Is the zero lower bound actually a ‘2%-lower bound’?

Following my recent reply to Ben Southwood on the relationship between mortgage rates, BoE base rate and banks’ margins and profitability (see here and here), a question came to my mind: if the BoE rate can fall to the zero lower bound but lending rates don’t, should we still speak of a ‘zero lower bound’? It looks to me that, strictly in terms of lending and deposit rates, setting the base rate at 0% or at 2% would have changed almost nothing at all, at least in the UK.

The culprit? Banks’ operational expenses. Indeed, it looks like the only way to break through the ‘2%-lower bound’ would be for banks to slash their costs…

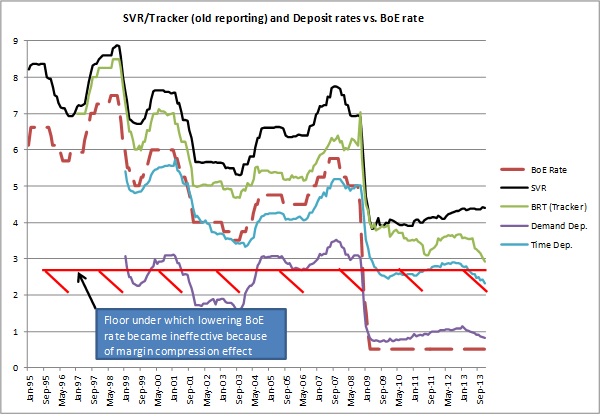

Let’s take a look at the following mortgage rates chart from one of my previous posts:

From this chart, it is clear that lowering the BoE rate below around 2.5% had no further effect on lowering mortgage rates. As described in my other posts, this is because banks’ net interest income necessarily has to be higher than expenses for them to remain profitable. When the BoE rate falls below a certain threshold that represents operational expenses, banks have to widen the margins on loans as a result.

From this chart, it is clear that lowering the BoE rate below around 2.5% had no further effect on lowering mortgage rates. As described in my other posts, this is because banks’ net interest income necessarily has to be higher than expenses for them to remain profitable. When the BoE rate falls below a certain threshold that represents operational expenses, banks have to widen the margins on loans as a result.

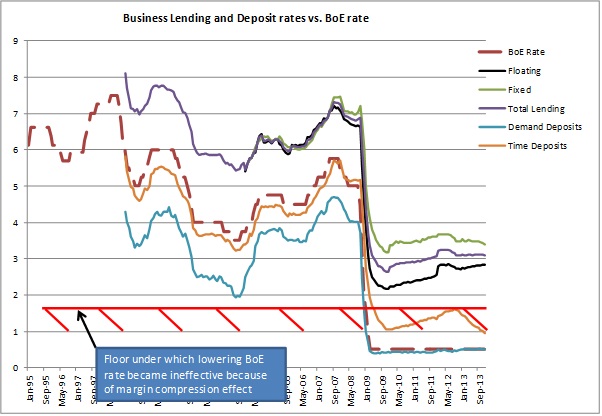

What about business lending rates? Since business lending is funded by both retail and corporate deposits (and excluding wholesale funding for the purpose of the exercise), the analysis must take a different approach. Banks don’t often disclose the share of corporate deposits within their funding base, but I managed to find a retail/corporate deposit split of 75%/25% at a large European peer, which I am going to use as a rough approximation to estimate banks’ business lending margins. Here are the results of my calculations (first chart: margin over time deposits, second chart: margin over demand deposits):

No surprise here, the same margin compression effect appears as a result of the BoE rate collapsing (as well as Libor, as floating corporate lending is often calculated on a Libor + margin basis, unlike mortgages, which are on a BoE + margin basis). Before that period, changes in the BoE and Libor rates had pretty much no effect on margins. After the fall, banks tried to rebuild their margins by progressively repricing their business loan books upward (i.e. increasing the margins over Libor).

No surprise here, the same margin compression effect appears as a result of the BoE rate collapsing (as well as Libor, as floating corporate lending is often calculated on a Libor + margin basis, unlike mortgages, which are on a BoE + margin basis). Before that period, changes in the BoE and Libor rates had pretty much no effect on margins. After the fall, banks tried to rebuild their margins by progressively repricing their business loan books upward (i.e. increasing the margins over Libor).

Here again we can identify a 1.5% BoE rate floor, under which lowering the base rate does not translate into cheaper borrowing for businesses:

This has repercussions on monetary policy. The banking/credit channel of monetary policy aims at: 1. easing the debt burden on indebted household and businesses and, 2. stimulating investments and consumption by making it cheaper to borrow. However, it seems like this channel is restricted in its effectiveness by banks’ ability in passing the lower rate on to customers. Banks’ short-term fixed cost base effectively raises the so-called zero lower bound to around 2%. The only way to make the transmission mechanism more efficient would be for banks to drastically improve their cost efficiency and have assets of good-enough quality not to generate impairment charges, which is tough in crisis times. Unfortunately, there are limits to this process, and a bank without employee and infrastructure is unlikely to lend in the first place…

This has repercussions on monetary policy. The banking/credit channel of monetary policy aims at: 1. easing the debt burden on indebted household and businesses and, 2. stimulating investments and consumption by making it cheaper to borrow. However, it seems like this channel is restricted in its effectiveness by banks’ ability in passing the lower rate on to customers. Banks’ short-term fixed cost base effectively raises the so-called zero lower bound to around 2%. The only way to make the transmission mechanism more efficient would be for banks to drastically improve their cost efficiency and have assets of good-enough quality not to generate impairment charges, which is tough in crisis times. Unfortunately, there are limits to this process, and a bank without employee and infrastructure is unlikely to lend in the first place…

Don’t get me wrong though, I am not saying that lowering the BoE rate (and unconventional monetary policies such as QE) is totally ineffective. Lowering rates also positively impact asset prices and market yields, ceteris paribus. This channel could well be more effective than the banking one but it isn’t the purpose of this post to discuss that topic. Nevertheless, from a pure banking channel perspective, one could question whether or not it is worth penalising savers in order to help borrowers that cannot feel the loosening.

PS: I am not aware of any academic paper describing this issue, so if you do, please send me the link!

Recent Comments

| pslebow on ‘Sovereign money’:… | |

| pslebow on A critique of Werner’s view on… | |

| Hugo Kramer on Welcome to Spontaneous Fi… | |

| Nathan on A critique of Werner’s view on… | |

| Nathan on More, more, more money endogen… |

Trackbacks / Pingbacks