Banks don’t lend out reserves. Or do they?

Over the last weeks/months there has been a lot of agitation in some circles of the financial blogosphere: are banks lending out their reserves? The matter might sound trivial, but it theoretically impacts various monetary policies, such as quantitative easing. I won’t speak about that here. For those of you who don’t know what reserves are, here is a quick reminder:

The money supply comprises several elements. To make things simple the monetary base is the ‘real’ money (remnants of the gold standard and since then, created by the central bank) and the rest of the money supply is some sort of credit money created by the banking system. The ‘real’ money (monetary base) is also what we call high-powered money, and comprises both physical cash and… reserves held by banks at their respective central banks. Credit money created by banks is actually a claim on high-powered money, or high-powered money substitute. Reserves are convertible into physical cash and vice versa. In the UK, the monetary base represents about 17% of M4 (a measure of the money supply that does not include reserves). Reserves represent 82% of the monetary base.

Frances Coppola keeps reiterating again, and again, and again, and sometimes again, that banks don’t lend out reserves. She wrote her latest piece on the topic last week on the Forbes website. The title couldn’t be clearer: “Banks Don’t Lend Out Reserves”

A simple question that could come to anyone’s mind is: what do banks lend out then?

To be honest, I think that a large part of the misunderstanding comes from semantics. I actually agree with Frances on a number of points she makes. I have some objections to her ‘extreme’ view, or at least ‘extreme semantics’. Things aren’t that clear-cut.

While the endogenous money view suffers in my opinion from fallacy of composition, it looked to me at first that the view that banks don’t lend out their reserves suffered from the converse fallacy, the fallacy of division. But it doesn’t look like Frances falls in that trap, given what she made clear in the comment section of her article.

To be clear, banks do need reserves. If a (single) bank makes a loan to a customer, the bank is going to increase both its assets and its deposits (liabilities) by the amount of the loan. So far it does seem that the bank has created money out of thin air. But what happens if the customer withdraws the money from the bank? Deposits will get back to their previous amount, creating a discrepancy with the total loan figure. At the same time, there will be a drain on the bank’s reserves equal to the amount of the loan, as reserves will have been converted into physical cash (while total high-powered money remained the same). Seen this way, we could probably say that banks do lend out reserves.

What happens if the customer doesn’t withdraw the money but pays with it for a good by bank transfer? The drain on reserves still occurs as the beneficiary bank knocks on the door of the borrower’s bank to get hold of the money. In this case again, we could probably say that banks do lend out reserves.

The borrower’s bank also sees its deposits decrease while, on the other hand, the beneficiary bank experiences a deposit and reserves inflow. As a result, its deposit base grows without lending beforehand. Its now increased reserves will allow it to invest or lend more. This clearly nuances Frances’ claim that

when a bank creates a new loan, it also creates a new balancing deposit. It creates this “from thin air”, not from existing money: banks do not “lend out” existing deposits, as is commonly thought.

As we can see, reserves are used for two things: cash withdrawals and interbank settlements.

Let’s now consider the banking system as a whole in a closed economy. If lending leads to cash withdrawals, we could say again that banks lend out their reserves. However, let’s consider the following case: nobody ever withdraws cash. In this situation, all payments are made by electronic bank transfer. While individual banks experience fluctuations in their reserves, the total amount of reserves in the system never changes. Here, we could say that, indeed, banks don’t lend out reserves.

Here is what I meant by fallacy of division: what is true of the system as a whole isn’t for individual banks.

But so far, apart from semantic issues, I think that Frances and I agree although I wish she were more precise in differentiating single banks from the banking system as a whole. However, what I (kind of) disagree with is about her treatment of reserves as a source (or not) of lending and deposit creation. Frances says:

The volume of excess reserves in the system is what it is, and banks cannot reduce it by lending. […]

The volume of excess reserves in the system is what it is, and banks cannot reduce it by lending. They could reduce excess reserves by converting them to physical cash, but that would simply exchange one safe asset (reserves) for another (cash). It would make no difference whatsoever to their ability to lend. Only the Fed can reduce the amount of base money (cash + reserves) in circulation. While it continues to buy assets from private sector investors, excess reserves will continue to increase and the gap between loans and deposits will continue to widen.

This is something I cannot agree with. She is right to say that reserves will permanently be higher than before they were created (at least until the central bank tries to destroy them one way or another). But she overlooks the multiplier effect on lending and deposit expansion.

Assuming no reserve requirements, a fractional reserve bank will estimate how much high-powered money it needs to retain in order to face withdrawals and settlements. It is well-documented that banks in free banking systems naturally maintained reserves. Let’s assume that a whole banking system estimated that it needed to maintain 10% of the amount of its deposits as reserves to face settlements and withdrawals without endangering its existence. This would de facto become an internally-defined reserve requirement. The system can now create a maximum amount of demand deposits (claims on high-powered money) equal to 1/RR = 1/0.10 = 10 times the amount of reserves in its vaults*.

Now let’s get back to the situation described in Frances’ article. Reserves have been created, but have not been ‘lent out’ apparently. Of course, as Frances said, those reserves will not leave the system, unless they are withdrawn. But, they theoretically do provide banks with the ability to create extra deposits ‘out of thin air’ (the pyramiding process), allowing them to maintain their pre-crisis reserves to deposits ratio. And, as deposits expand, the reserves would not disappear but would simply not be considered ‘in excess’ anymore…

The question becomes: why didn’t banks expand their loans and deposit base in line with the increase in reserves? According to the chart below, the M2 multiplier (obtained by dividing all demand and saving deposits by the monetary base), declined significantly when the Fed started its quantitative easing policies.

I don’t think anybody has a clear answer to this. Low demand for loans, the Fed now paying interests on excess reserves, maintenance of precautionary excess reserves to face a possible future liquidity squeeze as long as the crisis isn’t completely over, are some of the possible underlying reasons. From my experience, the third reason is highly likely. I’ve heard many banking executives over the past few years who made clear that they were temporarily hoarding extra cash and reserves not to lend but… “just in case”.

* This multiplier is obviously a very simple one. Chester A. Phillips, in its famous 1921 book Bank Credit, identified the maximum amount x that can be lent out as:

, with c being the amount of reserves deposited, r the reserve/deposit ratio and k the derivative deposit/loan ratio (derivative deposits being the amount of newly-created deposits by lending that are not withdrawn or transferred by the depositors).

, with c being the amount of reserves deposited, r the reserve/deposit ratio and k the derivative deposit/loan ratio (derivative deposits being the amount of newly-created deposits by lending that are not withdrawn or transferred by the depositors).

In 1984, Alex Mcleod also wrote a brilliant, but barely readable, book called Principles of Financial Intermediation. He covers pretty much all possible and theoretical cases involving credit expansion based on the public’s acceptance ratio for claims (notes and deposits) on ‘money proper’, reserve to deposit ratio of financial intermediaries, external drain in case of an open economy, simple, cross and compound pyramiding (when the claims on money of one or several institutions can be used as reserves by other institutions)… There is no way I can reproduce his massive equations here…

Moreover, things get even more complex when you add in secondary reserves (very liquid low-yielding financial instruments almost instantly convertible into cash), as well as technology and financial innovations that allow banks to economise on reserves.

We are now in a micromanaged economy

Interesting piece from Matt Levine on Bloomberg on Wednesday. It highlights how far regulators are now going to micromanage the financial system. They now prevent banks from lending to private equity firms (so-called ‘leveraged loans’), distorting lending mechanisms, market pricing and economic agents’ learning process. The whole scheme is subject to potential arbitrage and could possibly lead to even more devastating opaque financial engineering.

Some of my friends (senior bankers working in financial institutions mergers and acquisitions at other banks) recently told me that regulators prevent their clients (banks) from trying to acquire any other banks. Nonetheless, during the crisis, regulators almost forced, or at the very least engineered, banks mergers…Does anybody still believe we are in a free market?

This is a regulator:

The impact on private equity, a significant driver of what we see as risky practices, is an intended consequence of our actions,” Martin Pfinsgraff, the OCC’s senior deputy comptroller for large-bank supervision, said in an interview. “As regulators, we certainly hope to change bad practices and remove the extraordinary froth that’s experienced at the peak of a credit cycle. If we can mitigate that, it reduces the size of the valley to follow.

A suggestion to this person: why don’t you become a banker? It looks like you know better than bankers how to safely pick counterparties to lend to. Moreover, what he does not realise is that by restraining the flow of credit somewhere, it’s going to reappear somewhere else, shifting systemic risk to another (and possibly darker) corner of the economy.

Forcing banks: to add a bit of capital there and there and some liquidity here, to consider which assets are safe and liquid and which aren’t, to trade some products through specific counterparties, not to acquire competitors, to force the acquisition of competitors, and so on, was not enough. Regulators have now introduced another new tool and earned another power. Moreover, in their quest to make the banking system ‘safer’, regulators are likely to make it more vulnerable: banks will become less differentiated, holding the same types of assets, lending to the same types of clients, having the same types of internal models and engaged in the same types of trading activities. I let you guess what happens when those regulatory-favoured activities collapse.

Exactly 70 years after Hayek’s The Road to Serfdom was published, it looks like we’re back to the same point.

Photo: HR People

A UK housing bubble? Sam Bowman doubts it

On the Adam Smith Institute’s blog, Sam Bowman had a couple of posts (here and a follow-up here, and mentioned by Lars Christensen here) attempting to explain that there might not have been any house price bubble in the UK. He essentially says that there was no oversupply of housing in the 1990s and 2000s. Here’s Sam:

These charts show that housing construction was actually well below historical levels in the 1990s and 2000s, both in absolute terms and relative to population. It is difficult to see how someone could claim that the 2008 bust was caused by too many resources flowing toward housing and subsequently needing time to reallocate if there was no bubble in housing to begin with.

What this suggests is that the Austrian story about the crisis may be wrong in the UK (and, if Nunes’s graphs are right, the US as well). The Hayek-Mises story of boom and bust is not just about rises in the price of housing: it is about malinvestments, or distortions to the structure of production, that come about when relative prices are distorted by credit expansion.

Well, I think this is not that simple. Let me explain.

First, the Hayek/Mises theory does not apply directly to housing. In the UK, there are tons of reasons, both physical and legal, why housing supply is restricted. As a result, increased demand does not automatically translate into increased supply, unlike in Spain, which seems to have lower restrictions as shown by the housing start chart below:

Second, Sam overlooks what happened to commercial real estate. There was indeed a CRE boom in the UK and CRE was the main cause of losses for many banks during the crisis (unlike residential property, whose losses remained relatively limited).

Third, the UK is also characterised by a lot of foreign buyers, who do not live in the UK and hence not included in the population figures. Low rates on mortgages help them purchase properties, pushing up prices, triggering a reinforcing trend while supply in the demanded areas often cannot catch up.

Fourth, the impact of Basel regulations seems to be slightly downplayed. Coincidence or not, the first ‘bubble’ (in the 1980s) appeared right when Basel’s Risk Weighted Assets were introduced. And it is ‘curious’, to say the least, that many countries experienced the same trend at around the same time. Would house lending and house prices have increased that much if those rules had never been implemented? I guess not, as I have explained many times. I have yet to write posts on what happened in several countries. I’ll do it as soon as I find some time.

I recommend you to take a look at my RWA-based Austrian Business Cycle Theory, which seems to show that, while there should indeed be long-term real estate projects started (depending on local constraints of course), there is also an indirect distortion of the capital structure of the non-real estate sector.

While there may well be ‘real’ factors pushing up real estate prices in the UK, there also seems to be regulatory and monetary policy factors exacerbating the rise.

- Chart 1: Spanish Property Insight

- Chart 2: FT Alphaville

- Chart 3: Guardian

Mises’ Theory of Money and Credit, Funding Valuation Adjustment and other stuff

Quick post today. A few interesting Austrian economics links first.

Liberty Fund is hosting an interesting debate on Ludwig von Mises’ Theory of Money and Credit. I read that book in 2012, a 100 years after it was released and for its 101 years, Lawrence White is writing an interesting review of what he thinks was original and/or revolutionary in this work. Liberty Fund also asked a few other economists to comment on White’s article and on Mises’ book: Jörg Guido Hülsmann, Jeffrey Rogers Hummel, and George Selgin. They reply to each other so the debate is constantly evolving, which is cool.

The Bastiat blog of the Mises Institute advertised the Austrians in Finance LinkedIn group. Good opportunity to network with fellow Austrians working in financial services. I actually didn’t know that group before, so I just joined!

Bob Murphy had a funny post a few days ago about… the von Mises yield curve! Sounds financial, which would be logical given Mises’ work, but it is actually about material physics… And the theory’s author wasn’t Ludwig von Mises but Richard von Mises. They were contemporaries and the theory was formulated in 1913, just one year after The Theory of Money and Credit was published!

Finally, nothing to do with Mises or Austrian economics, but here is an interesting link for the (possibly very) few of you who analyse banks and would be interested in finding out more about Funding Value Adjustment (FVA). FVA is the new fashionable accounting tool used by some investments bank to help value their derivatives portfolio. JP Morgan reported a… USD1.5bn loss after implementing FVA last week, making people wonder where all those new acronyms came from and how they could lead to such losses out of nowhere. Deutsche Bank also reported a EUR623m charge related to FVA, as well as DVA and CVA (debt and credit valuation adjustments, now ‘famous’, unlike their ‘new’ little brother).

Diagram: Wikipedia

The bank branch is dying. Some politicians don’t seem to get it

Technology is both a curse and a blessing for banks. It usually starts as a curse and ends up being a blessing (at least for the banks that eventually managed to master technological disruptions). I’ve personally argued several times during BarcampBank debates that the branch was outdated. The rebuttal I usually got (especially from French financial actors and entrepreneurs, probably a cultural thing) is that customers want to ‘feel’ some humanity, and not interact with some faceless system. I don’t disagree, but I would argue that they are massively overestimating the ‘humanity’ factor. What people want is convenience.

‘Humanity’ is just an inefficient way of providing convenient services to customers. When your services and IT systems aren’t convenient and instinctive enough for customers to use easily, they will naturally seek human help and reassurance. Does it mean customers necessarily want ‘access to other humans’ for most of their banking transactions? No. What it does mean it that banks don’t have straightforward enough and easy-to-use systems.

So here I reiterate: branches are outdated. And, once again, it is both a curse and a blessing for banks. For now, it is a curse: the retail banking business of most (large) banks is plagued by an unsustainable cost/income ratio (often around 70%+ when it should be closer to 50). The internet revolution led banks to open websites but not to close branches: branches were still the primary medium through which they could attract depositors (hence funding). Having a branch near potential customers’ home was crucial in order to both obtain funding and revenues. Internet obviously changes everything. But with a lag. Young people quickly get used to utilising internet websites for shopping and banking, but don’t have the financial resources that drive banking revenues. On the other hand, older customers are much slower to keep up with the trend. Some of the very first internet banks, like UK’s Egg, were not as successful as expected as a result.

Now that mainstream internet use has been among us for around 15 years, much more customers use online services, including banking, and former early adopter but resource-poor students are now working professionals. Smartphones have compounded the trend. Brett King has extensively described the possible functions of a branch in the 21st century and documented the various trends in customer preferences in his Bank 2.0 and Bank 3.0 books. Mobile banking is booming and banks are at last starting to react. Over the last year, banks have followed each other in announcing reductions in their branch network, something that would have been unimaginable just a few years ago. In the US, banks are axing branches, the latest in line being Bank of America. In the UK, Barclays referred to branch closures as a ‘necessity’ at the end of last year. RBS and HSBC have also announced branch closures. In the rest of Europe, the trend is the same (see Belgian and French banks for instance). The other part of the curse is that banks do have to heavily invest in IT to catch up with the trend. And I am not even mentioning unions’ rejection of the branch axing plans, which indeed involve jobs cutting.

The blessing part of the story is that, while banks are constrained by increasing compliance costs and fall of revenues due to new regulations, smaller branch networks also means reduced cost bases. Bankers, desperate to improve their single-digit RoE can only welcome the change in the medium-term. More profitable banks also mean more flexible and more robust banks.

But. Some (most?) politicians don’t seem to get it. The UK’s Labour party came up with a brand new ‘brilliant’ idea to end the dominance of the largest retail banks of the country: a cap on the number (market share) of branches. As they are saying:

We are not asking whether existing banks might have to divest themselves of a significant number of branches. We are asking how we make that happen.

Well, you know what guys? It’s already happening. 21st century technological disruption does not require 20th century reasoning. Yet many professional politicians seem to have been blessed with the very skill of thinking using ‘previous century logic’. Politicians, please back away and let technology implement more efficient measures than anything you would have ever been able to plan.

PS: One of my (unrealistic at the moment) proposals was that alternative and independent interbank ‘superbranches’ could appear, gathering services/ATMs from all high-street banks under the same roof. This place would effectively be for banks what UK-based Carphone Warehouse and its competitors are for mobile phone providers. Banks would be a big step closer to being virtual service-providers and customers could potentially switch almost at will, intensifying competition. That would be a revolution.

PPS: Other technological disruptions I didn’t mention in the post were P2P-lending and associated services. This is also a big challenge but requires different responses, although some of the issues are interlinked.

- Chart 1: The Bankwatch, McKinsey

- Chart 2: McKinsey, The Triple Transformation, p. 33

- Chart 3: Mobility Enterprise

The central bank funding stigma

Yesterday the Federal Reserve Bank of New York published a brand new study about the stigma associated with banks borrowing from the central bank’s discount window. That was a nice coincidence following my response to Scott Fullwiler on the MMT and endogenous money theory, which seems to ignore this stigma (or at least to downplay its impact) and to consider that banks freely borrow from the central bank, providing a perfectly elastic high-powered money (reserves) supply. On the contrary, in my view, the stigma is one of the fundamental reasons that undermine the endogenous money theory.

Essentially, the NY Fed does not see much reason for this stigma to exist, but acknowledges that it does exist… I think they entirely forgot the possible impacts on a bank and its stakeholders of being considered illiquid, which I described in my previous post. Nonetheless, they made some good points (see below). A key point in my opinion is that banks are willing to pay more for other sources of funding than use the cheaper discount window.

The four main hypotheses they tested were very US-centric but interesting nonetheless. They found that:

- Banks inside the New York District were 14% less likely to experience the stigma than banks outside of the district (admittedly not that much difference)

- Foreign banks were 28% more likely to experience the stigma than similar US peers

- The largest the financial markets disruption, the higher the stigma

- The stigma does not decline when more banks utilise the discount window

Photo: MoneyAware

Risk-weighted assets and capital manipulations

As some of you might have noticed, the Bank of International Settlements published yesterday the final version of the Basel III leverage ratio (official report can be found here). This ratio is a measure of the capitalisation of a bank for regulatory purposes. I have already mentioned a few times those capital ratios. Since the first Basel regulations were introduced, capital ratios were based on risk-weighted assets (RWAs). Some of you might already be aware of my ‘love’ of RWAs… The leverage ratio, on the other hand, gets rid of RWAs.

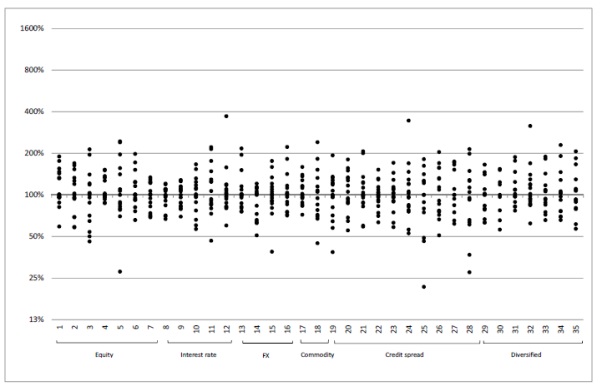

I am not going to speak about the leverage ratio here. But about other two other related BIS studies that, in a way, legitimate the use of unweighted capital ratios. In January 2013, the BIS published a first analysis of market RWAs. They tried to estimate the variability of risk-weights associated to equivalent securities across banks. The BIS provided 26 portfolios of financial securities to 16 different banks and asked them to risk-weigh them according to their internal models. The results were shocking (but not surprising).

Banks mostly assess market risks using statistical Value-at-Risk models. The graph below shows the dispersion of the results provided by the banks’ VaR models. The results are normalised so that the median result is centred on 100%.

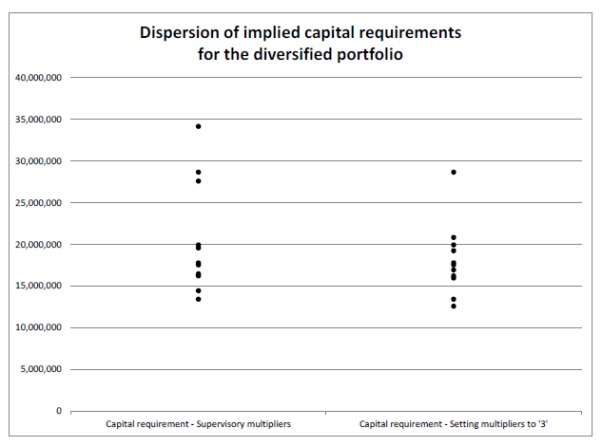

The dispersion is huge. Some banks judged portfolio 14 as being around 1000% riskier than the median bank’s perception of it (and I am not even talking about the most conservative one). Some comfort could be taken from the diversified portfolios (25 and 26), which are closer to real life portfolios. Nonetheless, even in those, variations are large enough to undermine the credibility of the risk-weights applied to them. The chart below demonstrates the capital requirements (in Euros) implied from the VaR results above for portfolio 25. Some banks would put aside more than twice the amount of capital than others would, for the same portfolio of securities.

The BIS believed at that time that different local regulatory requirements were partially responsible for the results (such as some banks following Basel 2.5 and others Basel 2. I’m going to skip the details but Basel 2.5 pushes market RWAs up).

The BIS eventually published its final study on market RWA at the end of December. This time, all banks had implemented Basel 2.5. So most of the observed variation could only come from the banks’ internal model differences. What did they find?

Not much difference. Variations were still huge. The resulting implied capital requirements (in thousands of Euros) for portfolios 29 and 30 were as follows:

Clearly, RWAs are unreliable. This questions the very utility of RWA-based regulatory capital ratios. How can one actually trust two different banks both reporting 10% Tier 1 ratios? One of them might in reality hold twice as little capital as the other one for what is actually the same risk level. Banks can easily game the system. Moreover, the FT was reporting yesterday that some banks were starting to report RoRWA (return on RWAs) instead of more traditional return on equity or return on assets. But those measures suffer from the exact same defects. While an unweighted leverage ratio is clearly not perfect, RWAs introduce far too much information distortion and even potentially exacerbate the business cycle. Time to get rid of them.

A response to Scott Fullwiler on MMT banking theory

Following my post about the problems with the MMT and endogenous money banking theory, Scott Fullwiler, one of its proponents, briefly (and very nicely) commented on it, suggesting that I was not criticising the theory and that we were in fact in agreement. I beg to differ.

Another commenter, JH, also left a link to a much more comprehensive article describing the theory, written by Scott (you can find it here). I recommend this article to everyone. It is a very interesting piece about banking, and Scott clearly demonstrates in it that his knowledge of the banking system is superior to most of his fellow economists.

I had started to write a fairly long post criticising the (few, but in my view, important) errors in Scott’s paper, but decided against it eventually, and deleted most of it to get directly to the main point. I could probably write a whole academic article about the topic but I have no idea how to get it published so won’t do it! (any advice appreciated though!)

Overall, I agree that Scott’s description of the lending process is largely accurate. However, I believe that the conclusions that seem to ‘naturally’ follow fall into a fallacy of composition. The endogenous money theory correctly assumes that the lending decision regarding a single loan is independent of the reserve status of the bank. However, the theory incorrectly assumes that this description also applies to lending as a whole.

The endogenous money theory correctly describes one-off borrowings from banks that temporarily lack reserves for some technical reasons. But this lack of reserves is only temporary as they have the necessary liquid holdings to generate new primary reserves. If banks can lend independently of their reserve status, it is because they have beforehand secured enough liquidity (= claims on primary reserves) to face settlements.

The fallacy of composition involves applying this reasoning to a bank’s aggregate lending. What happens as a one-off event cannot happen continuously, as it would progressively deplete the bank’s secondary reserves until it ends up only relying on interbank or central bank funding for marginal lending, assuming funding costs were maintained at a stable level. But they are not. The more secondary reserves fall, the more the bank’s ratings are cut, its cost of funding increases and its share price falls. At some point, not only the marginal increase in lending is not profitable anymore, but also the bank might have endangered its very existence by becoming borderline liquid resulting in all market actors getting hesitant to provide it with any fund.

Therefore, Scott is right when he says that we agree that banks are pricing-constrained. Indeed. But we disagree on the backstop mechanism. The endogenous view considers central bank funding (and pricing) as the backstop mechanism, against which banks are going to benchmark their new lending to assess its profitability (the interest rate spread) if other sources of funds are unavailable. As Scott says:

Borrowings and reserve balances can always be had at some rate of interest; the question is whether or not this rate of interest is one at which the bank can make a profit that provides a sufficient return on equity.

Scott here mainly refers to the lender of last resort, the central bank. This implies that the supply of reserve by the central bank is perfectly elastic at a given interest rate, and therefore entirely driven by demand. But he does not take into account the impact for a bank of being able to raise funds only from a central bank. Sure, a bank that cannot seem to find any reserve anywhere else can still usually borrow from the central bank. Nonetheless, this bank, is, well… screwed. It just committed suicide.

By overexpanding, it depleted its liquidity position (through adverse clearing) to such an extent that no market actor was willing to lend to it anymore. By admitting its new reliance on central bank funding for survival, it admits its failure. As I have already said in my previous post, this is why banks are doing their best to avoid using central banks’ facilities. Nonetheless, this bank has the possibility to regain market confidence: it can reduce its lending in order to generate new liquidity. This shows the limit of the endogenous money theory: in the medium-term, lending is indirectly reserve-constrained.

We can see that the benchmark against which banks assess the profitability of new lending isn’t the central bank’s rate. It is the various market rates. Even without the central bank changing its target rate, an overexpanding bank will inevitably be forced to contract its lending by market forces, and consequently, the money supply.

Endogenous money theorists could respond that financial markets act irrationally: there is no point in punishing banks that could actually obtain funding from the central bank, making liquidity risk irrelevant (at least as long as they are only illiquid and not insolvent). But investors have very good reasons: illiquid banks are usually either bailed-out or left to fail, with in either case serious consequences for shareholders, bondholders, and sometimes depositors. Think about Northern Rock and Bear Stearns. Those two banks were notoriously illiquid (rather than insolvent). You know what happened next.

Regarding the treatment of reserve requirements, I am not going to come back to the evidence from countries that actively use them as a policy tool. Nonetheless, the endogenous theory concludes that reserves are basically useless, except for interbank settlements and to comply with reserve requirements when needed (even cash withdrawals by customers are downplayed). I disagree; reserves are the most liquid asset banks can hold. When uncertainty increases in the markets and when even liquid securities suddenly become illiquid, banks increase their reserves holdings, which become precautionary reserves. Banks thus sacrifice some yield for liquidity. This does not mean that banks would not invest those reserves in loans or in securities should the economic conditions be normal.

I am going to stop here for today. There are a few other points I could have covered but as I said at the beginning of this post, this would require a 20-page article… Some of those include an overexpanding banking system as a whole (not just a single bank), the fact that, unlike what is implied in Scott’s article, banks are not maximising leverage, that leverage does seriously impact banks’ ratings, that deposits aren’t always the cheapest funding source, and even some details about banks’ regulatory capital calculations. Those are less important (or even very minor) points.

Update: See this post on the central bank funding stigma.

China as a spontaneous finance Frankenstein

China is an interesting case. Underneath its very tight government-controlled financial repression hide numerous financial experiments aimed at bypassing those very controls. The Chinese shadow banking system is now a well-known financial Frankenstein, with multiple asset management companies, wealth management products and other off-balance sheet entities providing around half the country’s credit volume. The more the government tries to regulate the system, the more financial innovation finds new workarounds and become increasingly more opaque.

Bitcoin is following this typical mechanism. China was one of the world’s most successful Bitcoin markets as local retailers and customers attempted to avoid government control and manipulation. In short, Chinese users liked that Bitcoin had fixed rules that could not be twisted by some corrupted officials. Bitcoin allowed them to transfer currency internationally almost without restriction. Its Chinese supporters felt free. Indeed, freedom and facilitation of transaction and saving is what drives most spontaneous financial innovations. Nonetheless, the love story couldn’t last as I have already described and the government launched a crackdown on Bitcoin in December.

Nonetheless, Bitcoin is coming back, the Frankenstein way. The FT reported today that local Chinese Bitcoin exchanges are now finding ways around new government rules. Surprising? It shouldn’t be. Governments around the world, a simple message: don’t underestimate your citizens. You’ll always run after them. Never ahead.

The issue is now that all those rules are pushing Bitcoin and other innovations even more into the shadows, making the whole system even more opaque and hard to analyse. For instance, while Chinese banks are now forbidden to clear Bitcoin transactions, a local platform route the money through its founder’s account. Some others have started to use voucher systems, essentially transferable claims on RMB accounts for people who want to buy and sell Bitcoins. Those vouchers effectively become claims on claims on money, or some sort of money substitutes redeemable on money substitutes (bitcoins) redeemable on money (USD)…

I personally don’t really welcome such evolutions. Government should stay away and not add further systemic risks to innovations already trying to figure out what their own limits are. As I recently said, learning is intrinsic to any system and should not be suppressed.

Blame the rich for the next asset bubble. Or not.

First of all, happy new year to all of you! Fingers crossed we don’t witness another market crash this year! 🙂

Indeed, credit markets are hot. Equity markets are also hot. The FT published an article yesterday with some striking facts about the ‘improvements’ in credit markets over the past couple of years. Some would say that it’s encouraging. I am not convinced…

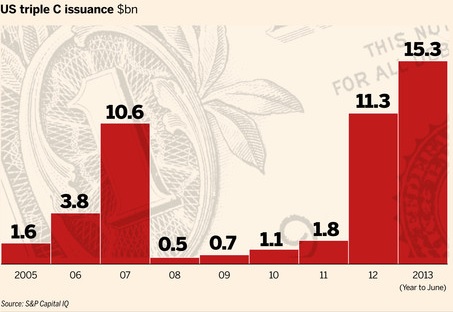

Most credit indicators are close to or above their pre-credit crisis high. Sales of leveraged loans and high-yield bonds are above their pre-crisis peak. The average leverage level of US LBOs is back to 2006 level. Issuance of collateralised loan obligations is close to its pre-crisis peak. Even CCC-rated junk bonds are way above their previous peak. I’ve already mentioned some of those facts a few months ago.

In a relatively recent presentation, Citi’s strategist Hans Lorenzen confirmed the trend: central banks are indirectly suppressing most risky investments’ risk premia. Most investors expect junk bonds’ spreads to tighten further or at least to stabilise at those narrow levels and emerging markets bonds and equities, as well as junk bonds are now among investors’ top asset classes .

My ‘theory’ at the time was that (see also here), if investors were piling in increasingly riskier asset classes, bringing their yield down to record low levels in the process, and nonetheless accepting this level of risk for such low returns, it was because current central bank-defined nominal interest rates were below the Wicksellian natural rate of interest. Inflation, as felt by investors rather than the one reported by national statistics agencies, was higher than most real rates of return on relatively safe assets. In order to see their capital growing (or at least to prevent it from declining), they were forced to pick riskier assets, such as high-yield bonds, which were not really high-yield anymore as a result but remained junk nonetheless. This would result in capital misallocation as, under ‘natural’ interest rate conditions, those investments would have never taken place. Thomas Aubrey’s Wicksellian differential, an indicator of the likely gap between the nominal and the natural rates of interest, was, in line with credit markets, reaching its pre-crisis high and seemed to confirm that ‘theory’.

Well, I now think that not all investors are responsible for what we are witnessing today. The (very) rich are.

This came to my mind some time ago while reading that FT piece by John Authers. This was revealing.

“Their wealth gives them scope to try imaginative investments, but they are terrified of inflation, even as deflation is emerging as a greater risk. That is in part because inflation for the goods and services bought by the very rich is running about 2 percentage points faster than retail inflation as a whole in the UK.” (my emphasis)

In the UK, real gilts’ yields were already in negative territory: adjusted by the (potentially underestimated) consumer price index, gilts were yielding around -1% early 2013. Savers were effectively losing money by investing in those bonds. Now think about the rich: by investing in such bonds, they would get a real return of around -3% instead.

Moreover, “71 per cent of respondents said they were more worried now about a steep rise in inflation than they were five years ago.”

Does it start to make sense? The cost of living I was mentioning earlier is increasing particularly quickly for the rich. And… they are the ones who own most financial assets. In order to offset those rising living costs, they naturally look for higher-yielding investments. And it is exactly what the FT reports:

“Their favourite asset classes for the next three decades are emerging markets equities, developed equities and agricultural land, in that order. Private equity comes close after farmland, while art and collectables were also a more popular asset class than any kind of bonds. […]

Hedge funds, as a group, have not fared well since the crisis. But wealthy investors preoccupied by inflation, and robbed of the easy option of bonds, are evidently disposed to give them a try, with an average projected allocation for the next three decades of 25 per cent. Meanwhile, the chance of a bubble in agricultural land prices, or in art, looks very real.”

Are the rich responsible for our current frothy markets then? Obviously not. They are acting rationally in response to central banks’ policies. Nonetheless, this raises an interesting question. Mainstream economics only considers a high aggregate inflation rate as dangerous. What about ‘class warfare’-type inflation? It does look like inflation experienced by one socioeconomic class could inadvertently lead to asset bubbles and bursts, despite aggregate inflation remaining subdued. This may be another destabilising effect of monetary injections on relative prices.

Granted, central banks possibly are on a Keynesian’s ‘euthanasia of the rentier’-type scheme in order to try to alleviate the pain of over-indebted borrowers (and/or to encourage further lending). But financial repression avoidance might well end-up coming back with a vengeance if savers’ reactions, and in particular, rich savers’, make financial markets bubble and crash.

Charts: FT (link above), Citi and Societé Générale

Recent Comments