The (negative) mechanics of negative ECB deposit rates

The ECB has finally announced last week that it would be lowering its main refinancing rate from 0.25% to 0.15%, and that it would lower the rate it pays on its deposit facility from 0% to -1%. The ECB hopes to incentivise banks to take money out of that facility and lend it to customers*, providing a boost to the broad money supply and counteracting deflation risks.

The interest rate of the ECB deposit facility is supposed to help the central bank define a floor under which the overnight interbank lending rate (EONIA) should not go. The reason is that deposits at the ECB are supposedly risk-free (or at least less risky than placing the money anywhere else). Consequently, banks would never place money (i.e. excess reserves) at another bank/ investment (which involves credit risk) for a lower rate. When the deposit facility rate is high, banks are incentivised to reduce their interbank lending exposures and leave their money at the ECB (and vice versa). On the other hand, the main refinancing rate is supposed to represent an upper boundary to the interbank lending rates: theoretically, banks should not borrow from another bank at a higher rate than what it would pay at the ECB. In practice, this is not exactly true, as banks do their best to avoid the stigma associated with borrowing from the central bank.

Unfortunately, there is a fundamental microeconomic reason why banks cannot diminish their lending rate indefinitely. I have already described how banks are not able to transmit interest rates lower than a certain threshold to their customers due to the margin compression effect (see also here). Indeed, banks’ net interest income must be able to cover banks’ fixed operating costs for the bank to remain profitable from an accounting point of view. When rates drop below a certain level, banks have to reprice their loan book by increasing the spread above the central bank rate on the marginal loans they make, breaking the transmission mechanism of the lending channel of monetary policy. As we have already seen, in the UK, that threshold seems to be around 2%.

But the same thing seems to happen in other European countries. This is Ireland (enlarge the charts)**:

We can notice the margin compression effect on the first chart. The lending rate stops dropping despite the ECB rate falling as banks reprice their lending upward to re-establish profitability (evidenced from the second chart, where interest rates on new lending increase rather than decrease).

This is France:

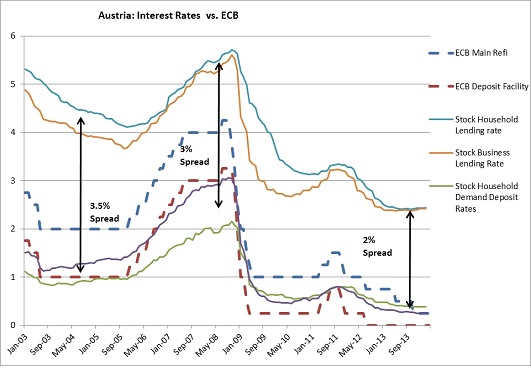

This is Austria:

Clearly, what happens in the UK regarding margin compression also occurs in those countries. When the ECB rate dropped, outstanding floating rate lending rates also dropped (because floating rate lending is indexed on either the ECB base rate or on Euribor), causing pressure on revenues. As long as deposit rates could also fall (this varies a lot by country, as French banks never pay anything on demand deposits), the loss in interest income was offset by reduced interest expense. But once deposit rates reached 0 and couldn’t fall any lower, banks in those countries experienced margin compression and their net interest income started to suffer. Moreover, this happened exactly when loan impairment charges peaked because of increased credit risk.

Banks in emerging countries have constantly high non-performing loans ratios. But they still manage to remain (often highly) profitable by maintaining very high net interest income and margins. In Western Europe, banks saw their net profits all but disappear with rates dropping that low. As a result, it is likely that the new ECB rate cut won’t affect lending rates much…

Nonetheless, the ECB had been trying to revive, or encourage, interbank lending throughout most of the crisis, and had already lowered to its deposit rate to 0%. Nevertheless, banks maintained cash in those accounts. Why would a bank leave its money in an account that pays 0%? Because banks adjust those interest rates for risk. An ECB risk-adjusted 0% can be worth more than a risk-adjusted 4% interbank deposit at a zombie/illiquid/insolvent bank. However, the ECB is clearly not satisfied with the situation: it now wants banks to take their money out of the facility and lend it to the ‘real economy’.

How do the combination of low refi rate and negative ECB deposit rates impact banks? Let’s remember banks’ basic profit equations:

Accounting Profit = II – IE – OC, and Economic Profit = II – IE – OC – Q

where II represents interest expense, IE interest income, OC operating costs (which include impairment charges on bad debt), and Q liquidity cost.

For a bank to remain economically profitable (or even viable in the long-term), the rate of economic profit must be at least equal to the bank’s cost of equity.

To maximise their economic profits, banks look for the most-profitable risk-adjusted lending opportunities. ‘Lending’ to the ECB is one of those opportunities. Placing money at the ECB generates interest income. This interest income is more than welcome to (at least) maintain some level of accounting profitability (though not necessarily economic profitability) when economic conditions are bad and income from lending drops while impairment charges jump***.

With deposit rates at 0, banks’ income became fully constrained by financial markets and the economy. With rates in negative territory, not only banks see their interest income vanish but also their interest expense increase. From the equations above, it is clear that it makes banks less profitable****. On top of that, lending that cash can make banks less liquid, which increases their riskiness and elevates their cost of capital (the ‘Q’ above). The question becomes: adjusted for credit and liquidity risk, is it still worth keeping that cash at the ECB? The answer is probably yes.

(unless banks find worthwhile investments outside of the Eurozone, which wouldn’t be of much help to prop up Euro economies…)

To summarise, ‘II’ is negatively impacted by a low base rate whereas ‘IE’ reaches a floor (= margin compression). ‘IE’ then increases when the central bank deposit rate turns negative. Meanwhile, ‘OC’ increases as loan impairment charges jump due to heightened credit risk. Profitability is depressed, partly due to the central bank’s decisions.

Many European banks aren’t currently lending because they are trying to implement new regulatory requirements (which makes them less profitable) in the middle of an economic crisis (which… also makes them less profitable). As a result, the ECB measures seem counterproductive: in order to lend more, banks need to be economically profitable. Healthy banks lend, dying ones don’t.

The ECB is effectively increasing the pressure on banks’ bottom line, hardly a move that will provide a boost to lending. The only option for banks will be to cut costs even further. And when a bank cut costs, it effectively reduces its ability to expand as it has less staff to monitor lending opportunities, and consequently needs to deleverage. Once profitability is re-established, hiring and lending could start growing again.

A counterintuitive (and controversial) approach to provide a boost to lending would be to subsidise even more the banking sector by increasing interest rates on both the refinancing and deposit facilities.

Defining the appropriate level of interest rates would be subtle work though: struggling over-indebted households and businesses may well start defaulting on their debt. On the other hand banks’ revenues would increase as margin compression disappears, making them able to lend more eventually. The subtle balance would be achieved when interest income improvements more than offset credit losses increases. Not easy to achieve, but pushing rates ever lower is likely to cripple the banking system ever more and reduce lending in proportion (while allowing zombie firms to survive).

Furthermore, banks are repricing their loan book upward anyway, making the ECB rate cuts pointless. The process takes time though and it would be better for banks to rebuild their revenue stream sooner than later. The ECB could still use other monetary tools to influence a range of interest rates and prices through OMO and QE measures, which would be less disruptive to banks’ margins.

Finally, the ECB has launched its own-FLS style ‘TLTRO’, a scheme that provides cheap funding to banks if they channel the funds to businesses. Similarly to the BoE’s FLS, I believe such scheme suffers from delusion. Banks are currently deleveraging to lower their RWAs in order to comply with the harsher capital requirements of Basel 3. If there is one thing banks want to avoid, it is to lend to RWA-dense customers such as SMEs… (and instead focus on better RWA/risk-adjusted profitable lending such as… mortgages). Banks can also already extract relatively low wholesale funding rates by issuing secured funding instruments such as covered bonds. (UPDATE: see this follow-up post on that topic)

* This does not mean that banks would ‘lend out’ money to customers, unless they withdraw it as cash. But by increasing lending, absolute reserve requirements increase and banks have to transfer money from the deposit facility to the reserve facility.

** Data comes from respective central banks. They are not fully comparable. I gathered data from many different Eurozone countries, but unfortunately, some central banks don’t provide the data I need (or the statistics database doesn’t work, as in Italy…). Spreads are approximate ones calculated between the middle point of deposit rates and the middle point of lending rates. Analysis is very superficial, and for a more comprehensive methodology please refer to my equivalent posts on the UK/BoE.

*** Don’t get me wrong though. Fundamentally speaking, I am not in favour of such central bank mechanisms as I believe this is akin to a subsidy that distorts banks’ risk-taking behaviour. In a central banking environment, like Milton Friedman I’d rather see the central bank manipulate interest rates solely through OMO-type operations.

**** Of course this remains marginal. But in crisis times, ‘marginal’ can save a bank. Let’s also not forget booming litigation charges, currently estimated at USD104Bn… Evidently making it a lot easier for banks to lend as you can imagine…

6 responses to “The (negative) mechanics of negative ECB deposit rates”

Trackbacks / Pingbacks

- - 11 June, 2014

- - 11 June, 2014

- - 30 July, 2014

- - 21 February, 2016

Leave a comment

Recent Comments

| pslebow on ‘Sovereign money’:… | |

| pslebow on A critique of Werner’s view on… | |

| Hugo Kramer on Welcome to Spontaneous Fi… | |

| Nathan on A critique of Werner’s view on… | |

| Nathan on More, more, more money endogen… |

I myself had been planning to blog on this topic, and I may yet. I agree with everything you say.

Banks chiefly make money by gathering below-market retail deposits and then lending them into wholesale money markets; secondarily, they make loans with spreads above their cost of funds. Banks have spent huge sums building deposit-gathering networks to obtain below-market consumer deposits. When inflation and interest rates are zero, those deposits cost more to obtain (due to overhead) than wholesale funding from the market. The banks are thus losing money on their core intermediation business. Net interest income has been kept afloat by the high yield of the banks’ dwindling asset books (bonds, mortgages, etc.), but this is a wasting asset. Once this endowment effect is gone, they will have no recourse but to push outwards on the maturity and risk spectrums. They will have strong incentives to play accounting games which inflate current income at the expense of future income, and to take long-term bets which are inappropriate for a deposit fiduciary. These chickens will start coming home to roost very soon, assuming that banks cannot fully control their financial reporting. In many countries, such as Japan, they can control their reported numbers. Whether that is true in Europe remains to be seen. The only way to interrupt this disaster scenario would be for the ECB to raise inflation and interest rates to their pre crisis levels, which is not in the cards given its commitment to deflation.

Chris,

I’m not sure banks will necessarily have to push outwards on the maturity and risk spectrum as long as there is enough new lending volume to reprice upward their loan book without increasing its risk profile. The effects though is that any interest rate cut will not be transmitted to new borrowers.

I also think inflation is unnecessary, but higher rates (excluding their inflation premium) are.