Blockchain everywhere

Banks are both scared and overexcited. Blockchain has the potential to fundamentally alter their business model, and they know it. Understanding tomorrow’s financial tech has become key to minimise business risks, key to remain relevant. A race that all financiers have joined is now going on, despite mocking Bitcoin just a couple of year ago. And blockchain is all over the news, despite most bankers having little to no understanding of what it is about. Financiers of all sorts now back blockchain-based technologies, from credit card companies to stock exchange and banks.

So a few weeks ago the NYT ironically remarked that:

Nowhere are more money and resources being spent on the technology than on Wall Street — the very industry that Bitcoin was created to circumvent.

Bloomberg reports that Blythe Masters, former MD at JPMorgan who helped kick start the credit default swap market, was now CEO of a blockchain startup, Digital Asset Holdings. Probably not what Satoshi Nakamoto, Bitcoin’s legendary creator, was expecting indeed. She says that, as I have explained on this blog, banks could massively benefit from blockchain technology if it can simplify back office operations. That is, if banks aren’t completely disintermediated first.

Matt Levin reflects on Masters’ comments and wonders why it is taking so long for the financial sector to eventually implement systems that drastically cut error-prone settlement delays (that can still be longer than 20 days, in the internet era…), and says that blockchain for banks can’t hurt. It’s certainly true, although don’t expect miracles: it’s going to take a few attempts, and perhaps a few failures or even mini-crises, for a blockchain-based system to evolve into something solid. And if it turns out that blockchain cannot offer a lasting, bulletproof solution, it will disappear.

Masters also declared that US banks were rather slow at looking at potential blockchain solutions. And indeed, most banks that seemed very active in that area, at least that I have heard of so far, were not US-based. Many of them were European, perhaps reflecting the fact that they currently are under more profitability pressure than their US peers. UBS, for instance, has been very vocal about its blockchain initiatives. See also this quite complex article on IBTimes on the various technologies behind UBS’ ideas, which include private blockchains, sidechains (transfer of assets between multiple blockchains) and ‘settlement coins’ (essentially a fiat money representation on blockchain that relies on central banks’ settlement processes):

Recently, UBS demonstrated how a bond could be automated on a blockchain, the shared ledger system similar in design to that used by Bitcoin. It also proposed a fiat currency-backed “settlement coin” to fit within the existing regulatory framework. The bank appears to be leading the way in distributed ledger technology at this time.

What’s happening is fascinating. What’s going to finally emerge remains a mystery. While individual institutions can put in place private blockchain-type systems to cut costs or offer more effective dark pool services to a selection of customers, the implementation of a ‘stock-market replacement’ blockchain requires an industry-wide agreement. And it does seem to be happening. A couple of days ago, the FT reported that 9 of the largest banks agreed to cooperate on a blockchain initiative that would define common standards and protocols (I’d just like to add that this is another example of private market actors cooperation; no need for a state to devise that sort of things in most, if not all, cases).

But blockchain technologies don’t only apply to financial services. The NYT mentioned property titles, diamond and gold ownership, airline miles. But also the music industry. And certainly a lot of other ones, as some at the MIT seem to believe with their Enigma project, or some entrepreneurs I met a few months ago at a conference, who believed that entire applications such as Facebook could be transferred onto the blockchain. It’s now ‘blockchain everywhere’.

PS: I’m on holidays abroad so have little time for updates!

The demand for cash and its consequences

I came across this very interesting chart on Twitter (apparently actually coming from JP Koning’s excellent blog) showing the demand for cash over time in various countries.

The demand for cash is a form of money demand. And it varies over time and across cultures and evolves as technology changes. In most countries, the demand for cash increases around times when the number of transactions increases (Christmas/New year for instance, although some countries, such as South Korea, present an interesting pattern – not sure why). But there are very wide variations across countries: notice the difference between the Brazilian and the Swedish, British or Japanese demand for cash. Countries that have implemented developed card and/or cashless/contactless payment systems usually see their domestic demand for cash decrease and banks less under pressure to convert deposits into cash.

Overall, this has interesting consequences for the financial analysis of banks, bank management, and for the required elasticity of the currency. Every time the demand for cash peaks, banks find themselves under pressure to provide currency. Loans to deposit ratios increase as deposits decrease, making the same bank’s balance sheet look (much) worse at FY-end than at any point during the rest of the year. A peaking cash demand effectively mimics the effect of a run on the banking system. Temporarily, banks’ funding structure are weakened as reserves decrease and they rely on their portfolio of liquid securities to obtain short-term cash through repos with central banks or private institutions (or, at worst, calling in or temporarily not renewing loans)*. Central bankers are aware of this phenomenon and accommodate banks’ demand for extra reserves.

In a free banking system though, banks can simply convert deposits into privately-issued banknotes without having to struggle to find a cash provider. This ability allows free banks to economise on reserves and makes the circulating private currencies fully elastic. In a 100%-reserve banking system, cash balances at banks are effectively maintained in cash (i.e. not lent out). Therefore, any increase in the demand for cash should merely reduce those cash balances without any destabilising effects on banks’ funding structure (which aren’t really banks the way we know them anyway). However, if some of this demand for cash is to be funded through debt, this can end up being painful: in a sticky prices world, as available cash balances (i.e. loanable funds not yet lent out) temporarily fall while short-term demand for credit jump, interest rates could possibly reach punitive levels, with potentially negative economic consequences (i.e. fewer commercial transactions).

However, technological innovations can improve the efficiency of payment systems and lower the demand for cash in all those cases. Banks of course benefit from any payment technology that bypass cash withdrawals, alleviating pressure on their liquidity and hence on their profitability. Unfortunately not all countries seem willing to adopt new payment methods. The cases of France and the UK are striking. Despite similar economic structures and population, whereas the UK is adopting contactless and innovative payment solutions at a record pace, the French look much more reluctant to do so.

As the chart above did not include France, I downloaded the relevant data in order to compare the evolution and fluctuations of cash demand over the same period of time vs. the UK. Unsurprisingly, the demand for cash has grown much more in France than in the UK and fluctuations of the same magnitude have remained, despite the availability of internet and mobile transfers as well as contactless payments, which all have appeared over the last 15 years**. What this shows is that the demand for cash had a strong cultural component.

*Outright securities sale can also occur but if all banks engage in the sale of the same securities at the exact same time, prices crashes and losses are made in order to generate some cash.

** I have to admit that the cash demand growth for the UK looks surprisingly steady (apart from a small bump at the height of the crisis) with effectively no seasonal fluctuations.

McKinsey on banking and debt

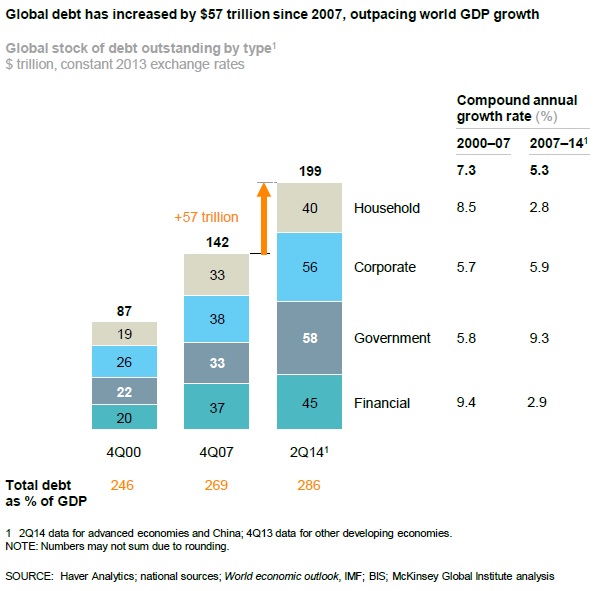

A recent report by the consultancy McKinsey highlights how much the world has not deleveraged since the onset of the financial crisis. Many newspapers have jumped on the occasion to question whether or not the policies adopted since the crisis were the right ones (FT, Telegraph, The Economist…). This is how the total stock of debt has evolved since 2000:

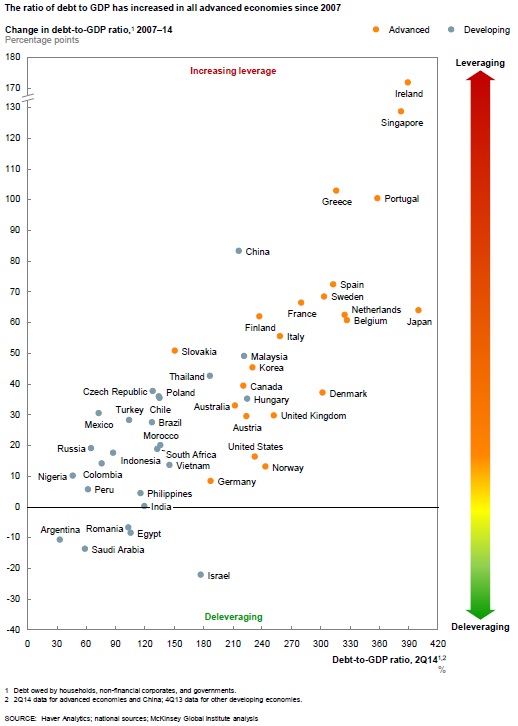

As the following chart shows, the vast majority of countries saw their overall level of debt increase:

As the following chart shows, the vast majority of countries saw their overall level of debt increase:

McKinsey affirms that “household debt continues to grow rapidly, and deleveraging is rare”, and that the same broadly applies to corporate debt. China is an extreme case: total debt level, as a share of GDP, grew from 121% of GDP in 2000, to 158% in 2007 to…282% at end-H114. And growing.

McKinsey affirms that “household debt continues to grow rapidly, and deleveraging is rare”, and that the same broadly applies to corporate debt. China is an extreme case: total debt level, as a share of GDP, grew from 121% of GDP in 2000, to 158% in 2007 to…282% at end-H114. And growing.

Unsurprisingly, household debt is driven by mortgage lending (including in China). It isn’t a surprise to see house prices increasing in so many countries. How this is a reflection that we currently are in a sustainable recovery, I can’t tell you. How this is a signal that monetary policy has been ‘tight’, I can’t tell you either. If monetary policy has indeed been ‘tight’, then it shows the power of Basel regulation in transforming a ‘tight’ monetary policy into an ‘easy’ one for households through mortgage lending. How this total stock of debt will react when interest rates start rising is anyone’s guess…

McKinsey’s claim that “banks have become healthier” is questionable at best, as they use regulatory Tier 1 ratios as a benchmark. Indeed a lot of banks have boosted their Tier 1 ratio by reducing RWA density (i.e. the average risk-weight applied to their assets) rather than actually raising or internally generating extra capital.

As expected given how capital intensive corporate lending has become thanks to our banking regulatory framework, and in line with recent research, banks are now mostly funding households at the expense of businesses:

As expected given how capital intensive corporate lending has become thanks to our banking regulatory framework, and in line with recent research, banks are now mostly funding households at the expense of businesses:

McKinsey highlights that P2P lending, while still small in terms of total volume, doubles in size every year, and is mostly present in China and the US.

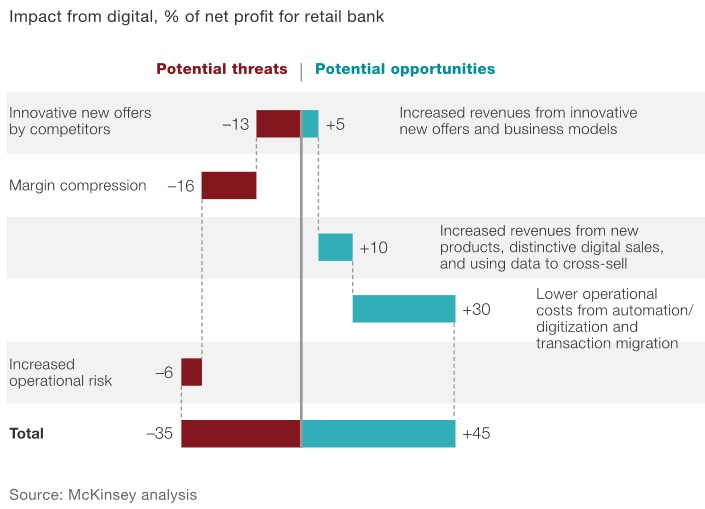

And in fact, in another article, McKinsey explains that the digital revolution is going to severely hit retail banking. I have several times described that banks’ IT systems were on average out-of-date, that this weighed on their cost efficiency and hence profitability, and that it even possibly impaired the monetary policy transmission channel. I also said that banks needed to react urgently if they were not to be taken over by more recent, more efficient, IT-enabled competitors. A point also made in The End of Banking, according to which technology allows us to get rid of banks altogether.

McKinsey is now backing up those claims with interesting estimates. According to the consultancy, and unsurprisingly, operating costs would be the main beneficiary of a more modern IT framework:

McKinsey goes as far as declaring that:

McKinsey goes as far as declaring that:

The urgency of acting is acute. Banks have three to five years at most to become digitally proficient. If they fail to take action, they risk entering a spiral of decline similar to laggards in other industries.

Unfortunately, current extra regulatory costs and litigation charges are making it very hard for banks to allocate any budget to replace antiquated IT systems.

If banks already had those systems in place as of today, I would expect to see lending rates declining further – in line with monetary policy – across all lending products as margin compression becomes less of an issue. In a world where banks have zero operating cost, its net interest income doesn’t need to be high to generate a net profit.

In the end, regulators are shooting themselves in the foot: not only new regulations and continuous litigations may well have the effect of facilitating new non-banking firms’ takeover of the financial system, but also monetary policy cannot have the effect that regulators/central bankers themselves desire.

Are ETFs and activist investors redefining the agency theory?

I wrote a few weeks ago that the rise of ETF might, in the end, make markets less efficient. While I still believe this to be a likely effect, The Economist just gave me a reason for hope. In two articles (here and here), the newspaper observes the parallel rise of activist investors.

The Economist adds another reason to my list of potentially negative effects of ETFs on financial markets: corporate governance. Indeed, not only buying indices raises the share price of all firms (good and bad) across a given portfolio, reducing the information contained in prices, but also ETFs are the most informal investors ever. They passively replicate the market and do not intervene in firms’ management. Underperforming managers consequently benefit from: 1. the value of their firm evolving in line with better-performing peers, and 2. not being questioned by demanding shareholders.

The Economist adds another reason to my list of potentially negative effects of ETFs on financial markets: corporate governance. Indeed, not only buying indices raises the share price of all firms (good and bad) across a given portfolio, reducing the information contained in prices, but also ETFs are the most informal investors ever. They passively replicate the market and do not intervene in firms’ management. Underperforming managers consequently benefit from: 1. the value of their firm evolving in line with better-performing peers, and 2. not being questioned by demanding shareholders.

Thankfully, this remains an imaginary world (at least for now), as some investors (mostly hedge funds) have decided to take a more active stance. Those activists take a small stake in the company and lobby other, more passive, investors to join them in their quest for sometimes radical changes in the firm’s structure. As I pointed out when hedge funds took over the UK-based Cooperative Bank, conventional wisdom depicts them as corporate vultures seeking short-term gains at the expense of the long-term health of the firms they invest in. But I also mentioned this study, which couldn’t be clearer in dispelling those common myths:

Starting with operating performance, we find that operating performance improves following activist interventions and there is no evidence that the improved performance comes at the expense of performance later on. During the third, fourth, and fifth year following the start of an activist intervention, operating performance tends to be better, not worse, than during the pre-intervention period. Thus, during the long, five-year time window that we examine, the declines in operating performance asserted by supporters of the myopic activism claim are not found in the data. We also find that activists tend to target companies that are underperforming relative to industry peers at the time of the intervention, not well-performing ones.

For sure, not all activists are beneficial. But to maximise the value of their stake, activists need to convince other potential investors that the longer-term operating performance of the firm has indeed been improved (which should reflect in the investment’s expected future cash flows). As we say, “you can fool all the people some of the time, and some of the people all the time, but you cannot fool all the people all the time.” While Gordon Gekko’s ‘Greed is Good’ speech might enrage some, it does contain a fundamental corporate governance truth. If activists on aggregate damaged companies’ prospects, the value of their stake would plummet and they would run out of business. As The Economist reports:

Activists point out that if they were to propose changes that clearly damaged a firm’s prospects the stock price would fall. “Unless you have one eye on the long term—how customers and products are affected—you will not succeed,” says Mr Loeb.

In short, financial markets are becoming increasingly polarised between two trends situated at almost the opposite side of the investing spectrum: on the one hand, conventional investors pile into cheaper but ‘dumb’ and passive index funds; on the other hand, very active shareholders get their hands dirty fighting to improve the operations of underperforming firms. This is welcome and reassuring, and provides further evidence that markets can spontaneously correct themselves when required and when there is the opportunity to do so.

This also represents a corporate governance paradigm change. Conventional agency theory states that, due to asymmetric information, managers may not always act in the best interest of shareholders. The theory also implies that shareholders aren’t actively involved in operational decisions. But activist investors turn the theory on its head. As a result, the new agency theory relies on a small number of activist investors (agents) taking the right strategy decisions for hundreds or thousands of other passive investors/ETFs (principals). I would argue that, while imperfect, this new version of the agency theory is more likely to work as agents’ and principals’ interests are naturally more aligned.

The end of banking? Not like this please

I recently read Jonathan McMillan’s The End of Banking, which I first heard of through FT Alphaville here (McMillan is actually a pseudonym to cover it two authors: an academic and a banker). I have mixed feelings about this book. I really wanted to agree with it. And I do, to some extent. But I simply cannot agree with a number of other points they make.

Their proposal to reform banking is as follows (see the book for details): lending can be disintermediated through P2P lending platforms (and equivalent), which both monitor potential borrowers through credit scoring and allocate savers’ funds to minimise the probability of losses. Marketplaces set up by platforms would enable savers to sell their investments to generate cash if needed. What about the payment system? Their solution is for non-bank FIs to continuously provide market liquidity a number of financial instruments using algorithmic trading. Current accounts would in fact be invested like mutual funds, which would instantly convert those investments into cash when required for payment. They also propose accounting rule changes to prevent corporations from creating money-like instruments.

As such, they propose to end banks’ inside money and have a financial system exclusively based on digital outside money controlled by a monetary authority. While they don’t classify it this way, it does seem to me to be some sort of 100%-reserve banking proposal: the money supply is fixed in the very-short term and exogenously-defined by the monetary authority.

What I agree with:

- The main thesis of the book is completely valid and is something I have also argued for a little while: technological disruptions are now allowing us to go beyond banking and disintermediate it. P2P lending, non-banking payment systems, decentralised payment frameworks and currencies, algorithm-driven credit scoring… In many areas, banks have almost become redundant. I totally adhere to the authors’ thesis (although credit scoring does have real limitations).

- Technological developments have facilitated regulatory arbitrage, if not enabled it. Computing power now allow banks to optimise their capital requirements through the use of complex models which, it is important to point out, are validated by regulators.

What I disagree with:

- The authors seem to believe that banking regulation is usually a good thing and cannot seem to understand the various distortions, bubbles and inefficiencies those regulations create. According to them, if only technology hadn’t boomed over the past three decades, the banking system would be more stable. I strongly disagree.

- I dislike the top-down banking reform approach taken by their thesis. Free markets, driven by technology, should decide under what form the next iteration of banking should arise.

- I also see weaknesses in their proposal. First, I cannot agree with their view that money belongs to the public sphere, and that IOUs must benefit from a state guarantee to qualify as money. This has been disproved by history over and over again. Second, I see their proposal to have algorithmic trading manage the payment system as not only unworkable, but also dangerous. As already witnessed, algorithmic trading is imperfect and can amplify crashes rather than prevent them. How their payment system would react during a crisis, when everyone tries to exit most investments and pile into a few others, is anyone’s guess. Mine is that the payment system would suddenly be down, paralysing the entire economy. To be fair, their treatment of cash is unclear: could we maintain a custody account comprising only digital cash in their framework?

- Their 100%-reserve banking reform does not address fluctuations in the demand for money. Centralised monetary authorities do neither have access to the right information, nor within the right timeframe, to accurately provide extra media of exchange when needed by the public. Private entities, in direct contact with the public, can.

- Finally, though this is a minor point, I disagree with their monetary policy stance. It is inaccurate to present price stability as ideal to avoid economic distortions: productivity increases should lead to mild deflation in a growing economy (see Selgin’s Less than Zero or any market monetarist or Austrian blog and research paper). I also reject their physical cash ban, from a libertarian standpoint: people should be able to withdraw cash if ever they wish to*. This would seriously limit their negative interest rates policy proposal.

Overall, it is a thought-provoking and interesting book, which also quite accurately describes our current banking system in its first part (mostly aimed at people who don’t know that much about banking). Its two authors are also right to point out the defects of regulation in an IT-intensive era. But, in my opinion, they draw the wrong conclusions and the wrong reform proposals from their original assessment.

* Here again, their treatment of cash is unclear: can cash be withdrawn in a digital form and maintain in a digital wallet outside the financial system? I doesn’t look so from their book but I cannot say for sure.

Are ETFs making markets less efficient?

I don’t have an answer to that question. But I have been wondering for a little while.

Noah Smith, on Bloomberg, and John Authers, in the FT, are pointing out that passive funds keep witnessing inflows at the expense of actively managed funds (which still represent the large majority of assets under management). Smith adds that academic research overwhelmingly demonstrates that active fund management (whether hedge funds or more traditional, and cheaper, mutual funds) is a ‘waste’ of money.

Market efficiency requires that many different individuals make their own investment assessment and decisions, in accordance with their limited means, knowledge and preferences. Some will gain, some will lose, market prices will continuously fluctuate one way or another in a permanent state of disequilibrium that reflects investors’ evolving views of what constitutes an efficient allocation of resources. In turn market price movements in themselves lead investors to reassess their opinions, bringing about further fluctuations but eventually producing something that resemble a near-equilibrium market, which almost accurately reflects investors’ preferences… for a few instants… after which other investors’ reactions are triggered. This is confusing; this is perpetual discovery and adaptation; this is the market process*.

Hence the importance of prices. And in particular, of relative prices. Investors can pick investments among a very wide range of securities. Such market granularity eases the market process: when one particular security looks underpriced relative to its peers, investors might start buying (until its price has gone up).

ETFs, index funds, on the other hand, allow investors to buy the whole market, or a large part of it, or a whole sector. They merely replicate market movements. As such, granularity, relative prices, and intra-market fluctuations disappear. Consequently, if everyone starts buying the whole market, there is no room left to pick winners within the market. Efficient firms and investments benefit as much from the inflow of capital as bad ones. Once a majority of investors start buying the whole market through index funds, stock pickers will have very limited choice to pick winners. Resources allocation, and in the end economic efficiency, becomes impaired**.

All this remains very theoretical. I haven’t been able to find any theoretical or empirical paper that researched this particular topic (please let me know if you know any). 2013 Nobel-winner Eugene Fama recently dismissed those concerns:

There’s this fallacy that you need active managers to make the market efficient. That’s true to some extent, but you need informed active managers to make it more efficient. Bad active managers make it less efficient.

Basically, he hasn’t answered the question. According to him, no, ETFs don’t make markets less efficient, but yes that’s true to an extent but no if you have bad active managers. Not that helpful to say the least. He is the father of the efficient market hypothesis so probably a little biased to start with.

Smith has another answer: he believes that asset-class picking could become the new stock-picking and that active management could shift from relative intra-market prices to relative inter-market prices. Basically, investors would take positions on, let’s say, the German stock market vs. the British one, instead of picking companies or securities within each of those markets. This is a possibility, albeit one that doesn’t really solve the economic resources allocation efficiency problem described above. Investors also don’t always have the option to invest outside of their domestic market, for contractual or FX fluctuation reasons.

It is likely that stock picking won’t disappear. Investors will always want to buy promising or sell disappointing individual securities. Still, the rise of index investing could have some interesting (and possibly far-reaching) implications for the market process and resource allocations. It is, as yet, unclear what form these implications may take.

* This ‘market efficiency’ definition is very close to the one defined by Austrian school scholars (which I prefer), as opposed to the more common market efficiency as defined under the equilibrium neo/new classical and Keynesian frameworks. See summaries here, as well as a more detailed description of the New classical efficient market hypothesis here.

** A real life comparison would be: instead of purchasing one TV, after carefully weighing the pros and cons of each option out there, everyone starts buying all possible models from all manufacturers, independently of their respective qualities. The company offering the worst product would benefit as much as the one offering the best product. Needless to say, this isn’t the best way of maximising economic resources.

NESTA’s alternative finance data goldmine

NESTA, a UK-based charity promoting innovation (and which also organised the annual UK Barcamp Bank), just released its new report on alternative finance trends in the UK. It is a goldmine. The report if full of interesting charts and figures and in many ways tells us a lot about the current state of our traditional financial sector (and possibly of the stance of monetary policy).

Some charts and comments are of particular interest. To my surprise, business lending through P2P platforms was the biggest provider of funds in terms of total amount:

According to the report:

79 per cent of borrowers had attempted to get a bank loan before turning to P2P business lending, with only 22 per cent of borrowers being offered a bank loan. 33 per cent thought it was unlikely or very unlikely that they would have been able to secure funding elsewhere had they not been successful in getting a loan through the P2P business lending platform, whereas 44 per cent of respondents thought they would have been likely or very likely to secure funding from other sources had they not used P2P business lending.

Given bank regulation that penalises banks for lending to small firms, none of this is surprising. As I keep saying, regulation is the primary driver of financial innovation. P2P business lending owes a lot to regulators… until it gets regulated itself?

Another very interesting chart was the following one:

This is crazy. Wealthy people pretty much shun P2P and other alternative finance forms. Why is that? Here’s my theory: wealthy people are usually well advised financially and have access to more investment opportunities than less-wealthy household. Consequently, a low interest environment isn’t that much of a problem (in the short-term): they have the ability to move down the risk scale to look for extra yield. On the other hand, household with more ‘moderate’ incomes do not have access to such investment opportunities: they are the ones hit by low returns on investments. P2P provides them with a unique opportunity to boost the meagre returns on their savings as long as real interest rates remain that low (i.e. lower than inflation):

[The funders] in P2P lending and equity-based crowdfunding were primarily driven by the prospect of financial returns with less concern for backing local businesses or supporting social causes.

Figures concerning P2P consumer lending are similar.

Those figures are both worrying and encouraging. Worrying because the harm that low interest rates and regulation seem to have on the economy and the traditional banking sector. Encouraging because finance is reorganising itself to respond to both borrowers’ and lenders’ demands. This is spontaneous order at work. Let just hope this does not add another layer of complexity and opacity to our already overly-complex financial system.

The Economist on mobile payments and market liquidity

The Economist recently published an article on mobile payment, which is suspicious of its success to say the least:

The fragmentation [of mobile payment systems] confuses merchants and consumers, who have yet to see what is in it for them. From their perspective, the current system works well. Swiping a credit card is not much harder than tapping a phone. Nor is it too risky, especially in America, since credit cards are protected against fraud. Upgrading to a new system is a hassle. Merchants have to install new terminals. Consumers need to store their card details on their phones, but still carry their cards around, since most stores are not yet properly equipped.

I believe the newspaper is too pessimistic. Yes, swapping credit cards is easy. But then it involves signing a bill (not the fastest and most modern system ever) and the card can be replicated. Hence why most of the rest of the developed world has moved to a ‘chip and pin’ form of card payment, which is only slightly more burdensome (and not very fast either). The US is also taking the same direction.

Most people who have recently swapped their ‘chip and pin’ card for a contactless one can witness how convenient and quick the new system is. Yet, they also believed that the previous system “worked well”. Following the same argument, it would have been hard to convince people to switch to cards since carrying cash also “worked well” (ok, it’s not as strong an argument). Switching to smartphone-based contactless payment would make the system as fast, yet reduce the number of cards and devices one carries.

The Economist continues:

But even Apple’s magic may not be enough to make mobile payments fly. It is not clear how merchants will benefit from Apple’s new ecosystem: it does not offer them lower fees for processing payments or useful data about their customers, as CurrentC does. As a result, they may refuse to sign up for Apple Pay or discourage its use.

Yet, as described above, speed is mobile payment’s major asset. Any retailer regularly experiencing long queues is likely to lose customers. Contactless cards already speed up the checkout process considerably. Unfortunately, they are usually capped to pay small amounts (GBP20 in the UK). Contactless mobile payment/NFC systems would remove that cap.

In another article, The Economist once again highlights its ambivalent stance towards regulation:

But the illiquidity problem will still be there when the next crisis occurs. In a sense, it is a problem caused by regulators; they wanted banks to be less exposed to the vicissitudes of markets. But you cannot make risk disappear altogether; you can only shift it to another place. Get ready for more moments of sheer market terror.

The article refers to the recent market turbulence and points to regulatory requirements that have made lack of liquidity a rather new problem:

Due to new regulatory restrictions and capital rules that make bond-trading less profitable, banks have cut back their inventories to the level of 2002, even though the value of bonds outstanding has doubled since then (see chart).

That is a problem when trading surges, as it did between October 10th and 16th, when volumes rose by 67%. “Credit is not a continuously priced market,” says Richard Ryan of M&G Investments, a fund manager. “When a bond price falls from 100 to 90, it won’t do so smoothly, but in big drops.”

This is correct. Market-making (mostly fixed income) is becoming trickier because harsher capital requirements make it more expensive to carry a large inventory of bonds through three channels: 1. deleveraging, as banks are pushed towards higher regulatory capital ratios (and as the new leverage ratio is introduced), 2. credit risk, as credit risk-weights are on upward trend, 3. market risk, as holding larger inventories penalise banks through higher market RWAs than before. I may write a whole post on this topic soon.

But the newspaper forgets liquidity requirements: banks are required to hold enough very liquid assets on their balance sheet (‘liquidity coverage ratio’). Given the combination of leverage and liquidity constraints, banks have to sacrifice other asset classes: the riskier bonds. This leads to the following very good chart, from a Citigroup report and reported by Felix Salmon at Reuters:

This has been an issue with The Economist since the start of the crisis: the same newspaper declares that banks needs to be regulated and safer and complains about the negative effects of regulation at the same time. Perhaps time to be less contradictory?

PS: The ECB published its stress test results yesterday. I won’t comment on them. I just thought the AQR was an interesting exercise, but its consequences must be carefully weighted and it is crucial not to over-interpret them (I’ve already written about the danger of ‘harmonizing’ assessments across multiple jurisdictions and cultures).

Blurry banks’ future is

A lot of articles on financial innovation and disruption in the FT over the last few days. Here, John Gapper argues that tech firms aim at using the existing financial system rather than challenge it. Here, Martin Arnold argues that banks shouldn’t forget their traditional branch network as this is how they make money through their oldest and wealthiest clients. Here, Luke Johnson argues that crowdfunding is riskier but also more exciting and, in a way, is the future.

John Gapper is right to point out that the regulatory and capital costs of setting up new bank-alike lending entities are very high. Yet he probably overstates his case. P2P lenders do not provide bank-type services: technology has enabled disintermediation by allowing investors to lend money (almost) directly to borrowers, but the money invested is stuck and does not represent a means of payment, unlike bank deposits. P2P lenders have the ability to take over a large market share of the lending market; and their business model does not require a high operating, regulatory and capital costs base (at least for now…). This is where the traditional intermediated lending channel could effectively approach death. On the other hand, P2P lender cannot handle deposits and banks still have a near-monopoly in this area.

Of course, we could imagine a 100%-reserve banking world in which the lending channel has moved entirely to P2P lenders, mutual and hedge funds and equivalent, whereas the deposit and payment system has moved entirely to Paypal-like payment firms. And this excludes alternative options offered by cryptocurrencies. In this world, banks are effectively dead.

Still, I am far from sure this would be the best solution: banks provide an elastic supply of currency (fractional reserve banking) that can adapt to the demand for money. (We could imagine a world without banks but still an elastic currency supply, if for instance the whole money supply only comprised competing cryptocurrencies. Let’s say this is highly unlikely to happen in the foreseeable future)

Banks can also survive by benefiting from those technologies (if ever they dare touching their antique IT systems…). As I’ve been saying for a while, banks can leverage their huge customer base to set up their own P2P/crowdfunding platform. This has already started to happen: RBS just announced the creation of its own P2P lending platform, Santander announced a partnership with Funding Circle, Lending Club is developing partnerships with many US banks. Banks could earn a fee from referring customers to their own (or third-party) platform, while deleveraging and reducing their on-balance sheet credit risk. Investors would earn more on those investments than on time deposits, but bear some risk.

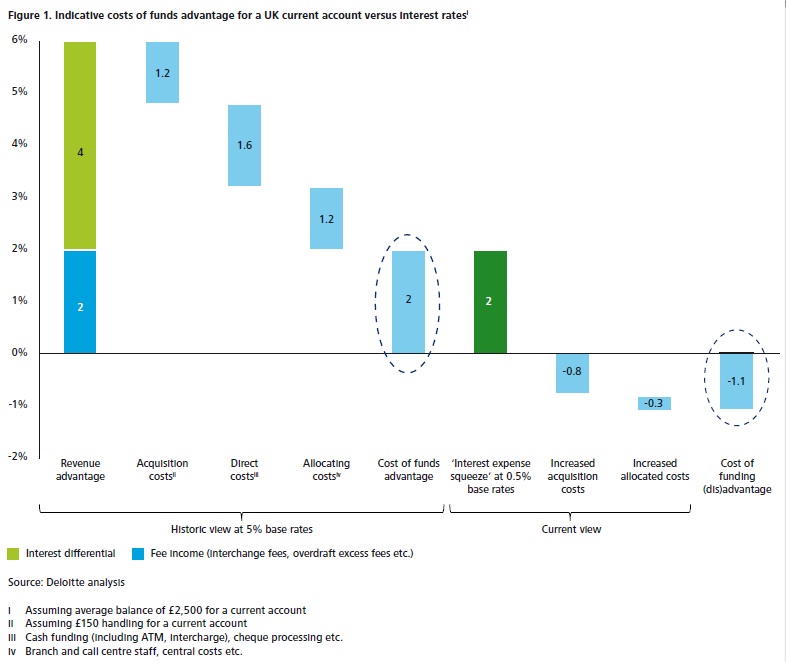

Whatever they decide to do, banks will have to adapt. But timing is key. Gapper referred to this recent, excellent, Deloitte report. They explain the margin compression effect (due to low base rates)*, which depresses banks’ profitability and adds another challenge on top of those that tech-enabled competitors and regulation already represent. According to them, closing down branches and moving online does not sufficiently slash cost to offset the decrease in net interest income. Closing down branches too quickly could also hurt banks by alienating the part of their client base born before the internet age. Deloitte provides evidence that a radical restructuring of IT systems could significantly improve returns, but this requires investments, which banks aren’t necessarily willing to undertake in a period of below-cost of capital RoE.

As the internet makes it easier for customers to compare pricing through aggregators and hence more difficult for banks to ‘extract value’ from them (what they call ’privileged access’), they recommend banks enhance ‘customer proposition’ (i.e. use ‘big data’) and focus on SME lending. As I’ve argued on this blog, capital regulation makes this difficult. They also indeed support the idea of in-house P2P platform, mostly to focus on local SMEs. This would help with capital requirements by maintaining SME exposures off-balance sheet, the risk borne by customers. Banks could effectively become risk assessment providers: rating lending opportunities to help customers (which include investment funds that don’t have such in-house capabilities) make their investment choices.

At the end of the day, banks are indeed likely to die if they don’t adapt. But also if they adapt too quickly. We could however see in the future surviving banks increasingly becoming like non-banks and non-banks increasingly providing banking services. The distinction between both types of institutions is likely to get very blurry. (That is, if regulation doesn’t kill non-banks first)

* Ben Southwood reiterated that interest rates are determined by markets and not by central banks. I already wrote responses to those claims here and here. Scott Sumner just mentioned his latest post, so I thought it would be a good idea to share Deloitte’s insight and own explanation of the margin compression effect and why “the spreads between Bank Rate and market rates seem to be narrow and fairly consistent—until they’re not.” In reality, lending spreads fluctuate only slightly when rates are above a certain threshold (i.e. banks’ risk-adjusted operating costs) and widen when they drop below it (explaining the “until they’re not”; see my previous posts). The fact that the “until they’re not” occurs does not imply that lending rates are “determined by the market”.

Here’s Deloitte own version:

The interest rate paid by banks on current accounts is typically lower than those paid for lump sum deposits (and the rates paid to borrow in the wholesale markets). However, this interest rate does not reflect the full cost of acquiring and servicing these current accounts. In the past, these acquisitions and servicing costs were offset by the fact that banks did not have to pay very high interest rates on current accounts.

Until the financial crisis, central bank interest rates (the ‘base rate’) were traditionally much higher. This meant that current account rates could easily be 500 or more basis points (hundredths of a percentage point) below lump-sum deposit rates.

Because base rates are at unprecedented lows, that maths does not work. Base rates have been low since 2009, and central bankers have signalled that they are likely to stay that way for some time yet. Figure 1 shows the economics of current accounts in the UK, where banks typically do not charge for them. A 200 basis point margin generated by current accounts when base rates are at 5 per cent turns into a 110 basis point loss at a 0.5 per cent base rate.

Two kinds of financial innovation

Paul Volcker famously said that the only meaningful financial innovation of the past decades was the ATM. Not only do I believe that his comment was strongly misguided, but he also seemed to misunderstand the very essence of innovation in the financial services sector.

Financial innovations are essentially driven by:

- Technological shocks: new technologies (information-based mostly) allow banks to adapt existing financial products and risk management techniques to new technological paradigms. Without tech shocks, innovations in banking and finance are relatively slow to appear.

- Regulatory arbitrage: financiers develop financial products and techniques that bypass or use loopholes in existing regulations. Some of those regulatory-driven innovations also benefit from the appearance of new technological and theoretical paradigms. Those innovations are typically quick to appear.

I usually view regulatory-driven innovations as the ‘bad’ ones. Those are the ones that add extra layers of complexity and opacity to the financial system, hiding risks and misleading investors in the process.

It took a little while, but financial innovations are currently catching up with the IT revolution. Expect to change the way you make or receive payments or even invest in the near future.

See below some of the examples of financial innovation in recent news. Can you spot the one(s) that is(are) the most likely to lead to a crisis, and its underlying driver?

- Bank branches: I have several times written about this, but a new report by CACI and estimates by Deutsche Bank forecasted that between 50% and 75% of all UK branches will have disappeared over the next decade. Following the growing branch networks of the 19th and 20th centuries, which were seen as compulsory to develop a retail banking presence, this looks like a major step back. Except that this is actually now a good thing as the IT and mobile revolution is enabling such a restructuring of the banking sector. SNL lists 10,000 branches for the top 6 UK bank and 16,000 in Italy. Cutting half of that would sharply improve banks’ cost efficiency (it would, however, also be painful for banks’ employees). It is widely reported that banks’ branches use has plunged over the past three years due to the introduction of digital and mobile banking.

- In China, regulators have introduced new rules to try to make it harder for mainstream banks to deal with shadow banks in order to slow the growth of the Chinese shadow banking system, which has grown to USD4.9 trillion from almost nothing just a few years ago. The Economist reports that, by using a simple accounting trick, banks got around the new rules. Moreover, while Chinese regulators are attempting to constrain investments in so-called trust and asset management companies, investors and banks have now simply moved the new funds to new products in securities brokerage companies.

- In London, underground travellers can now pay for their journey by simply using their contactless bank card. No need of a specific underground card anymore. NFC-enabled smartphones will be able to do the same in the near future.

- Barclays is experimenting contactless wristband that would effectively replace your contactless card for payments (or, for Londoners, your underground Oyster Card).

- Apple announced Apple Pay, a contactless payment system managed by Apple through its new iPhones and Watch devices. Apple will store your bank card details and charge your account later on. This allows users to bypass banks’ contactless payments devices entirely. Vodafone also just released a similar IT wallet-contactless chip system (why not using the phone’s NFC system though? I don’t know. Perhaps they were also targeting customers that did not own NFC-enabled devices).

- Lending Club, the large US-based P2P lending firm, has announced its IPO. This is a signal that such firms are now becoming mainstream, as well as growing competitors to banks.

Of course, a lot more is going on in the financial innovation area at the moment, and I only highlighted the most recent news. Identifying the regulatory arbitrage-driven innovations will help us find out where the next crisis is most likely to appear.

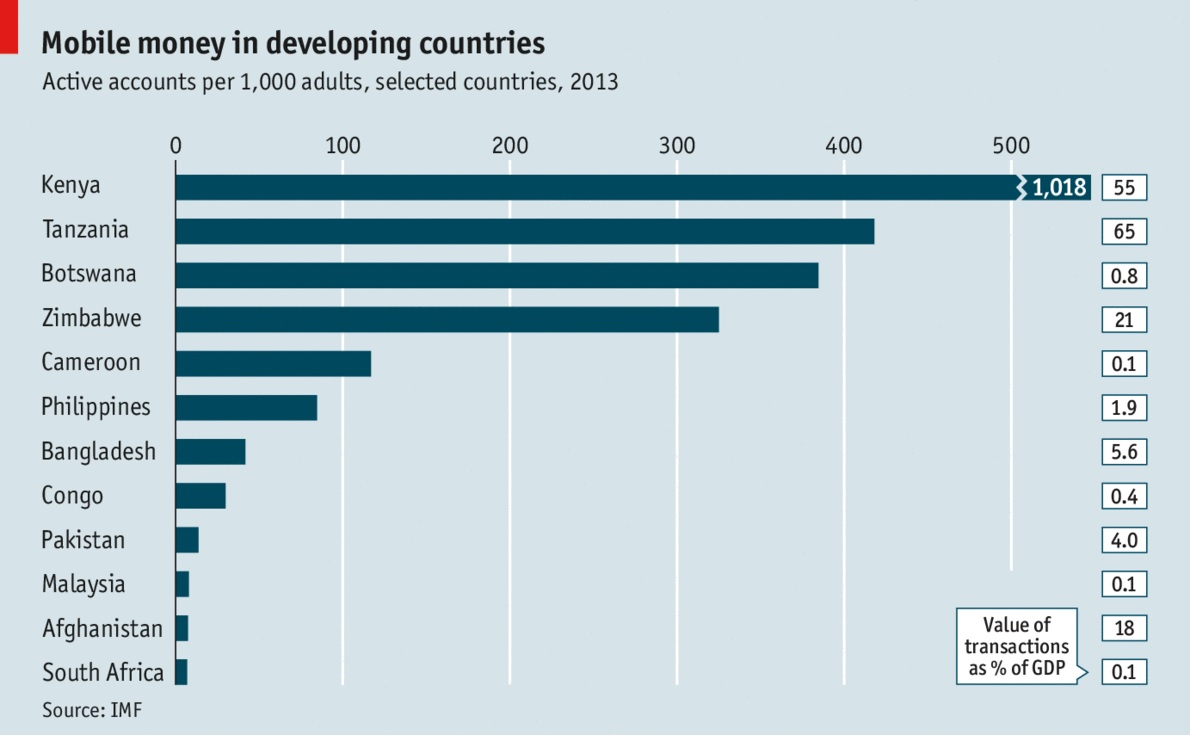

PS: the growth of cashless IT wallets has interesting repercussions on banks’ liquidity management and ability to extend credit (endogenous inside money creation), by reducing the drain of physical cash on the whole banking system’s reserves (outside money). If African economies are any guide to the future (see below, from The Economist), cash will progressively disappear from circulation without governments even outlawing it.

Recent Comments