Two kinds of financial innovation

Paul Volcker famously said that the only meaningful financial innovation of the past decades was the ATM. Not only do I believe that his comment was strongly misguided, but he also seemed to misunderstand the very essence of innovation in the financial services sector.

Financial innovations are essentially driven by:

- Technological shocks: new technologies (information-based mostly) allow banks to adapt existing financial products and risk management techniques to new technological paradigms. Without tech shocks, innovations in banking and finance are relatively slow to appear.

- Regulatory arbitrage: financiers develop financial products and techniques that bypass or use loopholes in existing regulations. Some of those regulatory-driven innovations also benefit from the appearance of new technological and theoretical paradigms. Those innovations are typically quick to appear.

I usually view regulatory-driven innovations as the ‘bad’ ones. Those are the ones that add extra layers of complexity and opacity to the financial system, hiding risks and misleading investors in the process.

It took a little while, but financial innovations are currently catching up with the IT revolution. Expect to change the way you make or receive payments or even invest in the near future.

See below some of the examples of financial innovation in recent news. Can you spot the one(s) that is(are) the most likely to lead to a crisis, and its underlying driver?

- Bank branches: I have several times written about this, but a new report by CACI and estimates by Deutsche Bank forecasted that between 50% and 75% of all UK branches will have disappeared over the next decade. Following the growing branch networks of the 19th and 20th centuries, which were seen as compulsory to develop a retail banking presence, this looks like a major step back. Except that this is actually now a good thing as the IT and mobile revolution is enabling such a restructuring of the banking sector. SNL lists 10,000 branches for the top 6 UK bank and 16,000 in Italy. Cutting half of that would sharply improve banks’ cost efficiency (it would, however, also be painful for banks’ employees). It is widely reported that banks’ branches use has plunged over the past three years due to the introduction of digital and mobile banking.

- In China, regulators have introduced new rules to try to make it harder for mainstream banks to deal with shadow banks in order to slow the growth of the Chinese shadow banking system, which has grown to USD4.9 trillion from almost nothing just a few years ago. The Economist reports that, by using a simple accounting trick, banks got around the new rules. Moreover, while Chinese regulators are attempting to constrain investments in so-called trust and asset management companies, investors and banks have now simply moved the new funds to new products in securities brokerage companies.

- In London, underground travellers can now pay for their journey by simply using their contactless bank card. No need of a specific underground card anymore. NFC-enabled smartphones will be able to do the same in the near future.

- Barclays is experimenting contactless wristband that would effectively replace your contactless card for payments (or, for Londoners, your underground Oyster Card).

- Apple announced Apple Pay, a contactless payment system managed by Apple through its new iPhones and Watch devices. Apple will store your bank card details and charge your account later on. This allows users to bypass banks’ contactless payments devices entirely. Vodafone also just released a similar IT wallet-contactless chip system (why not using the phone’s NFC system though? I don’t know. Perhaps they were also targeting customers that did not own NFC-enabled devices).

- Lending Club, the large US-based P2P lending firm, has announced its IPO. This is a signal that such firms are now becoming mainstream, as well as growing competitors to banks.

Of course, a lot more is going on in the financial innovation area at the moment, and I only highlighted the most recent news. Identifying the regulatory arbitrage-driven innovations will help us find out where the next crisis is most likely to appear.

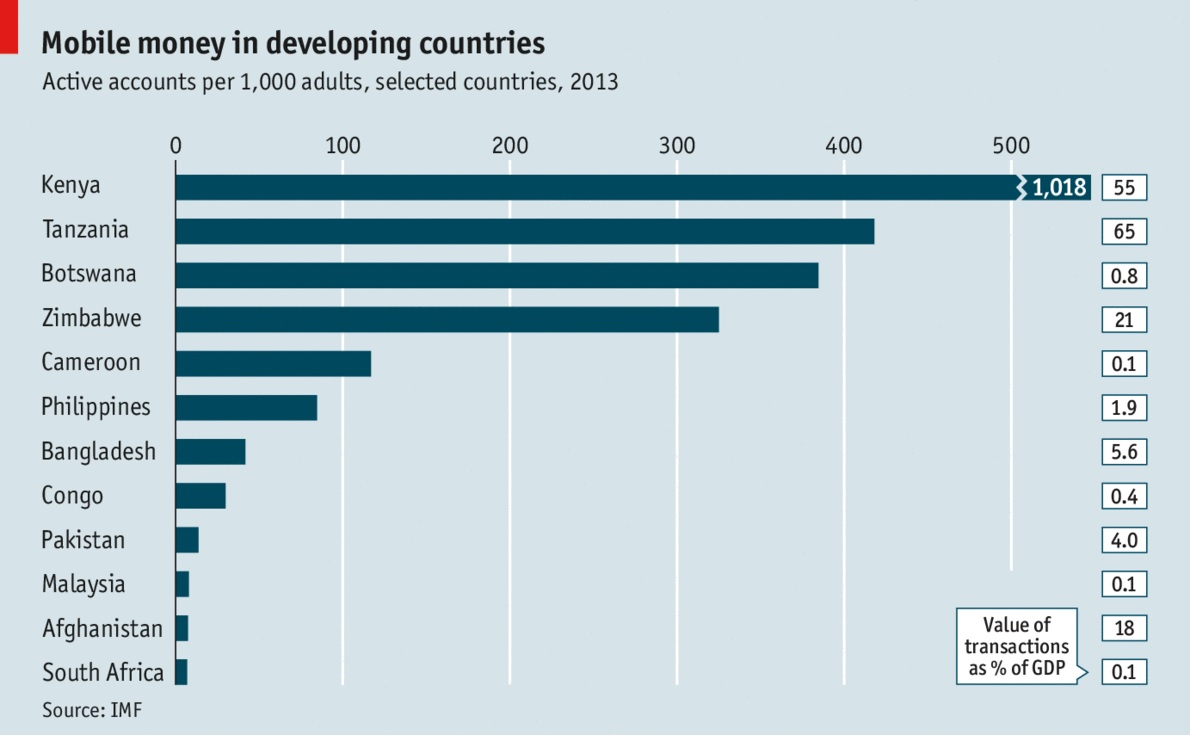

PS: the growth of cashless IT wallets has interesting repercussions on banks’ liquidity management and ability to extend credit (endogenous inside money creation), by reducing the drain of physical cash on the whole banking system’s reserves (outside money). If African economies are any guide to the future (see below, from The Economist), cash will progressively disappear from circulation without governments even outlawing it.

The mystery of collateral

Collateral has been the new fashionable area of finance and capital markets research over the past few years. Collateral and its associated transactions have been blamed for all the ills of the crisis, from runs on banks’ short-term wholesale funding to a scarcity of safe assets preventing an appropriate recovery. Some financial journalists have jumped on the bandwagon: everything is now seen through a ‘collateral lens’. The words ‘assets’, and, to a lesser extent ‘liquidity’ and ‘money’ themselves, have lost their meaning: all are now being replaced by ‘collateral’, or used interchangeably, by people who don’t seem to understand the differences.

A few researchers are the root cause. The work of Singh keeps referring to any sort of asset transfer between two parties as ‘collateral transfer’. This is wrong. Assets are assets. Securities are securities, a subset of assets. Collateral can be any type of assets, if designated and pledged as such to secure a lending or derivative transaction. Real estate, commodities and Treasuries can all be used as collateral. Money too. Unlike what Singh and his followers claim, a securities lender lends a security not a collateral. Whether or not this security is used as collateral in further transactions is an independent event.

This unfortunate vocabulary problem has led to perverse ramifications: all liquid assets, or, as they often say, collateral, are now seen as new forms of money (see chart below, from this paper). Specifically, collateral becomes “the money of the shadow banking system”. I believe this is incorrect. Collateral is used by shadow banks to get hold of money proper. Building on this line of reasoning, people like Pozsar assert that repo transactions are money… This makes even less sense. Repos simply are collateralised lending transactions. Nobody exchanges repos. The assets swapped through a repo (money and securities) could however be exchanged further. Depressingly, this view is taken increasingly seriously. As this recent post by Frances Coppola demonstrates, all assets seem now to be considered as money. This view is wrong in many ways, but I am ready to reconsider my position if ever Treasuries or RMBSs start being accepted as media of exchange at Walmart, or between Aston Martin and its suppliers. Others have completely misunderstood the differences between loan collateralisation and loan funding, which is at the heart of the issue: you don’t fund a loan, whether in the light or the dark side of the banking system, with collateral! The monetary base/high-powered money/cash/currency, is the only medium of settlement, the only asset that qualifies as a generally-accepted medium of exchange, store of value and unit of account (the traditional definition of money).

There is one exception though. Some particular transactions involve, not a non-money asset for money swap, but non-money asset for another non-money asset swap. This is almost a barter-like transaction, which does occur from time to time in securities lending activities (the lender lends a security for a given maturity, and the borrower pledges another security as collateral). Nonetheless, the accounting (including haircuts and interest calculations) in such circumstances is still being made through the use of market prices defined in terms of the monetary base.

Still, collateral seems to have some mysterious properties and Singh’s work offers some interesting insights into this peculiar world. The evolution of the collateral market might well have very deep effects on the economy. The facilitation of collateral use and rehypothecation, as well as the requirements to use them, either through specific regulatory and contractual frameworks, through the spread of new technology, new accounting rules or simply through the increased abundance of ‘safe assets’ (i.e. increased sovereign debt issuance), might well play a role in business cycles, via the interest rate channel. Indeed, by facilitating or requiring the use of increasingly abundant collateral, interest rates tend to fall. The concept of collateral velocity is in itself valuable: when velocity increases, interest rates tend to fall further as more transactions are executed on a secured basis. Still, are those transactions, and the resulting fall in interest rates, legitimate from an economic point of view? What are the possible effects on the generation of malinvestments?

An example: let’s imagine that a legal framework clarification or modification, and/or regulatory change, increases the use and velocity of safe collateral (government debt). New technological improvements also facilitate the accounting, transfer, and controlling processes of collateral. This increases the demand for government debt, which depresses its yield. Motivated by lower yield, the government indeed issues more debt that flow through financial markets. As the newly-enabled average velocity of collateral increases substantially, more leveraged secured transactions take place and at lower interest rates. While banks still have exogenous limits to credit expansion (as the monetary base is controlled by the central bank), the price of credit (i.e. endogenous money creation) has therefore decreased as a result of a mere regulatory/legal/technological change.

I have been wondering for a while whether or not such a change in the regulatory paradigm of collateral use could actually trigger an Austrian-type business cycle. I do not yet have an answer. Implications seem to be both economic and philosophical. What are the limits to property rights transfer? How would a fully laisse-faire market deal with collateral and react to such technological changes? Perhaps collateral has no real influence on business fluctuations after all. There is nevertheless merit in investigating further. I am likely to explore the collateral topic over the next few months.

PS: I will be travelling in North America over the next 10 days, so might not update this blog much.

* There are many many flaws in Frances’ piece. See this one:

But suppose that instead of a sterling bank account, a smartcard or a smartphone app enabled me to pay a bill in Euros directly from my holdings of UK gilts? This is not as unlikely as it sounds. It would actually be two transactions – a sale of gilts for sterling and a GBPEUR exchange. This pair of transactions in today’s liquid markets could be done instantaneously. I would in effect have paid for my meal with UK government debt.

She fails to see that she would have paid for her mean with Sterling, not with government debt! Government debt must be converted into currency as it is not a medium of exchange/settlement.

Hummel vs. Haldane: the central bank as central planner

Recent speeches and articles from most central bankers are increasingly leaving a bad aftertaste. Take this latest article by Andrew Haldane, Executive Director at the BoE, published in Central Banking. Haldane describes (not entirely accurately…) the history and evolution of central banking since the 19th century and discusses two possible paths for the next 25 years.

His first scenario is that central banks and regulation will step backward and get back to their former, ‘business as usual’, stance, focusing on targeting inflation and leaving most of the capital allocation work to financial markets. He views this scenario as unlikely. He believes that the central banks will more tightly regulate and intervene in all types of asset markets (my emphasis):

In this world, it would be very difficult for monetary, regulatory and operational policy to beat an orderly retreat. It is likely that regulatory policy would need to be in a constant state of alert for risks emerging in the financial shadows, which could trip up regulators and the financial system. In other words, regulatory fine-tuning could become the rule, not the exception.

In this world, macro-prudential policy to lean against the financial cycle could become more, not less, important over time. With more risk residing on non-bank balance sheets that are marked-to-market, it is possible that cycles in financial assets would be amplified, not dampened, relative to the old world. Their transmission to the wider economy may also be more potent and frequent. The demands on macro-prudential policy, to stabilise these financial fluctuations and hence the macro-economy, could thereby grow.

In this world, central banks’ operational policies would be likely to remain expansive. Non-bank counterparties would grow in importance, not shrink. So too, potentially, would more exotic forms of collateral taken in central banks’ operations. Market-making, in a wider class of financial instruments, could become a more standard part of the central bank toolkit, to mitigate the effects of temporary market illiquidity droughts in the non-bank sector.

In this world, central banks’ words and actions would be unlikely to diminish in importance. Their role in shaping the fortunes of financial markets and financial firms more likely would rise. Central banks’ every word would remain forensically scrutinised. And there would be an accompanying demand for ever-greater amounts of central bank transparency. Central banks would rarely be far from the front pages.

He acknowledged that central banks’ actions have already considerably influenced (distorted?…) financial markets over the past few years, though he views it as a relatively good thing (my emphasis):

With monetary, regulatory and operational policies all working in overdrive, central banks have had plenty of explaining to do. During the crisis, their actions have shaped the behaviour of pretty much every financial market and institution on the planet. So central banks’ words resonate as never previously. Rarely a day passes without a forensic media and market dissection of some central bank comment. […]

Where does this leave central banks today? We are not in Kansas any more. On monetary policy, we have gone from setting short safe rates to shaping rates of return on longer-term and wider classes of assets. On regulation, central banks have gone from spectator to player, with some granted micro-prudential as well as macro-prudential regulatory responsibilities. On operational matters, central banks have gone from market-watcher to market-shaper and market-maker across a broad class of assets and counterparties. On transparency, we have gone from blushing introvert to blooming extrovert. In short, central banks are essentially unrecognisable from a quarter of a century ago.

This makes me feel slightly unconfortable and instantly remind me of the – now classic – 2010 article by Jeff Hummel: Ben Bernanke vs. Milton Friedman: The Federal Reserve’s Emergence as the U.S. Economy’s Central Planner. While I believe there are a few inaccuracies and omissions in Hummel’s description of the financial crisis, his article is really good and his conclusion even more valid today than at the time of his writing:

In the final analysis, central banking has become the new central planning. Under the old central planning—which performed so poorly in the Soviet Union, Communist China, and other command economies—the government attempted to manage production and the supply of goods and services. Under the new central planning, the Fed attempts to manage the financial system as well as the supply and allocation of credit. Contrast present-day attitudes with the Keynesian dark ages of the 1950s and 1960s, when almost no one paid much attention to the Fed, whose activities were fairly limited by today’s standard. […]

As the prolonged and incomplete recovery from the recent recession suggests, however, the Fed’s new central planning, like the old central planning, will ultimately prove an unfortunate and possibly disastrous failure.

The contrast between central bankers’ (including Haldane’s) beliefs of a tightly controlled financial sector to those of Hummel couldn’t be starker.

Where it indeed becomes really worrying is that Hummel was only referring to Bernanke’s decision to allocate credit and liquidity facilities to some particular institutions, as well as to the multiplicity of interest rates and tools implemented within the usual central banking framework. At the time of his writing, macro-prudential policies were not as discussed as they are now. Nevertheless, they considerably amplify the central banks’ central planner role: thanks to them, central bankers can decide to reduce or increase the allocation of loanable funds to one particular sector of the economy to correct what they view as financial imbalances.

Moreover, central banks are also increasingly taking over the role of banking regulator. In the UK, for instance, the two new regulatory agencies (FCA and PRA) are now departments of the Bank of England. Consequently, central banks are in charge of monetary policy (through an increasing number of tools), macro-prudential regulation, micro-prudential regulation, and financial conduct and competition. Absolutely all aspects of banking will be defined and shaped at the central bank level. Central banks can decide to ‘increase’ competition in the banking sector as well as favour or bail-out targeted firms. And it doesn’t stop here. Tighter regulatory oversight is also now being considered for insurance firms, investment managers, various shadow banking entities and… crowdfunding and peer-to-peer lending.

Hummel was right: there are strong similarities between today’s financial sector planning and post-WW2 economic planning. It remains to be seen how everything will unravel. Given that history seems to point to exogenous origins of financial imbalances (whereas central bankers, on the other hand, believe in endogenous explanations, motivating their policies), this might not end well… Perhaps this is the only solution though: once the whole financial system is under the tight grip of some supposedly-effective central planner, the blame for the next financial crisis cannot fall on laissez-faire…

Could P2P Lending help monetary policy break through the ‘2%-lower bound’?

The ‘cut the middle man’ effect of P2P lending is already celebrated for offering better rates to both lenders and borrowers. But what many people miss is that this effect could also ease the transmission mechanism of central banks’ monetary policy.

I recently explained that the banking channel of monetary policy was limited in its effects by banks’ fixed operational costs. I came up with the following simplified net profit equation for a bank that only relies on interest income on floating rate lending as a source of revenues:

Net Profit = f1(central bank rate) – f2(central bank rate) – Costs, with

f1(central bank rate) = interest income from lending

= central bank rate + margin and,

f2(central bank rate) = interest expense on deposits

= central bank rate – margin

(I strongly advise you to take a look at the details here, which was a follow-up to my response to Ben Southwood’s own response on the Adam Smith Institute blog to my original post…which was also a response to his own original post…)

Consequently, banks can only remain profitable (from an accounting point of view) if the differential between interest income and interest expense (i.e. the net interest income) is greater than their operational costs:

Net interest income >= Costs

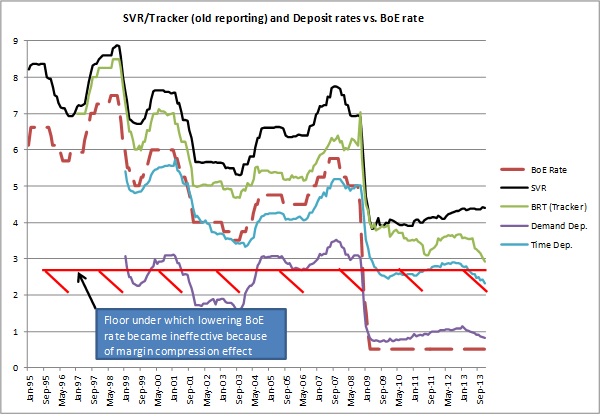

When the central bank base rate falls below a certain threshold, f2 reaches zero and cannot fall any lower, while f1 continues to decrease. This is the margin compression effect.

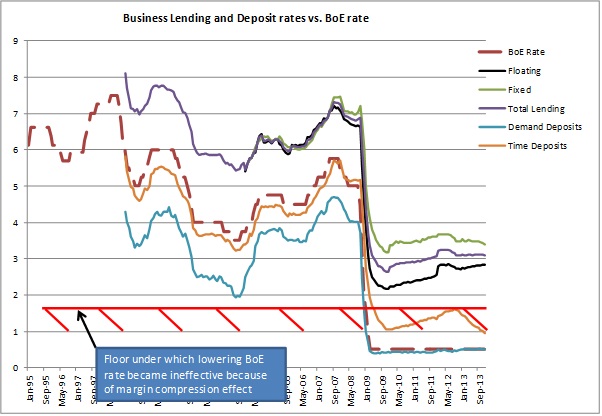

Above the threshold, the central bank base rate doesn’t matter much. Below, banks have to increase the margin on variable rate lending in order to cover their costs. This was evidenced by the following charts:

As the UK experience seems to show, banks stopped passing BoE rate cuts on to customers around a 2% BoE rate threshold. I called this phenomenon the ‘2%-lower bound’. I have yet to take a look at other countries.

Enter P2P lending.

By directly matching savers and borrowers and/or slicing and repackaging parts of loans, P2P platforms cut much of banks’ vital cost base. P2P platforms’ online infrastructure is much less cost-intensive than banks’ burdensome branch networks. As a result, it is well-known that both P2P savers and borrowers get better rates than at banks, by ‘cutting the middle man’. This is easy to explain using the equations described above, as costs approach zero in the P2P model. This is what Simon Cunningham called “the efficiency of Peer to Peer Lending”. As Simon describes:

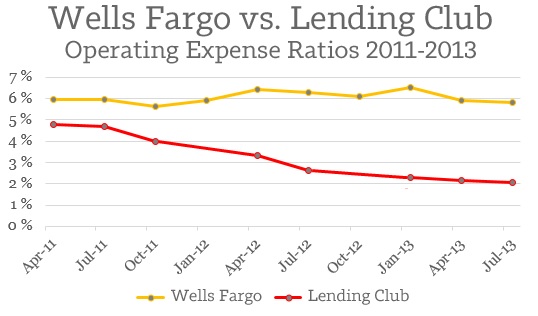

Looking purely at the numbers, Lending Club does business around 270% more efficiently than the comparable branch of a major American bank

Simon calculated the ‘efficiency’ of each type of lender by dividing the outstanding loans of Wells Fargo and Lending Club by their respective operational expenses (see chart below). I believe Lending Club’s efficiency is still way understated, though this would only become apparent as the platform grows. The marginal increase in lending made through P2P platforms necessitates almost no marginal increase in costs.

Perhaps P2P platforms’ disintermediation model could lubricate the banking channel of monetary policy the closer central banks’ base rate gets to the zero bound?

Possibly. From the charts above, we notice that the spread between savings rates and lending rates that banks require in order to cover their costs range from 2 to 3.5%. This is the cost of intermediation and maturity transformation. Banks hire experts to monitor borrowers and lending opportunities in-house and operate costly infrastructures as some of their liabilities (i.e. demand deposits) are part of the money supply and used by the payment system.

However, disintermediated demand and supply for loanable funds are (almost) unhampered by costs. As a result, the differential between borrowers and savers’ rate can theoretically be minimal, close to zero. That is, when the central bank lowers its target rate to 0%, banks’ deposit rates and short-term government debt yield should quickly follow. Time deposits and longer-dated government debt will remain slightly above that level. Savers would be incentivised to invest in P2P if the proposed rate at least matches them, adjusting for credit risk.

Let’s take an example: from the business lending chart above, we notice that business time deposit rates are currently quoted at around 1%. However, business lending is currently quoted at an average rate of about 3%. Banks generate income from this spread to pay salaries and other fixed costs, and to cover possible loan losses. Let’s now imagine that companies deposit their money in a time deposit-equivalent P2P product, yielding 1.5%. Theoretically, business lending could be cut to only slightly above 1.5%. This represents a much cheaper borrowing rate for borrowers.

P2P platforms would thus more closely follow the market process: the law of supply and demand. If most investments start yielding nothing, P2P would start attracting more investors through arbitrage, increasing the supply of loanable funds, and in turn lowering rates to the extent that they only cover credit risk.

The only limitation to this process stems from the nature of products offered by platforms. Floating rate products tend to be the most flexible and quickly follow changes in central banks’ rates. Fixed rate products, on the other hand, take some time to reprice, introducing a time lag in the implementation of monetary policy. I believe that most P2P products originated so far were fixed rate, though I could not seem to find any source to confirm that.

In the end, P2P lending is similar to market-based financing. The bond market already ‘cuts the middle man’, though there remains fees to underwriting banks, and only large firms can hope to issue bonds on the financial markets. In bond markets, investors exactly earn the coupon paid by borrowers. There is no differential as there is no middle man, unlike in banking. P2P platforms are, in a way, mini fixed-income markets that are accessible to a much broader range of borrowers and investors.

However, I view both bond markets and P2P lending as some version of 100%-reserve banking. While they could provide an increasingly large share of the credit supply, banks still have a role to play: their maturity transformation mechanism provides customers with a means of storing their money and accessing it whenever necessary. Would P2P platform start offering demand deposit accounts, their cost base would rise closer to that of banks, potentially raising the margin between savers and borrowers as described above.

It seems that, by partly shifting from the banking channel to the P2P channel over time, monetary policy could become more effective. I am sure that Yellen, Carney and Draghi will appreciate.

Regulating problems away doesn’t work

By ‘regulating’ the symptoms one does not cure the underlying disease. A few more examples in the press of this phenomenon that I keep describing:

– It’s no news that banks are being pressurised from all sides by regulation and lawsuits. The results? Banks aren’t that profitable anymore and remuneration stalls or even falls. Victory then? Wait a minute. Bloomberg reports that there is increased demand for young bankers by private equity funds, which are unsurprisingly more lightly regulated. This is part of a bigger trend that sees investors, funding and, as a result, credit, fleeing the traditional banking system towards the higher-yielding shadow banking system.

– The Economist also reports the same rebalancing towards shadow banking in China. I have already called China a ‘Spontaneous Finance Frankenstein’ given its strong, unnatural, regulatory-driven financial sector. This is typical:

China’s cap on deposit rates at banks is causing money to flood into shadow-banking products such as those offered by “trust” companies in search of higher yields. Offerings by internet firms, with their large existing customer bases, have opened the spigots wider. […]

Some see these online firms as a serious long-term threat to banks and the government’s ability to control the financial sector, prompting noisy demands (mostly by banks) to regulate the upstarts. Regulators have not yet expressed a clear view, but some observers see signals of a looming regulatory crackdown in attacks by the official media; a financial editor on the state-run television network recently branded online financial firms vampires and parasites.

What would be the effects of regulators successfully regulating those various areas of the shadow financial sector? A ‘shadow shadow’ banking sector would emerge. Liquidity, when in abundance, always finds its way. Regulation drives financial innovations, creating systemic risks through complex shadowy interlinked financial products and entities.

One does not regulate symptoms away. Market actors are the only natural, and the best, regulators.

China as a spontaneous finance Frankenstein

China is an interesting case. Underneath its very tight government-controlled financial repression hide numerous financial experiments aimed at bypassing those very controls. The Chinese shadow banking system is now a well-known financial Frankenstein, with multiple asset management companies, wealth management products and other off-balance sheet entities providing around half the country’s credit volume. The more the government tries to regulate the system, the more financial innovation finds new workarounds and become increasingly more opaque.

Bitcoin is following this typical mechanism. China was one of the world’s most successful Bitcoin markets as local retailers and customers attempted to avoid government control and manipulation. In short, Chinese users liked that Bitcoin had fixed rules that could not be twisted by some corrupted officials. Bitcoin allowed them to transfer currency internationally almost without restriction. Its Chinese supporters felt free. Indeed, freedom and facilitation of transaction and saving is what drives most spontaneous financial innovations. Nonetheless, the love story couldn’t last as I have already described and the government launched a crackdown on Bitcoin in December.

Nonetheless, Bitcoin is coming back, the Frankenstein way. The FT reported today that local Chinese Bitcoin exchanges are now finding ways around new government rules. Surprising? It shouldn’t be. Governments around the world, a simple message: don’t underestimate your citizens. You’ll always run after them. Never ahead.

The issue is now that all those rules are pushing Bitcoin and other innovations even more into the shadows, making the whole system even more opaque and hard to analyse. For instance, while Chinese banks are now forbidden to clear Bitcoin transactions, a local platform route the money through its founder’s account. Some others have started to use voucher systems, essentially transferable claims on RMB accounts for people who want to buy and sell Bitcoins. Those vouchers effectively become claims on claims on money, or some sort of money substitutes redeemable on money substitutes (bitcoins) redeemable on money (USD)…

I personally don’t really welcome such evolutions. Government should stay away and not add further systemic risks to innovations already trying to figure out what their own limits are. As I recently said, learning is intrinsic to any system and should not be suppressed.

Izabella Kaminska gets confused on 100%-reserve banking, or collateral, unless it’s… wait, I’m confused now

Meanwhile, Izabella Kaminska in the FT had an interesting (as usual), but very confused and confusing, blog post. I asked whether or not she was reading my blog given that some of her claims pretty much reflect mine (she calls the shadow banking system a “decentralised full-reserve banking system that just happens to run parallel with the official fractional system we are used to.” Compare that with my “[…] parallel 100%-reserve banking system. The shadow banking system is effectively some version of a 100%-reserve banking.”). But the similarities stop here. She sounds very confused… She gets mixed up between various terms, principles and concepts and tries to hide it behind quite complex wordings.

She mixes collateralised lending with 100%-reserve and uncollateralised lending with money creation. They are in fact totally unrelated. A bank or shadow bank can be fractional-reserve-based or 100%-reserve-based, which simply relates to whether or not a bank lends out a share of its deposits or if it maintains them in full in its vaults. Collateralised lending is, well, just lending provided against collateral (which can be almost any type of assets). Both fractional and 100%-reserve banks can lend against collateral in order to minimise the risk of loss in case of default. 100%-collateralised lending is not 100%-reserve.

True, 100%-cash collateralised lending could be thought of as some form of 100%-reserve banking as the cash reserve at the bank would virtually never depart from the deposit base amount. For example, if a fractional bank collects USD100 in deposits and lends out USD90, it only keeps 10% of cash deposits in reserve. If, though, it lends out USD90 collateralised against USD90 of cash, then it ends up with USD100 in its vault, the same amount as the deposit base (although there will be limitations on the liquidity of the cash as the collateral will likely be ‘stuck’ until repayment or default). But, following her claim, a mortgage bank would be a 100%-reserve bank as the value of the housing portfolio on which lending is secured is worth more than the amount of lending. This is obviously wrong. Unless houses are now a generally-accepted medium of exchange?

Then she claims that “the official banking sector, for example, has the capacity to make uncollateralised investments in growth areas it feels are promising regardless of whether borrowers have collateral, or whether they can be fully funded.” Not really. First, banks usually collateralise between a quarter and more than 100% of their lending. Second, “uncollateralised investments in growth areas it feels are promising regardless of whether borrowers have collateral” is called venture capital and is clearly not what banks do. Venture capital funds, business angels, and some crowdfunding and P2P platforms are here for that (you could also probably add the junk bond market to the list). She then adds that, in contrast to banks, “the shadow banking sector’s strength, of course, is that it is prepared to service those entities (whether directly or indirectly) the official banking sector is not prepared to service, thanks to a greater emphasis on collateral or funding.” As I just said, this is not the case. Venture capital-type investments cannot accept collateral as… there is none! This is why they are high-risk.

According to Izabella, there is a reason why shadow banks cannot create money: their use of collateral. While it is true that (most, probably all) shadow banks cannot create money, it is not because they lend against collateral as described above. A lot of shadow banks don’t lend against collateral: think most money market funds, P2P lending, hedge funds, mutual funds, payday lenders…or simply the bond market! But they don’t create money either! They only transfer cash.

In the comment section she also seems to claim that fractional reserve banking is an innovation of our modern banking system. Where did she get that? Fractional reserves have been used since antiquity: the use of the ‘monetary irregular-deposit’ contract in classical Roman law gave rise to fractional reserves as deposits were mixed with other ones of equivalent nature (as opposed to the mutuum, or monetary loan contract, which is similar to what we could describe as today’s mutual funds for example). Despite the illegality of lending out irregular-deposits, some bankers took advantage of the fungibility of money, and of the fact that many irregular-deposits were rarely withdrawn, to lend out a part of their deposit base. The ‘bank’ of Pope Callistus I (see photo) failed as it was unable to return the irregular-deposits on demand. Other examples of failed banks exist at this period but fractional reserves really took off from the late middle ages in Europe.

Not everything is wrong in her article as I mentioned at the beginning of my post. She’s right to claim that regulation would only displace risk to another corner of the financial system that shadow banking is merely a response to the regulatory-incentivised under-banked part of the economic system, and that P2P lending is a kind of shadow banking. But too many confusions or misunderstandings around collateral, money creation, bank funding, bank reserves, etc., obfuscate the topic.

News digest

I have been so busy since last week that I didn’t have much time to write for this blog… And, to tell you the truth, I was almost shocked: barely any news on banks capital, regulation, monetary policy, etc, over the past few days. Sure, the ECB cut its rate by 25bp to 0.25%, but I’m not sure I should comment within the scope of this blog: I am still not convinced by such such a diverse monetary union as the Eurozone and find it hard to believe we can actually set a common interest rate for all country members within the union… Anyway, today I only wish to comment on a few articles published over the last few days.

A very interesting article published on SNL (subscription required) called Everybody wants to rule the world, including bank regulators, in which an analyst argued that “Banks are not only facing over-regulation. They are also emerging as a convenient channel through which regulators can extend their reach far beyond their legal writ.” You probably understand as well as I do how dangerous this is.

I found out yesterday that Bear Stearns liquidators filed a lawsuit against the three credit rating agencies for alleged manipulation of structured products’ ratings. They are basically arguing that, if ratings had been right, Bears Stearns’ hedge funds would not have collapsed. Blaming the rating agencies because…..hedge funds collapsed? We are not talking about simple retail investors here. We are talking about sophisticated investors. Aren’t hedge funds supposed to undertake their own analysis? Are they just blindly investing in various assets? If hedge funds managers and analysts did not believe in rating agencies’ ratings, why did they invest in those assets the first place? Or perhaps they indeed did not believe in those ratings and took on the risk on purpose. In both cases, we cannot blame the agencies for the lack of competence of those highly-remunerated hedge funds employees.

Yesterday, the FT reported that shadow banks had been among the biggest beneficiaries of the Fed’s monetary policies. I’ve already argued that it might well be a sign that real interest rates are too low (i.e. lower than the equilibrium natural rate of interest). As a result, regulators wish to regulate (of course) this segment of the financial system. My guess is that surplus liquidity would then shift to another less-regulated sector or asset class, as it always does.

A few days ago, I read in horror that Germany may start backing the financial transaction tax. A tax of 0.1% of the value of the transaction (as is proposed on cash instruments) would be a massive drain of wealth: just imagine what would happen to a newly set-up EUR100bn mutual fund (ok, no new fund would ever be of that size, but follow me just for the intellectual exercise). The fund has evidently to invest those 100bn on behalf of its clients, meaning they have to buy EUR100bn of assets. Taxing 0.1% off the total value of the transactions would mean…EUR100m to pay in taxes. This is EUR100m that EU states would withdraw from people’s savings and pensions. Bad idea.

In the Wall Street Journal, a Fed insider described how disillusioned he was from the Fed and QE: he ‘apologises’ to Americans (Scott Sumner comments on this) for QE’s bad or lack of effects. While I do not necessarily share everything he said, I also dislike the Fed’s large scale market manipulation.

On Free Banking, George Selgin criticised this Business Insider piece about airlines debasing their reward points. Reminds me of my own response to Matt Klein on the exact same topic a few weeks ago. No guys: those cases do not reflect free banking and private currencies.

Well, that’s all for the catch up.

Financial innovation is back with a vengeance

What didn’t we hear about financial innovation throughout the crisis? Whereas innovation in general is good, financial innovation on the other hand was the worst possible thing coming out of a human mind. Paul Volcker, former Chairman of the Fed, famously declared that the ATM was the only useful financial innovation since the 1980s. Harsh.

True, some financial innovations are better than others. In particular, those used to bypass regulatory restrictions are more dangerous, not because they are intrinsically evil or anything, but simply because their often complex legal structure makes them opaque and difficult for external analysts and investors to analyse. This famous 2010 Fed paper attempted to map the shadow banking system (see picture), and usefully stated that not all shadow banking (and financial innovations) activities were dangerous (but those specifically designed to avoid regulations were). Ironically (and typically…) one of the first innovations to ever appear within the shadow banking system was money market funds. What was the rationale behind their creation? In the 1960s and 1970s in the US, interest payment on bank demand deposits was prohibited and capped on other types of deposits. The resulting financial repression through high inflation pushed financial innovators to come up with a way of bypassing the rule: money market funds became a deposit-equivalent that paid higher interests. Today we blame money market funds for being responsible for a quiet run on banks during the crisis, precipitating their fall. It would just be good to remember that without such stupid regulation in the first place, money market funds might have never existed…

The last decade has seen the growth of two particularly interesting innovations within the shadow banking system: one was relatively hidden (securitisation) while the other one grew in the spotlight (crowdfunding/peer-to-peer lending). One was deemed dangerous. The other one was more than welcome (ok, not in France). What had to happen happened: they are now combining their strength.

Various types of crowdfunding exist: equity crowdfunding, P2P lending, project financing… Today I’m going to focus on P2P lending only. What started as platforms enabling individuals to lend to other individuals are now turning into massive gates for complex institutional investors to lend to individuals and SMEs. Given the retreat of banks from the SME market (thank you Basel), various institutional investors (mutual and hedge funds, insurance firms) thought about diversifying their investments (and maximising their returns) by starting to offer loans to individuals and companies they normally can’t reach.

Basically, those funds had a few options: developing the capabilities to directly lend to those customers, investing in securitised portfolios of bank loans, or investing in securitised portfolios of P2P loans. The first option was very complex to implement and the required infrastructure would take a long time to develop. The second option had already existed for a little while, but was dependent on banks lending to customers, which current regulations limit due to higher capital requirements on such loans. The third option, on the other hand, allowed funds to maximise returns and attract more potential borrowers thanks to the reduction of the cost of borrowing by disintermediating banks. And funds could also strike deals with those still tiny online platforms that would have never happened with massive banks.

While securitisation sounds scary, it is actually only a simpler way of investing in loans of small sizes (the alternative being to invest in every single loan, some of them amounting to only USD500… Not only many funds don’t have the capability of doing such things, but many have also restrictions about the types of asset class and amounts they can invest in). Securitisation also bypasses Wall Street investment banks: funds directly invest in P2P loans, package them and sell them on to other investors while retaining a ‘tranche’ in the deal, which absorbs losses first. Now some entrepreneurs are even talking of setting up secondary markets to trade investments in loans, pretty much like a smaller version of the bond market.

Is this a welcome evolution for the P2P industry? I would say that it is a necessary evolution. It is once again a spontaneous development that merely reflects the need for funding of the P2P industry, which small retail investors cannot fulfil (unless all investment funds’ customers start withdrawing their money to directly invest in P2P, which is highly unlikely). Many start to think that large institutional investors will end up crowding out small retail investors. Possibly, but as long as regulation remains light, keeping barriers to entry low, new platforms only accepting retail investors could well appear if the demand is present.

All this is fascinating. Not only because technology and the internet enables new ways of channelling funds from savers to borrowers, but also because this is the growth of a parallel 100%-reserve banking system. The shadow banking system is effectively some version of a 100%-reserve banking. And it keeps growing through those various innovations. As I argued in a previous post, this may well have implications for monetary policy that current central banks and economists don’t take into account. A 100%-reserve banking system does not have a deposit multiplier and consequently does not have an elastic currency to respond to a sudden increase or decrease in the demand for money. However, such a system perfectly matches savers’ and borrowers’ intertemporal preferences, limiting malinvestments. Nonetheless, we for now remain in a mix system of 100% reserve (most of shadow banking) and fractional reserves (traditional banking). It would still be interesting to study the possible policy implications of a growth in the 100%-reserve part of the economy.

Spontaneous finance at work

The FT reported today that non-bank lending to SMEs was at its highest level since 2008 in the UK, whereas bank lending had been declining constantly since the start of the crisis, despite politicians’ and central bankers’ actions to revive it (such as the BoE’s Funding for Lending Scheme).

What kind of non-bank lending are we talking about? Personally, I would call this ‘shadow banks lending’, even though some other economists and analysts may have a different definition of shadow banking. To me, it comprises the less-regulated non-bank entities, from hedge funds to peer-to-peer lending platforms.

This is spontaneous finance at work: while the bloated, politically connected and over-regulated banking system does not seem to be able to channel resources (private savings) to smaller-than-large corporations, private actors, from investment funds to private individuals, step in to respond to their funding needs. This phenomenon has two sources: banks’ lending rates are often too high (blame regulatory capital requirements) and banks’ offered savings rate too low (blame too high inflation vs. BoE rate). And blame banks’ too high operating costs for both. As a result, there is a mismatch between what savers expect and what companies expect.

The solution? Bypass banks. Various investment companies (from hedge funds to more traditional mutual funds) are now setting up funds to gather savings and lend directly to companies that need them. Peer-to-peer and crowdfunding platforms basically act the same way by disintermediating all financial institutions: individuals directly lend to other individuals or firms. We also now see funds investing through P2P platforms (reversing the disintermediation process). Through those shadow banking channels, both savers and borrowers get better rates than they would do at a bank. At the time of my writing, savers can earn from 4% to 7% on their savings (even some hedge funds would love to get such steady returns). Rates vary for borrowers, but are on average lower than that of banks.

Lending volume is still pretty small as the wider public isn’t yet aware of those funding opportunities. In the UK, Funding Circle has only lent slightly less than GBP170m so far to small businesses (this compares to banks’ SME lending which stands at around GBP170…bn). But it’s growing quickly: it was only launched in 2010. Moreover, other shadow banks had lent around GBP17bn as of June (yes, a lot of 17 something, just a coincidence).

As this City AM article highlighted today, as usual, the main risk to those financial innovations is over-regulation, preventing their development and potentially leading to the creation of much riskier and opaque financial products. Regulators wish to ‘protect’ savers. I argue that savers do not need to be protected: they need to learn to invest responsibly and to understand the risks involved. Protection distorts risk-taking and capital allocation.

More worrying is the fact that some peer-to-peer industry actors are now even lobbying to be regulated… They claim that regulation will reassure potential investors. I claim that regulation will mainly protect the established firms by making it more difficult for new competitors to enter the market and offer competitive products to savers and borrowers. A brand new financial system is building before our eyes. It is important not to repeat mistakes that led to our current ineffective banking system.

Photograph: govopps.co.uk

Recent Comments