Could P2P Lending help monetary policy break through the ‘2%-lower bound’?

The ‘cut the middle man’ effect of P2P lending is already celebrated for offering better rates to both lenders and borrowers. But what many people miss is that this effect could also ease the transmission mechanism of central banks’ monetary policy.

I recently explained that the banking channel of monetary policy was limited in its effects by banks’ fixed operational costs. I came up with the following simplified net profit equation for a bank that only relies on interest income on floating rate lending as a source of revenues:

Net Profit = f1(central bank rate) – f2(central bank rate) – Costs, with

f1(central bank rate) = interest income from lending

= central bank rate + margin and,

f2(central bank rate) = interest expense on deposits

= central bank rate – margin

(I strongly advise you to take a look at the details here, which was a follow-up to my response to Ben Southwood’s own response on the Adam Smith Institute blog to my original post…which was also a response to his own original post…)

Consequently, banks can only remain profitable (from an accounting point of view) if the differential between interest income and interest expense (i.e. the net interest income) is greater than their operational costs:

Net interest income >= Costs

When the central bank base rate falls below a certain threshold, f2 reaches zero and cannot fall any lower, while f1 continues to decrease. This is the margin compression effect.

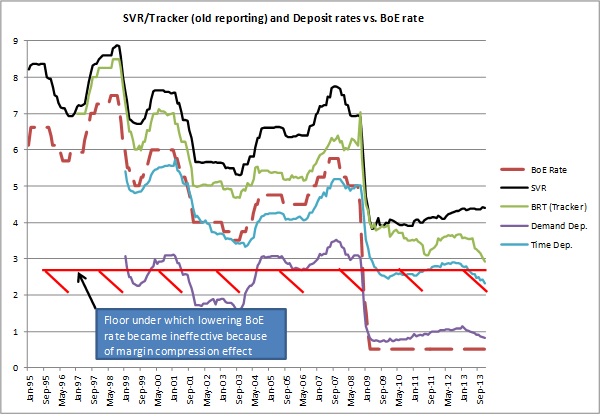

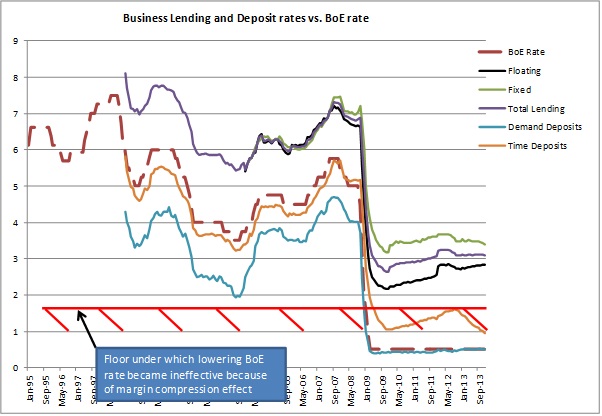

Above the threshold, the central bank base rate doesn’t matter much. Below, banks have to increase the margin on variable rate lending in order to cover their costs. This was evidenced by the following charts:

As the UK experience seems to show, banks stopped passing BoE rate cuts on to customers around a 2% BoE rate threshold. I called this phenomenon the ‘2%-lower bound’. I have yet to take a look at other countries.

Enter P2P lending.

By directly matching savers and borrowers and/or slicing and repackaging parts of loans, P2P platforms cut much of banks’ vital cost base. P2P platforms’ online infrastructure is much less cost-intensive than banks’ burdensome branch networks. As a result, it is well-known that both P2P savers and borrowers get better rates than at banks, by ‘cutting the middle man’. This is easy to explain using the equations described above, as costs approach zero in the P2P model. This is what Simon Cunningham called “the efficiency of Peer to Peer Lending”. As Simon describes:

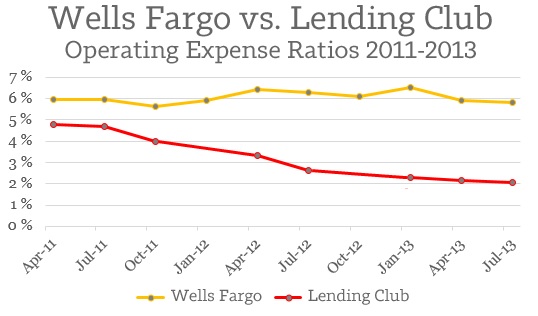

Looking purely at the numbers, Lending Club does business around 270% more efficiently than the comparable branch of a major American bank

Simon calculated the ‘efficiency’ of each type of lender by dividing the outstanding loans of Wells Fargo and Lending Club by their respective operational expenses (see chart below). I believe Lending Club’s efficiency is still way understated, though this would only become apparent as the platform grows. The marginal increase in lending made through P2P platforms necessitates almost no marginal increase in costs.

Perhaps P2P platforms’ disintermediation model could lubricate the banking channel of monetary policy the closer central banks’ base rate gets to the zero bound?

Possibly. From the charts above, we notice that the spread between savings rates and lending rates that banks require in order to cover their costs range from 2 to 3.5%. This is the cost of intermediation and maturity transformation. Banks hire experts to monitor borrowers and lending opportunities in-house and operate costly infrastructures as some of their liabilities (i.e. demand deposits) are part of the money supply and used by the payment system.

However, disintermediated demand and supply for loanable funds are (almost) unhampered by costs. As a result, the differential between borrowers and savers’ rate can theoretically be minimal, close to zero. That is, when the central bank lowers its target rate to 0%, banks’ deposit rates and short-term government debt yield should quickly follow. Time deposits and longer-dated government debt will remain slightly above that level. Savers would be incentivised to invest in P2P if the proposed rate at least matches them, adjusting for credit risk.

Let’s take an example: from the business lending chart above, we notice that business time deposit rates are currently quoted at around 1%. However, business lending is currently quoted at an average rate of about 3%. Banks generate income from this spread to pay salaries and other fixed costs, and to cover possible loan losses. Let’s now imagine that companies deposit their money in a time deposit-equivalent P2P product, yielding 1.5%. Theoretically, business lending could be cut to only slightly above 1.5%. This represents a much cheaper borrowing rate for borrowers.

P2P platforms would thus more closely follow the market process: the law of supply and demand. If most investments start yielding nothing, P2P would start attracting more investors through arbitrage, increasing the supply of loanable funds, and in turn lowering rates to the extent that they only cover credit risk.

The only limitation to this process stems from the nature of products offered by platforms. Floating rate products tend to be the most flexible and quickly follow changes in central banks’ rates. Fixed rate products, on the other hand, take some time to reprice, introducing a time lag in the implementation of monetary policy. I believe that most P2P products originated so far were fixed rate, though I could not seem to find any source to confirm that.

In the end, P2P lending is similar to market-based financing. The bond market already ‘cuts the middle man’, though there remains fees to underwriting banks, and only large firms can hope to issue bonds on the financial markets. In bond markets, investors exactly earn the coupon paid by borrowers. There is no differential as there is no middle man, unlike in banking. P2P platforms are, in a way, mini fixed-income markets that are accessible to a much broader range of borrowers and investors.

However, I view both bond markets and P2P lending as some version of 100%-reserve banking. While they could provide an increasingly large share of the credit supply, banks still have a role to play: their maturity transformation mechanism provides customers with a means of storing their money and accessing it whenever necessary. Would P2P platform start offering demand deposit accounts, their cost base would rise closer to that of banks, potentially raising the margin between savers and borrowers as described above.

It seems that, by partly shifting from the banking channel to the P2P channel over time, monetary policy could become more effective. I am sure that Yellen, Carney and Draghi will appreciate.

Recent Comments

| pslebow on ‘Sovereign money’:… | |

| pslebow on A critique of Werner’s view on… | |

| Hugo Kramer on Welcome to Spontaneous Fi… | |

| Nathan on A critique of Werner’s view on… | |

| Nathan on More, more, more money endogen… |

Trackbacks / Pingbacks