Two kinds of financial innovation

Paul Volcker famously said that the only meaningful financial innovation of the past decades was the ATM. Not only do I believe that his comment was strongly misguided, but he also seemed to misunderstand the very essence of innovation in the financial services sector.

Financial innovations are essentially driven by:

- Technological shocks: new technologies (information-based mostly) allow banks to adapt existing financial products and risk management techniques to new technological paradigms. Without tech shocks, innovations in banking and finance are relatively slow to appear.

- Regulatory arbitrage: financiers develop financial products and techniques that bypass or use loopholes in existing regulations. Some of those regulatory-driven innovations also benefit from the appearance of new technological and theoretical paradigms. Those innovations are typically quick to appear.

I usually view regulatory-driven innovations as the ‘bad’ ones. Those are the ones that add extra layers of complexity and opacity to the financial system, hiding risks and misleading investors in the process.

It took a little while, but financial innovations are currently catching up with the IT revolution. Expect to change the way you make or receive payments or even invest in the near future.

See below some of the examples of financial innovation in recent news. Can you spot the one(s) that is(are) the most likely to lead to a crisis, and its underlying driver?

- Bank branches: I have several times written about this, but a new report by CACI and estimates by Deutsche Bank forecasted that between 50% and 75% of all UK branches will have disappeared over the next decade. Following the growing branch networks of the 19th and 20th centuries, which were seen as compulsory to develop a retail banking presence, this looks like a major step back. Except that this is actually now a good thing as the IT and mobile revolution is enabling such a restructuring of the banking sector. SNL lists 10,000 branches for the top 6 UK bank and 16,000 in Italy. Cutting half of that would sharply improve banks’ cost efficiency (it would, however, also be painful for banks’ employees). It is widely reported that banks’ branches use has plunged over the past three years due to the introduction of digital and mobile banking.

- In China, regulators have introduced new rules to try to make it harder for mainstream banks to deal with shadow banks in order to slow the growth of the Chinese shadow banking system, which has grown to USD4.9 trillion from almost nothing just a few years ago. The Economist reports that, by using a simple accounting trick, banks got around the new rules. Moreover, while Chinese regulators are attempting to constrain investments in so-called trust and asset management companies, investors and banks have now simply moved the new funds to new products in securities brokerage companies.

- In London, underground travellers can now pay for their journey by simply using their contactless bank card. No need of a specific underground card anymore. NFC-enabled smartphones will be able to do the same in the near future.

- Barclays is experimenting contactless wristband that would effectively replace your contactless card for payments (or, for Londoners, your underground Oyster Card).

- Apple announced Apple Pay, a contactless payment system managed by Apple through its new iPhones and Watch devices. Apple will store your bank card details and charge your account later on. This allows users to bypass banks’ contactless payments devices entirely. Vodafone also just released a similar IT wallet-contactless chip system (why not using the phone’s NFC system though? I don’t know. Perhaps they were also targeting customers that did not own NFC-enabled devices).

- Lending Club, the large US-based P2P lending firm, has announced its IPO. This is a signal that such firms are now becoming mainstream, as well as growing competitors to banks.

Of course, a lot more is going on in the financial innovation area at the moment, and I only highlighted the most recent news. Identifying the regulatory arbitrage-driven innovations will help us find out where the next crisis is most likely to appear.

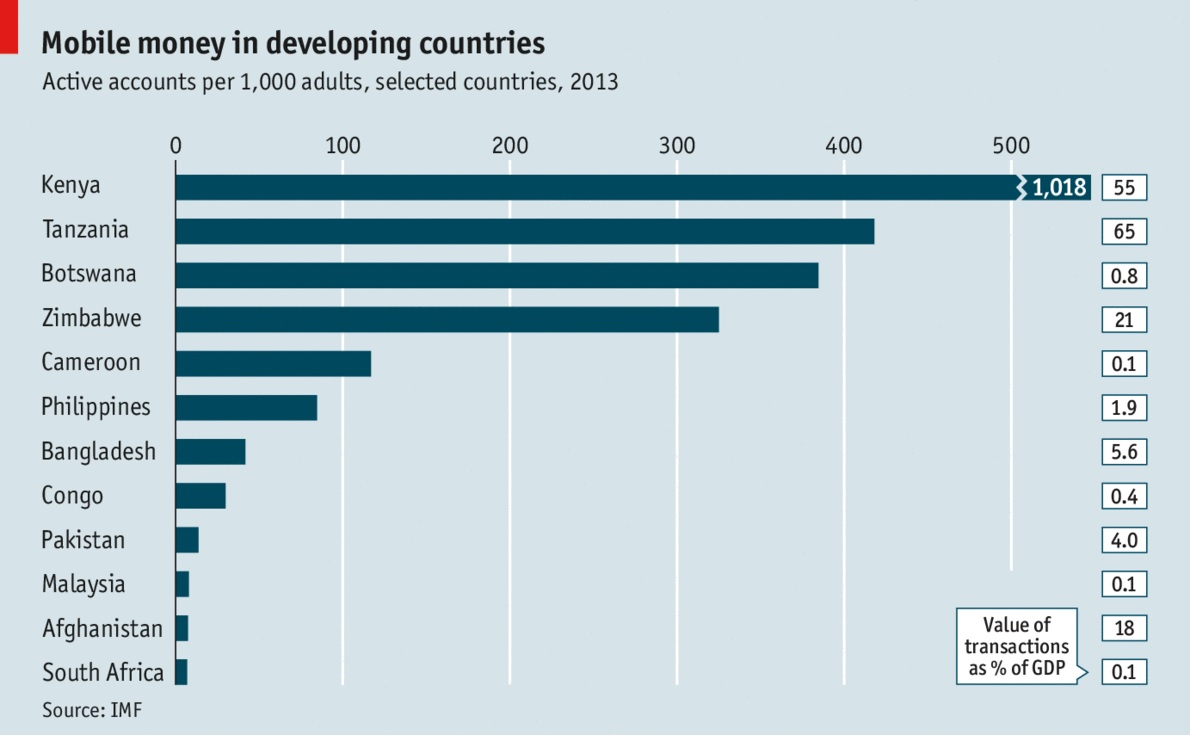

PS: the growth of cashless IT wallets has interesting repercussions on banks’ liquidity management and ability to extend credit (endogenous inside money creation), by reducing the drain of physical cash on the whole banking system’s reserves (outside money). If African economies are any guide to the future (see below, from The Economist), cash will progressively disappear from circulation without governments even outlawing it.

Recent Comments

| pslebow on ‘Sovereign money’:… | |

| pslebow on A critique of Werner’s view on… | |

| Hugo Kramer on Welcome to Spontaneous Fi… | |

| Nathan on A critique of Werner’s view on… | |

| Nathan on More, more, more money endogen… |

Trackbacks / Pingbacks