The bank branch is dying. Some politicians don’t seem to get it

Technology is both a curse and a blessing for banks. It usually starts as a curse and ends up being a blessing (at least for the banks that eventually managed to master technological disruptions). I’ve personally argued several times during BarcampBank debates that the branch was outdated. The rebuttal I usually got (especially from French financial actors and entrepreneurs, probably a cultural thing) is that customers want to ‘feel’ some humanity, and not interact with some faceless system. I don’t disagree, but I would argue that they are massively overestimating the ‘humanity’ factor. What people want is convenience.

‘Humanity’ is just an inefficient way of providing convenient services to customers. When your services and IT systems aren’t convenient and instinctive enough for customers to use easily, they will naturally seek human help and reassurance. Does it mean customers necessarily want ‘access to other humans’ for most of their banking transactions? No. What it does mean it that banks don’t have straightforward enough and easy-to-use systems.

So here I reiterate: branches are outdated. And, once again, it is both a curse and a blessing for banks. For now, it is a curse: the retail banking business of most (large) banks is plagued by an unsustainable cost/income ratio (often around 70%+ when it should be closer to 50). The internet revolution led banks to open websites but not to close branches: branches were still the primary medium through which they could attract depositors (hence funding). Having a branch near potential customers’ home was crucial in order to both obtain funding and revenues. Internet obviously changes everything. But with a lag. Young people quickly get used to utilising internet websites for shopping and banking, but don’t have the financial resources that drive banking revenues. On the other hand, older customers are much slower to keep up with the trend. Some of the very first internet banks, like UK’s Egg, were not as successful as expected as a result.

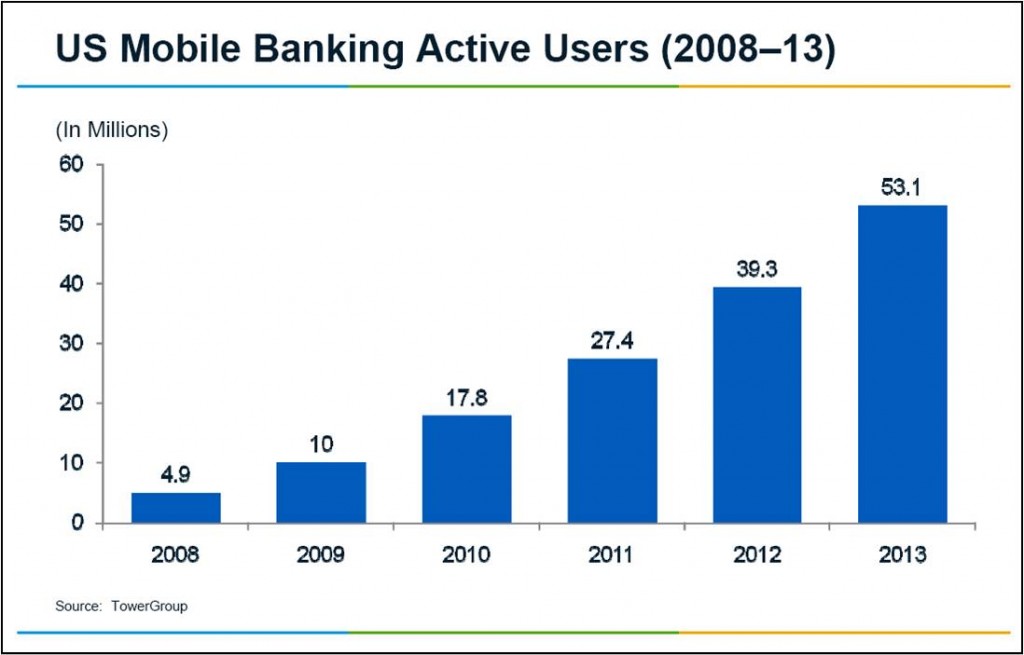

Now that mainstream internet use has been among us for around 15 years, much more customers use online services, including banking, and former early adopter but resource-poor students are now working professionals. Smartphones have compounded the trend. Brett King has extensively described the possible functions of a branch in the 21st century and documented the various trends in customer preferences in his Bank 2.0 and Bank 3.0 books. Mobile banking is booming and banks are at last starting to react. Over the last year, banks have followed each other in announcing reductions in their branch network, something that would have been unimaginable just a few years ago. In the US, banks are axing branches, the latest in line being Bank of America. In the UK, Barclays referred to branch closures as a ‘necessity’ at the end of last year. RBS and HSBC have also announced branch closures. In the rest of Europe, the trend is the same (see Belgian and French banks for instance). The other part of the curse is that banks do have to heavily invest in IT to catch up with the trend. And I am not even mentioning unions’ rejection of the branch axing plans, which indeed involve jobs cutting.

The blessing part of the story is that, while banks are constrained by increasing compliance costs and fall of revenues due to new regulations, smaller branch networks also means reduced cost bases. Bankers, desperate to improve their single-digit RoE can only welcome the change in the medium-term. More profitable banks also mean more flexible and more robust banks.

But. Some (most?) politicians don’t seem to get it. The UK’s Labour party came up with a brand new ‘brilliant’ idea to end the dominance of the largest retail banks of the country: a cap on the number (market share) of branches. As they are saying:

We are not asking whether existing banks might have to divest themselves of a significant number of branches. We are asking how we make that happen.

Well, you know what guys? It’s already happening. 21st century technological disruption does not require 20th century reasoning. Yet many professional politicians seem to have been blessed with the very skill of thinking using ‘previous century logic’. Politicians, please back away and let technology implement more efficient measures than anything you would have ever been able to plan.

PS: One of my (unrealistic at the moment) proposals was that alternative and independent interbank ‘superbranches’ could appear, gathering services/ATMs from all high-street banks under the same roof. This place would effectively be for banks what UK-based Carphone Warehouse and its competitors are for mobile phone providers. Banks would be a big step closer to being virtual service-providers and customers could potentially switch almost at will, intensifying competition. That would be a revolution.

PPS: Other technological disruptions I didn’t mention in the post were P2P-lending and associated services. This is also a big challenge but requires different responses, although some of the issues are interlinked.

- Chart 1: The Bankwatch, McKinsey

- Chart 2: McKinsey, The Triple Transformation, p. 33

- Chart 3: Mobility Enterprise

Recent Comments

| pslebow on ‘Sovereign money’:… | |

| pslebow on A critique of Werner’s view on… | |

| Hugo Kramer on Welcome to Spontaneous Fi… | |

| Nathan on A critique of Werner’s view on… | |

| Nathan on More, more, more money endogen… |

Trackbacks / Pingbacks