April fools and risk-weights

The Basel regulatory framework might look like a bad April fool. On the 1st of April (you couldn’t make that up) the BIS published a document reviewing the practices and average risk-weights applied to various types of assets by large banks. Since the introduction of Basel 2, large banks usually utilise the IRB framework, or ‘Internal-rating based’, which allows them to calculate their own risk-weight, which are then used to compute their regulatory capital ratio. Other banks use risk-weights directly provided by Basel (under Basel 1, all banks used fixed risk-weights).

One could believe that giving banks the ability to define their own risk-weight is a good thing, as it mimics a free market setting (i.e. banks rather than regulatory directives deciding how much capital they need to keep aside). Unfortunately it isn’t. Regulators verify banks’ models and validate them. The consequence of this is that banks attempt to benefit from this by amplifying the differential between what regulators usually view as risky and safe assets.

This is where the BIS paper comes in. It demonstrates the extent of risk-weight gaming among large international banks. The table below shows that median risk-weight on mortgage lending is 17%, whereas median SME corporate lending is 60% and large corporate lending 47%. Given that interest rates on corporate lending is usually not much higher (and sometimes lower, see this earlier analysis on the ECB’s TLTRO) than interest rates charged on mortgage lending, it is not surprising to see banks’ favouring real estate lending: it is much more efficient per unit of capital. Call this capital, or RoE, optimisation.

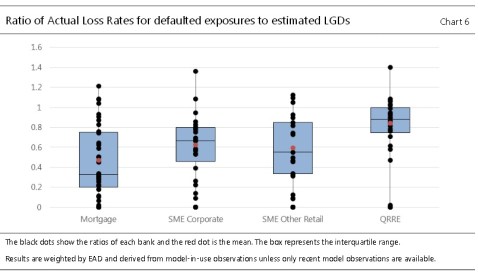

There are quite a few other interesting charts in this publication, see the following one:

This chart shows that actual loss rates on defaulted exposures aren’t much higher for small corporate lending than for mortgage lending. This adds to the increasing amount of evidence that nothing justifies Basel’s and regulators’ much higher capital requirements for corporate exposures. Other charts the paper provides seem to confirm this view.

Finally, the paper also looks at the new Basel 3 leverage ratio, which was supposed to avoid capital gaming by getting rid of risk-weights altogether, hence becoming a ‘backstop’ ratio. Ironically, Basel geniuses reintroduced risk-weights into the leverage ratio, but under another form: credit conversion factors (CCF). CCF essentially provide various risk-weights for various types of off-balance sheet products and commitments (see pages 18 and 19 of this document). Consequently, banks’ lending decisions also become affected by CCF… Here again you couldn’t make it up. The paper provides various implied CCF used by large banks, although by asset class rather than by product type.

PS: I wrote another post on the topic of risk-weight gaming about a year ago here.

PPS: There was a good article on shareholder value in The Economist, reminiscent of some of my own arguments.

Update: SNL reports that the BIS is thinking of preventing large banks to use their own IRB models to calculate risk-weights on loans to other loans and larger corporations. It’s not going to solve anything.

2 responses to “April fools and risk-weights”

Trackbacks / Pingbacks

- - 8 January, 2018

Leave a comment

Recent Comments

| pslebow on ‘Sovereign money’:… | |

| pslebow on A critique of Werner’s view on… | |

| Hugo Kramer on Welcome to Spontaneous Fi… | |

| Nathan on A critique of Werner’s view on… | |

| Nathan on More, more, more money endogen… |

The regulators by assigning a risk weight of 20% to AAA rated assets and 150% to those rated below BB-, evidence they have no understanding about what is really risky to the banking system.

http://bit.ly/1TgB6EJ