More inside/outside money endogeneity confusion

I was surprised by a Twitter discussion yesterday that linked to this good post by David Beckworth. As you can guess, the topic once again involved the endogeneity of money. Beckworth’s answer to an interview question was:

My answer was that inside money creation–money created by banks and other financial firms–is endogenous, but the Fed shapes in an important way the macroeconomic environment in which money gets created.

David is right. But what I do find surprising is that his interviewer could ask such question as “do you believe that money is endogenously created?”

Let’s clarify something: the fractional reserve banking/money multiplier model necessarily implies endogenous creation of bank inside money. It describes how banks multiply the money supply from a small amount of externally-supplied reserves. If this isn’t endogenous creation, I have no idea what this is. I don’t think anybody who accepts that model ever denied that fact.

The recent debate wasn’t about whether bank inside money was endogenously created but about whether or not the monetary base (i.e. outside money, or bank reserves) was also endogenously created. This is not at all the same thing and has very different implications altogether.

If the monetary base is endogenously created, the central bank cannot control the money supply, as MMTers and some post-Keynesians believe. I believe this is not the case, as highlighted in my various post (see here, here and here for examples).

However, if bank inside money is endogenously created and outside money exogenously created, this can only mean one thing: banks’ inside money creation ability is exogenously constrained by the amount of outside money in the system (though other factors also come into play).

This has always been the essence of the fractional reserve banking/money multiplier model. Model that has been severely misinterpreted recently, as Scott Sumner pointed out in a very recent post:

He [David Glasner] seems to believe multiplier proponents viewed it as a constant, which is clearly not true. Rather they argued the multiplier depends on the behavior of banks and the public, and varies with changes in nominal interest rates, banking instability, etc.

I can’t say how much I agree with Scott here, and this is exactly what I said in a recent post:

In their attempt to attack the money multiplier theory, they mistakenly say that the theory assumes a constant ratio of broad money to base money. There is nothing more wrong. What the money multiplier does is to demonstrate the maximum possible expansion of broad money on top of the monetary base. The theory does not state that banks will always, at all times, thrive to achieve this maximum expansion. I still find surreal that so many clever people cannot seem to understand the difference between ‘potentially can’ and ‘always does’.

A system in which there would be no money multiplier would effectively be a 100%-reserve banking system.

What’s interesting is that many proponents of the ‘uselessness’ of the money multiplier seem to have tone down their criticisms recently. Frances Coppola went from “the money multiplier is dead” to “it is improperly taught” (my paraphrasing)…

PS: when in my various posts I refer to (and say that I don’t believe in) the endogeneity of money, I refer to outside money/monetary base/high-powered money/reserves/whatever you want to call it, as I take inside money endogeneity for granted (with constraints, as already explained).

A central banker contradiction?

Last week, Mark Carney, the governor of the Bank of England, was at Cass Business School in London for the annual ‘Mais Lecture’. Coincidentally, I am an alumnus of this school. And I forgot to attend… Yes, I regret it.

Carney’s speech was focused on past, current, and future roles of the BoE. In particular, Carney mentioned the now famous monetary and macroprudential policies combination. It’s a classic for central bankers nowadays. They all have to talk about that.

In January, Andrew Haldane, a very wise guy and one my ‘favourite’ regulators, also from the BoE, made a whole speech about the topic. As Jens Weidmann, president of the Bundesbank, did in February.

I am not going to come back to the all the various possible problems caused and faced by macroprudential policies (see here and here). However, there seems to be a recurrent contradiction in their reasoning.

This is Carney:

The transmission channels of monetary and prudential policy overlap, particularly in their impact on banks’ balance sheets and credit supply and demand – and hence the wider economy. Monetary policy affects the resilience of the financial system, and macroprudential policy tools that affect leverage influence credit growth and the wider economy. […]

The use of macroprudential tools can decrease the need for monetary policy to be diverted from managing the business cycle towards managing the credit cycle. […]

That co-ordination, the shared monitoring of risks, and clarity over the FPC’s tools allows monetary policy to keep Bank Rate as low as necessary for as long as appropriate in order to support the recovery and maintain price stability. For example expectations of the future path of interest rates – and hence longer-term borrowing costs – have not risen as the housing market has begun to recover quickly.

First, it is very unclear from Carney’s speech what the respective roles of monetary policy and macroprudential policies are. He starts by saying (above) that “monetary policy affects the resilience of the financial system”, then later declares “macroprudential policy seeks to reduce systemic risks”, which is effectively the same thing. At least, he is right: both policy frameworks overlap. And this is the problem.

This is Haldane:

In the UK, the Bank of England’s Monetary Policy Committee (MPC) has been pursuing a policy of extra-ordinary monetary accommodation. Recently, there have been signs of renewed risk-taking in some asset markets, including the housing market. The MPC’s macro-prudential sister committee, the Financial Policy Committee (FPC), has been tasked with countering these risks. Through this dual committee structure, the joint needs of the economy and financial system are hopefully being satisfied.

Some have suggested that having monetary and macro-prudential policy act in opposite directions – one loose, the other tight – somehow puts the two in conflict [De Paoli and Paustian, 2013]. That is odd. The right mix of monetary and macro-prudential measures depends on the state of the economy and the financial system. In the current environment in many advanced economies – sluggish growth but advancing risk-taking – it seems like precisely the right mix. And, of course, it is a mix that is only possible if policy is ambidextrous.

Contrary to Haldane, this does absolutely not look odd to me…

Let’s imagine that the central bank wishes to maintain interest rates at a low level in order to boost economic activity after a crisis. After a little while, some asset markets start looking ‘frothy’ or, as Haldane says, there are “renewed signs of risk-taking.” Discretionary macroprudential policy (such as increased capital requirements) is therefore utilised to counteract the lending growth that drives those asset markets. But there is an inherent contradiction here: one of the goals that low interest rates try to achieve is to boost lending growth to stimulate the economy…whereas macroprudential policy aims at…reducing it. Another contradiction: while low interest rates tries to prevent deflation from occurring by promoting lending and thus money supply growth, macroprudential policy attempts to reduce lending, with evident adverse effects on money supply and inflation…

Central bankers remain very evasive about how to reconcile such goals without entirely micromanaging the banking system.

I guess that the growing power of central bankers and regulators means that, at some point, each bank will have an in-house central bank representative that tells the bank who to lend to. For social benefits of course. All very reminiscent of some regions of the world during the 20th century…

Weidman is slightly more realistic:

We have to acknowledge that in the world we live in, macroprudential policy can never be perfectly effective – for instance because safeguarding financial stability is complicated by having to achieve multiple targets all at the same time.

Indeed.

Photograph: Intermonk

Crowdfunding, naivety and scandals

John Kay wrote an interesting article for the FT yesterday, titled “Regulators will get the blame for the stupidity of crowds.” He argues that, despite crowdfunding and P2P enthousiasts blaming regulators for being too slow and too cautious, this new market will eventually crash and trigger calls for more advanced regulation as well as the setup of compensation schemes. Desintermediation firms would then reintermediate lending and effectively transform into… banks.

I partly agree with Kay. A collapse/crash/losses/fraud/scandals is/are inevitable. And this is a good thing.

I have already written about the importance of failure in free market financial systems. New financial innovations need to experience failures in order to end up reinforced, to distinguish what works from what doesn’t work. This is a Darwinian learning process. The system then becomes ‘antifragile’. Consequently, the state should refrain from intervening in order not to postpone this necessary learning process and resulting adjustments. When crowdfunding crashes, the state should resist any call for intervention/bailout/regulation. This is the only way crowdfunding can become a mature industry.

I however also partly disagree with Kay, who I believe does not see the bigger picture.

Kay argues that investors (in this case ‘crowds’) are naïve. That intermediation has benefits and non-professional investors lack the ‘cynicism’ to assess the risk/reward profile of those investments.

Where Kay is wrong though, is in considering P2P lending as “a substitute for deposit account.” It is not. P2P lending is an investment. Unsophisticated retail investors can also lose much of their money by investing in various stocks. Or by betting on the wrong horse. I don’t believe investors mistake crowdfunding for bank deposits…

I think that what Kay also fails to see is that, if historically many start-ups and young SMEs have struggled to grow and eventually failed, it is partly because they lacked the funds required to grow. Some start-ups ended-up collapsing or selling themselves to larger competitors simply because funding became scarce at the second or third round of funding. This funding gap was particularly prevalent in some markets such as the UK (less so in the US). Some other markets, such as France, on the other hand, lack first round financing (seed funding, mainly provided by ‘Angel’ investors).

When the supply for loanable funds is scarce relative to the demand, demanded return on investment is high. Many new firms, particularly in non-growth markets, find it hard to cope with this situation and are pretty much avoided by venture capital investors. What equity crowdfunding and P2P lending do is to increase the supply of loanable funds, reducing the average required rate of return. Refinancing risk mechanically recedes, guaranteeing the success or the failure of an SME on its business strategy and execution alone.

In addition, crowdfunding multiply investment opportunities, making it easier to diversify a portfolio of investments. Historically, venture capital funds could not diversify too much if they wanted to maintain appropriate levels of returns.

Scandals are inevitable, but the learning mechanism inherent to the market process must be allowed to run its course. Learning, combined with the increased supply of loanable funds, would reduce the probability of scandals occurring in the long-run and make crowdfunding a solid industry.

Tobin vs. Yeager, my view

I really hesitated to write this post. For the last 10 days my blogging frequency has been close to nil as I re-read and gave a thought to James Tobin’s Commercial Banks as Creators of Money, Leland Yeager’s What are Banks, as well as several blog posts, including David Glasner’s (here, here and here). In the end, it looked to me that everything that could be said had already been said. But I’ve been asked to provide my opinion. Moreover, I believe that most of what has been said so far derived from economists’ point of view (which doesn’t mean this is wrong per se) and that a financial analyst/practitioner could potentially bring useful points to the debate.

As I said, I’ve been asked to provide my opinion. Let me give you a quick answer. I believe that both Tobin’s New View and Yeager’s Old View (?) are right. I also believe they are both wrong. Some of their arguments are true. Some others seem to contradict other points they make.

I believe that banks’ expansion is indeed limited by economic constraints. Perhaps just not the exact ones Tobin was thinking of. I also believe banks can and usually indeed do fully ‘loan up’. But perhaps not exactly the way Yeager was seeing it as I believe that reserve requirements (in particular, internally-defined ones, see below) are part of banks’ economic constraints.

A lot of the discussion surrounding the debate in the economic area/blogosphere rests on the nature of bank inside money and whether it is subject to the ‘hot potato’ effect. This is very clear in David Glasner’s posts. I encourage you to take a look at them (including their comment sections) although this can be a little technical for non-economists. But here I am going to take a slightly different approach, more finance theory-based.

First, I don’t believe in Tobin’s arguments that demand deposits’ yields are key. Tobin says:

Given the wealth and the asset preferences of the community, the demand for bank deposits can increase only if the yields of other assets fall. […] Eventually, the marginal returns on lending and investing, account taken of the risks and administrative costs involved, will not exceed the marginal cost to the banks of attracting and holding additional deposits.

I don’t know anyone who keeps his/her money in demand deposit accounts because of their yield (by ‘demand deposit’ I mean checkable deposits, not saving deposits available on demand, this is an important distinction). People maintain real balances in demand deposits to cover their cost of living (i.e. expected cash outflows over a given month). Here, on the ‘hot potato’ issue, I side with Yeager. Demand deposits provide a convenience yield. Nominal yields are pretty much unimportant. It is only when banks’ customers have surplus balances in their account that yields become important in the choice between using them for consumption or investment (and to pick the type of investment). But this does not concern demand deposits. It is hard to imagine anyone transferring most (or all) of his money from a demand to a saving account (or any other sort of investment) for yield purposes…

In addition, banks always pay close to nothing on demand deposits. In order to grow their deposit base, banks barely vary rates on demand deposits. Saving accounts and related financial products (retail bonds, certificates of deposit, etc.) that are not media of exchange are the ones used by banks to attract customers.

But the Tobin/Yeager debate focuses on demand deposits due to their very nature. And there seems to be some confusion in both Tobin’s article and Glasner’s posts. Tobin explicitly refers to demand deposits, and how competition from non-bank FIs would push up their interest rates. This is unlikely as described above. Saving deposits would be the ones to suffer. But they are not media of exchange and not the topic of the discussion. As a result, I find myself in general agreement with Bill Woolsey, who commented on Glasner’s posts.

Second, Tobin seems to downplay the role of reserve requirements. What he fails to see is that they also are part of banks’ economic constraints. He also contradicts himself when he declares that reserve requirements are only a legal constraint that kicks in before natural economic constraints prevent the bank from expanding, only to say a few pages later that reserves…aren’t a constraint on lending (which I believe is wrong as I have already said many times).

Some readers already know the simple bank accounting profit equation I referred to in a couple of previous posts:

Net Profit = Interest Income from lending – Interest Expense from deposits – Operational Costs

Let’s now move on to a slightly more complex version.

In the short-term, banks survive by making accounting profits. However, in the long-term, banks survive by making economic profits (= at least covering their cost of capital). And, unlike accounting-based financial statements, the cost of capital incorporates risk.

The risk I am particularly interested in today, and which is the most relevant for the Tobin/Yeager debate is liquidity risk. Let’s now modify the profit equation using White’s The Theory of Monetary Institutions. A bank’s economic profit equation thus becomes:

Economic Profit = II – IE – OC – Q, where Q represents liquidity cost.

Liquidity cost isn’t a ‘tangible’ cost and is therefore excluded from a bank’s accounting profit. Nevertheless, the less liquid a bank becomes, the riskier it becomes, and investors demand as a result appropriate compensation for bearing that extra risk, reflected in a higher demanded return on capital. Eventually, liquidity cost can also impact accounting profitability through higher cost of funding (i.e. interest expense).

Why I am referring to liquidity risk? Because liquidity risk becomes a direct economic constraint on bank expansion. Individual banks maintain a liquidity buffer to face redemptions and interbank settlements. The traditional view is that reserves play this role, through the exogenously-defined reserve requirements. Without them, banks would turn ‘wild’ and become way too risky. This view is inaccurate.

Indeed, banks in free banking systems during the 19th century used to maintain a high level of reserves, despite the absence of reserve requirements (though this level used to vary with technological advancement and demand for banks’ liabilities). With the development of capital markets, banks found another solution: swap some of their reserve holdings for highly-marketable and high quality securities, which effectively became reserve-replacements, or claims on reserves.

In order to maximise economic profitability, modern banks now usually maintain their (primary) reserves to a minimum while also holding secondary reserves (that is, in a non-interest on excess reserves world). In a way, banks are never fully loaned-up. From a primary reserves point of view, they indeed are. From a total reserves point of view, they are not. Banks sacrifice higher yields on loans for lower yields on safe and liquid securities. However, I have to admit that, from a risk-adjusted point of view, banks could be considered fully loaned-up*.

Seen that way, Tobin was right to believe that economic constraints would prevent bank expansion, but was wrong in believing that reserve requirements merely prevented the expansion from reaching its natural economic limits and that banks’ special status was only derived from this legal restriction**:

In a régime of reserve requirements, the limit which they impose normally cuts the expansion short of this competitive equilibrium. […] In this sense it is more accurate to attribute the special place of banks among intermediaries to the legal restrictions to which banks alone are subjected than to attribute these restrictions to the special character of bank liabilities.

If anything, economic constraints kick in before reserve requirements***, and internally-defined reserve requirements are part of economic constraints.

On the other hand, Yeager sometimes seems to overstate the effects of reserve requirements and underplay economic constraints in limiting expansion:

Proponents of this view are evidently not attributing “the natural economic limit” to limitation of base money and to a finite money multiplier, for that would be old stuff and not a new view. Those familiar limitations operate on the supply-of-money side, while the New Viewers emphasize limitations on the demand side.

To be fair, Yeager’s exact point of view isn’t entirely clear in his article. He seems to reject the ‘natural economic limits’ only to later endorse them, though this might be due to the facts he does not view liquidity cost as an economic constraint in his reasoning:

It is hard to imagine why a bank might find it more profitable to hold reserves in excess of what the law and prudence call for than to buy riskless short-term securities with them.

I also partially disagree with Yeager’s point that “the real marginal cost of expanding the system’s nominal size is essentially zero.” This is true… in the long run. But in the short-term extending credit often involves growing operational costs (i.e. hiring further loan officers for example), which weigh on banks’ accounting profitability in real terms, and growing liquidity costs, which weigh on banks’ economic profitability, before the nominal size of the system is finally expanded.

I might be missing something, but the ‘hot potato’ effect of banks’ inside money and the natural economic constraints on banks expansion do not look irreconcilable to me. This is also the view that White seems to take in his book. Furthermore, only this view seems to be able to explain the behaviour of free banks. Banks loan up to a degree that maximise economic profitability (which includes safety/risk) but any exogenous increase in reserves can also bring about an expansion of banks’ inside money (money multiplier effect) that results in a new nominal paradigm.

It’s funny but I have the feeling that this debate will make me think for much longer.

** In addition, the margin between interest income and interest expense isn’t the only way to generate revenues. In fact, many banks accept to extend credit to customers at a loss, in order to generate profits through cross-selling of other financial products (derivatives, insurance, clearing and custody services…). This effectively pushes back the economic limits of expansion (without taking account liquidity cost). A traditional (i.e. non-IB) bank’s economic profit equation would then become:

Economic Profit = II – IE + CS – OC – Q, where CS represents revenues from cross-selling.

*** Some of you might believe that this is in contradiction with my claim that reserve requirement policies have been successfully implemented in various countries. It isn’t. Primary reserves that are not in excess are essentially ‘stuck’ at the central bank. As banks fully ‘loan-up’ on them, increasing reserve requirements merely reduce lending expansion unless banks decide to slash their secondary reserves (which essentially replace excess reserves), which would in turn increase liquidity cost.

The Economist on Bitcoin (and some weird claims)

The Economist has two interesting articles on Bitcoin this week (here and here), as well as a blog entry (here). Coloured coins and the potential development (and other uses) of Bitcoin’s technology are mentioned.

But two of the articles make very strange (if not outright wrong) claims in order to criticise some of the principles underlying Bitcoin. One considers the inherent deflationary effect of Bitcoin as being a limitation on the ability of the currency to become mainstream. The article once again seems to miss the difference between good and bad deflation. For sure, this differentiation wasn’t mainstream until recently and is still not accepted by many mainstream economists (see one of the latest examples here). Still, introducing some nuance in its articles wouldn’t hurt the newspaper. In addition, the Economist makes claims such as:

A modicum of inflation greases the system by, in effect, cutting the wages of workers whose pay cheques fail to keep pace with inflation.

Don’t they see the problem with this sentence? Inflation fuelling inflation anyone?

In the blog post, Ryan Avent also makes a very inaccurate claim:

What’s more, the idea that modern central banks with their loosey-goosey printing presses have generated an epidemic of inflation is a little nuts; if anything, rich-world central banks have become too effective at protecting the value of their respective currencies.

Really? According to research by Selgin and White, the dollar has lost most of its value since the Fed was set up (whereas the value remained relatively stable over the previous century, though with short-term large fluctuations). (although it is possible that Ryan only refers to the last few years)

While I agree that Bitcoin isn’t perfect, its critics will have to find other angles of attack.

The BoE says that money is endo, exo… or something

The Bank of England just published an already very controversial paper, titled “Money creation in the modern economy”. Scott Sumner, Nick Rowe, Cullen Roche, Frances Coppola, JKH, and surely others have already commented on it. Some think the BoE is wrong, some, like Frances, think that this confirms that “the money multiplier is dead”. Some think that the BoE endorses an endogenous money point of view. Many are actually misreading the BoE paper.

To be fair, this might not even be an official BoE report, and might only reflect the views of some of its economists. That type of paper is published in many institutions.

I am unsure what to think about this piece… They seem to get some things right and some other things wrong, and even in contradiction to other things they say. Overall, it is hard to reconcile. What I read was a piece written by economists. Not by banks analysts or market participants. Therefore, some ‘ivory tower’ ideas were present, though in general the paper was surprisingly quite realistic.

I have also been left with a weird feeling. I might be wrong, but almost the whole ‘Limits on how much banks can lend’ section really seems to be paraphrasing my two relatively recent posts on the topic (here, where I criticise the MMT version of endogenous money theory, and here, where I respond to Scott Fullwiller). The paper does say that

The limits to money creation by the banking system were discussed in a paper by Nobel Prize winning economist James Tobin and this topic has recently been the subject of debate among a number of economic commentators and bloggers. (emphasis added)

Indeed…

Contrary to what some seem to believe, the BoE does not endorse a fully endogenous view of the monetary system, and certainly not an MMT-type endogenous money theory.

Let me address point by point what I think they got wrong or contradictory (I am not going to address the points in the QE section, which simply follow the mechanism described in the first section of the paper).

- First, there seems to be an absolute obsession with differentiating the ‘modern’ from the ‘pre-modern’ banking and monetary system. The paper keeps repeating that

in reality, in the modern economy, commercial banks are the creators of deposit money. (page 2)

Well… You know what, guys? It was already the case in the pre-fiat money era… Banks also created broad money on top of gold reserves, thereby creating deposits, the exact same way they now do it on top of fiat money reserves. The only difference is the origins of the reserves/monetary base.

- They very often refer to Tobin’s ‘new view’. But they never mention Leland Yeager, who strongly criticised Tobin’s theory in his article ‘What are Banks?’ As a result, their view is one-sided.

- The point that “saving does not by itself increase the deposits or ‘funds available’ for banks to lend” (page 2) is slightly misinterpreted. By not saving, and hence, consuming, customers are likely to maintain higher real cash balances, leading to a reserve drain. Moreover, even if no reserve drain occurs, banks end up with a much less stable funding structure, that does not make it easier to undertake maturity transformation. It is always easier to lend when you know that your depositors aren’t going to withdraw their money overnight. This is also in contradiction with their later point that

banks also need to manage the risks associated with making new loans. One way in which they do this is by making sure that they attract relatively stable deposits to match their new loans, that is, deposits that are unlikely or unable to be withdrawn in large amounts. This can act as an additional limit to how much banks can lend. (page 5)

- In their attempt to attack the money multiplier theory, they mistakenly say that the theory assumes a constant ratio of broad money to base money (page 2). There is nothing more wrong. What the money multiplier does is to demonstrate the maximum possible expansion of broad money on top of the monetary base. The theory does not state that banks will always, at all times, thrive to achieve this maximum expansion. I still find surreal that so many clever people cannot seem to understand the difference between ‘potentially can’ and ‘always does’. Moreover, the BoE economists once again contradict themselves, when on pages 3 and 5 to 7 they essentially describe a pyramiding system akin to the money multiplier theory!

- The paper also keeps mistakenly attacking the money multiplier theory and reserve requirements while entirely forgetting all the successful implementations of reserve requirement policies by central banks throughout the world (China, Turkey, Brazil…).

- The ‘banks lend out their reserves’ misconception is itself misconceived. I strongly suggest those BoE economists to read my recent post on this very topic. Here again this is in opposition with their later point that individual banks can suffer reserve drains and withdrawals through overlending…

- The ‘Limits on how much banks can lend’ section is very true (though I might be biased given how similar to my posts this section is), and I appreciate the differentiation between individual banks and the system as a whole, differentiation that I kept emphasizing in my various posts and that I believe is absolutely crucial in understanding the banking system. Nonetheless, while their description of the effects of over-expanding individual banks and what this implies for broad money growth is accurate, it is less so in regards to the system as a whole. Indeed, they seem to believe that all banks could expand simultaneously, resulting in each bank avoiding adverse clearing and loss of reserves. This situation cannot realistically occur. Each bank wishes to have a different risk/return profile. As a result, banks with different risk profile would not be expanding at the exact same time, resulting in the more aggressive ones losing reserves at the expense of the more conservative ones in the medium term, stopping their expansion. At this point, we get back to the case I (and they) made of what happens to over-expanding single banks.

- Finally, despite describing a banking system in which lending is built up on top of reserves (pages 3 and 4) and in which banks cannot over-expand due to reserve drains (pages 5 and 6), they still dare declaring that:

In reality, neither are reserves a binding constraint on lending, nor does the central bank fix the amount of reserves that are available. (page 2) (emphasis added)

I just don’t know what to say…

What do we learn from this piece? For one thing, those BoE economists do not believe in the endogenous money theory. This is self-explanatory in the mechanism described in pages 5 and 6. They clearly know that an individual bank cannot expand broad money by itself. They seem to admit that the central bank does not have the ability to provide reserves on demand (despite saying a couple of times that the BoE supplies them on demand, another apparent contradiction). Their only qualification is that this can happen when all banks simultaneously expand their lending. This is theoretically true but impossible in practice as I said above.

Why would the central bank not have the ability to provide those reserves on demand? Actually, it can. It’s just that there is no (or low) demand for those reserves. This is due to the central bank funding stigma, an absolutely key factor that is not referred to even once in this BoE paper. As a result, their description seems to lack something: if individual banks lack reserves to expand further, why aren’t they simply borrowing them from the central bank? By overlooking the stigma, their mechanism lacks a coherent whole.

This is how things work (in the absence of innovations that economise on reserves): money supply expansion is endogenous in the short-term. But any endogenous expansion will also lead to an endogenous contraction in the short-term. In the long-term, only an increase in the monetary base can expand broad money. Only central bank injections free of any stigma, such as OMO, can sustainably expand the monetary base by swapping assets for reserves without touching at banks’ funding structure.

I have a minor qualification to add to this mechanism though. The endogenous contraction does not necessarily always occur around the same time. A period of economic euphoria could well lead to lower risk expectations, allowing banks to reshape their funding structure and the liquidity of their balance sheet in a riskier way than usual before the natural contractionary process kicks in.

In the end, the few ‘ivory tower’ ideas that are present in this research paper make it look incoherent and internally inconsistent. Central banks are notorious for their intentional or unintentional twisting of economic reality and history (see this brand new article by George Selgin on the Fed misrepresenting its history and performance. Brilliant read), so we should always take everything they say with a pinch of salt.

Could P2P Lending help monetary policy break through the ‘2%-lower bound’?

The ‘cut the middle man’ effect of P2P lending is already celebrated for offering better rates to both lenders and borrowers. But what many people miss is that this effect could also ease the transmission mechanism of central banks’ monetary policy.

I recently explained that the banking channel of monetary policy was limited in its effects by banks’ fixed operational costs. I came up with the following simplified net profit equation for a bank that only relies on interest income on floating rate lending as a source of revenues:

Net Profit = f1(central bank rate) – f2(central bank rate) – Costs, with

f1(central bank rate) = interest income from lending

= central bank rate + margin and,

f2(central bank rate) = interest expense on deposits

= central bank rate – margin

(I strongly advise you to take a look at the details here, which was a follow-up to my response to Ben Southwood’s own response on the Adam Smith Institute blog to my original post…which was also a response to his own original post…)

Consequently, banks can only remain profitable (from an accounting point of view) if the differential between interest income and interest expense (i.e. the net interest income) is greater than their operational costs:

Net interest income >= Costs

When the central bank base rate falls below a certain threshold, f2 reaches zero and cannot fall any lower, while f1 continues to decrease. This is the margin compression effect.

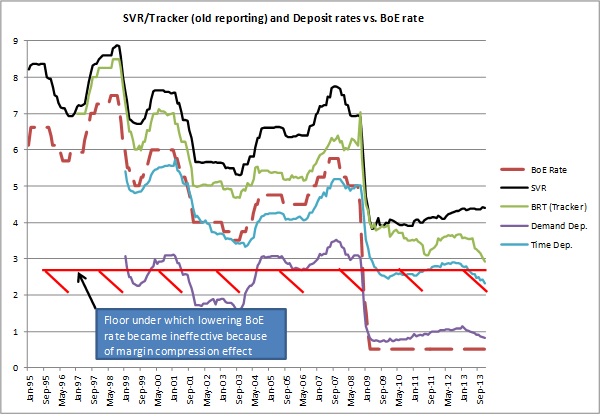

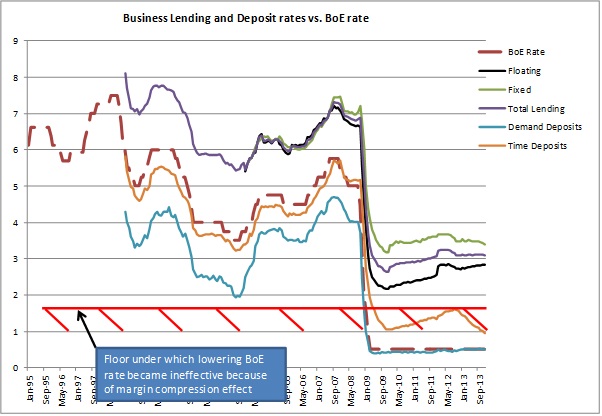

Above the threshold, the central bank base rate doesn’t matter much. Below, banks have to increase the margin on variable rate lending in order to cover their costs. This was evidenced by the following charts:

As the UK experience seems to show, banks stopped passing BoE rate cuts on to customers around a 2% BoE rate threshold. I called this phenomenon the ‘2%-lower bound’. I have yet to take a look at other countries.

Enter P2P lending.

By directly matching savers and borrowers and/or slicing and repackaging parts of loans, P2P platforms cut much of banks’ vital cost base. P2P platforms’ online infrastructure is much less cost-intensive than banks’ burdensome branch networks. As a result, it is well-known that both P2P savers and borrowers get better rates than at banks, by ‘cutting the middle man’. This is easy to explain using the equations described above, as costs approach zero in the P2P model. This is what Simon Cunningham called “the efficiency of Peer to Peer Lending”. As Simon describes:

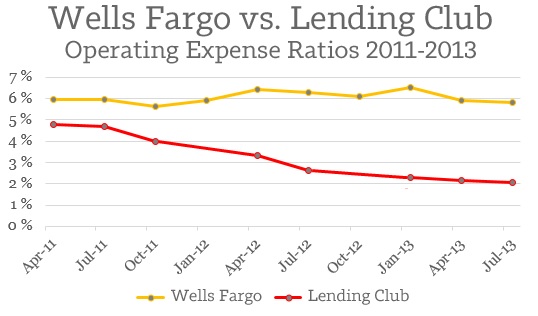

Looking purely at the numbers, Lending Club does business around 270% more efficiently than the comparable branch of a major American bank

Simon calculated the ‘efficiency’ of each type of lender by dividing the outstanding loans of Wells Fargo and Lending Club by their respective operational expenses (see chart below). I believe Lending Club’s efficiency is still way understated, though this would only become apparent as the platform grows. The marginal increase in lending made through P2P platforms necessitates almost no marginal increase in costs.

Perhaps P2P platforms’ disintermediation model could lubricate the banking channel of monetary policy the closer central banks’ base rate gets to the zero bound?

Possibly. From the charts above, we notice that the spread between savings rates and lending rates that banks require in order to cover their costs range from 2 to 3.5%. This is the cost of intermediation and maturity transformation. Banks hire experts to monitor borrowers and lending opportunities in-house and operate costly infrastructures as some of their liabilities (i.e. demand deposits) are part of the money supply and used by the payment system.

However, disintermediated demand and supply for loanable funds are (almost) unhampered by costs. As a result, the differential between borrowers and savers’ rate can theoretically be minimal, close to zero. That is, when the central bank lowers its target rate to 0%, banks’ deposit rates and short-term government debt yield should quickly follow. Time deposits and longer-dated government debt will remain slightly above that level. Savers would be incentivised to invest in P2P if the proposed rate at least matches them, adjusting for credit risk.

Let’s take an example: from the business lending chart above, we notice that business time deposit rates are currently quoted at around 1%. However, business lending is currently quoted at an average rate of about 3%. Banks generate income from this spread to pay salaries and other fixed costs, and to cover possible loan losses. Let’s now imagine that companies deposit their money in a time deposit-equivalent P2P product, yielding 1.5%. Theoretically, business lending could be cut to only slightly above 1.5%. This represents a much cheaper borrowing rate for borrowers.

P2P platforms would thus more closely follow the market process: the law of supply and demand. If most investments start yielding nothing, P2P would start attracting more investors through arbitrage, increasing the supply of loanable funds, and in turn lowering rates to the extent that they only cover credit risk.

The only limitation to this process stems from the nature of products offered by platforms. Floating rate products tend to be the most flexible and quickly follow changes in central banks’ rates. Fixed rate products, on the other hand, take some time to reprice, introducing a time lag in the implementation of monetary policy. I believe that most P2P products originated so far were fixed rate, though I could not seem to find any source to confirm that.

In the end, P2P lending is similar to market-based financing. The bond market already ‘cuts the middle man’, though there remains fees to underwriting banks, and only large firms can hope to issue bonds on the financial markets. In bond markets, investors exactly earn the coupon paid by borrowers. There is no differential as there is no middle man, unlike in banking. P2P platforms are, in a way, mini fixed-income markets that are accessible to a much broader range of borrowers and investors.

However, I view both bond markets and P2P lending as some version of 100%-reserve banking. While they could provide an increasingly large share of the credit supply, banks still have a role to play: their maturity transformation mechanism provides customers with a means of storing their money and accessing it whenever necessary. Would P2P platform start offering demand deposit accounts, their cost base would rise closer to that of banks, potentially raising the margin between savers and borrowers as described above.

It seems that, by partly shifting from the banking channel to the P2P channel over time, monetary policy could become more effective. I am sure that Yellen, Carney and Draghi will appreciate.

Bitcoin Burgers in London!

Walking in London yesterday, look at what I found near Bricklane:

This is genius 🙂

Congrats guys for democratising cryptocurrencies!

Regulating problems away doesn’t work

By ‘regulating’ the symptoms one does not cure the underlying disease. A few more examples in the press of this phenomenon that I keep describing:

– It’s no news that banks are being pressurised from all sides by regulation and lawsuits. The results? Banks aren’t that profitable anymore and remuneration stalls or even falls. Victory then? Wait a minute. Bloomberg reports that there is increased demand for young bankers by private equity funds, which are unsurprisingly more lightly regulated. This is part of a bigger trend that sees investors, funding and, as a result, credit, fleeing the traditional banking system towards the higher-yielding shadow banking system.

– The Economist also reports the same rebalancing towards shadow banking in China. I have already called China a ‘Spontaneous Finance Frankenstein’ given its strong, unnatural, regulatory-driven financial sector. This is typical:

China’s cap on deposit rates at banks is causing money to flood into shadow-banking products such as those offered by “trust” companies in search of higher yields. Offerings by internet firms, with their large existing customer bases, have opened the spigots wider. […]

Some see these online firms as a serious long-term threat to banks and the government’s ability to control the financial sector, prompting noisy demands (mostly by banks) to regulate the upstarts. Regulators have not yet expressed a clear view, but some observers see signals of a looming regulatory crackdown in attacks by the official media; a financial editor on the state-run television network recently branded online financial firms vampires and parasites.

What would be the effects of regulators successfully regulating those various areas of the shadow financial sector? A ‘shadow shadow’ banking sector would emerge. Liquidity, when in abundance, always finds its way. Regulation drives financial innovations, creating systemic risks through complex shadowy interlinked financial products and entities.

One does not regulate symptoms away. Market actors are the only natural, and the best, regulators.

Inside regulator trading

While some people keep praising the virtues of regulation on anything and everything (see Izabella Kaminska here on Bitcoin), a brand new study seems to picture a slightly less rosy view of regulators…

(This research was originally pointed by Lars Christensen on his blog and Facebook account. Thank you again Lars)

The abstract is telling:

We use a new data set obtained via a Freedom of Information Act request to investigate the trading strategies of the employees of the Securities and Exchange Commission (SEC). We find that a hedge portfolio that goes long on SEC employees’ buys and short on SEC employees’ sells earns positive and economically significant abnormal returns of (i) about 4 % per year for all securities in general; and (ii) about 8.5% in U.S. common stocks in particular. The abnormal returns stem not from the buys but from the sale of stock ahead of a decline in stock prices. We find that at least some of these SEC employee trading profits are information based, as they tend to divest (i) in the run-up to SEC enforcement actions; and (ii) in the interim period between a corporate insider’s paper-based filing of the sale of restricted stock with the SEC and the appearance of the electronic record of such sale online on EDGAR. These results raise questions about potential rent seeking activities of the regulator’s employees.

Wait. Do you mean that Securities and Exchange Commission employees are humans like anybody else, driven by their own sense of greed? Amazing.

A few absolutely striking facts were listed in this paper. The SEC lacked a system to monitor employees’ trades until… 2009. Despite the system implemented early 2009, employees seem to be able to avoid large losses by selling their holdings just before a negative SEC decision is announced. Moreover, previous research also found that politicians and congressmen benefited from insider trading… A law was passed in… 2012 to prevent them from trading on privileged information. 2012! They must be kidding. How late is that?! The logic seems to be: impose red tape on corporations ASAP but please do not affect rent-seeking and other benefits of government officials! The effectiveness of the law still has to be researched…

For sure there are some limitations to this paper and its methodology: the authors only effectively analysed 7,200 transactions out of a total of 29,081. This is because many transactions had invalid tickers (some were mutual funds but… how is even this possible for other securities?), were not traded on American exchanges or had very limited data due to illiquidity. Moreover, they couldn’t identify individual employees and as a result worked on an aggregate portfolio. It is also fair to admit that the ‘abnormal return on short positions’ actually didn’t generate any profit but only prevented losses, as they were not short sales but outright ones.

Still, independently of our view of insider trading (many people argue that it isn’t such a bad thing after all), such results are significant and should be further researched. Regulators like to portray themselves as being on a moral high ground, shaming those guilty of insider trading and other frauds. So the news that they may well succumb to the same temptation as those vulgar and immoral capitalist insiders not only sounds very ironic but also reaches extreme levels of cynicism.

As Lars said:

Who is regulating the regulators?

Recent Comments