume too much. First, they assume that economic problems appear as soon as financial stress starts occurring. There is no evidence of that, and the slow and progressive slowdown in lending triggered by financial issues affect the economy with a lag. It is when total credit, and hence total money supply, starts contracting that the economy starts suffering.

Second, they assume that the problem was ‘manageable’, once again according to Gorton’s misleading figure. This is misunderstanding the underlying accounting. 6% of banking assets that fall by more than 50% in value is huge. Let me repeat that: it is huge. It means that more than 50% of banks’ capital has been disintegrated. Remember that, at this time, banks’ leverage (equity/assets) was in the 5 to 7% range, and even lower outside the US (like 2.5% to 6%). Meaning that a fall of asset value of between 5 and 8% was sufficient to make institutions insolvent (and even less if considering the harsher Basel criteria). Against all evidence, Beckworth and Ponnuru are telling us that it was ‘manageable’…

Moreover, and even more importantly, it is not only securities linked to subprime mortgages that fell in value: a number of non-subprime loans defaulted (or didn’t, but the fall in house prices forced banks to massively increase their provisioning, leading to losses that further eroded their capital base), in turn securities based on non-subprime loans also lost value, stock prices were falling, fixed income securities’ spreads were widening… Consequently, the percentage of US banks’ assets at risk wasn’t just 6%; it was much higher (although I can’t put an exact figure on this). There was nothing manageable about that. The amount of malinvestments that had accumulated before the crisis was staggering.

Don’t get me wrong though. Beckworth and Ponnuru are mostly right. Central banks did make huge mistakes. And inflation targeting is a bad policy that cannot properly respond to supply shocks. I cannot agree more. And I see a rule-based policy such as NGDP targeting as a second best to free banking (or perhaps third, if we include Selgin’s productivity norm).

But as I described in a separate post (to which Scott Sumner responded here, albeit avoiding my main points), too many economists simply tend to avoid talking about banks. Yet they face structural rigidities which, as I wrote in a number of other posts, make them crucial. Bank accounting frameworks and regulations directly impact the way monetary policy is transmitted and the way the broader money supply grows. Given how banking regulation is structured, malinvestments are hard-wired in lending expansion, meaning you don’t even need easy money to eventually trigger a crash. Accounting matters too: change a single rule such as mark-to-market accounting, and you’d surely have never experienced a crisis of the same scale.

So we can stick to the story that describes the crisis as a fall in NGDP, or we can question whether or not this NGDP growth trend was sustainable in the first place, or even whether or not the components of NGDP were sustainable (whereas the aggregate figure was) as Salter and Cachanosky would point out. It is not the topic of this post. But I believe we should not oversimplify the events that led to and followed the crisis. Yes, central banks’ reactions in the first year of the crisis were poor. The market monetarist story (i.e. tight monetary policy) is a good depiction of what amplified the crisis. But certainly not a comprehensive explanation of the boom and its subsequent dramatic correction.

PS: I have a few posts in the pipeline that review recent research that provides further empirical evidence in favour of my version of the story (i.e. regulation that leads to unsustainable housing, sovereign debt and exotic securities boom while depressing corporate lending – and hence possibly playing a major role in the weak recovery and the secular stagnation theory).

7 responses to “The limitations of the market monetarist story of the recession”

Trackbacks / Pingbacks

- - 2 February, 2016

- - 23 June, 2016

Leave a comment

Recent Comments

| pslebow on ‘Sovereign money’:… | |

| pslebow on A critique of Werner’s view on… | |

| Hugo Kramer on Welcome to Spontaneous Fi… | |

| Nathan on A critique of Werner’s view on… | |

| Nathan on More, more, more money endogen… |

the argument doesn’t stack up considering default rate in prime borrowers became higher than sub prime.

http://www.nber.org/digest/aug15/w21261.html

so like you say banks misspriced risk in assets with low risk profiles too.

Precisely. Hence why the Gorton figure is misleading.

In particular, in the US, when households fall into negative equity, they often just walk away, even if they have the means to pay, leading to large losses for banks.

So the fall in house prices was key in triggering financial stress across the board. It never was just a limited subprime story to which central banks misresponded.

Very interesting take on the crisis. My spin is that of government policy. Carter and then Clinton pushed homeownership until it broke. Bush the Younger did little to stop it. Then The Fed’s absurd rate policies fed and killed the beast. Gorton is correct in that investors were spooked, but it was more than that. I have a chart to show what I mean, but I cannot post it here.

Nice analysis!

“… they assume that economic problems appear as soon as financial stress starts occurring.”

I have noticed that most mainstream economists assume everything happens at the same time. Scott Sumner actually wrote once on his blog that prices adjust immediately to changes in Fed policy. I think they spend so much time with their timeless models that they actually begin to believe that lags don’t exist.

I have begun to see all of the business-cycle theories as being a correct description of some aspect of the cycle, but not comprehensive. I think the Austrian theory the only comprehensive one that actually explains instead of just describing what happened. The Austrian theory provides a skeleton on which the other theories can provide some flesh and blood.

I agree. I see the ABCT as the base, the story of the boom. Other theories can then complement it to explain why a bust was worse/better than it could have been.