The money multiplier is alive

Remember, just a few years ago when a number of economic bloggers tried to assure us, based on some misunderstandings, that banks didn’t lend out reserves and that the ‘money multiplier was dead’?

I wrote several posts explaining why those views were wrong, from debunking endogenous money theory, to highlighting that a low multiplier did not imply that it, and the basis of fractional reserve theory, was ‘dead’.

Even within the economic community that still believed in the money multiplier, there were highly unrealistic (and pessimistic) expectations: high (if not hyper) inflation would strike within a few years we were being told, as the first round of quantitative easing was announced. Of course those views were also wrong: the banking system cannot immediately adjust to a large injection of reserves; even absent interest on excess reserves, it takes decades for new reserves to expand the money supply as lending opportunities are limited at a given point in time.

A few years later, it is time for those claims to face scrutiny. So let’s take a look at what really happened to the US banking system.

This is the M2 multiplier:

As already pointed out several years ago, the multiplier is low; much lower than it used to be between 1980 and 2009. But it is not unusual and this pattern already happened during the Great Depression. See below:

Similarly to the post-Depression years, the multiplier is now increasing again.

Let’s zoom in:

Since the end of QE3, the M2 multiplier in the US has increased from 2.9 to 3.7 in barely more than three years. This actually represents a much faster expansion than that followed the Great Depression: between 1940 and 1950, it increased from 2.5 to 3.5, and from 1950 to 1960, it increased from 3.5 to 4.2.

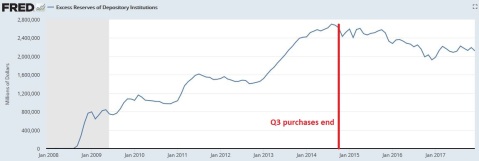

Unsurprisingly, this increase occurred as excess reserves finally started to decline sustainably:

As we all know, following the 1950s, the multiplier eventually went on increasing for a couple more decades, reaching highs during the stagflation of the 1970s and early 1980s. Unless a new major crisis strikes, it is likely that our multiplier will follow the same trajectory, although I am a little worried about the rapid pace at which it is currently increasing. One thing is certain: the money multiplier is alive and well.

A boring story of critical Basel risk-weight differentials

After years of negotiations, international banking regulators have finally come up with an apparent finalisation of Basel 3 standards. Warning: this post is going to be quite technical, and clearly not as exciting as topics such as monetary policy. But in order to understand the fundamental weaknesses of the banking system, it is critical to understand the details of its inner mechanical structure. This is where the Devil is, as they say.

The main, and potentially worrying, evolution of the standards is the

aggregate output floor, which will ensure that banks’ risk-weighted assets (RWAs) generated by internal models are no lower than 72.5% of RWAs as calculated by the Basel III framework’s standardised approaches. Banks will also be required to disclose their RWAs based on these standardised approaches.

What does this imply in practice? A while ago, I described the various methods under which banks were allowed to calculate their ‘risk-weighted assets’, which represent the denominator in their regulatory capitalisation formula:

Banks can calculate the risk-weighs they apply to their assets based on a few different methodologies since the introduction of Basel 2 in the years prior to the crisis. Under the ‘Standardised Method’ (which is similar to Basel 1), risk-weights are defined by regulation. Under the ‘Internal Rating Based’ method, banks can calculate their risk-weights based on internal model calculations. Under IRB, models estimate probability of default (PD), loss given default (LGD), and exposure at default (EAD). IRB is subdivided between Foundation IRB (banks only estimate PD while the two other parameters are provided by regulators) and Advanced IRB (banks use their own estimate of those three parameters). Typically, small banks use the Standardised Method, medium-sized banks F-IRB and large banks A-IRB. Basel 2 wasn’t implemented in the US before the crisis and was only progressively implemented in Europe in the few years preceding the crisis.

While Basel 3 did not make any significant change to those methods, at least in the case of credit risk, regulators have argued for years about the possibility of tightening the flexibility given to banks under IRB.

As followers of this blog already know, I view Basel’s RWA concept as one of the most critical factors which triggered the build-up of financial imbalances that led to the financial crisis. In particular Basel 1 – in place until the mid-2000s in the US – only provided fixed risk-weights – and therefore incentives for bankers to optimise their return per unit of equity by investing in asset classes benefiting from low risk-weights (i.e. real estate, securitised products, OECD sovereign exposures…). This in turn distorted the allocation of capital in the economy out of line with the long-term plan of economic actors.

Since the introduction of IRB and internal models by Basel 2, it has been uncertain whether banks using their own models to calculate risk-weights made it more or less likely for misallocations to develop in a systemic manner. There are two opposing views.

On the one hand, more calculations flexibility can give banks the opportunity to reduce the previously artificially-large risk-weight differential between mortgage and business lending for example, thereby reducing the potential for regulatory-induced misallocation and representing a state of affairs closer to what a free market would look like.

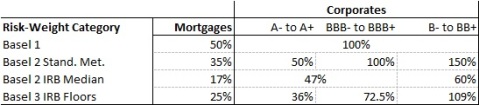

On the other hand, there are also instances of banks mostly ‘gaming’ the system with regulators’ support. Those banks usually understand that regulators see real estate/mortgage lending as safer than other types of activities and consequently attempt to push risk-weights on such lending as low as possible. This often succeeds and gains regulatory approval, and it is not a rare sight to see mortgages being risk-weighted around 10% of their balance sheet value (vs. 50% in Basel 1 and 35% in Basel 2’s standardised method). If they do not succeed in lowering risk-weights on business lending by the same margin, this exacerbates the differential between the two types of activities and adds further incentives for banks to grow their real estate lending business at the expense of more productive lending to private corporations.

Now Basel 3 is finally introducing floor to banks’ internal models. The era of the 10% risk-weighted mortgage has come to an end. Once fully applied, asset classes’ risk weights will not be allowed to be lower than 72.5% of the standardised approach value. Unless I am mistaken, this seems to imply a minimum of about 25% for residential mortgages.

Now whether this is good or bad depends on our starting point. If banks, on aggregate, tended to game the system, amplifying the differential vs. the free market, then this floor is likely to reduce the difference between low and high risk-weight asset classes. However, if on aggregate internal models’ flexibility represented an improvement vs. Basel’s rigid calculation methods, then this new approach will tend to deteriorate the capital allocation capabilities of the banking system.

Indeed, the critical concept here is the differential between Basel and the free market. A free market would also take a view as to how much capital a free banking system should maintain against certain types of exposures. While there would be no risk-weight, market actors would have an average view as to the safe level of leverage that free banks should have according to the structure of their balance sheet. In order to simplify this concept of capital requirements in a free market for this post, we can translate this view into a ‘free market risk-weight-equivalent’. Perhaps I’ll write a more elaborate demonstration another time.

So let’s assume a free market in which, on average, mortgages are risk-weighted at 40%, lending to large international firms at 50% and to SMEs at 70%. As this represents a free market ‘equilibrium’, there is no distortion in the allocation of loanable funds. Both corporate and mortgage banks are able to cover their cost of capital at the margin.

Now some newly-designed regulatory framework called, well… Bern (let’s stick to Swiss cities), comes to the conclusion that mortgages should be risk-weighted 50%, and lending to any corporation 100%. While this represents an increase in the case of all types of exposure, the differential between mortgages and corporations is now 50%, whereas it used to be just 10% and 30% under the free market. As a result, bankers whose specialty was corporate lending will have to adjust the structure of their balance sheet if they wish to maintain the same level of profitability. Corporate lending volume is likely to decline as the least profitable lending opportunities at the margin are not renewed as they now do not cover their cost of capital anymore. The outcome of this alteration in risk-weight hierarchy is a reduction in the supply of loanable funds towards the most capital-intensive asset classes. This reduction potentially leads to unused (or ‘excess’) bank reserves released on the interbank market, lowering funding costs and making it possible to profitably extend credit to marginal borrowers within the ‘cheapest’ (from a capital perspective) asset classes.

So this latest Basel reform, good or bad? Existing research is unclear. As I reported in a previous post, researchers found a set of results that seemed to confirm that German banks on aggregate tended to ‘game’ the system using regulatory-validated internal models. However, Germany is a very peculiar and unique banking market and this result may not apply everywhere, and this research doesn’t tell much about the differential described above.

Another research piece published by the BIS showed some confusing results. Among a portfolio of large banks surveyed by the BIS, median risk-weights on mortgages were down to a mere 17%, whereas median SME corporate lending stood at 60% and large corporate lending 47%. Clearly mortgage lending represented the easiest way for banks on aggregate to optimise their RoE, and it does look like the banks surveyed tried to push risk-weights as low as possible in a number of cases.

We could argue that those risk-weights are too low for all those lending categories and therefore endanger the resilience of the banking system. This is indeed possible, but not my point today.

Today, I am not interested in looking at the absolute required amounts of capital that should be held against exposures, but at the relative amounts of capital across types of exposures. I am exclusively focusing on loanable fund allocation within the economic system as a whole. From a systemic point of view, risk-weight differentials matter considerably as explained above.

Basel 1’s risk weight for all corporate exposures stood at 100%, while Basel 2’s were more granular, with 50% for corporations rated between A- and A+, 100% between BBB- and BBB+ and 150% between B- and BB+. This rating spectrum covers the vast majority of small to large companies.

Now look at the differentials. The differentials in risk-weight between the Standardised Method and IRB for an average large industrial company rated in the BBB-range and an average SME rated in the BB-range are respectively 53% and 90%. Between mortgages and the same average corporates under IRB? 30% and 43%, whereas it used to be 65% and 115% under the rigid Basel framework. No wonder business lending growth started slowing down to the benefit of real estate lending since the introduction of Basel.

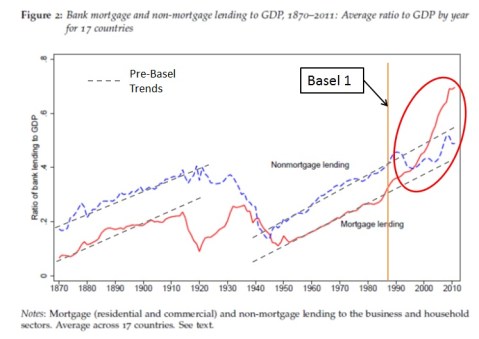

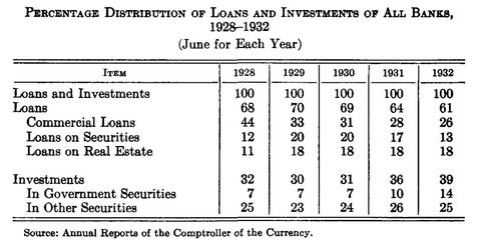

How will Basel’s ‘output floors’ affect those differentials? Here again it is hard to say. If the asset class differentials seen under IRB represented those that would be prevalent in a free market, then Basel’s new output floor is a big step backwards. My intuition indeed tells me that IRB was an improvement: banks’ balance sheet mostly comprised commercial loans in the past (see chart above and the table below on US banks from C.A. Phillips ‘Banking and the Business Cycle), and it looks highly unlikely that bankers would held two, three or four times more capital against those loans as against mortgages or sovereign exposures. Seen this way, this latest Basel twist is bad news.

PS: while most economists and virtually all politicians are unaware of the potentially devastating effects of their bank capital requirements alchemy, they do understand that lowering risk-weights/capital requirements on some types of exposures has the effect of boosting them.

Politicians’ latest brilliant idea? Lower requirements for ‘climate financing’ “in a bid to boost the green economy and counter climate change.” Perhaps time they looked at the overall picture and start wondering how on Earth real estate markets, securitised products and sovereign debt are so attractive to the financial sector?

Back to blogging, and to Basel’s latest twists

After a very long break, I finally decided to start blogging again. This break was due to a very busy lifestyle since last summer: getting back home at 11pm on most week days is not necessarily conducive to quality blogging. As a result of the combination of high workloads and plenty of other activities, and with high level of exhaustion as a result, I realised that blogging was at the bottom end of my list of priorities. On my few free weekends, the few hours of relaxation I could get became a much more appealing option.

Moreover, the post-crisis debate around banking theory and regulation had almost vanished from social and mainstream media amid the benign economic environment. The publication frequency of interesting economic research pieces and other thought-provoking economic commentaries had also declined sharply. There wasn’t much to fight for as there was no one to debate. Not even an endogenous money theorist in sight. Motivation was low.

This state of affairs couldn’t last of course. The accumulation of regulatory news and some (admittedly limited) renewed attacks against free markets and banking on social media were enough to reignite my motivation and finally force me to find enough time to put together a few posts. \My non-blogging activities remain pretty time-consuming; therefore posts are likely to be few and far between.

So where to start? The (apparently) final and long-awaited completion of the new Basel 3 rulebook has been recently published. While I was originally planning to dissect some of its features in this post, it rapidly became clear that a whole separate publication was necessary. So there you go: tomorrow I’ll publish another post on my favourite topic, Basel regulations. And it will be wonkish.

Recent Comments