When regulators become defiant of… regulation

After years of regulatory boom, some politicians, and regulators, seem to be – slowly – waking up. I have already described how UK’s Vince Cable seemed to now partially understand that regulation doesn’t make it easy for banks to lend to small and medium-sized businesses, and how Andrew Bailey, from the Bank of England’s Prudential Regulation Authority, complained about the lack of regulatory coordination across country:

I am trying to build capital in firms, and it is draining out down the other side.

Well, Bailey is at it again. Reuters summarized Bailey’s latest speech as:

The over-zealous application of anti-money laundering rules is hampering British banks abroad and cutting off poorer countries from global financial markets, a top Bank of England regulator said on Tuesday.

He said:

We have no sympathy with money laundering, but we are facing a frankly serious international coordination problem. […] We are seeing clear evidence … of parts of the world and activities that are being cut off from the mainstream banking system. […] It cannot be a good thing for the development of the world economy and the support of emerging countries … that we get into that situation. […] I have to spend a large part of my time dealing with the issues that come up in this field … because some of the consequences of the actions taken are potentially existential.

I find it quite ironic to see a regulator disapproving ‘over-zealous’ regulation. Another regulator, Jon Cunliffe, Deputy Governor of the Bank of England, declared that:

Liquidity and market making does seem to have been reduced. […] We’re not sure how much of it is the result of regulatory action, and how much of it is do with the change in business model for the institutions.

While he believes that some of the pre-crisis liquidity was ‘illusory’, his statement clearly indicates that he knows that regulation might not have had only positive effects. (Four days after I spoke about regulatory effects on market liquidity, Fitch published a press release arguing the exact same thing. I still have to write that post…)

Unfortunately, not all regulators are waking up. Reuters reported that David Rule, also from the BoE, said that:

banks had responded to regulatory incentives and increased their focus on the real economy, rather than financial market trading for its own sake.

Really? With business lending stuck at the bottom and mortgage lending (a very productive form a lending to the real economy) booming again? I see.

Andreas Dombret, of the Bundesbank, recently declared in a relatively reasonable speech* that:

But are we really overregulating? If we look at the benefits to society of a stable banking system and the social costs of a banking crisis, I believe the costs of regulation are justifiable.

Clearly he and Bailey should have a proper conversation…

Others, like Andrea Enria, Chairman of the European Banking Authority, which recently ran the European stress tests, warned that

The story is not over, even for the banks who passed it

I am unsure what the goal of that sort of threatening comment is, but I don’t see how this can reintroduce confidence in the European banking system. It certainly will push bankers to consolidate their balance sheet further rather than to start lending more. Let’s not forget that the EBA and ECB tests have the power to create a panic and destabilise markets when nothing would have occurred. Too soft and nobody would trust the tests. Too tough and a panic might set in (imagine the headlines: “Half of European banks at risk of failure!”). Another risk is that investors and commentators stop relying on their own judgment and analysis and start relying too much on regulators’ assessment. This would be extremely dangerous. Yet this already happens to an extent. Perhaps, as more and more regulators start waking up to the potentially harmful side effects of regulatory measures, they will back off and let the market play its role?

* While the speech is overall reasonable, Dombret still comes up with usual myths such as

Yet a leverage ratio would also create the wrong incentives. If banks had to hold the same percentage of capital against all assets, any institution wanting to maximise its profits would probably invest in high-risk assets, as they produce particularly high returns.

This is not correct.

Funnily, he also kind of admitted that regulators did not always understand how banking works, as I’ve been arguing a few times recently:

Do supervisors have to be the “better bankers”? No, absolutely not. Business decisions must be left to those being paid to make them. However, supervisors have to know – and understand – how banking works. Against this background, I personally would very much welcome an increase in the migration of staff between the banking industry and the supervisory agencies.

Still, many regulators influence business decisions…

Kupiec on central banking/planning

In the WSJ a couple of days ago, Paul Kupiec wrote an article that looks so similar to my blog that I had to quote it here.

Macroprudential regulation, macro-pru for short, is the newest regulatory fad. It refers to policies that raise and lower regulatory requirements for financial institutions in an attempt to control their lending to prevent financial bubbles. […]

There is also the very real risk that macroprudential regulators will misjudge the market. Banks must cover their costs to stay in business, and in the end bank customers will pay the cost banks incur to comply with regulatory adjustments, regardless of their merit. By the way, when was the last time regulators correctly saw a coming crisis?

He concludes with:

With Mr. Fischer now heading the Fed’s new financial stability committee, might we soon see regulations requiring product-specific minimum interest rates? Or maybe rules that single out new loan products and set maximum loan maturities and debt-to-income limits to stop banks from lending on activities the Fed decides are too “risky”? None of these worries is an unimaginable stretch.

Since the 2008 financial crisis, U.S. bank regulators have put in place new supervisory rules that limit banks’ ability to make specific types of loans in the so-called leverage-lending market—loans to lower-rated corporations—and for home mortgages. Since there is no scientific means to definitively identify bubbles before they break, the list of specific lending activities that could be construed as “potentially systemic” is only limited by the imagination of financial regulators.

Few if any centrally planned economies have provided their citizens with a standard of living equal to the standard achieved in market economies. Unfortunately the financial crisis has shaken belief in the benefits of allowing markets to work. Instead we seem to have adopted a blind faith in the risk-management and credit-allocation skills of a few central bank officials.

Government regulators are no better than private investors at predicting which individual investments are justified and which are folly. The cost of macroprudential regulation in the name of financial stability is almost certainly even slower economic growth than the anemic recovery has so far yielded.

This is very good, and I can’t agree more.

He points to his own research on macro-prudential policies. In a paper published in June 2014, Kupiec, Lee and Rosenfeld declare that

Compared to the magnitude of loan growth effects attributable to [increase in supervisory scrutiny or losses on loan/securities], the strength of macroprudential capital and liquidity effects are weak. This data suggest that traditional monetary policy (lowering banks’ cost of funding) is likely to be a much more potent tool for stimulating bank loan growth following widespread bank losses than modifying regulatory capital or liquidity requirements.

(note: they also say that the opposite logic applies)

While it doesn’t mean that they are wrong, I am not fully convinced by their arguments, especially given the dataset they base their analysis on (an economic and credit boom period, with less than tight monetary policy and many variables that could have been distorted as a result). In another paper, Aiyar, Calomiris and Wieladek point to the fact that macro-prudential policy can be effective at reducing banks’ lending, but that alternative sources of credit (i.e. shadow banking) grow as a result (they say that macro-prudential policies ‘leak’).

What is clear is that the effects of macro-prudential policies are unclear. What is also clear is that, whatever the effects of those policies, none are necessarily desirable. If macropru is indeed effective, then the resulting distorted capital allocation may be harmful. If macropru isn’t effective, then it may lead central bankers to (wrongly) believe they can maintain interest rates below/above their natural level while controlling the collateral damages this creates. In both cases the economy ends up suffering.

ECB policies: from flop to flop… to flop?

Even central bankers seem to be acknowledging that their measures aren’t necessarily effective…

ECB’s Benoit Coeuré made some interesting comments on negative deposit rates in a speech early September. Surprisingly, he and I agree on several points he makes on the mechanics of negative rates (he and I usually have opposite views). Which is odd. Given the very cautious tone of his speech, why is he even supporting ECB policies?

Here is Coeuré:

Will the transmission of lower short-term rates to a lower cost of credit for the real economy be as smooth? While bank lending rates have come down in the past in line with lower policy rates, there is a limit to how cheap bank lending can be. The mark-up that banks add to the cost of obtaining funding from the central bank compensates for credit risk, term premia and the cost of originating, screening and monitoring loans. The need for such compensation does not necessarily fall when policy rates are lowered. If anything, a central bank lowers rates when the economy needs stimulus, which is precisely when it is difficult for banks to find good loan making opportunities. It remains to be seen whether and to what extent the recent monetary policy accommodation translates into cheaper bank lending.

This is a point I’ve made many times when referring to margin compression: banks are limited in their ability to lower the interest rate they charge customers as, absent any other revenue sources, their net interest income necessarily need to cover their operating costs (at least; as in reality it needs to be higher to cover their cost of capital in the long run). Banks’ only solution to lower rates is to charge customers more for complimentary products (it has been reported that this is in effect what has been happening in the US recently).

Negative rates are similar to a tax on excess reserves, which evidently doesn’t make it easier for a bank to improve its profitability, and as a result its internal capital generation. And Coeuré agrees:

A negative deposit rate can, however, also have adverse consequences. For a start, it imposes a cost on banks with excess reserves and could therefore reduce their profitability. Note, however, that this applies to any reduction of the deposit rate and not just to those that make the rate negative. For sure, lower bank profitability could hamper economic recovery, especially in times when banks have to deleverage owning to stricter regulation and enhanced market scrutiny. But whether bank profitability really falls when policy rates are lowered depends more generally on the slope of the yield curve (as banks’ funding costs may also fall), on banks’ investment policies (as there is scope for them to diversify their cash investment both along the curve and across the credit universe) and on factors driving non-interest income.

Coeuré clearly understands the issue: central banks are making it difficult for banks to grow their capital base, while regulators (often the same central bankers) are asking banks to improve their capitalisation as fast as possible. Still, he supports the policy…

Other regulators are aware of the problem, and not all are happy about it… Andrew Bailey, from the Bank of England’s PRA, said last week that regulatory agencies should co-ordinate:

I am trying to build capital in firms, and it is draining out down the other side.

This says it all.

Meanwhile, and as I expected, the ECB’s TLTRO is unlikely to have much effect on the Eurozone economy… Banks only took up EUR83m of TLTRO money, much below what the central bank expected. It is also likely that a large share of this take up will only be used for temporary liquidity purposes, or even for temporary profitability boosting effects (through the carry trade, by purchasing capital requirement-free sovereign debt), until banks have to pay it off after two years (as required by the ECB, and without penalty, if they don’t lend the money to businesses).

Fitch also commented negatively on TLTRO, with an unsurprising title: “TLTROs Unlikely to Kick-Start Lending in Southern Europe”.

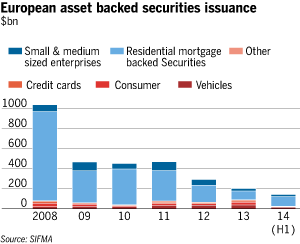

Finally, the ECB also announced its intention to purchase asset-backed securities (which effectively represents a version of QE). While we don’t know the details yet, the scheme has fundamentally a higher probability to have an effect on banks’ behaviour. There is a catch though: ABS issuance volume has been more than subdued in Europe since the crisis struck (see chart below, from the FT). The ECB might struggle to buy the quantity of assets it wishes. Perhaps this is why central bankers started to encourage European banks to issue such structured products, just a few years after blaming banks for using such products.

Oh, actually, there is another catch. ABSs are usually designed in tranches. Equity and mezzanine tranches absorb losses first and are more lowly rated than senior tranches, which usually benefit from a high rating. Consequently, equity and mezzanine tranches are capital intensive (their regulatory risk-weight is higher), whereas senior tranches aren’t. To help banks consolidate their regulatory capital ratios and prevent them from deleveraging, the ECB needs to buy the riskier tranches. But political constraints may prevent it to do so… Will this new ECB scheme also fail? As long as central bankers (and politicians) continue to push for schemes and policies without properly understanding their effects on banks’ internal ‘mechanics’, they will be doomed to fail.

PS: I have been busy recently so few updates. I have a number of posts in the pipeline… I just need to find the time to write them!

Central banks: an expanding regulatory toolkit

Following my latest post on central banks as the new central planners, a very recent New York Fed Staff Report by Adrian, Covitz and Liang demonstrates the extent of possible central banks’/regulators’ involvement in financial markets, and therefore in what ways they can control, or attempt to control, the allocation of resources within the financial system. Here is a summary of various classes of tools (most of them discretionary) that monetary and financial authorities can play with:

– Monetary policy: the authors classify monetary policy as a “broader tool” that “would affect the rates for all financial institutions”. Indeed, central banks not only set the short-term refinancing rates and reserve requirements and run open market operations, but now also have in place interest rates paid on excess reserves, fixed-rate full allotment reverse repos, as well as various temporary long-term lending facilities such as the BoE’s Funding for Lending Scheme or the ECB’s LTRO and TLTRO, and temporary liquidity facilities such as the ABCP MMF liquidity facility, and can decide what collateral to accept and what securities to purchase, way beyond the traditional Treasury-based OMO.

– Asset markets: central banks can regulate what they view as ‘imbalances’ in the valuation of some asset markets by tightening underwriting standards as well as “through regulated banks and broker-dealers by tightening standards on implicit leverage through securitization or other risk transformations, or by limiting the debt they provide to investors in either unsecured or secured funding markets, if the asset prices are being fuelled by leverage.” In the case of real estate markets and household burdens, central bankers can impose LTV restrictions* and other similar macro-prudential policies.

– Banking policies: central banks have under their control all traditional micro-prudential regulatory tools. In addition, Basel 3 provide them with some flexibility in setting macro-prudential regulatory tools that apply specifically to the banking system, such as counter-cyclical capital requirements (capital conservation buffer, equity systemic surcharge…). Other ad-hoc tools include: sectoral capital requirements (higher/lower capital charges/RWAs for specific asset classes), dynamic provisioning, stress tests…

– Shadow banking policies: harder to regulate, central banks could “address pro-cyclical incentives in secured funding markets, such as repo and sec lending, […] propose minimum standards for haircut practices, to limit the extent to which haircuts would be reduced in benign markets. Other elements of this proposal include consideration of the use of central clearing for sec lending and repo markets, limiting liquidity risks associated with cash collateral reinvestment, addressing risks associated with re-hypothecation of client assets, strengthening collateral valuation and management practices, and improving report, disclosures, and transparency.” Other direct tools include “the explicit regulation of margins and haircuts for macroprudential purposes.”

– Nonfinancial sector: “Tools to address emerging imbalances in asset valuations likely would also address building vulnerabilities in the nonfinancial sector. For example, increasing* [sic] LTVs or DTIs on mortgages, which could reduce a leverage-induced rise in prices, could also limit an increase in exposures of households and businesses to a collapse in prices, thereby bolstering their resilience.”

Given the increased scope of central banks’ operations, it is clear that market prices can be manipulated and distorted in all sort of ways. To be fair however, not all those powers are currently concentrated in the central bankers’ hands. In many countries, there are still a few different institutions that perform those tasks. Nevertheless, the trend is clear: most of those powers are increasingly taken over by and aggregated at central banks.

While this new paper advocates the use of such tools, it admits that their effectiveness and effects on the financial system and the broader economy remains untested and uncertain:

New government backstops to address the risks arising from shadow banking, of course, can be costly. First, an expansion along these lines would require a new regulatory structure to prevent moral hazard, which can be expensive and difficult to implement effectively. Second, an expansion of regulations does not reduce the incentives for regulatory arbitrage, but just pushes it beyond the beyond the existing perimeter. Third, there is a limited understanding of the impact that such a fundamental change would have on the efficiency and dynamism of the financial system.

In a subsequent guest post, Justin Merrill will investigate macro-prudential policy tools more in depth.

* The paper mistakenly describes those potential measures as “increasing” LTV ratios to mitigate house price and household indebtedness increases. I believe this is a typo, even though the same claim reappears several times throughout the paper (if not a typo then the authors have no clue how LTVs work…).

Hummel vs. Haldane: the central bank as central planner

Recent speeches and articles from most central bankers are increasingly leaving a bad aftertaste. Take this latest article by Andrew Haldane, Executive Director at the BoE, published in Central Banking. Haldane describes (not entirely accurately…) the history and evolution of central banking since the 19th century and discusses two possible paths for the next 25 years.

His first scenario is that central banks and regulation will step backward and get back to their former, ‘business as usual’, stance, focusing on targeting inflation and leaving most of the capital allocation work to financial markets. He views this scenario as unlikely. He believes that the central banks will more tightly regulate and intervene in all types of asset markets (my emphasis):

In this world, it would be very difficult for monetary, regulatory and operational policy to beat an orderly retreat. It is likely that regulatory policy would need to be in a constant state of alert for risks emerging in the financial shadows, which could trip up regulators and the financial system. In other words, regulatory fine-tuning could become the rule, not the exception.

In this world, macro-prudential policy to lean against the financial cycle could become more, not less, important over time. With more risk residing on non-bank balance sheets that are marked-to-market, it is possible that cycles in financial assets would be amplified, not dampened, relative to the old world. Their transmission to the wider economy may also be more potent and frequent. The demands on macro-prudential policy, to stabilise these financial fluctuations and hence the macro-economy, could thereby grow.

In this world, central banks’ operational policies would be likely to remain expansive. Non-bank counterparties would grow in importance, not shrink. So too, potentially, would more exotic forms of collateral taken in central banks’ operations. Market-making, in a wider class of financial instruments, could become a more standard part of the central bank toolkit, to mitigate the effects of temporary market illiquidity droughts in the non-bank sector.

In this world, central banks’ words and actions would be unlikely to diminish in importance. Their role in shaping the fortunes of financial markets and financial firms more likely would rise. Central banks’ every word would remain forensically scrutinised. And there would be an accompanying demand for ever-greater amounts of central bank transparency. Central banks would rarely be far from the front pages.

He acknowledged that central banks’ actions have already considerably influenced (distorted?…) financial markets over the past few years, though he views it as a relatively good thing (my emphasis):

With monetary, regulatory and operational policies all working in overdrive, central banks have had plenty of explaining to do. During the crisis, their actions have shaped the behaviour of pretty much every financial market and institution on the planet. So central banks’ words resonate as never previously. Rarely a day passes without a forensic media and market dissection of some central bank comment. […]

Where does this leave central banks today? We are not in Kansas any more. On monetary policy, we have gone from setting short safe rates to shaping rates of return on longer-term and wider classes of assets. On regulation, central banks have gone from spectator to player, with some granted micro-prudential as well as macro-prudential regulatory responsibilities. On operational matters, central banks have gone from market-watcher to market-shaper and market-maker across a broad class of assets and counterparties. On transparency, we have gone from blushing introvert to blooming extrovert. In short, central banks are essentially unrecognisable from a quarter of a century ago.

This makes me feel slightly unconfortable and instantly remind me of the – now classic – 2010 article by Jeff Hummel: Ben Bernanke vs. Milton Friedman: The Federal Reserve’s Emergence as the U.S. Economy’s Central Planner. While I believe there are a few inaccuracies and omissions in Hummel’s description of the financial crisis, his article is really good and his conclusion even more valid today than at the time of his writing:

In the final analysis, central banking has become the new central planning. Under the old central planning—which performed so poorly in the Soviet Union, Communist China, and other command economies—the government attempted to manage production and the supply of goods and services. Under the new central planning, the Fed attempts to manage the financial system as well as the supply and allocation of credit. Contrast present-day attitudes with the Keynesian dark ages of the 1950s and 1960s, when almost no one paid much attention to the Fed, whose activities were fairly limited by today’s standard. […]

As the prolonged and incomplete recovery from the recent recession suggests, however, the Fed’s new central planning, like the old central planning, will ultimately prove an unfortunate and possibly disastrous failure.

The contrast between central bankers’ (including Haldane’s) beliefs of a tightly controlled financial sector to those of Hummel couldn’t be starker.

Where it indeed becomes really worrying is that Hummel was only referring to Bernanke’s decision to allocate credit and liquidity facilities to some particular institutions, as well as to the multiplicity of interest rates and tools implemented within the usual central banking framework. At the time of his writing, macro-prudential policies were not as discussed as they are now. Nevertheless, they considerably amplify the central banks’ central planner role: thanks to them, central bankers can decide to reduce or increase the allocation of loanable funds to one particular sector of the economy to correct what they view as financial imbalances.

Moreover, central banks are also increasingly taking over the role of banking regulator. In the UK, for instance, the two new regulatory agencies (FCA and PRA) are now departments of the Bank of England. Consequently, central banks are in charge of monetary policy (through an increasing number of tools), macro-prudential regulation, micro-prudential regulation, and financial conduct and competition. Absolutely all aspects of banking will be defined and shaped at the central bank level. Central banks can decide to ‘increase’ competition in the banking sector as well as favour or bail-out targeted firms. And it doesn’t stop here. Tighter regulatory oversight is also now being considered for insurance firms, investment managers, various shadow banking entities and… crowdfunding and peer-to-peer lending.

Hummel was right: there are strong similarities between today’s financial sector planning and post-WW2 economic planning. It remains to be seen how everything will unravel. Given that history seems to point to exogenous origins of financial imbalances (whereas central bankers, on the other hand, believe in endogenous explanations, motivating their policies), this might not end well… Perhaps this is the only solution though: once the whole financial system is under the tight grip of some supposedly-effective central planner, the blame for the next financial crisis cannot fall on laissez-faire…

Financial instability: Beckworth and output gap

I recently mentioned David Beckworth’s excellent new paper on inflation targeting, which, according to him, promotes financial instability by inadequately responding to supply shocks. Like free bankers and some other economists, Beckworth understands the effects of productivity growth on prices and the distorting economic effects of inflation targeting in a period of productivity improvements.

Nevertheless, I am a left a little surprised by a few of his claims (on his blog), some of which seem to be in contradiction with his paper: according to him, current US output gap demonstrates that the nominal natural rate of interest has been negative for a while. Consequently, the current Fed rate isn’t too low and raising it would be premature.

While I believe that the real natural interest rate (in terms of money) is very unlikely to ever be negative (though some dispute this), it is theoretically and empirically unclear whether or not the nominal natural rate could fall in negative territory, especially for such a long time.

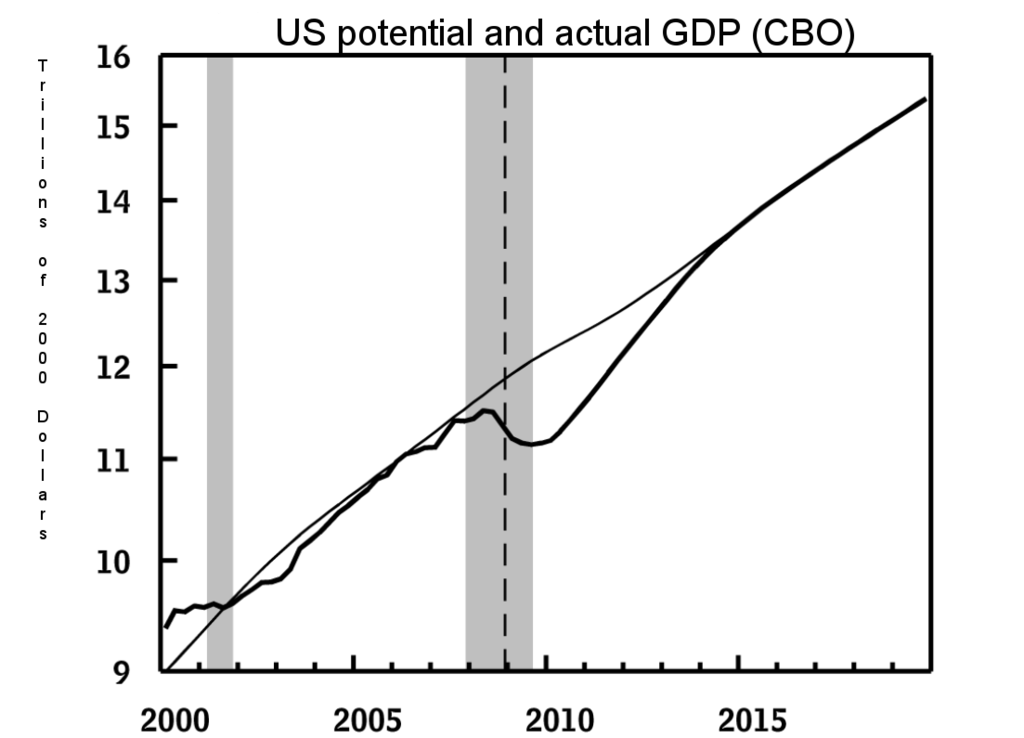

Beckworth uses a measure of US output gap calculated by the CBO and derived from their potential GDP estimate. This is where I become very sceptical. GDP itself is already subject to calculation errors and multiple revisions. Furthermore, there are so many variables and methodologies involved in calculating ‘potential’ GDP, that any output gap estimate takes the risk of being meaningless due to extreme inaccuracy, if not completely flawed or misleading.

This is the US potential GDP, as estimated by the CBO:

Wait a minute. For most of the economic bubble of the 2000s, the US was below potential? This estimate seems to believe that credit-fuelled pre-crisis years were merely in line with ‘potential’. This is hardly believable, and this reminds me of the justification used by many Keynesian economists: we should have used more fiscal stimulus as we are below ‘trend’ (‘trend’ being calculated from 2007 of course, as if the bubble years had never happened). Does this also mean that the natural rate of interest has been negative or close to zero since 2001? This seems to contradict Beckworth’s own inflation targeting article, in which he says that the Fed rate was likely too low during the period.

Let’s have a look at a few examples of the wide range of potential GDP estimates (and hence output gap) that are available out there*. The Economic Report of the President estimates potential GDP as even higher than the CBO’s (source: Morgan Stanley):

The Fed of San Francisco, on the other hand, estimated very different output gap variations. According to some measures, the US is currently… above potential:

Some of the methodologies used to calculate some of those estimates might well be inaccurate, or simply wrong. Still, this clearly shows how hard it is to determine potential GDP and thus the output gap. Any conclusion or recommendation based on such dataset seems to me to reflect conjectures more than evidences.

This is where we get to my point.

In his very good article, Beckworth brilliantly declares that:

the productivity gains will also create deflationary pressures that an inflation-targeting central bank will try to offset. To do that, the central bank will have to lower its target interest rate even though the natural interest rate is going up. Monetary authorities, therefore, will be pushing short-term interest rates below the stable, market-clearing level. To the extent this interest rate gap is expected to persist, long-term interest rates will also be pushed below their natural rate level. These developments mean firms will see an inordinately low cost of capital, investors will see great arbitrage opportunities, and households will be incentivized to take on more debt. This opens the door for unwarranted capital accumulation, excessive reaching for yield, too much leverage, soaring asset prices, and ultimately a buildup of financial imbalances. By trying to promote price stability, then, the central bank will be fostering financial instability.

Please see the bold part (my emphasis): isn’t it what we are currently experiencing? It looks to me that the current state of financial markets exactly reflects Beckworth’s description of a situation in which the central bank rate is below the natural rate. This is also what the BIS warned against, explicitely rejected by Beckworth on the basis of this CBO output gap estimate. (see also this recent FT report on bubbles forming in credit markets)

I am asking here how much trust we should place in some potentially very inaccurate estimates.

Perhaps the risk-aversion suppression and search for yield of the system is not apparent to everyone, including Beckworth, not helping him diagnose our current excesses. But, his ‘indicators that don’t show asset price froth’ are arguable: the risk premium between Baa-rated yields and Treasuries are ‘elevated’ due to QE pushing yields on Treasuries lower, and it doesn’t mean much that households still hold more liquid assets than in the financial boom years of 1990-2007.

At the end of the day, we should perhaps start relying on actual** – rather than estimated and potentially flawed – indicators for policy-making purposes (that is, as long as discretion is in place). Had US GDP been considered as above potential in the pre-crisis years and the Fed stance adapted as a result, the impact of the financial crisis might have been far less devastating. I agree with Beckworth: time to end inflation targeting.

* The IMF estimate also shows that the US was merely in line with potential as of 2007. Others are more ‘realistic’ but as the charts below demonstrate, estimates vary widely, along with confidence intervals (link, as well as this full report for tons of other output gap charts from the same authors):

** I understand and agree that ‘actual’ market and economic data can also be subject to interpretation. I believe, however, that the range of interpretations is narrower: these datasets represents more ‘crude’ or ‘hard’ data that haven’t been digested through multiple, potentially biased, statistical computations.

Is the BIS on the Dark Side of macroeconomics?

The BIS has got a hobby: to annoy other economists and central bankers. It’s a good thing. It published its annual report about two weeks ago, and the least we can say is that it didn’t please many.

Gavin Davies wrote a very good piece in the FT last week, summarising current opposite views: “Keynesian Yellen versus Wicksellian BIS”. What’s interesting is that Davies views the BIS as representing the ‘Wicksellian’ view of interest rates: that current interest rates are lower than their natural level (i.e. monetary policy is ‘loose’ or ‘easy’). On the other hand, Scott Sumner and Ryan Avent seem to precisely believe the opposite: that current rates are higher than their natural level and that the BIS is mistaken in believing that low nominal rates mean easy money. This is hard to reconcile both views.

Neither is the BIS particularly explicit. Why does it believe that interest rates are low? Because their headline nominal level is low? Because their real level is low? Or because its own natural rates estimates show that central banks’ rates are low?

It is hard to estimate the Wicksellian ‘natural rate’ of interest. Some people, such as Thomas Aubrey, attempt to estimate the natural rate using the marginal product of capital theory. There are many theories of the rate of interest. Fisher (described by Milton Friedman as America’s best ever economist), Bohm-Bawerk, and Mises would argue that the natural interest rate is defined by time preference (even though they differ on details), and Keynes liquidity preference. Some economists, such as Miles Kimball, currently argue that the natural rate of interest is negative. This view is hard to reconcile with any of the theories listed above. Fisher himself declared in The Rate of Interest that interest rates in money terms cannot be negative (they can in commodity terms).

Unfortunately, and as I have been witnessing for a while now, Wicksell is very often misinterpreted, even by senior economists. The latest example is Paul Krugman, evidently not a BIS fan. Apart from his misinterpretation of Wicksell (see below), he shot himself in the foot by declaring (my emphasis):

Now, what about the BIS? It is arguing that central banks have consistently kept rates too low for the past couple of decades. But this is not a statement about the Wicksellian natural rate. After all, inflation is lower now than it was 20 years ago.

Given that we indeed got two decades of asset bubbles and crashes, it looks to me that the BIS view was vindicated…

Furthermore, in a very good post, Thomas Aubrey corrects some of those misconceptions:

The second issue to note is that when the natural rate is higher than the money rate there is no necessary impact on the general price level. As the Swedish economist Bertie Ohlin pointed in the 1930s, excess liquidity created during a Wicksellian cumulative process can flow into financial assets instead of the real economy. Hence a Wicksellian cumulative process can have almost no discernible impact on the general price level as was seen during the 1920s in the US, the 1980s in Japan and more recently in the credit bubble between 2002-2007.

(Bob Murphy also wrote a very good post here on Krugman vs. Wicksell)

But there are other problematic issues. First, inflation (as defined by CPI/RPI/general increase in the price level) itself is hard to measure, and can be misleading. Second, as I highlighted in an earlier post, wealthy people, who are the ones who own most investible assets, experience higher inflation rates. In order to protect their wealth from declining through negative real returns (what Keynes called the ‘euthanasia of the rentiers’), they have to invest it in higher-yielding (and higher-risk) assets, causing bubbles is some asset classes (while expectations that central bank support to asset prices will remain and allow them to earn a free lunch, effectively suppressing risk-aversion).

If natural rates were negative – or at least very low – and the environment deflationary, it is unlikely that we would witness such hunt for yield: people care about real rates, not nominal ones (though in the short-run, money illusion can indeed prevail). But this is not only an ultra-rich problem: there are plenty of stories of less well-off savers complaining of reduced purchasing power.

Meanwhile, the rest of the population and overleveraged companies, supposedly helped by lower interest rates, seem not to deleverage much: overall debt levels either stagnate or even increase in most economies, as the BIS pointed out.

Banks also suffer from the combination of low rates* and higher regulatory requirements that continue to pressurise their bottom line, and have ceased to pass lower rates on to their customers.

In this context, the BIS seems to have a point: rates may well be too low. Current interest rate levels seem to only prevent the reallocation of capital towards more economically efficient uses, while struggling banks are not able to channel funds to productive companies.

Critics of the BIS point to their call to rise rates to counter inflation back in 2011. Inflation, as conventionally measured, indeed hasn’t stricken in many countries. In the UK and some other European countries though, complaints about quickly rising prices and falling purchasing power have been more than common (and I’m not even referring to house price inflation). This mismatch between aggregate inflation indicators and widespread perception is a big issue, which underlies financial risk-taking.

In the end, Keynes’ euthanasia of the rentiers only seem to prop up dying overleveraged businesses and promote asset bubbles (and financial instability) as those rentiers pile in the same asset classes. I side with the BIS in believing this is not a good and sustainable policy.

I also side with the BIS and with Mohamed El-Erian in believing in the poor forecasting ability of most central bankers, who seem to constantly display a dovish view of the economy, which apparently experiences never-ending ‘slack’, as well as the very uncertain effect of macro-prudential policies, which cannot and will not get in all the cracks. Nevertheless, many mainstream economists and economic publications seem to be overconfident in the effectiveness of macro-prudential policies (see The Economist here, Yellen here, Haldane here, who calls macropru policies “targeted lightning strikes”…).

While central banks’ rates should probably already have risen in several countries (and remain low in others, hence the absurdity of having a single monetary policy for the whole Eurozone), everybody should keep the BIS warnings in mind: after all, they were already warning us before the financial crisis, yet few people listened and many laughed at them.

Unfortunately, politicians and regulators have repeated some of the mistakes made during the Great Depression: they increased regulation of business and banking while the economy was struggling. I have many times referred to the concept of regulatory uncertainty, as well as the over-regulation that most businesses are now subject to (in the US at least, though this is also valid in most European countries). Businesses complaints have been increasing and The Economist reported on that issue last week.

In the meantime, while monetary policy has done (almost) everything it could to boost credit growth and to prevent the money supply from collapsing, harsher banking regulation has been telling banks to do the exact opposite: raise capital, deleverage, and don’t take too much risk.

In the end, monetary policy cannot fix those micro-level issues. It is time to admit that we do not live in the same microeconomic environment as before the crisis. What about cutting red tape to unleash growth rather than risk another financial crisis?

* Yes, for banks, rates are low, whichever way you look at them. Banks can simply not function by earning zero income on their interest-earning assets (loan book and securities portfolio).

PS: Noah Smith, another member of the anti-BIS crowd, has a nonsense ‘let’s keep interest rate low forever’-type article here: raising interest rates would lead to an asset price crash, so we should keep them low to have a crash later. Thanks Noah. The way he describes a speculative bubble is also wrong (my emphasis):

The theory of speculation tells us that bubbles form when people think they can find some greater fool to sell to. But when practically everyone is convinced that asset prices are relatively high, like now, it’s pretty obvious that there aren’t many greater fools out there.

Really? No, speculation involved buying as long as you believe you can get the right timing to exit the position. Even if everyone believed that asset prices were overvalued, as long as investors expect prices to continue to increase, speculation would continue: profits can still be made by exiting on time, even if you join the party late.

PPS: A particularly interesting chart from the BIS report was the one below:

It is interesting to see how coordinated financial cycles have become. Yet the BIS seems not to be able to figure out that its own work (i.e. Basel banking rules) could well be the common denominator of those cycles (which were rarely that synchronised in the past).

It is interesting to see how coordinated financial cycles have become. Yet the BIS seems not to be able to figure out that its own work (i.e. Basel banking rules) could well be the common denominator of those cycles (which were rarely that synchronised in the past).

The surprising effects of negative rates on German banks

Several banks have already made public their intentions to withdraw their excess reserves from the ECB, following the central bank’s decision to charge banks for keeping excess reserves deposited with it (i.e. negative deposit rates). It is unclear what’s going to happen to this cash. If it is redeposited at another Eurozone bank, then it still ends up on an ECB account. Euros could potentially be placed somewhere outside the Eurozone to reduce the aggregate amount of excess reserves in the system, but there is no guarantee they would not come back either (through non-Euro companies paying Euro suppliers for instance). Banks could also withdraw paper money, but this involves storage costs.

Very low ECB main rates already represented a pressure on banks’ net interest margins. The ECB negative deposit rates were seen as a way to bolster the interbank money markets. Unfortunately, many banks are now also retracting from interbank markets altogether because of the very poor yields obtained on those placements… thanks to the low ECB main rate. Seen this way, very low ECB refinancing rates and negative ECB deposit rates look contradictory.

But there’s something new.

In Germany, some banks (mostly the largest ones), are now passing on negative rates to… their clients. Handelsblatt reported last week that institutional clients such as mutual funds and insurers have now been asked to pay interests on short-term deposits… To be honest, I wasn’t really expecting such a move, given the instability it can create in banks’ funding structure. However, the effects remain for now limited as retail clients, as well as other types of corporate clients, are unaffected.

Let’s get back to our basic bank’s profit equation:

Economic Profit = II – IE – OC – Q

where II represents interest expense, IE interest income, OC operating costs (which include impairment charges on bad debt), and Q liquidity cost.

As we recently saw, low ECB interest rates impact II downward, negative ECB deposit rates impact IE upward, meaning ceteris paribus that the only thing banks can do to remain profitable in the short-run is to cut fixed costs (OC). Ex-post, banks can also influence IE by repricing their loan book upward.

This is indeed what has been happening in Germany: banks have been cutting staff, deleveraging, and outsourcing expenses to low-cost countries. The spread between new lending rates and the ECB main rate has also remained consistently high since the rate cuts, and has even started to increase again following the most recent rate cuts (see below, blue arrows represent rate cuts, red arrows represent spread increases).

By passing negative deposit rates onto customers, banks found a way of quickly increasing II to partially offset the increase in IE. The effects are faster than further increasing the interests charged on lending, as it directly impacts the outstanding stock of deposits (unlike repricing, whose pace depends on the volume and maturity profile of the bank’s loan book).

However, this provides customers with an incentive to withdraw their deposits, introducing instability in the banks’ funding structure, increasing Q. Given the limited range of customer concerned so far, those banks probably thought it was a worthwhile temporary bet. Indeed, increasing their lending volume to reduce their excess reserves, or investing those reserves somewhere, would also have increased Q anyway. Furthermore, those institutional clients are likely to have significant brokerage/trading/custody relationships with those banks, making it difficult for them to close their accounts and move funds away without disrupting their business.

I have no information regarding the implementation of such policies by other banks of the Eurozone so far. If those policies become widespread, the ECB’s decisions will not only have been pointless, but they will also have succeeded in making the funding structure of the whole Eurozone banking system more unstable and in reducing the purchasing power of non-bank corporations that have to maintain deposits in the Eurozone.

The (negative) mechanics of negative ECB deposit rates

The ECB has finally announced last week that it would be lowering its main refinancing rate from 0.25% to 0.15%, and that it would lower the rate it pays on its deposit facility from 0% to -1%. The ECB hopes to incentivise banks to take money out of that facility and lend it to customers*, providing a boost to the broad money supply and counteracting deflation risks.

The interest rate of the ECB deposit facility is supposed to help the central bank define a floor under which the overnight interbank lending rate (EONIA) should not go. The reason is that deposits at the ECB are supposedly risk-free (or at least less risky than placing the money anywhere else). Consequently, banks would never place money (i.e. excess reserves) at another bank/ investment (which involves credit risk) for a lower rate. When the deposit facility rate is high, banks are incentivised to reduce their interbank lending exposures and leave their money at the ECB (and vice versa). On the other hand, the main refinancing rate is supposed to represent an upper boundary to the interbank lending rates: theoretically, banks should not borrow from another bank at a higher rate than what it would pay at the ECB. In practice, this is not exactly true, as banks do their best to avoid the stigma associated with borrowing from the central bank.

Unfortunately, there is a fundamental microeconomic reason why banks cannot diminish their lending rate indefinitely. I have already described how banks are not able to transmit interest rates lower than a certain threshold to their customers due to the margin compression effect (see also here). Indeed, banks’ net interest income must be able to cover banks’ fixed operating costs for the bank to remain profitable from an accounting point of view. When rates drop below a certain level, banks have to reprice their loan book by increasing the spread above the central bank rate on the marginal loans they make, breaking the transmission mechanism of the lending channel of monetary policy. As we have already seen, in the UK, that threshold seems to be around 2%.

But the same thing seems to happen in other European countries. This is Ireland (enlarge the charts)**:

We can notice the margin compression effect on the first chart. The lending rate stops dropping despite the ECB rate falling as banks reprice their lending upward to re-establish profitability (evidenced from the second chart, where interest rates on new lending increase rather than decrease).

This is France:

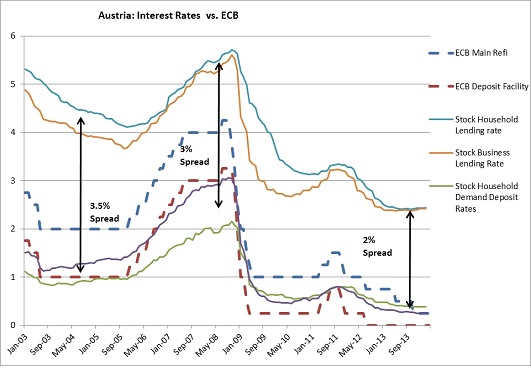

This is Austria:

Clearly, what happens in the UK regarding margin compression also occurs in those countries. When the ECB rate dropped, outstanding floating rate lending rates also dropped (because floating rate lending is indexed on either the ECB base rate or on Euribor), causing pressure on revenues. As long as deposit rates could also fall (this varies a lot by country, as French banks never pay anything on demand deposits), the loss in interest income was offset by reduced interest expense. But once deposit rates reached 0 and couldn’t fall any lower, banks in those countries experienced margin compression and their net interest income started to suffer. Moreover, this happened exactly when loan impairment charges peaked because of increased credit risk.

Banks in emerging countries have constantly high non-performing loans ratios. But they still manage to remain (often highly) profitable by maintaining very high net interest income and margins. In Western Europe, banks saw their net profits all but disappear with rates dropping that low. As a result, it is likely that the new ECB rate cut won’t affect lending rates much…

Nonetheless, the ECB had been trying to revive, or encourage, interbank lending throughout most of the crisis, and had already lowered to its deposit rate to 0%. Nevertheless, banks maintained cash in those accounts. Why would a bank leave its money in an account that pays 0%? Because banks adjust those interest rates for risk. An ECB risk-adjusted 0% can be worth more than a risk-adjusted 4% interbank deposit at a zombie/illiquid/insolvent bank. However, the ECB is clearly not satisfied with the situation: it now wants banks to take their money out of the facility and lend it to the ‘real economy’.

How do the combination of low refi rate and negative ECB deposit rates impact banks? Let’s remember banks’ basic profit equations:

Accounting Profit = II – IE – OC, and Economic Profit = II – IE – OC – Q

where II represents interest expense, IE interest income, OC operating costs (which include impairment charges on bad debt), and Q liquidity cost.

For a bank to remain economically profitable (or even viable in the long-term), the rate of economic profit must be at least equal to the bank’s cost of equity.

To maximise their economic profits, banks look for the most-profitable risk-adjusted lending opportunities. ‘Lending’ to the ECB is one of those opportunities. Placing money at the ECB generates interest income. This interest income is more than welcome to (at least) maintain some level of accounting profitability (though not necessarily economic profitability) when economic conditions are bad and income from lending drops while impairment charges jump***.

With deposit rates at 0, banks’ income became fully constrained by financial markets and the economy. With rates in negative territory, not only banks see their interest income vanish but also their interest expense increase. From the equations above, it is clear that it makes banks less profitable****. On top of that, lending that cash can make banks less liquid, which increases their riskiness and elevates their cost of capital (the ‘Q’ above). The question becomes: adjusted for credit and liquidity risk, is it still worth keeping that cash at the ECB? The answer is probably yes.

(unless banks find worthwhile investments outside of the Eurozone, which wouldn’t be of much help to prop up Euro economies…)

To summarise, ‘II’ is negatively impacted by a low base rate whereas ‘IE’ reaches a floor (= margin compression). ‘IE’ then increases when the central bank deposit rate turns negative. Meanwhile, ‘OC’ increases as loan impairment charges jump due to heightened credit risk. Profitability is depressed, partly due to the central bank’s decisions.

Many European banks aren’t currently lending because they are trying to implement new regulatory requirements (which makes them less profitable) in the middle of an economic crisis (which… also makes them less profitable). As a result, the ECB measures seem counterproductive: in order to lend more, banks need to be economically profitable. Healthy banks lend, dying ones don’t.

The ECB is effectively increasing the pressure on banks’ bottom line, hardly a move that will provide a boost to lending. The only option for banks will be to cut costs even further. And when a bank cut costs, it effectively reduces its ability to expand as it has less staff to monitor lending opportunities, and consequently needs to deleverage. Once profitability is re-established, hiring and lending could start growing again.

A counterintuitive (and controversial) approach to provide a boost to lending would be to subsidise even more the banking sector by increasing interest rates on both the refinancing and deposit facilities.

Defining the appropriate level of interest rates would be subtle work though: struggling over-indebted households and businesses may well start defaulting on their debt. On the other hand banks’ revenues would increase as margin compression disappears, making them able to lend more eventually. The subtle balance would be achieved when interest income improvements more than offset credit losses increases. Not easy to achieve, but pushing rates ever lower is likely to cripple the banking system ever more and reduce lending in proportion (while allowing zombie firms to survive).

Furthermore, banks are repricing their loan book upward anyway, making the ECB rate cuts pointless. The process takes time though and it would be better for banks to rebuild their revenue stream sooner than later. The ECB could still use other monetary tools to influence a range of interest rates and prices through OMO and QE measures, which would be less disruptive to banks’ margins.

Finally, the ECB has launched its own-FLS style ‘TLTRO’, a scheme that provides cheap funding to banks if they channel the funds to businesses. Similarly to the BoE’s FLS, I believe such scheme suffers from delusion. Banks are currently deleveraging to lower their RWAs in order to comply with the harsher capital requirements of Basel 3. If there is one thing banks want to avoid, it is to lend to RWA-dense customers such as SMEs… (and instead focus on better RWA/risk-adjusted profitable lending such as… mortgages). Banks can also already extract relatively low wholesale funding rates by issuing secured funding instruments such as covered bonds. (UPDATE: see this follow-up post on that topic)

* This does not mean that banks would ‘lend out’ money to customers, unless they withdraw it as cash. But by increasing lending, absolute reserve requirements increase and banks have to transfer money from the deposit facility to the reserve facility.

** Data comes from respective central banks. They are not fully comparable. I gathered data from many different Eurozone countries, but unfortunately, some central banks don’t provide the data I need (or the statistics database doesn’t work, as in Italy…). Spreads are approximate ones calculated between the middle point of deposit rates and the middle point of lending rates. Analysis is very superficial, and for a more comprehensive methodology please refer to my equivalent posts on the UK/BoE.

*** Don’t get me wrong though. Fundamentally speaking, I am not in favour of such central bank mechanisms as I believe this is akin to a subsidy that distorts banks’ risk-taking behaviour. In a central banking environment, like Milton Friedman I’d rather see the central bank manipulate interest rates solely through OMO-type operations.

**** Of course this remains marginal. But in crisis times, ‘marginal’ can save a bank. Let’s also not forget booming litigation charges, currently estimated at USD104Bn… Evidently making it a lot easier for banks to lend as you can imagine…

News digest: central bank independence, TBTF and ironic regulators

I’m quite busy at the moment so not many updates here. However I am almost done with Michael Lewis’ new book on high-frequency trading Flashboys. I’ll surely write something about it soon.

The FT had this week an interesting and quite comprehensive article on fintech and new financial start-ups (not sure they all qualify as ‘fintech’ though…). It’s a good introduction for those who don’t know what’s going on in the sector.

On the other hand, about a week ago, Martin Wolf had one of the worst articles on the recent BoE paper on money creation I have had the occasion to read. It looks like Wolf is oblivious to the intense debate on the blogosphere (and elsewhere) that was triggered by the publication of this controversial, and flawed, paper. But… I guess I have given up on Martin Wolf…

US banks have published (through the Clearinghouse association) a new paper arguing that large banks had not been benefiting from the ‘too big to fail’ funding advantage since 2013. I believe this study is quite right but I also think it misses the point made by previous research papers (see one of them here): the main question wasn’t “are banks subsidised for being TBTF?” but “were banks subsidised for being TBTF?”, which could lead to a crisis. There are many reasons why spreads between TBTF and non-TBTF banks would narrow in the short-term. A simple one could be: many large banks are actually currently in a worse financial shape than smaller banks. Another one: states have kept repeating their intentions not to bail out banks and introduced bail-in mechanisms. The paper doesn’t seem to have an answer to this and takes a way too short time horizon to really assess the effectiveness of anti-TBTF measures. It will take another few years to have a definitive answer.

As I said in a recent post, regulators are taking over all the corners of our modern financial system. Another recent target: bank overdraft fees. They basically complain that overdrafts can be more expensive than…payday loans. But they attacked payday loans as predatory. They didn’t seem to get the underlying mechanism at play here… So what’s their logic? Protecting the consumer. But by limiting payday loans, some people will be cut off credit altogether, while some others will have to use…more expensive overdrafts. If overdrafts costs are then pushed down, then it is highly likely that the cost of other services will be pushed up. In the end, regulators just move the problem rather than solve it.

The ironic news of the week is: US state regulators are concerned about the methods used by US federal regulators to crack down on payday lenders (gated link). Just wow.

Christine Lagarde, head of the IMF, declared this week that central bank independence from government control should probably end. While central banks are already arguably not fully independent, I find really scary the types of reaction brought about by the financial crisis. It is like humanity had all of a sudden forgotten the lessons learnt from several centuries of financial history.

Finally, the FT reports a new research paper on the use of pseudo-mathematical models in investment strategies (paper available here). Researchers argue that most of those models are deeply flawed as they are twisted to fit past data. I haven’t read the paper yet but I will soon as I suspect their conclusions also involve other parts of the banking industry.

Recent Comments