The demand for cash and its consequences

I came across this very interesting chart on Twitter (apparently actually coming from JP Koning’s excellent blog) showing the demand for cash over time in various countries.

The demand for cash is a form of money demand. And it varies over time and across cultures and evolves as technology changes. In most countries, the demand for cash increases around times when the number of transactions increases (Christmas/New year for instance, although some countries, such as South Korea, present an interesting pattern – not sure why). But there are very wide variations across countries: notice the difference between the Brazilian and the Swedish, British or Japanese demand for cash. Countries that have implemented developed card and/or cashless/contactless payment systems usually see their domestic demand for cash decrease and banks less under pressure to convert deposits into cash.

Overall, this has interesting consequences for the financial analysis of banks, bank management, and for the required elasticity of the currency. Every time the demand for cash peaks, banks find themselves under pressure to provide currency. Loans to deposit ratios increase as deposits decrease, making the same bank’s balance sheet look (much) worse at FY-end than at any point during the rest of the year. A peaking cash demand effectively mimics the effect of a run on the banking system. Temporarily, banks’ funding structure are weakened as reserves decrease and they rely on their portfolio of liquid securities to obtain short-term cash through repos with central banks or private institutions (or, at worst, calling in or temporarily not renewing loans)*. Central bankers are aware of this phenomenon and accommodate banks’ demand for extra reserves.

In a free banking system though, banks can simply convert deposits into privately-issued banknotes without having to struggle to find a cash provider. This ability allows free banks to economise on reserves and makes the circulating private currencies fully elastic. In a 100%-reserve banking system, cash balances at banks are effectively maintained in cash (i.e. not lent out). Therefore, any increase in the demand for cash should merely reduce those cash balances without any destabilising effects on banks’ funding structure (which aren’t really banks the way we know them anyway). However, if some of this demand for cash is to be funded through debt, this can end up being painful: in a sticky prices world, as available cash balances (i.e. loanable funds not yet lent out) temporarily fall while short-term demand for credit jump, interest rates could possibly reach punitive levels, with potentially negative economic consequences (i.e. fewer commercial transactions).

However, technological innovations can improve the efficiency of payment systems and lower the demand for cash in all those cases. Banks of course benefit from any payment technology that bypass cash withdrawals, alleviating pressure on their liquidity and hence on their profitability. Unfortunately not all countries seem willing to adopt new payment methods. The cases of France and the UK are striking. Despite similar economic structures and population, whereas the UK is adopting contactless and innovative payment solutions at a record pace, the French look much more reluctant to do so.

As the chart above did not include France, I downloaded the relevant data in order to compare the evolution and fluctuations of cash demand over the same period of time vs. the UK. Unsurprisingly, the demand for cash has grown much more in France than in the UK and fluctuations of the same magnitude have remained, despite the availability of internet and mobile transfers as well as contactless payments, which all have appeared over the last 15 years**. What this shows is that the demand for cash had a strong cultural component.

*Outright securities sale can also occur but if all banks engage in the sale of the same securities at the exact same time, prices crashes and losses are made in order to generate some cash.

** I have to admit that the cash demand growth for the UK looks surprisingly steady (apart from a small bump at the height of the crisis) with effectively no seasonal fluctuations.

Cachanosky on the productivity norm, Hayek’s rule and NGDP targeting

Nicolas Cachanosky and I should get married (intellectually, don’t get overexcited). Some time ago, I wrote about his very interesting paper attempting to start the integration of finance and Austrian capital theories. A couple of weeks ago, I discovered another of his papers, published a year ago, but which I had completely missed (coincidentally, Ben Southwood also discovered that paper at the exact same time).

Titled Hayek’s Rule, NGDP Targeting, and the Productivity Norm: Theory and Application, this paper is an excellent summary of the policies named above and the theories underpinning them. It includes both theoretical and practical challenges to some of those theories. Cachanosky’s paper reflects pretty much exactly my views and deserved to be quoted at length.

Cachanosky defines the productivity norm as “the idea that the price level should be allowed to adjust inversely to changes in productivity. […] In other words, money supply should react to changes in money demand, not to changes in production efficiency.” Referring to the equation of exchange, he adds that “because a change in productivity is not in itself a sign of monetary disequilibrium, an increase in money supply to offset a fall in P moves the money market outside equilibrium and puts into motion an unnecessary and costly process of readjustment”, which is what current central bank policies of price level targeting do. The productivity norm allows mild secular deflation by not reacting to positive ‘real’ shocks.

He goes on to illustrate in what ways Hayek’s rule and NGDP targeting resemble and differ from the productivity norm:

There are instances where the productivity norm illuminated economists that talked about monetary policy. Two important instances are Hayek during his debate with Keynes on the Great Depression and the market monetarists in the context of the Great Recession. Both, Hayek and market monetarism are concerned with a policy that would keep monetary equilibrium and therefore macroeconomic stability. Hayek’s Rule and NGDP Targeting are the denominations that describe Hayek’s and market monetarism position respectively. Taking the presence of a central bank as a given, Hayek argues that a neutral monetary policy is one that keeps constant nominal income (MV) stable. Sumner argues instead that

“NGDP level targeting (along 5 percent trend growth rate) in the United States prior to 2008 would similarly have helped reduce the severity of the Great Recession.”

Hayek’s Rule of constant nominal income can be understood in total values or as per factor of production. In the former, Hayek’s Rule is a notable case of the productivity norm in which the quantity of factors of production is assumed to be constant. In the latter case, Hayek’s rule becomes the productivity norm. However, for NGDP Targeting to be interpreted as an application that does not deviate from the productivity norm, it should be understood as a target of total NGDP, with an assumption of a 5% increase in the factors of production. In terms of per factor of production, however, NGDP Targeting implies a deviation of 5% from equilibrium in the money market.

Cachanosky then highlights his main criticisms of NGDP targeting as a form of nominal income control, that is the distinction between NGDP as an ‘emergent order’ and NGDP as a ‘designed outcome’. He says that targeting NGDP itself rather than considering NGDP as an outcome of the market can affect the allocation of resources within the NGDP: “the injection point of an increase in money supply defines, at least in the short-run, the effects on relative prices and, as such, the inefficient reallocation of factors of production.” In short, he is referring to the so-called Cantillon effect, in which Scott Sumner does not believe. I am still wondering whether or not this effect could be sterilized (in a closed economy) simply by growing the money supply through injections of equal sums of money directly into everyone’s bank accounts.

To Cachanosky (and Salter), “NGDP level matters, but its composition matters as well.” He believes that targeting an NGDP growth level by itself confuses causes and effects: “that a sound and healthy economy yields a stable NGDP does not mean that to produce a stable NGDP necessary yields a sound and healthy economy.” He points out that the housing bubble is a signal of capital misallocation despite the fact that NGDP growth was pretty stable in pre-crisis years.

I evidently fully agree with him, and my own RWA-based ABCT also points to lending misallocation that would also occur and trigger a crisis despite aggregate lending growth remaining stable or ‘on track’ (whatever that means). I should also add that it is unclear what level of NGDP growth the central bank should target. See the following chart. I can identify many different NGDP growth ‘trends’ since the 1940s, including at least two during the ‘great moderation’. Fluctuations in the trend rate of US NGDP growth can reach several percentage points. What happens if the ‘natural’ NGDP growth changes in the matter of months whereas the central bank continues to target the previous ‘natural’ growth rate? Market monetarists could argue that the differential would remain small, leading to only minor distortions. Possibly, but I am not fully convinced. I also have other objections to NGDP level targeting (related to banking and transmission mechanism), but this post isn’t the right one to elaborate on this (don’t forget that I view NGDP targeting as a better monetary policy than inflation targeting but a ‘less ideal’ alternative to free banking or the productivity norm).

Cachanosky also points out that NGDP targeting policies using total output (Py in the equation of exchange) and total transactions (PT) do not lead to the same result. According to him “the housing bubble before 2008 crisis is an exemplary symptom os this problem, where PT increases faster than Py.”

Cachanosky also points out that NGDP targeting policies using total output (Py in the equation of exchange) and total transactions (PT) do not lead to the same result. According to him “the housing bubble before 2008 crisis is an exemplary symptom os this problem, where PT increases faster than Py.”

Finally, he reminds us that a 100%-reserve banking system would suffer from an inelastic money supply that could not adequately accommodate changes in the demand for money, leading to monetary equilibrium issues.

I can’t reproduce the whole paper here, but it is full of very interesting (though quite technical) details and I strongly encourage you to take a look.

The end of banking? Not like this please

I recently read Jonathan McMillan’s The End of Banking, which I first heard of through FT Alphaville here (McMillan is actually a pseudonym to cover it two authors: an academic and a banker). I have mixed feelings about this book. I really wanted to agree with it. And I do, to some extent. But I simply cannot agree with a number of other points they make.

Their proposal to reform banking is as follows (see the book for details): lending can be disintermediated through P2P lending platforms (and equivalent), which both monitor potential borrowers through credit scoring and allocate savers’ funds to minimise the probability of losses. Marketplaces set up by platforms would enable savers to sell their investments to generate cash if needed. What about the payment system? Their solution is for non-bank FIs to continuously provide market liquidity a number of financial instruments using algorithmic trading. Current accounts would in fact be invested like mutual funds, which would instantly convert those investments into cash when required for payment. They also propose accounting rule changes to prevent corporations from creating money-like instruments.

As such, they propose to end banks’ inside money and have a financial system exclusively based on digital outside money controlled by a monetary authority. While they don’t classify it this way, it does seem to me to be some sort of 100%-reserve banking proposal: the money supply is fixed in the very-short term and exogenously-defined by the monetary authority.

What I agree with:

- The main thesis of the book is completely valid and is something I have also argued for a little while: technological disruptions are now allowing us to go beyond banking and disintermediate it. P2P lending, non-banking payment systems, decentralised payment frameworks and currencies, algorithm-driven credit scoring… In many areas, banks have almost become redundant. I totally adhere to the authors’ thesis (although credit scoring does have real limitations).

- Technological developments have facilitated regulatory arbitrage, if not enabled it. Computing power now allow banks to optimise their capital requirements through the use of complex models which, it is important to point out, are validated by regulators.

What I disagree with:

- The authors seem to believe that banking regulation is usually a good thing and cannot seem to understand the various distortions, bubbles and inefficiencies those regulations create. According to them, if only technology hadn’t boomed over the past three decades, the banking system would be more stable. I strongly disagree.

- I dislike the top-down banking reform approach taken by their thesis. Free markets, driven by technology, should decide under what form the next iteration of banking should arise.

- I also see weaknesses in their proposal. First, I cannot agree with their view that money belongs to the public sphere, and that IOUs must benefit from a state guarantee to qualify as money. This has been disproved by history over and over again. Second, I see their proposal to have algorithmic trading manage the payment system as not only unworkable, but also dangerous. As already witnessed, algorithmic trading is imperfect and can amplify crashes rather than prevent them. How their payment system would react during a crisis, when everyone tries to exit most investments and pile into a few others, is anyone’s guess. Mine is that the payment system would suddenly be down, paralysing the entire economy. To be fair, their treatment of cash is unclear: could we maintain a custody account comprising only digital cash in their framework?

- Their 100%-reserve banking reform does not address fluctuations in the demand for money. Centralised monetary authorities do neither have access to the right information, nor within the right timeframe, to accurately provide extra media of exchange when needed by the public. Private entities, in direct contact with the public, can.

- Finally, though this is a minor point, I disagree with their monetary policy stance. It is inaccurate to present price stability as ideal to avoid economic distortions: productivity increases should lead to mild deflation in a growing economy (see Selgin’s Less than Zero or any market monetarist or Austrian blog and research paper). I also reject their physical cash ban, from a libertarian standpoint: people should be able to withdraw cash if ever they wish to*. This would seriously limit their negative interest rates policy proposal.

Overall, it is a thought-provoking and interesting book, which also quite accurately describes our current banking system in its first part (mostly aimed at people who don’t know that much about banking). Its two authors are also right to point out the defects of regulation in an IT-intensive era. But, in my opinion, they draw the wrong conclusions and the wrong reform proposals from their original assessment.

* Here again, their treatment of cash is unclear: can cash be withdrawn in a digital form and maintain in a digital wallet outside the financial system? I doesn’t look so from their book but I cannot say for sure.

The rather curious and awkward alliance between statists and libertarians against free banking

Free banking has a very bad reputation within mainstream economics. As free banking scholars such as George Selgin, Larry White, Kevin Dowd or Steve Horwitz have been demonstrating over the past 30 years, this is mostly due to a misunderstanding of history. The track record of the systems that were as close as possible to free banking is crystal clear however: free banking episodes were more stable than any alternative banking frameworks.

However, this doesn’t seem to please many, from both sides of the political spectrum. Izabella Kaminska, a long-time libertarian critic from FT Alphaville, wrote a piece on the Alphaville blog partly criticizing non-central banking-based banking systems. In two separate replies (here and here), George Selgin highlighted all the self-serving ‘inaccuracies’ of her post (this is a euphemism). He also wrote a rebuttal in a follow-up post. Izabella skipped the interesting bits, accused Selgin of ad hominem, and wrote in turn another unsourced name-calling post on her own private blog. So much for the academic debate.

Perhaps more surprisingly, David Howden just posted a curious article on the Mises Institute website, which described the Fed as arising from “fractional-reserve free banks”. I say surprisingly, because Howden and the Mises Institute are at the other end of the political spectrum: libertarians, and often anarcho-capitalists. Nevertheless, he seemed to agree with Izabella Kaminska to an extent.

Unfortunately, Howden and Kaminska make the same mistake: they misread history, and/or focus far too much on US banking history. First, Howden claims that:

The year 1857 is a somewhat strange one for these clearinghouse certificates to make their first appearance. It was, after all, a full twenty years into America’s experiment with fractional-reserve free banking. This banking system was able to function stably, especially compared to more regulated periods or central banking regimes. However, the dislocation between deposit and lending activities set in motion a credit-fuelled boom that culminated in the Panic of 1857.

This could not be more inaccurate. The so-called ‘US free banking era’ had nothing much to do with free banking. And the credit boom and crises that follow were unrelated to either free banking or fractional reserves (see here for details, as well as below). I’d like Howden to explain why other fractional reserve free banking systems did not experience such recurring crises…

I have been left bewildered by Howden’s claim that privately-created clearinghouses were ‘illegal’ entities involved in ‘illegal’ activities (i.e. issuing clearinghouse certificates to get bank runs under control). Not only does this ironically sound like contradicting laissez-faire principles, but his whole argument rests on a lacking understanding of 19th century US banking.

What Howden got wrong is that, if American banks had such recurring liquidity issues before the creation of the Fed, it wasn’t due to their fractional reserve nature, but to the rule requiring them to back their note issues with government debt, thereby limiting the elasticity of those issues and the ability of banks to respond to fluctuations in the demand for money. Laws preventing cross-state branching also weakened banks as their ability to diversify was inherently limited. Banks viewed local clearinghouses as a way to make the system more resilient. It was a free-market answer to a state-created problem. This does not mean that the system was perfect of course. But Howden the libertarian blames a free-market solution here, and completely ignores the laws that originally created the problem.

Moreover, clearinghouses weren’t only a characteristic of the 19th century US banking system. They were present in several major free banking systems throughout history and set up by private parties (Scotland being a prime example). Their original goal wasn’t to create ‘illegal money claims’, but to help settle large volume of interbank transactions and economise on reserves: they were a necessary part of a well-functioning privately-owned free banking system. US clearinghouse certificates were merely a private solution to tame state-created liquidity crises. Those solutions were not perfect, but Howden is guilty of shooting the messenger here.

Clearinghouse-equivalents still exist today: the German savings and cooperative banks, as well as the Austrian Raiffeisen operate under the same sort of model, in which multiple tiny institutions park their reserves at their local central bank/clearinghouse. Finally, it is necessary to point out that clearinghouse would also surely exist in a full reserve banking system and would have the same basic goal: settle interbank payments.

Why a libertarian such as Howden would be against this natural laissez-faire process is beyond me. My guess is that at the end of the day, it all goes down to the fractional/full reserve banking debate within the libertarian space. Howden is trying at all costs to justify his views that full reserve banking would be more stable. But this time, such rhetoric is counter-productive and only demonstrates Howden’s ignorance of the issue (at least as described in this article). Using the fractional reserve argument to explain the 19th century US crises is self-serving and wholly inappropriate. Blaming a free-market reaction (i.e. the clearinghouse system) to such crises for the creation of the Fed completely misses the point. By doing so, and cherry-picking facts, Howden helps Kaminska’s arguments (despite fundamentally disagreeing with her) and shoots himself in the foot.

Update: I mistakenly thought that Peter Klein had written the article as his profile appeared on it. I should have paid more attention, but David Howden was the author. I have updated the post and apologised to Peter.

Update 2: I only just found out that David Glasner and Scott Sumner also wrote two good posts on free banking and Iza Kaminska/Selgin, followed by very interesting comments (here and here).

Photo: Marvel

Martin Wolf’s not so shocking shocks

Martin Wolf, FT’s chief economist, recently published a new book, The Shifts and the Shocks. The book reads like a massive Financial Times article. The style is quite ‘heavy’ and not always easy to read: Wolf throws at us numbers and numbers within sentences rather than displaying them in tables. This format is more adapted to newspaper articles.

Overall, it’s typical Martin Wolf, and FT readers surely already know most of the content of the book. I won’t come back to his economic policy advices here, as I wish to focus on a topic more adapted to my blog: his views on banking.

And unfortunately his arguments in this area are rather poor. And poorly researched.

Wolf is a fervent admirer of Hyman Minsky. As a result, he believes that the financial system is inherently unstable and that financial imbalances are endogenously generated. In Minsky’s opinion, crises happen. It’s just the way it is. There is no underlying factor/trigger. This belief is both cynical and wrong, as proved by the stability of both the numerous periods of free banking throughout history (see the track record here) and of the least regulated modern banking systems (which don’t even have lenders of last resort or deposit insurance). But it doesn’t fit Wolf’s story so let’s just forget about it: banking systems are unstable; it’s just the way it is.

Wolf identifies several points that led to the 2000s banking failure. In particular, liberalisation stands out (as you would have guessed) as the main culprit. According to him “by the 1980s and 1990s, a veritable bonfire of regulations was under way, along with a general culture of laissez-faire.” What’s interesting is that Wolf never ever bothers actually providing any evidence of his claims throughout the book (which is surprising given the number of figures included in the 350+ pages). What/how many regulations were scrapped and where? He merely repeats the convenient myth that the banking system was liberalised since the 1980s. We know this is wrong as, while high profile and almost useless rules like Glass-Steagall or the prohibition of interest payment on demand deposits were repealed in the US, the whole banking sector has been re-regulated since Basel 1 by numerous much more subtle and insidious rules, which now govern most banking activities. On a net basis, banking has been more regulated since the 1980s. But it doesn’t fit Wolf’s story so let’s just forget about it: banking systems were liberalised; it’s just the way it is.

Financial innovation was also to blame. Nevermind that those innovations, among them shadow banking, mostly arose from or grew because of Basel incentives. Basel rules provided lower risk-weight on securitized products, helping banks improve their return on regulatory capital. But it doesn’t fit Wolf’s story so let’s just forget about it: greedy bankers always come up with innovations; it’s just the way it is.

The worst is: Wolf does come close to understanding the issue. He rightly blames Basel risk-weights for underweighting sovereign debt. He also rightly blames banks’ risk management models (which are based on Basel guidance and validated by regulators). Still, he never makes the link between real estate booms throughout the world and low RE lending/RE securitized risk-weights (and US housing agencies)*. Housing booms happened as a consequence of inequality and savings gluts; it’s just the way it is.

All this leads Wolf to attack the new classical assumptions of efficient (and self-correcting) markets and rational expectations. While he may have a point, the reasoning that led to this conclusion couldn’t be further from the truth: markets have never been free in the pre-crisis era. Rational expectations indeed deserve to be questioned, but in no way does this cast doubt on the free market dynamic price-researching process. He also rightly criticises inflation targeting, but his remedy, higher inflation targets and government deficits financed through money printing, entirely miss the point.

What are Wolf other solutions? He first discusses alternative economic theoretical frameworks. He discusses the view of Austrians and agrees with them about banking but dismisses them outright as ‘liquidationists’ (the usual straw man argument being something like ‘look what happened when Hoover’s Treasury Secretary Mellon recommended liquidations during the Depression: a catastrophe’; sorry Martin, but Hoover never implemented Mellon’s measures…). He also only relies on a certain Rothbardian view of the Austrian tradition and quotes Jesus Huerta de Soto. It would have been interesting to discuss other Austrian schools of thought and writers, such as Selgin, White and Horwitz, who have an entirely different perception of what to do during a crisis. But he probably has never heard of them. He once again completely misunderstands Austrian arguments when he wonders how business people could so easily be misled by wrong monetary policy (and he, incredibly, believes this questions the very Austrian belief in laissez-faire), and when he cannot see that Austrians’ goals is to prevent the boom phase of the cycle, not ‘liquidate’ once the bust strikes…

Unsurprisingly, post-Keynesian Minsky is his school of choice. But he also partly endorses Modern Monetary Theory, and in particular its banking view:

banks do not lend out their reserves at the central bank. Banks create loans on their own, as already explained above. They do not need reserves to do so and, indeed, in most periods, their holdings of reserves are negligible.

I have already written at length why this view (the ‘endogenous money’ theory) is inaccurate (see here, here, here, here and here).

He then takes on finance and banking reform. He doubts of the effectiveness of Basel 3 (which he judges ‘astonishingly complex’) and macro-prudential measures, and I won’t disagree with him. But what he proposes is unclear. He seems to endorse a form of 100% reserve banking (the so-called Chicago Plan). As I have written on this blog before, I am really unsure that such form of banking, which cannot respond to fluctuations in the demand for money and potentially create monetary disequilibrium, would work well. Alternatively, he suggests almost getting rid of risk-weighted assets and hybrid capital instruments (he doesn’t understand their use… shareholder dilution anyone?) and force banks to build thicker equity buffers and report a simple leverage ratio. He dismisses the fact that higher capital requirements would impact economic activity by saying:

Nobody knows whether higher equity would mean a (or even any) significant loss of economic opportunities, though lobbyists for banks suggest that much higher equity ratios would mean the end of our economy. This is widely exaggerated. After all, banks are for the most part not funding new business activities, but rather the purchase of existing assets. The economic value of that is open to question.

Apart from the fact that he exaggerates banking lobbyists’ claims to in turn accuse them of… exaggerating, he here again demonstrates his ignorance of banking history. Before Basel rules, banks’ lending flows were mostly oriented towards productive commercial activities (strikingly, real estate lending only represented 3 to 8% of US banks’ balance sheets before the Great Depression). ‘Unproductive’ real estate lending only took over after the Basel ruleset was passed.

The case for higher capital requirements is not very convincing and primarily depends on the way rules are enforced. Moreover, there is too much focus on ‘equity’. Wolf got part of his inspiration from Admati and Hellwig’s book, The Bankers’ New Clothes. But after a rather awkward exchange I had with Admati on Twitter, I question their actual understanding of bank accounting:

While his discussion of the Eurozone problems is quite interesting, his description of the Eurozone crisis still partly rests on false assumptions about the banking system. Unfortunately, it is sad to see that an experienced economist such as Martin Wolf can write a whole book attacking a straw man.

* In a rather comical moment, Wolf finds ‘unconvincing’ that US government housing policy could seriously inflate a housing bubble. To justify his opinion, he quotes three US Republican politicians who said that this view “largely ignores the credit bubble beyond housing. Credit spreads declined not just for housing, but also for other asset classes like commercial real estate.” Let’s just not tell them that ‘Real Estate’ comprises both residential housing and CRE…

Blurry banks’ future is

A lot of articles on financial innovation and disruption in the FT over the last few days. Here, John Gapper argues that tech firms aim at using the existing financial system rather than challenge it. Here, Martin Arnold argues that banks shouldn’t forget their traditional branch network as this is how they make money through their oldest and wealthiest clients. Here, Luke Johnson argues that crowdfunding is riskier but also more exciting and, in a way, is the future.

John Gapper is right to point out that the regulatory and capital costs of setting up new bank-alike lending entities are very high. Yet he probably overstates his case. P2P lenders do not provide bank-type services: technology has enabled disintermediation by allowing investors to lend money (almost) directly to borrowers, but the money invested is stuck and does not represent a means of payment, unlike bank deposits. P2P lenders have the ability to take over a large market share of the lending market; and their business model does not require a high operating, regulatory and capital costs base (at least for now…). This is where the traditional intermediated lending channel could effectively approach death. On the other hand, P2P lender cannot handle deposits and banks still have a near-monopoly in this area.

Of course, we could imagine a 100%-reserve banking world in which the lending channel has moved entirely to P2P lenders, mutual and hedge funds and equivalent, whereas the deposit and payment system has moved entirely to Paypal-like payment firms. And this excludes alternative options offered by cryptocurrencies. In this world, banks are effectively dead.

Still, I am far from sure this would be the best solution: banks provide an elastic supply of currency (fractional reserve banking) that can adapt to the demand for money. (We could imagine a world without banks but still an elastic currency supply, if for instance the whole money supply only comprised competing cryptocurrencies. Let’s say this is highly unlikely to happen in the foreseeable future)

Banks can also survive by benefiting from those technologies (if ever they dare touching their antique IT systems…). As I’ve been saying for a while, banks can leverage their huge customer base to set up their own P2P/crowdfunding platform. This has already started to happen: RBS just announced the creation of its own P2P lending platform, Santander announced a partnership with Funding Circle, Lending Club is developing partnerships with many US banks. Banks could earn a fee from referring customers to their own (or third-party) platform, while deleveraging and reducing their on-balance sheet credit risk. Investors would earn more on those investments than on time deposits, but bear some risk.

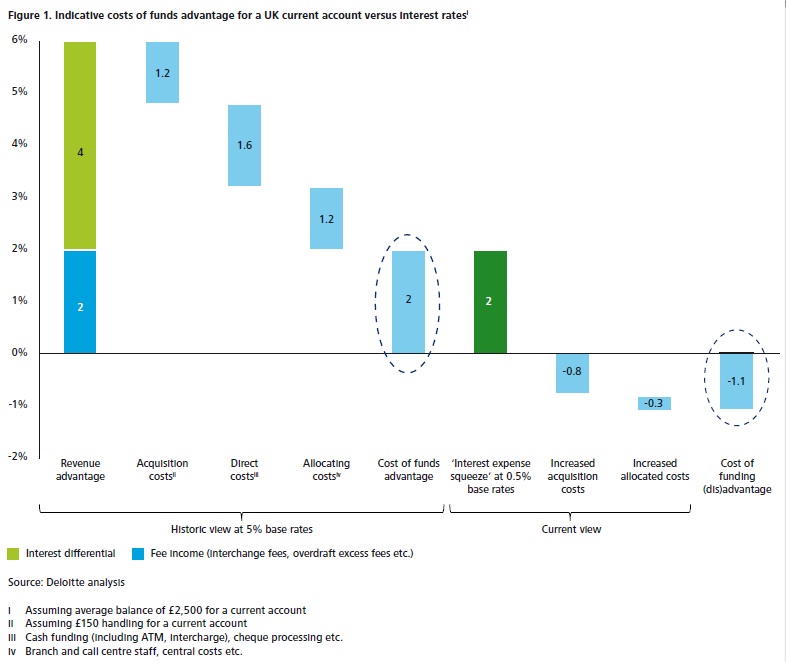

Whatever they decide to do, banks will have to adapt. But timing is key. Gapper referred to this recent, excellent, Deloitte report. They explain the margin compression effect (due to low base rates)*, which depresses banks’ profitability and adds another challenge on top of those that tech-enabled competitors and regulation already represent. According to them, closing down branches and moving online does not sufficiently slash cost to offset the decrease in net interest income. Closing down branches too quickly could also hurt banks by alienating the part of their client base born before the internet age. Deloitte provides evidence that a radical restructuring of IT systems could significantly improve returns, but this requires investments, which banks aren’t necessarily willing to undertake in a period of below-cost of capital RoE.

As the internet makes it easier for customers to compare pricing through aggregators and hence more difficult for banks to ‘extract value’ from them (what they call ’privileged access’), they recommend banks enhance ‘customer proposition’ (i.e. use ‘big data’) and focus on SME lending. As I’ve argued on this blog, capital regulation makes this difficult. They also indeed support the idea of in-house P2P platform, mostly to focus on local SMEs. This would help with capital requirements by maintaining SME exposures off-balance sheet, the risk borne by customers. Banks could effectively become risk assessment providers: rating lending opportunities to help customers (which include investment funds that don’t have such in-house capabilities) make their investment choices.

At the end of the day, banks are indeed likely to die if they don’t adapt. But also if they adapt too quickly. We could however see in the future surviving banks increasingly becoming like non-banks and non-banks increasingly providing banking services. The distinction between both types of institutions is likely to get very blurry. (That is, if regulation doesn’t kill non-banks first)

* Ben Southwood reiterated that interest rates are determined by markets and not by central banks. I already wrote responses to those claims here and here. Scott Sumner just mentioned his latest post, so I thought it would be a good idea to share Deloitte’s insight and own explanation of the margin compression effect and why “the spreads between Bank Rate and market rates seem to be narrow and fairly consistent—until they’re not.” In reality, lending spreads fluctuate only slightly when rates are above a certain threshold (i.e. banks’ risk-adjusted operating costs) and widen when they drop below it (explaining the “until they’re not”; see my previous posts). The fact that the “until they’re not” occurs does not imply that lending rates are “determined by the market”.

Here’s Deloitte own version:

The interest rate paid by banks on current accounts is typically lower than those paid for lump sum deposits (and the rates paid to borrow in the wholesale markets). However, this interest rate does not reflect the full cost of acquiring and servicing these current accounts. In the past, these acquisitions and servicing costs were offset by the fact that banks did not have to pay very high interest rates on current accounts.

Until the financial crisis, central bank interest rates (the ‘base rate’) were traditionally much higher. This meant that current account rates could easily be 500 or more basis points (hundredths of a percentage point) below lump-sum deposit rates.

Because base rates are at unprecedented lows, that maths does not work. Base rates have been low since 2009, and central bankers have signalled that they are likely to stay that way for some time yet. Figure 1 shows the economics of current accounts in the UK, where banks typically do not charge for them. A 200 basis point margin generated by current accounts when base rates are at 5 per cent turns into a 110 basis point loss at a 0.5 per cent base rate.

News digest: P2P lending and HFT, CoCo bonds, Co-op Bank…

Ron Suber, President at Prosper, the US-based P2P lending company, sent me a very interesting NY Times article a few days ago. The article is titled “Loans That Avoid Banks? Maybe Not.” This is not really accurate: the article indeed mentions institutional investors such as mutual and hedge funds increasingly investing in bundles of P2P loans through P2P platforms, but never refers to banks. Unlike what the article says, I don’t think platforms were especially set up to bypass institutional investors… They were set up to bypass banks and their costly infrastructure and maturity transformation.

Some now fear that the industry won’t be ‘P2P’ for very long as institutional investors increasingly take over a share of the market. I think those beliefs are misplaced. Last year, I predicted that this would create opportunities for niche players to enter the market, focusing on real ‘P2P’.

A curious evolution is the application of high-frequency trading strategies to P2P. I haven’t got a lot of information about their exact mechanisms, but I doubt they would resemble the ones applied in the stock market given that P2P is a naturally illiquid and borrower-driven market.

The main challenge of the industry at the moment seems to be the lack of potential customer awareness. Despite offering better deals (i.e. cheaper borrowing rates) than banks, demand for loans remains subdued and the industry tiny next to the banking sector.

In this FT article, Alberto Gallo, head of macro-credit research at RBS, argues that regulators should intervene on banks’ contingent convertible bonds’ risks. I think this is strongly misguided. Investors’ learning process is crucial and relying on regulators to point out the potential risks is very dangerous in the long-term. Not only such paternalism disincentives investors to make their own assessment, but also regulators have a very bad track record at spotting risks, bubbles and failures (see Co-op bank below).

This piece here represents everything that’s wrong with today’s banking theory:

We know that a combination of transparency, high capital and liquidity requirements, deposit insurance and a central bank lender of last resort can make a financial system more resilient. We doubt that narrow banking would.

Not really… They also argue that 100% reserve banking would not prevent runs on banks:

The mutual funds of the narrow banking world would be subject to the same runs. Indeed, recent research highlights that – in the presence of small investors – relatively illiquid mutual funds are more likely to face exit in the event of past bad performance. […] Since the mutual funds would be holding illiquid loans – remember, they are taking over functions of banks – collective attempts at liquidation to meet withdrawal requests would lead to ruinous fire sales.

They misunderstand the purpose of such a banking system. Those ‘mutual funds’ would not be similar to the ones we currently have, which invests in relatively liquid securities on the stock market, and can as a result exit their positions relatively quickly and easily. Those 100% reserve funds would invest in illiquid loans and investors in those funds would have their money contractually locked in for a certain time. With no legal power to withdraw, no risk of bank run.

The FT reported a few days ago the results of the investigation on the Co-operative bank catastrophe. Despite regulators not noticing any of the problems of the bank, from corporate governance to bad loans and capital shortfall, as well as approving unsuitable CEOs and mergers, the report recommends to… “heed regulatory warnings.” I see…

The impossible sometimes happens: I actually agree with Paul Krugman’s last week piece on endogenous money. No guys, the BoE paper didn’t reveal any mystery of banking or anything…

Finally, Chris Giles wrote a very good article in the FT today, very clearly highlighting the contradictions in the Bank of England policies and speeches, and their tendency to be too dovish whatever the circumstances:

Mark Carney, the governor, certainly displays dovish leanings. Before he took the top job, he said monetary policy could be tightened once growth reached “escape velocity”. But now that growth has shot above 3 per cent, he advocates waiting until the economy has “sustained momentum” – without acknowledging that his position has changed. His attitude to prices also betrays a knee-jerk dovishness. When inflation was above target, he stressed the need to look at forecasts showing a more benign period ahead. Now that inflation is lower it is apparently the short-term data that matters – and it justifies stimulus.

So much for forward guidance… Time to move to a rule-based monetary policy?

Could P2P Lending help monetary policy break through the ‘2%-lower bound’?

The ‘cut the middle man’ effect of P2P lending is already celebrated for offering better rates to both lenders and borrowers. But what many people miss is that this effect could also ease the transmission mechanism of central banks’ monetary policy.

I recently explained that the banking channel of monetary policy was limited in its effects by banks’ fixed operational costs. I came up with the following simplified net profit equation for a bank that only relies on interest income on floating rate lending as a source of revenues:

Net Profit = f1(central bank rate) – f2(central bank rate) – Costs, with

f1(central bank rate) = interest income from lending

= central bank rate + margin and,

f2(central bank rate) = interest expense on deposits

= central bank rate – margin

(I strongly advise you to take a look at the details here, which was a follow-up to my response to Ben Southwood’s own response on the Adam Smith Institute blog to my original post…which was also a response to his own original post…)

Consequently, banks can only remain profitable (from an accounting point of view) if the differential between interest income and interest expense (i.e. the net interest income) is greater than their operational costs:

Net interest income >= Costs

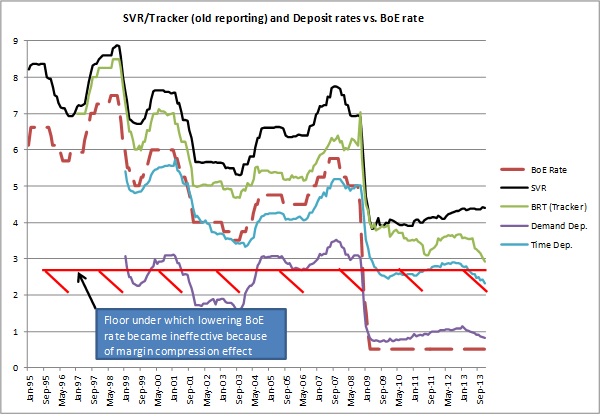

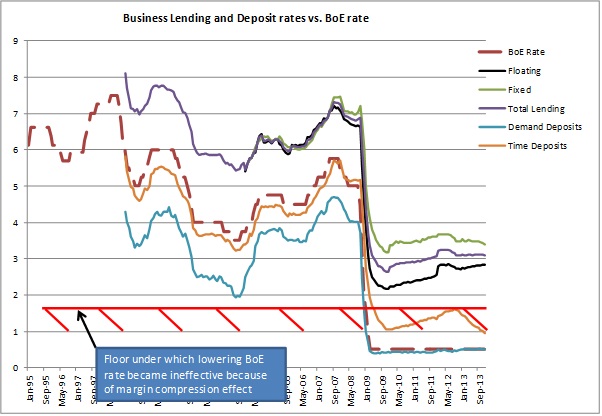

When the central bank base rate falls below a certain threshold, f2 reaches zero and cannot fall any lower, while f1 continues to decrease. This is the margin compression effect.

Above the threshold, the central bank base rate doesn’t matter much. Below, banks have to increase the margin on variable rate lending in order to cover their costs. This was evidenced by the following charts:

As the UK experience seems to show, banks stopped passing BoE rate cuts on to customers around a 2% BoE rate threshold. I called this phenomenon the ‘2%-lower bound’. I have yet to take a look at other countries.

Enter P2P lending.

By directly matching savers and borrowers and/or slicing and repackaging parts of loans, P2P platforms cut much of banks’ vital cost base. P2P platforms’ online infrastructure is much less cost-intensive than banks’ burdensome branch networks. As a result, it is well-known that both P2P savers and borrowers get better rates than at banks, by ‘cutting the middle man’. This is easy to explain using the equations described above, as costs approach zero in the P2P model. This is what Simon Cunningham called “the efficiency of Peer to Peer Lending”. As Simon describes:

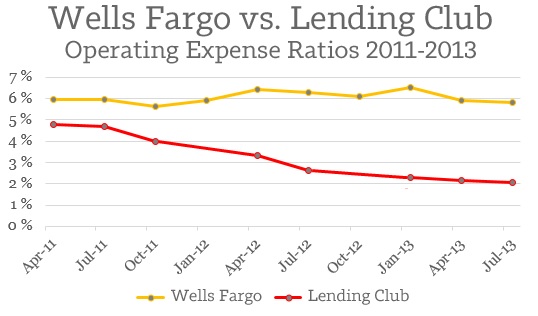

Looking purely at the numbers, Lending Club does business around 270% more efficiently than the comparable branch of a major American bank

Simon calculated the ‘efficiency’ of each type of lender by dividing the outstanding loans of Wells Fargo and Lending Club by their respective operational expenses (see chart below). I believe Lending Club’s efficiency is still way understated, though this would only become apparent as the platform grows. The marginal increase in lending made through P2P platforms necessitates almost no marginal increase in costs.

Perhaps P2P platforms’ disintermediation model could lubricate the banking channel of monetary policy the closer central banks’ base rate gets to the zero bound?

Possibly. From the charts above, we notice that the spread between savings rates and lending rates that banks require in order to cover their costs range from 2 to 3.5%. This is the cost of intermediation and maturity transformation. Banks hire experts to monitor borrowers and lending opportunities in-house and operate costly infrastructures as some of their liabilities (i.e. demand deposits) are part of the money supply and used by the payment system.

However, disintermediated demand and supply for loanable funds are (almost) unhampered by costs. As a result, the differential between borrowers and savers’ rate can theoretically be minimal, close to zero. That is, when the central bank lowers its target rate to 0%, banks’ deposit rates and short-term government debt yield should quickly follow. Time deposits and longer-dated government debt will remain slightly above that level. Savers would be incentivised to invest in P2P if the proposed rate at least matches them, adjusting for credit risk.

Let’s take an example: from the business lending chart above, we notice that business time deposit rates are currently quoted at around 1%. However, business lending is currently quoted at an average rate of about 3%. Banks generate income from this spread to pay salaries and other fixed costs, and to cover possible loan losses. Let’s now imagine that companies deposit their money in a time deposit-equivalent P2P product, yielding 1.5%. Theoretically, business lending could be cut to only slightly above 1.5%. This represents a much cheaper borrowing rate for borrowers.

P2P platforms would thus more closely follow the market process: the law of supply and demand. If most investments start yielding nothing, P2P would start attracting more investors through arbitrage, increasing the supply of loanable funds, and in turn lowering rates to the extent that they only cover credit risk.

The only limitation to this process stems from the nature of products offered by platforms. Floating rate products tend to be the most flexible and quickly follow changes in central banks’ rates. Fixed rate products, on the other hand, take some time to reprice, introducing a time lag in the implementation of monetary policy. I believe that most P2P products originated so far were fixed rate, though I could not seem to find any source to confirm that.

In the end, P2P lending is similar to market-based financing. The bond market already ‘cuts the middle man’, though there remains fees to underwriting banks, and only large firms can hope to issue bonds on the financial markets. In bond markets, investors exactly earn the coupon paid by borrowers. There is no differential as there is no middle man, unlike in banking. P2P platforms are, in a way, mini fixed-income markets that are accessible to a much broader range of borrowers and investors.

However, I view both bond markets and P2P lending as some version of 100%-reserve banking. While they could provide an increasingly large share of the credit supply, banks still have a role to play: their maturity transformation mechanism provides customers with a means of storing their money and accessing it whenever necessary. Would P2P platform start offering demand deposit accounts, their cost base would rise closer to that of banks, potentially raising the margin between savers and borrowers as described above.

It seems that, by partly shifting from the banking channel to the P2P channel over time, monetary policy could become more effective. I am sure that Yellen, Carney and Draghi will appreciate.

Izabella Kaminska gets confused on 100%-reserve banking, or collateral, unless it’s… wait, I’m confused now

Meanwhile, Izabella Kaminska in the FT had an interesting (as usual), but very confused and confusing, blog post. I asked whether or not she was reading my blog given that some of her claims pretty much reflect mine (she calls the shadow banking system a “decentralised full-reserve banking system that just happens to run parallel with the official fractional system we are used to.” Compare that with my “[…] parallel 100%-reserve banking system. The shadow banking system is effectively some version of a 100%-reserve banking.”). But the similarities stop here. She sounds very confused… She gets mixed up between various terms, principles and concepts and tries to hide it behind quite complex wordings.

She mixes collateralised lending with 100%-reserve and uncollateralised lending with money creation. They are in fact totally unrelated. A bank or shadow bank can be fractional-reserve-based or 100%-reserve-based, which simply relates to whether or not a bank lends out a share of its deposits or if it maintains them in full in its vaults. Collateralised lending is, well, just lending provided against collateral (which can be almost any type of assets). Both fractional and 100%-reserve banks can lend against collateral in order to minimise the risk of loss in case of default. 100%-collateralised lending is not 100%-reserve.

True, 100%-cash collateralised lending could be thought of as some form of 100%-reserve banking as the cash reserve at the bank would virtually never depart from the deposit base amount. For example, if a fractional bank collects USD100 in deposits and lends out USD90, it only keeps 10% of cash deposits in reserve. If, though, it lends out USD90 collateralised against USD90 of cash, then it ends up with USD100 in its vault, the same amount as the deposit base (although there will be limitations on the liquidity of the cash as the collateral will likely be ‘stuck’ until repayment or default). But, following her claim, a mortgage bank would be a 100%-reserve bank as the value of the housing portfolio on which lending is secured is worth more than the amount of lending. This is obviously wrong. Unless houses are now a generally-accepted medium of exchange?

Then she claims that “the official banking sector, for example, has the capacity to make uncollateralised investments in growth areas it feels are promising regardless of whether borrowers have collateral, or whether they can be fully funded.” Not really. First, banks usually collateralise between a quarter and more than 100% of their lending. Second, “uncollateralised investments in growth areas it feels are promising regardless of whether borrowers have collateral” is called venture capital and is clearly not what banks do. Venture capital funds, business angels, and some crowdfunding and P2P platforms are here for that (you could also probably add the junk bond market to the list). She then adds that, in contrast to banks, “the shadow banking sector’s strength, of course, is that it is prepared to service those entities (whether directly or indirectly) the official banking sector is not prepared to service, thanks to a greater emphasis on collateral or funding.” As I just said, this is not the case. Venture capital-type investments cannot accept collateral as… there is none! This is why they are high-risk.

According to Izabella, there is a reason why shadow banks cannot create money: their use of collateral. While it is true that (most, probably all) shadow banks cannot create money, it is not because they lend against collateral as described above. A lot of shadow banks don’t lend against collateral: think most money market funds, P2P lending, hedge funds, mutual funds, payday lenders…or simply the bond market! But they don’t create money either! They only transfer cash.

In the comment section she also seems to claim that fractional reserve banking is an innovation of our modern banking system. Where did she get that? Fractional reserves have been used since antiquity: the use of the ‘monetary irregular-deposit’ contract in classical Roman law gave rise to fractional reserves as deposits were mixed with other ones of equivalent nature (as opposed to the mutuum, or monetary loan contract, which is similar to what we could describe as today’s mutual funds for example). Despite the illegality of lending out irregular-deposits, some bankers took advantage of the fungibility of money, and of the fact that many irregular-deposits were rarely withdrawn, to lend out a part of their deposit base. The ‘bank’ of Pope Callistus I (see photo) failed as it was unable to return the irregular-deposits on demand. Other examples of failed banks exist at this period but fractional reserves really took off from the late middle ages in Europe.

Not everything is wrong in her article as I mentioned at the beginning of my post. She’s right to claim that regulation would only displace risk to another corner of the financial system that shadow banking is merely a response to the regulatory-incentivised under-banked part of the economic system, and that P2P lending is a kind of shadow banking. But too many confusions or misunderstandings around collateral, money creation, bank funding, bank reserves, etc., obfuscate the topic.

Financial innovation is back with a vengeance

What didn’t we hear about financial innovation throughout the crisis? Whereas innovation in general is good, financial innovation on the other hand was the worst possible thing coming out of a human mind. Paul Volcker, former Chairman of the Fed, famously declared that the ATM was the only useful financial innovation since the 1980s. Harsh.

True, some financial innovations are better than others. In particular, those used to bypass regulatory restrictions are more dangerous, not because they are intrinsically evil or anything, but simply because their often complex legal structure makes them opaque and difficult for external analysts and investors to analyse. This famous 2010 Fed paper attempted to map the shadow banking system (see picture), and usefully stated that not all shadow banking (and financial innovations) activities were dangerous (but those specifically designed to avoid regulations were). Ironically (and typically…) one of the first innovations to ever appear within the shadow banking system was money market funds. What was the rationale behind their creation? In the 1960s and 1970s in the US, interest payment on bank demand deposits was prohibited and capped on other types of deposits. The resulting financial repression through high inflation pushed financial innovators to come up with a way of bypassing the rule: money market funds became a deposit-equivalent that paid higher interests. Today we blame money market funds for being responsible for a quiet run on banks during the crisis, precipitating their fall. It would just be good to remember that without such stupid regulation in the first place, money market funds might have never existed…

The last decade has seen the growth of two particularly interesting innovations within the shadow banking system: one was relatively hidden (securitisation) while the other one grew in the spotlight (crowdfunding/peer-to-peer lending). One was deemed dangerous. The other one was more than welcome (ok, not in France). What had to happen happened: they are now combining their strength.

Various types of crowdfunding exist: equity crowdfunding, P2P lending, project financing… Today I’m going to focus on P2P lending only. What started as platforms enabling individuals to lend to other individuals are now turning into massive gates for complex institutional investors to lend to individuals and SMEs. Given the retreat of banks from the SME market (thank you Basel), various institutional investors (mutual and hedge funds, insurance firms) thought about diversifying their investments (and maximising their returns) by starting to offer loans to individuals and companies they normally can’t reach.

Basically, those funds had a few options: developing the capabilities to directly lend to those customers, investing in securitised portfolios of bank loans, or investing in securitised portfolios of P2P loans. The first option was very complex to implement and the required infrastructure would take a long time to develop. The second option had already existed for a little while, but was dependent on banks lending to customers, which current regulations limit due to higher capital requirements on such loans. The third option, on the other hand, allowed funds to maximise returns and attract more potential borrowers thanks to the reduction of the cost of borrowing by disintermediating banks. And funds could also strike deals with those still tiny online platforms that would have never happened with massive banks.

While securitisation sounds scary, it is actually only a simpler way of investing in loans of small sizes (the alternative being to invest in every single loan, some of them amounting to only USD500… Not only many funds don’t have the capability of doing such things, but many have also restrictions about the types of asset class and amounts they can invest in). Securitisation also bypasses Wall Street investment banks: funds directly invest in P2P loans, package them and sell them on to other investors while retaining a ‘tranche’ in the deal, which absorbs losses first. Now some entrepreneurs are even talking of setting up secondary markets to trade investments in loans, pretty much like a smaller version of the bond market.

Is this a welcome evolution for the P2P industry? I would say that it is a necessary evolution. It is once again a spontaneous development that merely reflects the need for funding of the P2P industry, which small retail investors cannot fulfil (unless all investment funds’ customers start withdrawing their money to directly invest in P2P, which is highly unlikely). Many start to think that large institutional investors will end up crowding out small retail investors. Possibly, but as long as regulation remains light, keeping barriers to entry low, new platforms only accepting retail investors could well appear if the demand is present.

All this is fascinating. Not only because technology and the internet enables new ways of channelling funds from savers to borrowers, but also because this is the growth of a parallel 100%-reserve banking system. The shadow banking system is effectively some version of a 100%-reserve banking. And it keeps growing through those various innovations. As I argued in a previous post, this may well have implications for monetary policy that current central banks and economists don’t take into account. A 100%-reserve banking system does not have a deposit multiplier and consequently does not have an elastic currency to respond to a sudden increase or decrease in the demand for money. However, such a system perfectly matches savers’ and borrowers’ intertemporal preferences, limiting malinvestments. Nonetheless, we for now remain in a mix system of 100% reserve (most of shadow banking) and fractional reserves (traditional banking). It would still be interesting to study the possible policy implications of a growth in the 100%-reserve part of the economy.

Recent Comments