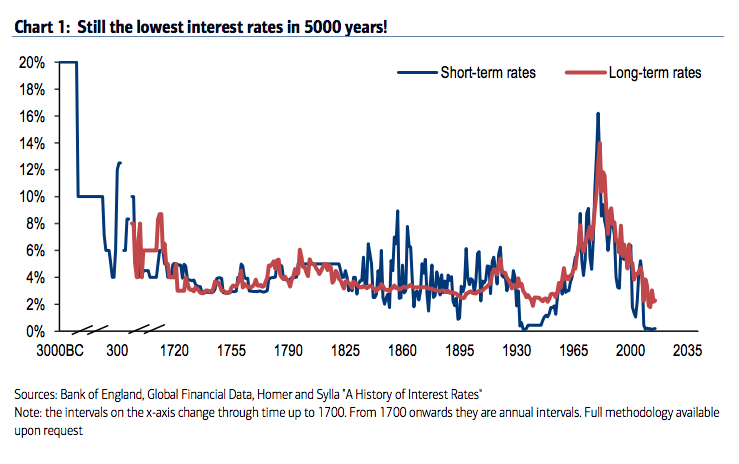

150 years of nominal interest rates distortion?

A very useful post was published on the FT Alphaville blog by David Keohane. It shows nominal interest rates levels over the past 5000 years in three different charts.

The first one comes from Andy Haldane, from the BoE:

The second one from Hartnett, from Bank of America Merrill Lynch:

The last one comes from Costa Vayenas, from UBS:

Those charts use different sources so don’t look exactly the same. Nevertheless, they all show the same striking facts. In particular, the 20th and 21st centuries seem to have been huge monetary experiments: nominal rates went both sky high and negative within a few decades… Within a period of barely more than a 100 years, rates fell to the bottom (Great Depression), then jumped ridiculously high to counteract inflationary pressure in the 1970s and 1980s (i.e. the disastrous impact of crude Keynesian macro theory) that resulted from the money multiplier recovering after the Depression, then fell to the bottom again or even negative (Great Recession).

Remember: the 20th century was the period of the generalisation of central banking. It definitely looks like they have been successful at stabilising money markets (and remember this paper by Selgin and White, which shows how successful the Fed has been at stabilising the value of the dollar since its creation). In short, great success for central bankers*.

Another interesting fact is that nominal rates started to wildly fluctuate once the BoE was granted the exclusive right to issue banknotes in the London area in 1844. Unlikely to be a coincidence.

Something that worries me though is the current state of monetary policy throughout most of the Western world. Rates are stuck at the zero bound or even went negative for the first time in history. Perhaps this is justified. But I keep wondering whether our economies currently are in a worse state than at any time in history to justify such low rates (although to be fair, Haldane’s chart does show that long-term nominal rates remain around historical levels – but not Hartnett’s).

Real interest rate charts would also have been interesting for a more comprehensive analysis of the underlying drivers of the rate movements we see here. If ever anyone has access to real interest rate data that go back several hundred years, please let me know (probably hard, or even impossible, to obtain as historical inflation data is likely to be non-existent).

In a parallel world, the BoE recently opened a forum weirdly titled ‘Building real markets for the good of the people’ which, putting aside the slightly communist tone of its chosen name, describes markets are “prone to excess” if “left unattended”**. This is another great example of central banks succeeding in making public opinion believe that economic issues originate, not in central bankers’ failed policies, not in economically distortive banking regulation, but in free markets. Which aren’t actually free. Here again Selgin had a remarkable article reporting how the Fed promotes itself.

One reaches some sort of supreme irony after contrasting those BoE statements with the charts above. Worse, central banks’ power, despite the instability they have brought to the economy for 100+ years, is growing, and their adherence to the rule of law has all but vanished (see Salter here and here arguing that a stable monetary framework such as the gold standard or NGDP targeting would respect the rule of law, unlike current regimes, and that adherence to the rule of law should be the primary consideration for judging monetary regimes).

*Sarcasm, of course

**I’m not sure what’s going on at the BoE, but a culture shift seems to be happening: anti-market rhetoric and rather strange monetary and banking theories are overtaking the institution (see my posts on endogenous money theory)

The demand for cash and its consequences

I came across this very interesting chart on Twitter (apparently actually coming from JP Koning’s excellent blog) showing the demand for cash over time in various countries.

The demand for cash is a form of money demand. And it varies over time and across cultures and evolves as technology changes. In most countries, the demand for cash increases around times when the number of transactions increases (Christmas/New year for instance, although some countries, such as South Korea, present an interesting pattern – not sure why). But there are very wide variations across countries: notice the difference between the Brazilian and the Swedish, British or Japanese demand for cash. Countries that have implemented developed card and/or cashless/contactless payment systems usually see their domestic demand for cash decrease and banks less under pressure to convert deposits into cash.

Overall, this has interesting consequences for the financial analysis of banks, bank management, and for the required elasticity of the currency. Every time the demand for cash peaks, banks find themselves under pressure to provide currency. Loans to deposit ratios increase as deposits decrease, making the same bank’s balance sheet look (much) worse at FY-end than at any point during the rest of the year. A peaking cash demand effectively mimics the effect of a run on the banking system. Temporarily, banks’ funding structure are weakened as reserves decrease and they rely on their portfolio of liquid securities to obtain short-term cash through repos with central banks or private institutions (or, at worst, calling in or temporarily not renewing loans)*. Central bankers are aware of this phenomenon and accommodate banks’ demand for extra reserves.

In a free banking system though, banks can simply convert deposits into privately-issued banknotes without having to struggle to find a cash provider. This ability allows free banks to economise on reserves and makes the circulating private currencies fully elastic. In a 100%-reserve banking system, cash balances at banks are effectively maintained in cash (i.e. not lent out). Therefore, any increase in the demand for cash should merely reduce those cash balances without any destabilising effects on banks’ funding structure (which aren’t really banks the way we know them anyway). However, if some of this demand for cash is to be funded through debt, this can end up being painful: in a sticky prices world, as available cash balances (i.e. loanable funds not yet lent out) temporarily fall while short-term demand for credit jump, interest rates could possibly reach punitive levels, with potentially negative economic consequences (i.e. fewer commercial transactions).

However, technological innovations can improve the efficiency of payment systems and lower the demand for cash in all those cases. Banks of course benefit from any payment technology that bypass cash withdrawals, alleviating pressure on their liquidity and hence on their profitability. Unfortunately not all countries seem willing to adopt new payment methods. The cases of France and the UK are striking. Despite similar economic structures and population, whereas the UK is adopting contactless and innovative payment solutions at a record pace, the French look much more reluctant to do so.

As the chart above did not include France, I downloaded the relevant data in order to compare the evolution and fluctuations of cash demand over the same period of time vs. the UK. Unsurprisingly, the demand for cash has grown much more in France than in the UK and fluctuations of the same magnitude have remained, despite the availability of internet and mobile transfers as well as contactless payments, which all have appeared over the last 15 years**. What this shows is that the demand for cash had a strong cultural component.

*Outright securities sale can also occur but if all banks engage in the sale of the same securities at the exact same time, prices crashes and losses are made in order to generate some cash.

** I have to admit that the cash demand growth for the UK looks surprisingly steady (apart from a small bump at the height of the crisis) with effectively no seasonal fluctuations.

Central banks don’t/do/don’t/do control interest rates

Ben Southwood and I agree on most things but a few topics. Whether central banks’ decisions affect interest rates is one of those, though I do think we have more common than we’re willing to admit. Here are the various reasons that convince me that central banks exert a relatively strong influence on most market rates.

On ASI’s blog, Ben wrote a piece about a 2013 research paper from Fama, who looked into interest rate time series to determine whether or not the Fed controlled interest rates. According to Ben’s own interpretation of the paper, the answer is ‘probably not’. Ironically, my take is completely different.

Throughout most of his paper, Fama’s results do indicate that the Fed exercises a relatively firm grip on all sorts of interest rates, as he admits it himself many times. For example, in his conclusion he writes:

A good way to test for Fed effects on open market interest rates is to examine the responses of rates to unexpected changes in the Fed’s target rate. Table 5 confirms that short-term rates (the one month commercial paper rate and three-month and six-month Treasury bill rates), respond to the unexpected part of changes in TF. Table 5 is the best evidence of Fed influence on rates, and event studies of this sort are center stage in the active Fed literature.

But I find Fama a little biased as he always tries to defend his original position that the Fed does not exert such a strong control:

But skeptics have a rejoinder. The response of short rates to unexpected changes in the Fed’s target rate might be a signaling effect. Rates adjust to unexpected changes in TF because the Fed is viewed as an informed agent that sets TF to line up with its forecasts of how market forces will shape open market rates.

Or also:

The Table 4 evidence that short-term interest rates forecast changes in the Fed funds target rate is not news (Hamilton and Jorda 2002). For those who believe in a powerful Fed, the driving force is TF, the concrete expression of Fed interest rate policy, and the forecast power of short rates simply says that rates adjust in advance to predictable changes in the Fed’s target rate. (See, for example, Taylor 2001.) The evidence is, however, also quite consistent with a passive Fed that changes TF in response to open market interest rates. There are, of course, scenarios in which both forces are at work, possibly to different extents at different times. The Fed may go passive and let the market dictate changes in TF when inflation and real activity are satisfactory, but turn active when it is dissatisfied with the path of inflation or real activity. This mixed story is also consistent with the evidence in Table 3 that the Fed funds rate moves toward both the open market commercial paper rate and the Fed’s target rate.

However Fama never explains why the Fed would simply passively change its base rate in response to private markets. This seems to defeat the purpose of having an active monetary policy.

In short, most of the evidences that Fama finds seem to demonstrate that the Fed indeed does control most interest rates to an extent (in particular short-term ones). But he does not seem to accept his own result and tries to come up with alternative explanations that are less than convincing, to say the least. He concludes by basically saying that…we cannot come to a conclusion.

But Fama’s paper suffers from a major flaw. Let’s break down a market interest rate here:

Market rate = RFR + Inflation Premium + Credit Risk Premium + Liquidity Premium

Fama’s dataset wrongly runs regressions between Fed’s base rate movements and observable market yields on some securities. The rate that the Fed influences is the risk free rate (RFR). But as seen above, market rates contain a number of premia that vary with economic conditions and the type of security/lending and on which the Fed has limited control.

For instance, when a crisis strikes, the credit risk premium is likely to jump. In response, the Fed is likely to cut its base rate, meaning the RFR declines. But the observable rate does not necessarily follow the Fed movement. It all depends on the amplitude of the variation in each variable of the equation above. Hence the correlation will only provide adequate results if the economic conditions are stable, with no expected change in inflation or credit risk. Does this imply that the Fed has no control over the interest rate? Surely not, as the RFR it defines is factored in all other rates. In the example above, the market rates ends up lower than it would have normally been if fully set by private markets.

David Beckworth had a couple of interesting charts on its blog, which attempted to strip out premia from the 10-year Treasury yield (it’s not fully accurate but better than nothing):

Now compare the 1990-2014 non-adjusted and adjusted 10-year Treasury yield with the evolution of the Fed base rate below:

The shapes of the adjusted 10-year yield and the Fed funds rate curves are remarkably similar, whereas this isn’t the case for the unadjusted yield*. Yet most of Fama’s argument about the Fed having a limited influence on long-term rates rests on his interpretation of the evolution of the spread between the Fed funds target rate and the unadjusted 10-year yield.

(the same reasoning applies to commercial paper spread, though the inflation premium is close to nil in such case)

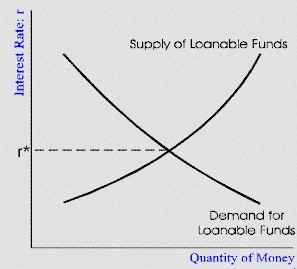

Second, I find it hard to understand Ben’s point that markets set rates, when central banks’ role is indeed to define monetary policies and, by definition, impact those market rates. If only markets set rates, then surely it is completely pointless to have central banks that attempt to control monetary policies through various tools, including the control on the quantity of high-powered money. In a simple loanable funds model (let’s leave aside the banking transmission mechanism), in which the interest rate is defined by the equilibrium point between supply and demand for loanable funds, it is quite obvious that a central bank injecting, or removing, base money from the system (that is, pushing the supply curve one way or another) will affect the equilibrium rate. Of course the central bank does not control the demand curve. But the fact that the bank does not have a total control over the interest rate does not imply that it has none and that its policies have no effect. What does count is that the resulting equilibrium rate differs from the outcome that free markets would have produced.

I am also trying to get my head around what I perceive as a contradiction here (I might be wrong). Market monetarists (of whom Ben seems to belong) believe that money has been ‘tight’ throughout the recession due to central banks’ misguided monetary policies. They seem to think that rates would have dropped much faster in a free market. This seems to demonstrate that market monetarist believe in the strong influence of central banks on many rates. But according to Ben, central banks do not have much influence on rates. Does he imply that free markets were responsible for the ‘tight’ policy that followed the crisis?

So far in this post we’ve only seen cases in which the central bank indirectly affects market rates. But some markets are linked to the central bank base rate from inception. For instance, in the UK, most mortgage rates (‘standard variable rates’) are explicitly and contractually defined as ‘BoE Base Rate + Margin’**. The margin rarely changes after the contract has been agreed. Any change in the BoE rate ends up being automatically reflected in the rate borrowers have to pay (that is, before banks are all forced to widen the contract margin because of the margin compression phenomenon, as I described in my previous exchange with Ben here and here). The only effect of banking competition is to lead to fluctuations of a few bp up or down on newly originated mortgages (i.e. one bank offers you BoE + 1.5% and another one BoE + 1.3%).

At the end of the day, I have the impression that a part of our disagreement is merely due to semantics. I don’t think anybody has declared that central banks fully control rates. This would be foolish. But they certainly exert a strong influence (at least) through the risk-free rate, and this reflects on all other rates across maturities and risk profiles.

*To be fair, it does look like some of the Fed’s decisions were anticipated by markets and reflected in Treasury yields just before the target rate was changed.

**In some other countries the link is looser, as the central bank rate is replaced by the local interbank lending rate (Libor, Euribor…).

Cachanosky on the productivity norm, Hayek’s rule and NGDP targeting

Nicolas Cachanosky and I should get married (intellectually, don’t get overexcited). Some time ago, I wrote about his very interesting paper attempting to start the integration of finance and Austrian capital theories. A couple of weeks ago, I discovered another of his papers, published a year ago, but which I had completely missed (coincidentally, Ben Southwood also discovered that paper at the exact same time).

Titled Hayek’s Rule, NGDP Targeting, and the Productivity Norm: Theory and Application, this paper is an excellent summary of the policies named above and the theories underpinning them. It includes both theoretical and practical challenges to some of those theories. Cachanosky’s paper reflects pretty much exactly my views and deserved to be quoted at length.

Cachanosky defines the productivity norm as “the idea that the price level should be allowed to adjust inversely to changes in productivity. […] In other words, money supply should react to changes in money demand, not to changes in production efficiency.” Referring to the equation of exchange, he adds that “because a change in productivity is not in itself a sign of monetary disequilibrium, an increase in money supply to offset a fall in P moves the money market outside equilibrium and puts into motion an unnecessary and costly process of readjustment”, which is what current central bank policies of price level targeting do. The productivity norm allows mild secular deflation by not reacting to positive ‘real’ shocks.

He goes on to illustrate in what ways Hayek’s rule and NGDP targeting resemble and differ from the productivity norm:

There are instances where the productivity norm illuminated economists that talked about monetary policy. Two important instances are Hayek during his debate with Keynes on the Great Depression and the market monetarists in the context of the Great Recession. Both, Hayek and market monetarism are concerned with a policy that would keep monetary equilibrium and therefore macroeconomic stability. Hayek’s Rule and NGDP Targeting are the denominations that describe Hayek’s and market monetarism position respectively. Taking the presence of a central bank as a given, Hayek argues that a neutral monetary policy is one that keeps constant nominal income (MV) stable. Sumner argues instead that

“NGDP level targeting (along 5 percent trend growth rate) in the United States prior to 2008 would similarly have helped reduce the severity of the Great Recession.”

Hayek’s Rule of constant nominal income can be understood in total values or as per factor of production. In the former, Hayek’s Rule is a notable case of the productivity norm in which the quantity of factors of production is assumed to be constant. In the latter case, Hayek’s rule becomes the productivity norm. However, for NGDP Targeting to be interpreted as an application that does not deviate from the productivity norm, it should be understood as a target of total NGDP, with an assumption of a 5% increase in the factors of production. In terms of per factor of production, however, NGDP Targeting implies a deviation of 5% from equilibrium in the money market.

Cachanosky then highlights his main criticisms of NGDP targeting as a form of nominal income control, that is the distinction between NGDP as an ‘emergent order’ and NGDP as a ‘designed outcome’. He says that targeting NGDP itself rather than considering NGDP as an outcome of the market can affect the allocation of resources within the NGDP: “the injection point of an increase in money supply defines, at least in the short-run, the effects on relative prices and, as such, the inefficient reallocation of factors of production.” In short, he is referring to the so-called Cantillon effect, in which Scott Sumner does not believe. I am still wondering whether or not this effect could be sterilized (in a closed economy) simply by growing the money supply through injections of equal sums of money directly into everyone’s bank accounts.

To Cachanosky (and Salter), “NGDP level matters, but its composition matters as well.” He believes that targeting an NGDP growth level by itself confuses causes and effects: “that a sound and healthy economy yields a stable NGDP does not mean that to produce a stable NGDP necessary yields a sound and healthy economy.” He points out that the housing bubble is a signal of capital misallocation despite the fact that NGDP growth was pretty stable in pre-crisis years.

I evidently fully agree with him, and my own RWA-based ABCT also points to lending misallocation that would also occur and trigger a crisis despite aggregate lending growth remaining stable or ‘on track’ (whatever that means). I should also add that it is unclear what level of NGDP growth the central bank should target. See the following chart. I can identify many different NGDP growth ‘trends’ since the 1940s, including at least two during the ‘great moderation’. Fluctuations in the trend rate of US NGDP growth can reach several percentage points. What happens if the ‘natural’ NGDP growth changes in the matter of months whereas the central bank continues to target the previous ‘natural’ growth rate? Market monetarists could argue that the differential would remain small, leading to only minor distortions. Possibly, but I am not fully convinced. I also have other objections to NGDP level targeting (related to banking and transmission mechanism), but this post isn’t the right one to elaborate on this (don’t forget that I view NGDP targeting as a better monetary policy than inflation targeting but a ‘less ideal’ alternative to free banking or the productivity norm).

Cachanosky also points out that NGDP targeting policies using total output (Py in the equation of exchange) and total transactions (PT) do not lead to the same result. According to him “the housing bubble before 2008 crisis is an exemplary symptom os this problem, where PT increases faster than Py.”

Cachanosky also points out that NGDP targeting policies using total output (Py in the equation of exchange) and total transactions (PT) do not lead to the same result. According to him “the housing bubble before 2008 crisis is an exemplary symptom os this problem, where PT increases faster than Py.”

Finally, he reminds us that a 100%-reserve banking system would suffer from an inelastic money supply that could not adequately accommodate changes in the demand for money, leading to monetary equilibrium issues.

I can’t reproduce the whole paper here, but it is full of very interesting (though quite technical) details and I strongly encourage you to take a look.

Why can’t economists understand margin compression?

Are basic accounting statements so difficult to interpret? According to Viennacapitalist, who commented on my previous post, it does seem so. At least for macroeconomists. Indeed, Werner seemed to imply that most economists did not know that deposits sat on the liability side of a bank’s balance sheet (he’s surely wrong), and I have many times pointed out the central bankers’ and policymakers’ misunderstanding of banking mechanics.

Three researchers from the BIS just confirmed the trend. In a new working paper called ‘Has the transmission of policy rates to lending rates been impaired by the Global Financial Crisis?’, they wonder, and try to find out, why spreads between central banks’ base rates and lending rates have jumped once base rates reached the zero-lower bound.

It’s a debate I’ve already had almost a year ago, when I tried to explain that, due to the margin compression effect (an accounting phenomenon), spreads would have to increase in order allow banks to generate sufficient earnings to report (at least) positive accounting net incomes (see here and here).

Those BIS researchers have come up with the same sort of dataset and charts I did over the past year, although they also looked at the US (but didn’t look as other European countries, unlike what I did in this post). This is what they got:

This looks very very similar to my own charts. Clearly, spreads jumped across the board: pre-crisis, they were around 1.5% in the US, 1.5% in the UK and 1.25/1.5% in Spain and Italy. In 2009/2010, with base rate dropping to the zero-lower bound, things changed completely: spreads were of 3% in the US, 2.25% in the UK, 2% in Spain and 1.5% in Italy. Rates had not dropped as much as base rates. Worse, spreads on average increased afterwards: by 2013, spreads were around 2.5% in all countries.

This looks very very similar to my own charts. Clearly, spreads jumped across the board: pre-crisis, they were around 1.5% in the US, 1.5% in the UK and 1.25/1.5% in Spain and Italy. In 2009/2010, with base rate dropping to the zero-lower bound, things changed completely: spreads were of 3% in the US, 2.25% in the UK, 2% in Spain and 1.5% in Italy. Rates had not dropped as much as base rates. Worse, spreads on average increased afterwards: by 2013, spreads were around 2.5% in all countries.

The BIS researchers tried to understand why. Unfortunately, they focused on the wrong factors. They built a model that concluded that the “less pass-through seems to be related in part to higher premium for risk required by banks and by worsening of their financial conditions as well.” They are probably right that some of these factors did play a role. But they cannot explain why the spread remains so elevated even in economies that have experienced strong recoveries such as the US or, more recently the UK.

But their study also has a number of other problems. First, they used new lending data only. It is extremely tricky to extract credit risk information from new lending rate figures. Why? Because new lending rates only show credit actually extended. Many borrowers cannot access credit altogether or simply refuse to do so at high rates. Consequently, the figures could well only reflect borrowers that have relatively good credit risk in the first place as banks try to eliminate credit risk from their portfolio. Second, they never ever discuss operating costs and margin compression, as if banks could simply lower interest income to close to 0 and get away with it.

But for this, they should have looked at two things: deposit rates and banks’ back books (i.e. legacy lending). Not new lending only. When the margin between deposit rates and lending rates on back books fall below banks’ operating costs, banks have to offset that decline by increasing spreads. This is why I suggested that the actual lowering base rates ceased to be effective from around 1.5 to 2% downward as a means of reducing household and companies’ borrowing rates.

Problem is, very few researchers and policymakers seem to get it. Patrick Honohan, of the Irish Central Bank, and Benoit Coeuré, of the ECB, do seem to understand what the issue is. Bankers and consultants have for a while (see Deloitte at the end of this post). Some economic commentators assert that it is hard to figure out why bankers keep complaining about low rates. This dichotomy between theorists and practitioners is leading to misguided, and potentially harmful, policies.

But let me ask a simple question. How hard is it to understand bank accounting really?

Myths are slowly being debunked. Slowly…

A few institutions have recently raised voices to try to debunk some of the banking legends that had appeared and became conventional knowledge as a result of the crisis. Here’s an overview.

S&P, the rating agency, just published a note declaring that, surprise surprise, the UK’s ring fencing plans could have clear adverse consequences. Those include: possible downgrade to ‘junk’ status and lower ‘stability’ of the non-ring fenced entities, costs for customers could rise, credit supply could be squeezed, and, what I view as the most important problem of all, ring fencing rules “will undoubtedly further constrain fungibility.” According to the S&P analyst, as reported by Reuters:

“The sharing of resources (and brand, expertise, and economies of scale) means we view most banking groups as being more than the sum of their parts,” the report said.

It said disrupting these benefits could lead S&P to have a weaker view of the group as a whole and to lower its credit ratings on some parts of the banks.

S&P said the complexity of separating functions “represents a significant operational challenge” for banks at a time of multiple other regulations.

I cannot agree more. I have already written four long pieces explaining why intragroup liquidity and capital transfers were key in maintaining a banking group safe. Ring fencing does the exact opposite, putting those liquidity buffers and capital bases in silos from which they cannot be used elsewhere, potentially endangering the whole bank.

The BoE just reported that households could actually cope with raising interest rates. One of the Bank’s justification for not raising rates was that it would push many households towards default, so it is now kind of contradicting itself. And anyway, as I have described previously, lowering rates ceased to translate into lower borrowing rates due to margin compression. Patrick Honohan, Governor of the central bank of Ireland, reported that the exact same phenomenon occurred in Ireland:

Because of the impact on trackers, though, the lower ECB interest rates have not directly improved the banks’ profitability, because the average and marginal cost of bank funds does not fall as much. The banks’ drive to restore their profitability, combined with the lack of sufficient new competition, has meant that, far from lowering their standard variable rates over the past three years as ECB rates have fallen, they have (as is well known) actually increased the standard variable rates somewhat. […] These rates indicate that standard variable rate borrowers are still paying less than they were before the crisis, but not by much. A widening of mortgage interest rate spreads over policy rates also occurred in the UK and in many euro area countries after the crisis, but spreads have begun to narrow in the UK and elsewhere. Until very recently bank competition has been too weak in Ireland to result in any substantial inroads on rates.

This chart exactly looks like what happened in the UK. Spread over BoE/ECB rates have increased, and increasing rates could actually translate into the same level of mortgage rates. This is because, as margin compression starts disappearing, competition can start driving down the spread over BoE/ECB. Households may have to remortgage to benefit from the same rates though.

In Germany, regulators said that the ECB’s negative deposit rates could incite more risk-taking and declared that:

Excess liquidity could even threaten the banking system if it is put to poor use

Regulators vs. ECB. This is getting interesting.

In FT Alphaville, David Keohane reports a few charts from Morgan Stanley. One of them clearly shows the Chinese Central Bank’s use of reserve requirements to manage lending growth. I’m sure my MMT and ‘endogenous money’ friends will appreciate.

Liquidity and collateral are two sides of the same coin

I recently wrote a piece listing all the current regulatory constraints that arise from banking regulation and which weigh on liquidity. Unfortunately, there is more. As Singh explained in this FT article (as well as in many of his research papers), monetary policy, and in particular quantitative easing, can have serious repercussions on market liquidity:

From a financial lubrication angle, markets need both good collateral and money for smooth market functioning and, ultimately, financial stability. Having a ready supply of good collateral like US Treasuries or German Bunds also helps in reallocating the not-so-good collateral.

QE that isolates good collateral from the wider market reduces financial lubrication. Its substitute, money that shows up as excess reserves, is basically contained in a closed circuit system built to avoid inflation by introducing “interest on excess reserves”.

Indeed, the combination of QE and Basel rules effectively drives so-called ‘high-quality assets’ out of the market by ‘siloing’ them in various places (central banks’ and banks’ balance sheets, clearinhouses’ margins…). This is what many have dubbed ‘scarcity of good collateral’. (I personally think that Singh is wrong to call all highly rated and liquid assets ‘collateral’. When the Fed buys Treasuries, it doesn’t purchase collateral. It purchases an asset that could potentially be used as collateral. Yet, Singh just uses the word ‘collateral’ in every single circumstance. Semantics I know, but the distinction is important I believe)

The potential solution? Governments could issue more debt, meaning more indebtedness. Not certain this is a good one, especially as increased indebtedness would at some point cause the quality of the asset to decline… (reducing the maturity of existing issues could potentially ease liquidity constraints, but the effect is going to be limited)

JP Koning once declared that he didn’t understand how such ‘collateral shortage’ could even happen. Any asset could serve as collateral, with bigger haircut applied to riskier asset to offset potential market value fluctuations. He is fundamentally right. In a free market, there is no real reason why such shortage should ever appear.

Unfortunately, we do not live in a fully free market, and financial regulations institutionalised the use of certain classes of assets as collateral for certain transactions and increased the required associated haircut (for example, see here for OTC derivatives, see here for shadow banking transactions). Many transactions are also pushed towards central clearing at clearinghouses, which often require posting more (standardised) collateral, hence reducing supply by placing high-quality assets in a silo.

Cash, which can also be used as collateral, is itself siloed at the central bank level because of interest on excess reserves*.

As a result of those new rules, the latest ISDA survey tells us that:

Estimated total collateral in circulation related to non-cleared OTC derivatives has decreased 14%, from $3.7 trillion at the end of 2012 to $3.2 trillion at the end of 2013 as a consequence of mandatory clearing.

Regulations have created a lot of ‘know unknowns’. How the entanglement of all those rules will unravel in a crisis will be ‘interesting’ to follow.

* I know that those reserves don’t usually leave the central bank (unless withdrawn by depositors). But when banks expand their loan book, reserves that were previously in excess suddenly become ‘required’ (unless there is no reserve requirement of course).

The rather curious and awkward alliance between statists and libertarians against free banking

Free banking has a very bad reputation within mainstream economics. As free banking scholars such as George Selgin, Larry White, Kevin Dowd or Steve Horwitz have been demonstrating over the past 30 years, this is mostly due to a misunderstanding of history. The track record of the systems that were as close as possible to free banking is crystal clear however: free banking episodes were more stable than any alternative banking frameworks.

However, this doesn’t seem to please many, from both sides of the political spectrum. Izabella Kaminska, a long-time libertarian critic from FT Alphaville, wrote a piece on the Alphaville blog partly criticizing non-central banking-based banking systems. In two separate replies (here and here), George Selgin highlighted all the self-serving ‘inaccuracies’ of her post (this is a euphemism). He also wrote a rebuttal in a follow-up post. Izabella skipped the interesting bits, accused Selgin of ad hominem, and wrote in turn another unsourced name-calling post on her own private blog. So much for the academic debate.

Perhaps more surprisingly, David Howden just posted a curious article on the Mises Institute website, which described the Fed as arising from “fractional-reserve free banks”. I say surprisingly, because Howden and the Mises Institute are at the other end of the political spectrum: libertarians, and often anarcho-capitalists. Nevertheless, he seemed to agree with Izabella Kaminska to an extent.

Unfortunately, Howden and Kaminska make the same mistake: they misread history, and/or focus far too much on US banking history. First, Howden claims that:

The year 1857 is a somewhat strange one for these clearinghouse certificates to make their first appearance. It was, after all, a full twenty years into America’s experiment with fractional-reserve free banking. This banking system was able to function stably, especially compared to more regulated periods or central banking regimes. However, the dislocation between deposit and lending activities set in motion a credit-fuelled boom that culminated in the Panic of 1857.

This could not be more inaccurate. The so-called ‘US free banking era’ had nothing much to do with free banking. And the credit boom and crises that follow were unrelated to either free banking or fractional reserves (see here for details, as well as below). I’d like Howden to explain why other fractional reserve free banking systems did not experience such recurring crises…

I have been left bewildered by Howden’s claim that privately-created clearinghouses were ‘illegal’ entities involved in ‘illegal’ activities (i.e. issuing clearinghouse certificates to get bank runs under control). Not only does this ironically sound like contradicting laissez-faire principles, but his whole argument rests on a lacking understanding of 19th century US banking.

What Howden got wrong is that, if American banks had such recurring liquidity issues before the creation of the Fed, it wasn’t due to their fractional reserve nature, but to the rule requiring them to back their note issues with government debt, thereby limiting the elasticity of those issues and the ability of banks to respond to fluctuations in the demand for money. Laws preventing cross-state branching also weakened banks as their ability to diversify was inherently limited. Banks viewed local clearinghouses as a way to make the system more resilient. It was a free-market answer to a state-created problem. This does not mean that the system was perfect of course. But Howden the libertarian blames a free-market solution here, and completely ignores the laws that originally created the problem.

Moreover, clearinghouses weren’t only a characteristic of the 19th century US banking system. They were present in several major free banking systems throughout history and set up by private parties (Scotland being a prime example). Their original goal wasn’t to create ‘illegal money claims’, but to help settle large volume of interbank transactions and economise on reserves: they were a necessary part of a well-functioning privately-owned free banking system. US clearinghouse certificates were merely a private solution to tame state-created liquidity crises. Those solutions were not perfect, but Howden is guilty of shooting the messenger here.

Clearinghouse-equivalents still exist today: the German savings and cooperative banks, as well as the Austrian Raiffeisen operate under the same sort of model, in which multiple tiny institutions park their reserves at their local central bank/clearinghouse. Finally, it is necessary to point out that clearinghouse would also surely exist in a full reserve banking system and would have the same basic goal: settle interbank payments.

Why a libertarian such as Howden would be against this natural laissez-faire process is beyond me. My guess is that at the end of the day, it all goes down to the fractional/full reserve banking debate within the libertarian space. Howden is trying at all costs to justify his views that full reserve banking would be more stable. But this time, such rhetoric is counter-productive and only demonstrates Howden’s ignorance of the issue (at least as described in this article). Using the fractional reserve argument to explain the 19th century US crises is self-serving and wholly inappropriate. Blaming a free-market reaction (i.e. the clearinghouse system) to such crises for the creation of the Fed completely misses the point. By doing so, and cherry-picking facts, Howden helps Kaminska’s arguments (despite fundamentally disagreeing with her) and shoots himself in the foot.

Update: I mistakenly thought that Peter Klein had written the article as his profile appeared on it. I should have paid more attention, but David Howden was the author. I have updated the post and apologised to Peter.

Update 2: I only just found out that David Glasner and Scott Sumner also wrote two good posts on free banking and Iza Kaminska/Selgin, followed by very interesting comments (here and here).

Photo: Marvel

Chinese regulation, the European way

Some European banking regulators are currently considering the implementation of a sovereign bond exposure cap of 25% of capital to any one sovereign. Their goal is to break the link between sovereigns and banks. I think they don’t really know what they are doing.

European sovereign bond markets are distorted in all possible ways:

- The Basel banking regulation framework has been awarding 0% risk-weight to OECD sovereign debt since the 1980s, meaning purchasing such asset does not require any capital. Recent rules haven’t changed anything to this.

- On the contrary, Basel 3 introduces a liquidity ratio (LCR) basically requiring banks to hold even more sovereign debt on their balance sheet (as part of so-called highly-liquid ‘Level 1 assets’).

- Meanwhile, the ECB, as well as the BoE, have been trying to revive business lending (which suffers from the opposite problem: high risk-weights) by launching cheap funding programmes (LTRO, TLTRO, FLS…). Banks drawn on those facilities to invest in… more 0% weighted sovereign debt, and earn capital-free interest income. We call this the ‘carry trade’.

- Furthermore, investors (including banks) have started seeing peripheral European debt as virtually risk-free thanks to the ECB pledge that it would do whatever it takes to prevent defaults in those countries.

There you are: had European regulators wanted to reinforce the link between sovereigns and banks, they wouldn’t have been more successful. Their usual talk of breaking the link between banks and sovereigns has been completely undermined by their own actions.

The easy solution would have been to scrap risk-weights (or at least increase them on sovereign bonds). But this was too simple, so European policymakers decided to go the Chinese way: never scrap a bad rule; design a new one to fix it; and another one to fix the previous one that fixed the original one.

The new 25% cap would only add further distortion: while Basel’s risk-weights do not differentiate between Portuguese and German bonds, the 25% rule doesn’t either. But, you would retort, this isn’t the point: the point is to limit the exposure to any single sovereign. I agree that diversification is usually a good thing. But 1. lack of diversification has been encouraged by policymakers’ own decisions, and 2. forcing banks to diversify away from the safest sovereigns just for the sake of diversifying may well put many banks’ balance sheet more at risk.

Finally, Fitch estimates at EUR1.1Trn the amount of debt that would need to be offloaded. This is very likely to affect markets and could result in banks taking serious one-off hits on their available-for-sale and marked-to-market bond portfolios, resulting in weaker capital positions. This could also raise overall interest rates, in particular in riskier (and weaker) European countries. Fitch believes banks could rebalance into Level 1-elligible covered bonds. Maybe, but this would only introduce even more distortions in the market by artificially raising the demand for their underlying assets, and this would encumber banks’ balance sheets even further, creating other sorts of risks.

Why pick a simple solution when you can do it the Chinese way?

Photo: picture-alliance / dpa through www.dw.de

How short is the economics profession’s memory?

Although prices were not perfectly steady, it is true, they were relatively stable for a period of time longer than any prior period involving comparable conditions. Yet depression ensued, in the face of what the advocates of the older form of monetary theory of the business cycle regarded as the sine qua non of freedom from depression.

It follows particularly from the point of view of the monetary theory of the trade cycle, that it is by no means justifiable to expect the total disappearance of cyclical fluctuations to accompany a stable price-level.

Where do these quotes come from? From any recent critic of inflation targeting, such as David Beckworth, referring to our latest crisis (which followed around two decades of inflation targeting by central banks)?

No. The first one is a 1937 quote from Chester Arthur Phillips, in his Banking and the Business Cycle. The second one is from F.A. Hayek, in his 1933 Monetary Theory and the Trade Cycle. I am sure it is possible to find tons of similar quotes from the pre-WW2 era.

In his book, Phillips has a sub-chapter called ‘Policy of Stabilization of Price Level Tends Towards its Own Collapse’, which is worth quoting here:

The endeavor has been to show that stabilization of the wholesale price level, or of any one price index, is not a proper objective of banking policy of credit control, because aberrations continue to occur in the case of particular types of prices when any one index is sought to be stabilized. […]

Stability of the price level is no adequate safeguard against depression, it is contended, because any policy aimed at stabilizing a single index is bound to set up countervailing influences elsewhere in the economic system. Although the policy of stabilization may appear to be successful for a time, eventually it will break down, because there is no way of insuring that the agencies of control will be able to make their influence at precisely those “points” of strategic importance. As long as economic progress is maintained, resulting in increasing productivity and an expanding total output, there will be an ever-present force working for lower prices. Any amount of credit expansion which will offset that force will find outlets unevenly in sundry compartments of the economic structure; the new credit will have an effect upon the market rate of interest, upon the prices of capital goods, upon real estate, upon security prices, upon wages, or upon all of these, as happened during the late boom. A policy which seeks to direct credit influences at any single index, whether it be of prices, either wholesale or retail, or production, or incomes, in the interest of stabilization, will result in unexpected and unforeseen repercussions which may be expected to prove disastrous in the long run.

What about the following one?

During recent years a number of pseudo-economists have indulged in much glibness about the passing of the “economy of scarcity” and the arrival of the “economy of abundance.” Sophistry of this sort has claimed the public ear far too long; it is high time that the speciousness of such fantastic views be clearly and definitely exposed.

An angry economist about some FT Alphaville blogger? No. Phillips again, in the same 1937 book.

George Selgin posted an old Keynes’ quote two days ago, which may be relevant for some of today’s theorists. Backhouse and Laidler also published a very good paper describing everything that has been ‘lost’ with the IS-LM framework following the post-war Keynesian revolution.

It is slightly scary to see that economics tends to easily forget more ‘ancient’ theories in favour of recent and trendy ones. The same is true regarding banking history: listening to most policymakers makes it clear that past experiences and knowledge have mostly been lost. With such short memories, it is unsurprising that crises occur.

PS: On a side note, George Soros completely misunderstands Hayek. I cannot even believe he could write this article. No, Hayek wasn’t a member of the Chicago School. No, Hayek never believed in the efficient market hypothesis (Hayek didn’t believe in rational expectations). No, Hayek didn’t believe in equilibrium economics but in dynamic frameworks that completely include uncertainty and perpetually fluctuating conditions and agents’ expectations, as well as entrepreneurial experiments (including failures, which are indeed healthy). So… basically the exact opposite of what Soros claims Hayek believed in.

Recent Comments