More on the natural rate of interest

Since my recent post on Wicksell, a number of famous economists have also blogged on the Wicksellian ‘natural’ rate of interest.

Tyler Cowen asked ‘what’s the natural rate of interest?’ and has a few interesting points. Paul Krugman responds to Cowen by making the usual mistake (albeit shared by most mainstream academics) of defining the natural Wicksellian rate as the “the rate of interest at which the economy would be more or less at full employment, which in turn implies that inflation will be more or less stable.” He adds that there is no reasonable case that interest rates are kept artificially low. Meanwhile, on Econlog, Scott Sumner added that there was “nothing natural about the natural rate of interest” and added some comments and charts on his own blog, declaring that the natural rate is surely negative.

Cowen in turn responded to Krugman, highlighting that risk was not a good reason to justify low risk-free natural rates. He elaborates on a few points, but one in particular was, I believe, spot on: what he calls “growing legal and institutional requirements for T-Bills as collateral”. While he believes that this hypothesis still has to be demonstrated empirically, he linked to a 2-year old post of his I had missed in which he discusses this theory in more detail.

Here are his first few points:

1. Imagine that financial institutions and traders have to hold large quantities of T-Bills (and similar assets) to participate in financial markets. That may be to satisfy collateral requirements, to meet government regulations, to be credible in private market transactions, and so on.

2. The demand for these assets is now so high and so persistent that the assets have persistently low nominal returns and often negative real returns.

3. The holders of these assets do not however receive negative returns on their portfolio as a whole, when deciding to hold these T-Bills. Holding the T-Bills is like paying an entry fee into financial markets. And once they are in financial markets of the right kind, these market players can earn high returns by possessing special trading technologies (the technology may vary across market participants, but think HFT, hedge funds, prop trading, employing quants, and so on).

4. Let’s say you are not a major financial institution. Then you really will earn negative returns on your safe saving. You might try holding equities, but a) you are not wealthy and thus you are fairly risk averse, and b) as a small player you do not have access to these special trading technologies and indeed you must trade against those who do. You thus will often earn negative or low returns on your portfolio no matter what.

5. The implied prediction is that differential rates of wealth accumulation will be a driver of inequality over time. This seems to be the case.

It is sad that Cowen is not an expert in banking and financial regulation, because he had a remarkable insight there.

US Treasury yields (as well as most government-issued securities and a number of highly-rated corporate ones) do not reflect the ‘natural’ supply and demand of the market. Instead, demand is artificially raised by financial regulation, as I have explained in a number of posts (see this previous blog post on the BIS, which explained how its recent financial reforms will impact a number of reference rates, and also this post for instance). This is where Krugman is wrong when he says that interest rates are not kept artificially low. While we can argue whether or not the Fed and other central banks manipulate rates downward, there is no argument here: regulation does push a number of reference interest rates down.

This was also the case (to a lesser extent) in the post-war era, making Scott Sumner’s reasoning inaccurate, as pointed out by one his commenters. Remarkably, Scott seemed to agree that this might indeed be a good point. Over the past three decades, regulation has fundamentally influenced the demand for a number of assets, modifying their market prices/yields in the process. Any comprehensive analysis, from the causes of the crisis to secular stagnation, should take those microeconomic changes into account. I have read countless academic papers over the past few years, and almost none did. They seemed to consider that banking behaviour and incentives were (mostly) constant over time. They weren’t.

So a number of economists might be slowly waking up to the fact that financial market prices are not freely determined, which seriously constrains our ability to reach conclusions based on market trends. There are many other underlying drivers (the ‘microeconomics of banking’ that I keep mentioning) that are at play.

PS: Marcus Nunes has an interesting post on determining (or not) the natural rate of interest. I agree that there is no point trying to determine the rate to target it.

Will Switzerland reveal the lower bound?

Given that a number of central banks have moved some of their monetary policy tools into negative territory for the first time in their history, many people have questioned the assumption that the zero lower bound is effectively the lower bound that conventional economic theory describes. However, most economists do think that the lower bound exists; it is simply negative (as storing cash also involves a cost) and nobody really knows what its precise level is.

Hence the interesting experiment now happening in Switzerland, which seems to provide us with some indications. The SNB target range has now been in negative territory for a little while, and demand deposits at the central bank are currently charged a negative rate of 0.75%:

This is causing some issues for Swiss banks, in particular those that don’t have any international presence. SNL (link) reports that overall Swiss net interest income is declining by 6% this year and net interest margin is down from 1.8% in 2007 to less than 1.3% in 2014. Including the two largest and international Swiss lenders, NIM drops to 60pb, lower than in Japan. Between 2013 and 2015, NIM is forecasted to fall by 11%. Unsurprisingly, profitability is low. Add the harsh Swiss banking regulation and SNL now calls Swiss banks ‘low-return low-risk utilities’. This is a typical effect of the margin compression effect I keep mentioning on this blog.

Evidently, many Swiss banks are private entities that don’t really enjoy this situation. First, despite the lowest interest rates ever, banks have increased rates on mortgages; a phenomenon I had predicted in a margin compression period (see my discussion with Ben Southwood, who believes that competitive pressure cannot allow banks to raise rates). Second, a number of Swiss banks have been charging negative rates on large corporate deposits for several months already. Recently. a small Swiss bank revealed it would charge 0.125% on slightly less than a third of its clients’ accounts.

SNL reports that a large pension fund attempted to withdraw physical cash earlier in the year. Attempt that failed. But there is apparently growing demand for safe deposit boxes in the country, although demand remains limited as negative rates are only charged on corporate, and now some large retail, deposits.

While those are early signs, they remain important signs that we are getting closer to the actual lower bound. Various types of customers can also have different lower bound tolerance, and small retail depositors, for now unconcerned by negative rates, may be less tolerant of such charges. Once negative rates generalise, we’ll find out how deep the lower bound really is.

Central bankers, who believe they can stabilise the economy by imposing negative rates, might well endanger it in reality. If negative rates generalise, the banking sector will be weakened: not only its profitability will get depressed (and you need a healthy banking system to extend credit for productive purposes), but also its funding structure will become much more unstable. Indeed, depositors will be more likely to withdraw their deposits and avoid getting locked in longer maturity saving products, exacerbating banks’ maturity mismatches. Eventually, the net effect of negative rates might not be that positive.

PS: I’d like to know what the proponents of ‘the Wicksellian natural rate of interest is negative because of our depressed economy’ think in the case of Switzerland. Its economy doesn’t look particularly under stress, yet it is imposed negative rates by its central bank to control FX fluctuations. George Selgin also has a nice post on deflation in Switzerland, which, unlike conventional wisdom, doesn’t seem to be damaging.

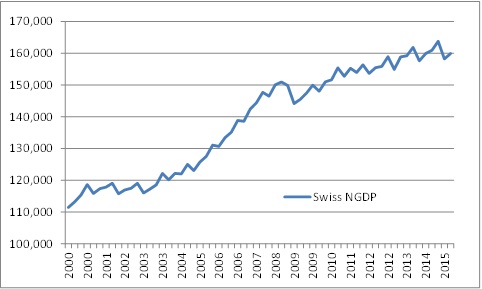

This is the quarterly Swiss NGDP since 2000, extracted from the SNB website:

Note that the post-crisis NGDP trend has not caught up with pre-crisis trend. Very far from that (also note that the growth trend changed twice over the past 15 years). I suspect that some would advocate a much larger SNB stimulus to cause inflation to get NGDP back on track (but on which track?). Despite this ‘output gap’, the Swiss economy seems to be relatively healthy, at least for European standards.

PPS: an analyst, interviewed by SNL on the topic of the abolition of cash cherished by Kimball or Buiter, perfectly answered:

“That,” said Maier, “would be my definition of hell.”

Wicksell is hiding; the real estate boom isn’t

The Wicksellian natural rate of interest remains an economic mystery. No one knows what its level is. That wouldn’t be a problem if no one tried to emulate (or voluntarily tried to manipulate it downward or upward), that is, if we had a free market for money. But we don’t and a number of central banks attempt to estimate what this interest rate is so they can play with their own monetary policy tools.

Problem is, no one has a proper definition, and we often hear about a ‘neutral’ rate of interest, or a ‘natural’ rate that would maintain CPI stable or on a stable growth trend, and/or a rate that would be consistent with ‘full employment’ or that would allow GDP growth in line with an often ill-defined ‘potential output’. This is all very confusing, and doesn’t seem to accurately represent what Wicksell originally called the ‘natural rate of interest’, that is, the rate whose level would not affect ‘commodity prices’ and is similar to the rate of interest of a money free world (see Interest and Prices). Some believe the natural rate to be relatively stable; others believe it to fluctuate in line with business cycles. This Bruegel post sums up quite well the differing views that a number of current economists hold.

A common view today is that the natural rate has turned negative in most of the Western world since the financial crisis. It’s a view held by a wide range of economists, from Keynesians to Market Monetarists. Scott Sumner believes that the rate is firmly negative (David Beckworth too, and he denies that central banks affect interest rates – see also my response to Ben Southwood on the same topic) because

Since 2008, the inflation rate has usually been below the Fed’s 2% target, and if you add in employment (part of their dual mandate) they’ve consistently fallen short. This means that money has been too tight, i.e. the actual interest rate has clearly been above the Wicksellian equilibrium rate.

He is therefore surprised by a new piece of research by two Richmond Fed economists, who came up with very different conclusions.

First, they remind us of an estimate of the natural rate made by Laubach and Williams, which shows the nominal rate to have fallen into negative territory since the crisis, but also that the real rate is too loose:

Using a different methodology, which they believe more accurately reflects Wicksell’s original vision, the authors estimate the natural rate of interest to be higher than that estimated by LW. They also point out that it never turns negative.

This demonstrates how tricky it can be to estimate this rate (see their lower/upper bound estimates…), and how easily central bankers could make policy mistakes as a result. (See also estimates from Thomas Aubrey’s methodology, i.e. ‘Wicksellian differential’)

Interestingly, all Fed economists above estimate the natural rate to be below the real money rate of interest from around 1994 to 2002, that is, money was too tight during the period. Thomas Aubrey, by contrast, finds the opposite result, with a positive Wicksellian differential over the period, meaning that money was too loose. Similarly, Anthony Evans writes on Kaleidic Economics that his own estimate of the UK natural rate is 2.3%; much higher than the current BoE rate.

If the Fed economists are right, it means that the classic Austrian Business Cycle theory (i.e. malinvestments originating in economic discoordination due to money rate of interest below the natural rate) cannot apply to most of the two decades preceding the crisis (it can in the case of Aubrey’s theory however).

As some readers already know, malinvestments and economic discoordination can still happen independently of the level of the risk-free natural rate of interest. This is what I theorised in my RWA-based ABCT: Basel banking regulations add another layer of distortion to the credit allocation process.

Where it gets scary is that, according to the same Fed economists, the current monetary policy stance is too loose. I find it hard to understand the outright dismissal of those estimates by a number of economic commentators and professors. Some commenters on Sumner’s post don’t even try to discuss the theoretical basis of this Richmond Fed paper. They see some sort of conspiracy or whatever. Not really the highest sort of intellectual debate to say the least. When some ‘evidence’ seems to challenge your theoretical framework, don’t dismiss it outright. Address it.

Personally, I have repeated a number of times that I find it hard to believe that our recent economic woes were so severe that they led to a market clearing, natural, Wicksellian rate below zero for the first time in the history of mankind. I have also tried to show elsewhere that a free banking system would be highly unlikely to drop rates below the zero-lower bound.

Now, if the estimates highlighted above are right, I fear possibly huge distortions in the real estate market. Let’s define a simplified free-market mortgage interest rate as

MR = RFR + IP + CRP – C,

where MR is the mortgage rate, RFR is the applicable, same maturity, risk-free rate, IP the expected inflation premium, CRP the credit risk premium that applies to that particular customer and C the protection provided by the collateral (that is, house value, with lower LTV loans leading to higher C).

Ceteris paribus, if the RFR is pushed downward, MR goes down, likely stimulating the demand for real estate credit. But this can also apply to all sort of lending. Enter Basel.

In a Basel world, the favourable capital treatment of such loans increases the supply of loanable funds towards the real estate sector. MR is pushed down even further, leading to an increase in demand for mortgages, in turn pushing house prices up, which raises the value of collateral C, which lowers MR further. It’s a virtuous (or rather vicious) circle. On the other hand, the stimulating effect of the lower RFR applied to SME lending gets ‘suppressed’ by the reduced supply of loanable funds for that type of credit. (and there are many other impacts on the RFR emanating from Basel)

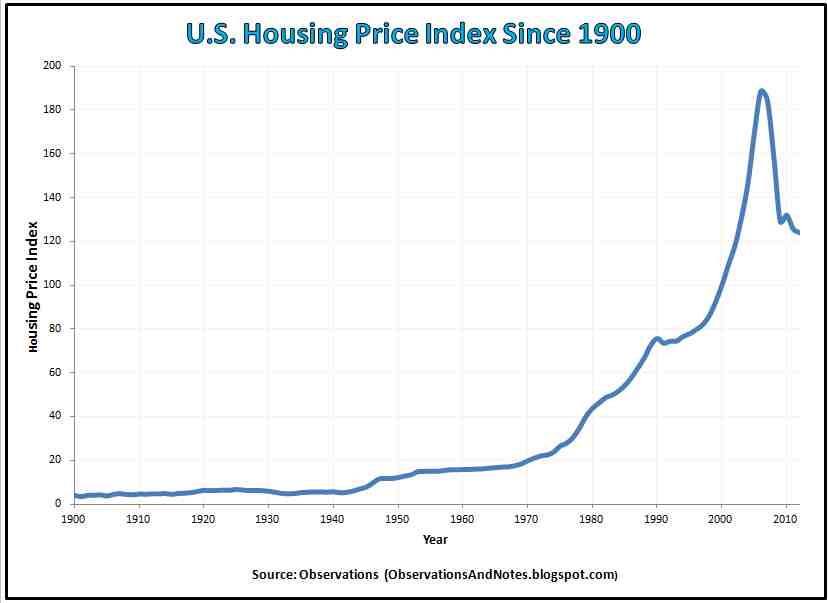

I warned more than two years ago that this situation would continue. And this is precisely what has been happening. While the media complain on a weekly basis that SMEs are starved of bank credit and turn to alternative lenders (while regulators attempt to revive the market for securitised corporate loans), the Economist reports that housing markets are either strongly recovering or even way overvalued in most advanced economies. This sort of continuous and rapid house prices booms and busts was unknown in history before the 80s/90s (see also here).

It is unclear what the exact contribution of low risk-free rates is, relative to Basel’s. What is certain is that, if Richmond Fed economists are right, we’re in for another housing disaster as Basel’s effects get amplified by monetary policy (which doesn’t necessarily imply that the effects would be similar to those of the 2008/9 crisis, although historical evidence shows that housing bubble are the most damaging types of ‘bubbles’).

150 years of nominal interest rates distortion?

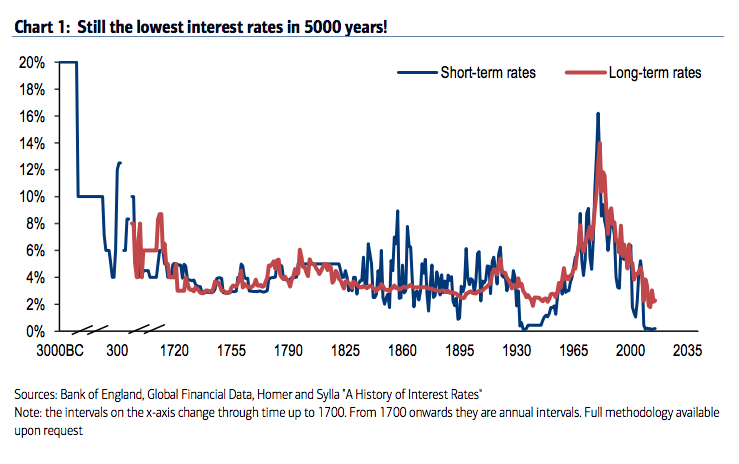

A very useful post was published on the FT Alphaville blog by David Keohane. It shows nominal interest rates levels over the past 5000 years in three different charts.

The first one comes from Andy Haldane, from the BoE:

The second one from Hartnett, from Bank of America Merrill Lynch:

The last one comes from Costa Vayenas, from UBS:

Those charts use different sources so don’t look exactly the same. Nevertheless, they all show the same striking facts. In particular, the 20th and 21st centuries seem to have been huge monetary experiments: nominal rates went both sky high and negative within a few decades… Within a period of barely more than a 100 years, rates fell to the bottom (Great Depression), then jumped ridiculously high to counteract inflationary pressure in the 1970s and 1980s (i.e. the disastrous impact of crude Keynesian macro theory) that resulted from the money multiplier recovering after the Depression, then fell to the bottom again or even negative (Great Recession).

Remember: the 20th century was the period of the generalisation of central banking. It definitely looks like they have been successful at stabilising money markets (and remember this paper by Selgin and White, which shows how successful the Fed has been at stabilising the value of the dollar since its creation). In short, great success for central bankers*.

Another interesting fact is that nominal rates started to wildly fluctuate once the BoE was granted the exclusive right to issue banknotes in the London area in 1844. Unlikely to be a coincidence.

Something that worries me though is the current state of monetary policy throughout most of the Western world. Rates are stuck at the zero bound or even went negative for the first time in history. Perhaps this is justified. But I keep wondering whether our economies currently are in a worse state than at any time in history to justify such low rates (although to be fair, Haldane’s chart does show that long-term nominal rates remain around historical levels – but not Hartnett’s).

Real interest rate charts would also have been interesting for a more comprehensive analysis of the underlying drivers of the rate movements we see here. If ever anyone has access to real interest rate data that go back several hundred years, please let me know (probably hard, or even impossible, to obtain as historical inflation data is likely to be non-existent).

In a parallel world, the BoE recently opened a forum weirdly titled ‘Building real markets for the good of the people’ which, putting aside the slightly communist tone of its chosen name, describes markets are “prone to excess” if “left unattended”**. This is another great example of central banks succeeding in making public opinion believe that economic issues originate, not in central bankers’ failed policies, not in economically distortive banking regulation, but in free markets. Which aren’t actually free. Here again Selgin had a remarkable article reporting how the Fed promotes itself.

One reaches some sort of supreme irony after contrasting those BoE statements with the charts above. Worse, central banks’ power, despite the instability they have brought to the economy for 100+ years, is growing, and their adherence to the rule of law has all but vanished (see Salter here and here arguing that a stable monetary framework such as the gold standard or NGDP targeting would respect the rule of law, unlike current regimes, and that adherence to the rule of law should be the primary consideration for judging monetary regimes).

*Sarcasm, of course

**I’m not sure what’s going on at the BoE, but a culture shift seems to be happening: anti-market rhetoric and rather strange monetary and banking theories are overtaking the institution (see my posts on endogenous money theory)

Natural interest rates are dead, the BIS (indirectly) says

In May (I only found out a couple of weeks ago), the BIS released a big report titled Regulatory change and monetary policy, in which it investigates the effects of the new banking regulatory framework on market interest rates and the implied consequences for the conduct of monetary policy. By the BIS’ own admission, the whole yield curve has nothing ‘natural’ left.

The report is an interesting, though pretty technical read. It is also scary. Scary to see how much banking regulation is affecting interest rates all along the yield curve across most banking products. Scary to see that the suggested remediation by the BIS is more central bank involvement to counteract the effects of those regulations.

Of course, the Basel framework originates from… Basel in Switzerland, where the BIS is located, and where BIS experts have spent years drafting apparently clever rules to make our banking system apparently safer, in spite of all historical evidences and what we’ve learned about the spontaneous order of free markets (remember: “banking is different” they say). So I wasn’t expecting this BIS report to declare that the very rules it put in place was endangering the economy. And indeed it doesn’t. But it does admit that there will be ‘impacts’, which of course will be ‘limited’ and ‘manageable’. They always are.

I won’t replicate here everything that’s in that report. It’s way too long and I’ll let you take a look at it if you’re interested. There is a quite detailed description of the potential effects of the Liquidity Coverage Ratio, the Net Stable Funding Ratio, the Leverage Ratio and the Large Exposure Limits on banks’ product pricing and volume and the impact on central bank’s monetary policy operations. And despite its 30+ pages, the report isn’t even comprehensive. It forgets to look at the large distortive effects of risk-weighted assets and credit conversation factors.

What I’m going to show you below is merely the BIS researchers’ own conclusions, which they neatly summarised in handy tables. This is what they view as the potential changes in money market interest rates:

By their own admission, the cumulative effect of those new rules is unclear. And even when they believe they know which way the interest rate will move, it remains a best guess. To this table you can add the hugely distortive effects of RWAs and CCFs, which I have described on this blog a number of times.

The only conclusion is that there is no free market-defined Wicksellian ‘natural’ interest rate anymore in the marketplace. As interest rates are manipulated by regulatory measures in myriads of ways, entire yield curves across the whole spectrum of banking products and asset classes stop reflecting the pricings that market actors would normally agree on in an unhampered market. The result is a large shift in the structure of relative prices in the economy.

The economic consequences are likely to be damaging (and it is clear, at least to me, that RWAs have already done a lot of damages, i.e. the financial crisis), even though the BIS reckons that central banks could potentially offset some of those interest rates movements:

More central bank intermediation: Many of the new regulations will increase the tendency of banks to take recourse to the central bank as an intermediary in financial markets – a trend that the central bank can either accommodate or resist. Weakened incentives for arbitrage and greater difficulty of forecasting the level of reserve balances, for example, may lead central banks to decide to interact with a wider set of counterparties or in a wider set of markets.

In addition, in a number of instances, the regulations treat transactions with the central bank more favourably than those with private counterparties. For example, Liquidity Coverage Ratio rollover rates on a maturing loan from a central bank, depending on the collateral provided, can be much higher than those for loans from private counterparties.

Problem is (and the BIS also admits it): there is no way non-omniscient central bankers know by how much and in what direction rates should be offset. We here get back again to the knowledge problem. There is no way the central bank can act in a timely manner. It is also unlikely that central bankers could act free from any political interference. Finally, even if central banks managed to figure out what the ‘natural’ rate is for a given asset at a given maturity, central banks’ policies are likely to have unintended consequences by altering the rates of other products and maturities.

The effectiveness of the transmission mechanism (banking channel) of monetary policy is more than ever questioned. Rates will move in unexpected ways. And, as the BIS describes, banks could simply opt out of monetary programmes altogether:

The question is whether there are exceptional situations in which banks would refrain from subscribing to fund-supplying operations because concerns over the LR impact of the reserves that would be added to the banking system in aggregate outweigh the financial benefits accrued by participating in the operations. If so, this lack of participation could prevent a central bank whose operating framework entailed increasing the quantity of reserves from meeting its operating target.

The BIS believes that “the changing regulatory environment will, by design, affect banks’ relative demand across various types of assets and liabilities”. It summarises the potential changes in the demand for central bank tools below:

Here again, a lot of uncertainties remain.

Something looks certain however. The involvement of central banks in the financial and economic system is likely to become more intense. As regulations bound banks’ behaviour and prevent an effective allocation of capital, central banks are increasingly going to step in to boost or restrict the supply of credit to certain market actors and asset classes. See what happened with SMEs, starved of credit as Basel makes it too expensive to extend credit to such customers, while central banks attempted to offset this effect by starting specific lending programmes (such as the Funding for Lending scheme in the UK). We are here again back to Jeff Hummel’s arguments of the central bank as central planner.

Nonetheless, I am certain that capitalism and free markets will get blamed for the next round of crisis. It is becoming urgent that we replicate the achievement of academics such as Friedman and Hayek, who managed to overturn the nonsense post-War Keynesian consensus. Sadly, free markets academics seem to have virtually disappeared nowadays or at least cut off from most policymaking positions and public debate.

Negative interest rates and free banking

Is the universe about to make a switch to antimatter? Interest rates in negative territory is the new normal. Among regions that introduced negative rates, most have only put them in place on deposit at the central bank (like the -0.2% at the ECB for instance). Sweden’s Riksbank is innovating with both deposit and repo rates in negative territory. It now both has to pay banks that borrow from it overnight and… charge commercial banks that deposit money with it, like a mirror image of the world we used to know. However, like antimatter and matter and the so-called CP violation (which describes why antimatter has pretty much disappeared from the universe), positive rates used to dominate the world. Until today.

Many of those monetary policy decisions seem to be taken in a vacuum: nobody seems to care that the banking regulation boom is not fully conductive to making the banking channel of monetary policy work (and bankers are attempting to point it out, but to no avail). In some countries, those decisions also seem to be based on the now heavily-criticised inflation target, as CPI inflation is low and central bankers try to avoid (whatever sort of) deflation like the plague.

As I described last year with German banks, negative rates have….negative effects on banks: it further amplifies the margin compression that banks already experience when interest rates are low by adding to their cost base, and destabilise banks’ funding structure by providing depositors a reason to withdraw, or transfer, their deposits. Some banks are now trying to charge some of their largest, or wealthiest, customers to offset that cost. At the end of the day, negative rates seem to slightly tighten monetary policy, as the central bank effectively removes cash from the system.

It is why I was delighted to read the below paragraphs in the Economist last week, a point that I have made numerous times (and also a point that many economists seem not to understand):

In fact, the downward march of nominal rates may actually impede lending. Some financial institutions must pay a fixed rate of interest on their liabilities even as the return on their assets shrivels. The Bank of England has expressed concerns about the effect of low interest rates on building societies, a type of mutually owned bank that is especially dependent on deposits. That makes it hard to reduce deposit rates below zero. But they have assets, like mortgages, with interest payments contractually linked to the central bank’s policy rate. Money-market funds, which invest in short-term debt, face similar problems, since they operate under rules that make it difficult to pay negative returns to investors. Weakened financial institutions, in turn, are not good at stoking economic growth.

Other worries are more practical. Some Danish financial firms have discovered that their computer systems literally cannot cope with negative rates, and have had to be reprogrammed. The tax code also assumes that rates are always positive.

In theory, most banks could weather negative rates by passing the costs on to their customers in some way. But in a competitive market, increasing fees is tricky. Danske Bank, Denmark’s biggest, is only charging negative rates to a small fraction of its biggest business clients. For the most part Danish banks seem to have decided to absorb the cost.

Small wonder, then, that negative rates do not seem to have achieved much. The outstanding stock of loans to non-financial companies in the euro zone fell by 0.5% in the six months after the ECB imposed negative rates. In Denmark, too, both the stock of loans and the average interest rate is little changed, according to data from Nordea, a bank. The only consolation is that the charges central banks levy on reserves are still relatively modest: by one estimate, Denmark’s negative rates, which were first imposed in 2012, have cost banks just 0.005% of their assets.

Additionally, a number of sovereign, and even corporate, bonds yields have fallen (sometimes just briefly) into negative territory, alarming many financial commentators and investors. The causes are unclear, but my guess is that what we are seeing is the combination of unconventional monetary policies (QE and negative rates) and artificially boosted demand due to banking regulation (and there is now some evidence for this view as Bloomberg reports that US banks now hoard $2Tr of low-risk bonds). Some others report that supply is also likely to shrink over the next few years, amplifying the movement. There are a few reasons why investors could still invest in such negative-yielding bonds however.

As Gavyn Davies points out, we are now more in unknown than in negative territory. Nobody really knows how low rates can drop and what happens as monetary policy (and, I should add, regulation) pushes the boundaries of economic theory. At what point, and when, will economic actors start reacting by inventing innovative low-cost ways to store cash? The convenience yield of holding cash in a bank account seems to be lower than previously estimated, although it is for now hard to precisely estimate it as only a tiny share of the population and corporations is subject to negative rates (banks absorb the rest of the cost). The real test for negative rates will occur once everyone is affected.

Free markets though can’t be held responsible for what we are witnessing today. As George Selgin rightly wrote in his post ‘We are all free banking theories now’, what we currently experience and the options we could possibly pick have to measure up against what would happen in a free banking framework.

Coincidentally, a while ago, JP Koning wrote a post attempting to describe how a free banking system could adapt to a negative interest rates environment. He argued that commercial banks faced with negative lending rates would have a few options to deal with the zero lower bound on deposit rates. He came up with three potential strategies (I’ll let you read his post for further details): remove cash from circulation by implementing ‘call’ features, cease conversion into base money, and penalize cash by imposing through various possible means what is effectively a negative interest rate on cash. I believe that, while his strategies sound possible in theory, it remains to be seen how easy they are to implement in practice, for the very reason that the Economist explains above: competitive forces.

But, more fundamentally, I think his assumptions are the main issue here. First, the historical track record seems to demonstrate that free banking systems are more stable and dampen economic and financial fluctuations. Consequently, a massive economic downturn would be unlikely to occur, possibly unless caused by a massive negative supply shock. Even then, the results in such economic system could be short-term inflation, maintaining nominal (if not real) interest rates in positive territory.

Second (and let’s leave my previous point aside), why would free banks lend at negative rates in the first place? This doesn’t seem to have ever happened in history (and surely pre-industrial rates of economic growth were not higher than they are now, i.e. ‘secular stagnation’) and runs counter to a number of theories of the rate of interest (time preference, liquidity preference, marginal productivity of capital, and their combinations). JPK’s (and many others’) reasoning that depositors wouldn’t accept to hold negative-yielding deposits for very long similarly applies to commercial banks’ lending.

Why would a bank drop its lending rate below zero? In the unrealistic case of a bank that does not have a legacy loan book, bankers would be faced by two options: lend the money at negative rates, during an economic crisis with all its associated heightened credit and liquidity risk, or keep all this zero-yielding cash on its balance sheet and make a loss equivalent to its operating costs. If a free bank is uncertain to be able to lower deposit rates below lending rates, better hold cash, make a loss for a little while, the time the economic crisis passes, and then increase rates again. This also makes sense in terms of competitive landscape. A bank that, unlike its competitors, decides to take a short-term loss without penalising the holders of its liabilities is likely to gain market shares in the bank notes (and deposits) market.

Now, in reality, banks do have a legacy loan book (i.e. ‘back book’) before the crisis strike, a share of which being denominated at fixed, positive, nominal interest rates. Unless all customers default, those loans will naturally shield the bank from having to take measures to lower lending rates. The bank could merely sit on its back book, generating positive interest income, and not reinvest the cash it gets from loan repayments. Profits would be low, if not negative, but it’s not the end of the world and would allow banks to support their brand and market share for the longer run*.

Finally, the very idea that lending rates (on new lending, i.e. ‘front book’) could be negative doesn’t seem to make sense. Even if we accept that the risk-free natural rate of interest could turn negative, once all customer-relevant premia are added (credit and liquidity**), the effective risk-adjusted lending rate is likely to be above the zero bound anyway. As the economic crisis strikes, commercial banks will naturally tend to increase those premia for all customers, even the least risky ones. Consequently, a bank that lent to a low-risk customer at 2% before the crisis, could well still lend to this same customer at 2% during the crisis (if not higher), despite the (supposed) fall of the risk-free natural rate.

I conclude that it is unlikely that a free banking system would ever have to push lending (or even deposit) rates in negative territories, and that this voodoo economics remains a creature of our central banking system.

*Refinancing remains an option for borrowers though. However, in crisis times, it’s likely that only the most creditworthy borrowers would be likely to refinance at reasonable rates (which, as described above, could indeed remain above zero)

**Remember this interest rate equation that I introduced in a very recent post:

Market rate = RFR + Inflation Premium + Credit Risk Premium + Liquidity Premium

Photo: MIT

Central banks don’t/do/don’t/do control interest rates

Ben Southwood and I agree on most things but a few topics. Whether central banks’ decisions affect interest rates is one of those, though I do think we have more common than we’re willing to admit. Here are the various reasons that convince me that central banks exert a relatively strong influence on most market rates.

On ASI’s blog, Ben wrote a piece about a 2013 research paper from Fama, who looked into interest rate time series to determine whether or not the Fed controlled interest rates. According to Ben’s own interpretation of the paper, the answer is ‘probably not’. Ironically, my take is completely different.

Throughout most of his paper, Fama’s results do indicate that the Fed exercises a relatively firm grip on all sorts of interest rates, as he admits it himself many times. For example, in his conclusion he writes:

A good way to test for Fed effects on open market interest rates is to examine the responses of rates to unexpected changes in the Fed’s target rate. Table 5 confirms that short-term rates (the one month commercial paper rate and three-month and six-month Treasury bill rates), respond to the unexpected part of changes in TF. Table 5 is the best evidence of Fed influence on rates, and event studies of this sort are center stage in the active Fed literature.

But I find Fama a little biased as he always tries to defend his original position that the Fed does not exert such a strong control:

But skeptics have a rejoinder. The response of short rates to unexpected changes in the Fed’s target rate might be a signaling effect. Rates adjust to unexpected changes in TF because the Fed is viewed as an informed agent that sets TF to line up with its forecasts of how market forces will shape open market rates.

Or also:

The Table 4 evidence that short-term interest rates forecast changes in the Fed funds target rate is not news (Hamilton and Jorda 2002). For those who believe in a powerful Fed, the driving force is TF, the concrete expression of Fed interest rate policy, and the forecast power of short rates simply says that rates adjust in advance to predictable changes in the Fed’s target rate. (See, for example, Taylor 2001.) The evidence is, however, also quite consistent with a passive Fed that changes TF in response to open market interest rates. There are, of course, scenarios in which both forces are at work, possibly to different extents at different times. The Fed may go passive and let the market dictate changes in TF when inflation and real activity are satisfactory, but turn active when it is dissatisfied with the path of inflation or real activity. This mixed story is also consistent with the evidence in Table 3 that the Fed funds rate moves toward both the open market commercial paper rate and the Fed’s target rate.

However Fama never explains why the Fed would simply passively change its base rate in response to private markets. This seems to defeat the purpose of having an active monetary policy.

In short, most of the evidences that Fama finds seem to demonstrate that the Fed indeed does control most interest rates to an extent (in particular short-term ones). But he does not seem to accept his own result and tries to come up with alternative explanations that are less than convincing, to say the least. He concludes by basically saying that…we cannot come to a conclusion.

But Fama’s paper suffers from a major flaw. Let’s break down a market interest rate here:

Market rate = RFR + Inflation Premium + Credit Risk Premium + Liquidity Premium

Fama’s dataset wrongly runs regressions between Fed’s base rate movements and observable market yields on some securities. The rate that the Fed influences is the risk free rate (RFR). But as seen above, market rates contain a number of premia that vary with economic conditions and the type of security/lending and on which the Fed has limited control.

For instance, when a crisis strikes, the credit risk premium is likely to jump. In response, the Fed is likely to cut its base rate, meaning the RFR declines. But the observable rate does not necessarily follow the Fed movement. It all depends on the amplitude of the variation in each variable of the equation above. Hence the correlation will only provide adequate results if the economic conditions are stable, with no expected change in inflation or credit risk. Does this imply that the Fed has no control over the interest rate? Surely not, as the RFR it defines is factored in all other rates. In the example above, the market rates ends up lower than it would have normally been if fully set by private markets.

David Beckworth had a couple of interesting charts on its blog, which attempted to strip out premia from the 10-year Treasury yield (it’s not fully accurate but better than nothing):

Now compare the 1990-2014 non-adjusted and adjusted 10-year Treasury yield with the evolution of the Fed base rate below:

The shapes of the adjusted 10-year yield and the Fed funds rate curves are remarkably similar, whereas this isn’t the case for the unadjusted yield*. Yet most of Fama’s argument about the Fed having a limited influence on long-term rates rests on his interpretation of the evolution of the spread between the Fed funds target rate and the unadjusted 10-year yield.

(the same reasoning applies to commercial paper spread, though the inflation premium is close to nil in such case)

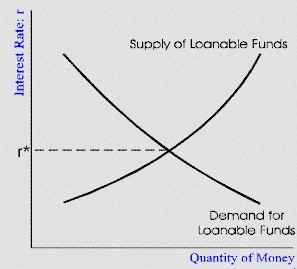

Second, I find it hard to understand Ben’s point that markets set rates, when central banks’ role is indeed to define monetary policies and, by definition, impact those market rates. If only markets set rates, then surely it is completely pointless to have central banks that attempt to control monetary policies through various tools, including the control on the quantity of high-powered money. In a simple loanable funds model (let’s leave aside the banking transmission mechanism), in which the interest rate is defined by the equilibrium point between supply and demand for loanable funds, it is quite obvious that a central bank injecting, or removing, base money from the system (that is, pushing the supply curve one way or another) will affect the equilibrium rate. Of course the central bank does not control the demand curve. But the fact that the bank does not have a total control over the interest rate does not imply that it has none and that its policies have no effect. What does count is that the resulting equilibrium rate differs from the outcome that free markets would have produced.

I am also trying to get my head around what I perceive as a contradiction here (I might be wrong). Market monetarists (of whom Ben seems to belong) believe that money has been ‘tight’ throughout the recession due to central banks’ misguided monetary policies. They seem to think that rates would have dropped much faster in a free market. This seems to demonstrate that market monetarist believe in the strong influence of central banks on many rates. But according to Ben, central banks do not have much influence on rates. Does he imply that free markets were responsible for the ‘tight’ policy that followed the crisis?

So far in this post we’ve only seen cases in which the central bank indirectly affects market rates. But some markets are linked to the central bank base rate from inception. For instance, in the UK, most mortgage rates (‘standard variable rates’) are explicitly and contractually defined as ‘BoE Base Rate + Margin’**. The margin rarely changes after the contract has been agreed. Any change in the BoE rate ends up being automatically reflected in the rate borrowers have to pay (that is, before banks are all forced to widen the contract margin because of the margin compression phenomenon, as I described in my previous exchange with Ben here and here). The only effect of banking competition is to lead to fluctuations of a few bp up or down on newly originated mortgages (i.e. one bank offers you BoE + 1.5% and another one BoE + 1.3%).

At the end of the day, I have the impression that a part of our disagreement is merely due to semantics. I don’t think anybody has declared that central banks fully control rates. This would be foolish. But they certainly exert a strong influence (at least) through the risk-free rate, and this reflects on all other rates across maturities and risk profiles.

*To be fair, it does look like some of the Fed’s decisions were anticipated by markets and reflected in Treasury yields just before the target rate was changed.

**In some other countries the link is looser, as the central bank rate is replaced by the local interbank lending rate (Libor, Euribor…).

Easy money is secondary to bank regulation in triggering housing booms

I’ve already reported on the excellent piece of research that Jordà et al published last year. Last month, they elaborated on their previous research to publish another good paper, titled Betting the House. While their previous paper focused on gathering and aggregating real estate and business lending data across most major economies since the second half of the 19th century, their new paper built on this great database to try to extract correlations between ‘easy’ monetary conditions and housing bubbles.

Remember their remarkable chart, to which I had added Basel and trend lines:

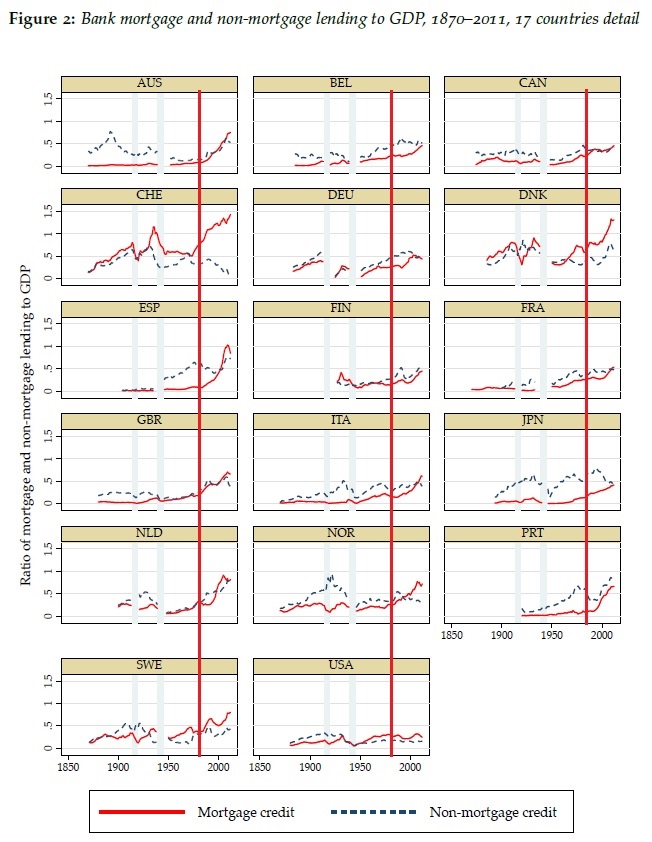

They also produced the following chart, which shows disaggregated data across countries (click on it to zoom in). I added red vertical bars that show the introduction of Basel 1 regulations (roughly… it’s not very precise). What’s striking is that, almost everywhere, mortgage debt boomed as a share of GDP and overtook business lending. It was a simultaneous paradigm change that can hardly be separated from the major changes in banking regulation and supervision that occurred at that time.

They also produced the following chart, which shows disaggregated data across countries (click on it to zoom in). I added red vertical bars that show the introduction of Basel 1 regulations (roughly… it’s not very precise). What’s striking is that, almost everywhere, mortgage debt boomed as a share of GDP and overtook business lending. It was a simultaneous paradigm change that can hardly be separated from the major changes in banking regulation and supervision that occurred at that time.

Their new study repeats most of what had been said in their previous one (i.e. that mortgage credit had been the primary driver of post-WW2 bank lending) and then compares real estate lending cycles with monetary policy. And they conclude that:

Their new study repeats most of what had been said in their previous one (i.e. that mortgage credit had been the primary driver of post-WW2 bank lending) and then compares real estate lending cycles with monetary policy. And they conclude that:

loose monetary conditions lead to booms in real estate lending and house prices bubbles; these, in turn, materially heighten the risk of financial crises. Both effects have become stronger in the postwar era.

As I said in my post on Jordà et al’s previous research, most (if not all) of what they identify as post-WW2 housing cycles actually happened post-Basel implementation. I wish they had differentiated pre- and post-Basel cycles.

They start by assessing the stance of monetary policy in the Eurozone over the past 15 years, using the Taylor rule as an indicator of easy/tight monetary policy. While the Taylor rule is possibly not fully adequate to measure the natural rate of interest, it remains better than the simplistic reasoning that low rates equal ‘easy’ money and high rates equal ‘tight’ money. According to their Taylor rule calculation, the stance of monetary policy in the Eurozone before the crisis was too tight in Germany and too loose in Ireland and Spain. In turn they say, this correlated well with booms in mortgage lending and house prices (see chart below).

At first sight, this seems to confirm the insight provided by the Austrian business cycle theory: Spain and Ireland benefited from interest rates that were lower than their domestic natural rates, launching a boom/bust cycle driven by the housing market. (While Germany was the ‘sick’ man of Europe as the ECB policy was too tight in its case)

At first sight, this seems to confirm the insight provided by the Austrian business cycle theory: Spain and Ireland benefited from interest rates that were lower than their domestic natural rates, launching a boom/bust cycle driven by the housing market. (While Germany was the ‘sick’ man of Europe as the ECB policy was too tight in its case)

And while this is probably right, this is far from being the whole story. In fact, I would say that ‘easy’ monetary policy is only secondary to banking regulation in causing financial crises through real estate booms. As I have attempted to describe a little more technically here, Basel reorganised the allocation of loanable funds towards real estate, at the expense of business lending. This effectively lowered the market rate of interest on real estate lending below its natural rate, triggering the unsustainable housing cycle, and preventing a number of corporations to access funds to grow their business. By itself, Basel causes the discoordination in the market for loanable funds: usage of the newly extended credit does not reflect the real intertemporal preference of the population. No need for any central bank action.

What ‘easy’ monetary policy does is to amplify the downward movement of interest rates, boosting real estate lending further. But it is not the initial cause. In a world without Basel rules, the real estate boom would certainly have occurred in those proportions, and quick lending growth would have been witnessed across sectors and asset classes. The disproportion between real estate and business lending in the pre-crisis years suggests otherwise.

* They continue by building a model that tries to identify the stance of monetary policy throughout the more complex pre-WW2 and pre-1971 monetary arrangements. I cannot guarantee the accuracy of their model (I haven’t spent that much time on their paper) but as described above, everything changed from the 1980s onward anyway.

PS: The ‘RWA-based ABCT’ that I described above is one of the reasons why I recently wrote a post arguing that the original ABCT needed new research to be adapted to our modern financial system and be of interest to policymakers and the wider public.

Why can’t economists understand margin compression?

Are basic accounting statements so difficult to interpret? According to Viennacapitalist, who commented on my previous post, it does seem so. At least for macroeconomists. Indeed, Werner seemed to imply that most economists did not know that deposits sat on the liability side of a bank’s balance sheet (he’s surely wrong), and I have many times pointed out the central bankers’ and policymakers’ misunderstanding of banking mechanics.

Three researchers from the BIS just confirmed the trend. In a new working paper called ‘Has the transmission of policy rates to lending rates been impaired by the Global Financial Crisis?’, they wonder, and try to find out, why spreads between central banks’ base rates and lending rates have jumped once base rates reached the zero-lower bound.

It’s a debate I’ve already had almost a year ago, when I tried to explain that, due to the margin compression effect (an accounting phenomenon), spreads would have to increase in order allow banks to generate sufficient earnings to report (at least) positive accounting net incomes (see here and here).

Those BIS researchers have come up with the same sort of dataset and charts I did over the past year, although they also looked at the US (but didn’t look as other European countries, unlike what I did in this post). This is what they got:

This looks very very similar to my own charts. Clearly, spreads jumped across the board: pre-crisis, they were around 1.5% in the US, 1.5% in the UK and 1.25/1.5% in Spain and Italy. In 2009/2010, with base rate dropping to the zero-lower bound, things changed completely: spreads were of 3% in the US, 2.25% in the UK, 2% in Spain and 1.5% in Italy. Rates had not dropped as much as base rates. Worse, spreads on average increased afterwards: by 2013, spreads were around 2.5% in all countries.

This looks very very similar to my own charts. Clearly, spreads jumped across the board: pre-crisis, they were around 1.5% in the US, 1.5% in the UK and 1.25/1.5% in Spain and Italy. In 2009/2010, with base rate dropping to the zero-lower bound, things changed completely: spreads were of 3% in the US, 2.25% in the UK, 2% in Spain and 1.5% in Italy. Rates had not dropped as much as base rates. Worse, spreads on average increased afterwards: by 2013, spreads were around 2.5% in all countries.

The BIS researchers tried to understand why. Unfortunately, they focused on the wrong factors. They built a model that concluded that the “less pass-through seems to be related in part to higher premium for risk required by banks and by worsening of their financial conditions as well.” They are probably right that some of these factors did play a role. But they cannot explain why the spread remains so elevated even in economies that have experienced strong recoveries such as the US or, more recently the UK.

But their study also has a number of other problems. First, they used new lending data only. It is extremely tricky to extract credit risk information from new lending rate figures. Why? Because new lending rates only show credit actually extended. Many borrowers cannot access credit altogether or simply refuse to do so at high rates. Consequently, the figures could well only reflect borrowers that have relatively good credit risk in the first place as banks try to eliminate credit risk from their portfolio. Second, they never ever discuss operating costs and margin compression, as if banks could simply lower interest income to close to 0 and get away with it.

But for this, they should have looked at two things: deposit rates and banks’ back books (i.e. legacy lending). Not new lending only. When the margin between deposit rates and lending rates on back books fall below banks’ operating costs, banks have to offset that decline by increasing spreads. This is why I suggested that the actual lowering base rates ceased to be effective from around 1.5 to 2% downward as a means of reducing household and companies’ borrowing rates.

Problem is, very few researchers and policymakers seem to get it. Patrick Honohan, of the Irish Central Bank, and Benoit Coeuré, of the ECB, do seem to understand what the issue is. Bankers and consultants have for a while (see Deloitte at the end of this post). Some economic commentators assert that it is hard to figure out why bankers keep complaining about low rates. This dichotomy between theorists and practitioners is leading to misguided, and potentially harmful, policies.

But let me ask a simple question. How hard is it to understand bank accounting really?

The mystery of collateral

Collateral has been the new fashionable area of finance and capital markets research over the past few years. Collateral and its associated transactions have been blamed for all the ills of the crisis, from runs on banks’ short-term wholesale funding to a scarcity of safe assets preventing an appropriate recovery. Some financial journalists have jumped on the bandwagon: everything is now seen through a ‘collateral lens’. The words ‘assets’, and, to a lesser extent ‘liquidity’ and ‘money’ themselves, have lost their meaning: all are now being replaced by ‘collateral’, or used interchangeably, by people who don’t seem to understand the differences.

A few researchers are the root cause. The work of Singh keeps referring to any sort of asset transfer between two parties as ‘collateral transfer’. This is wrong. Assets are assets. Securities are securities, a subset of assets. Collateral can be any type of assets, if designated and pledged as such to secure a lending or derivative transaction. Real estate, commodities and Treasuries can all be used as collateral. Money too. Unlike what Singh and his followers claim, a securities lender lends a security not a collateral. Whether or not this security is used as collateral in further transactions is an independent event.

This unfortunate vocabulary problem has led to perverse ramifications: all liquid assets, or, as they often say, collateral, are now seen as new forms of money (see chart below, from this paper). Specifically, collateral becomes “the money of the shadow banking system”. I believe this is incorrect. Collateral is used by shadow banks to get hold of money proper. Building on this line of reasoning, people like Pozsar assert that repo transactions are money… This makes even less sense. Repos simply are collateralised lending transactions. Nobody exchanges repos. The assets swapped through a repo (money and securities) could however be exchanged further. Depressingly, this view is taken increasingly seriously. As this recent post by Frances Coppola demonstrates, all assets seem now to be considered as money. This view is wrong in many ways, but I am ready to reconsider my position if ever Treasuries or RMBSs start being accepted as media of exchange at Walmart, or between Aston Martin and its suppliers. Others have completely misunderstood the differences between loan collateralisation and loan funding, which is at the heart of the issue: you don’t fund a loan, whether in the light or the dark side of the banking system, with collateral! The monetary base/high-powered money/cash/currency, is the only medium of settlement, the only asset that qualifies as a generally-accepted medium of exchange, store of value and unit of account (the traditional definition of money).

There is one exception though. Some particular transactions involve, not a non-money asset for money swap, but non-money asset for another non-money asset swap. This is almost a barter-like transaction, which does occur from time to time in securities lending activities (the lender lends a security for a given maturity, and the borrower pledges another security as collateral). Nonetheless, the accounting (including haircuts and interest calculations) in such circumstances is still being made through the use of market prices defined in terms of the monetary base.

Still, collateral seems to have some mysterious properties and Singh’s work offers some interesting insights into this peculiar world. The evolution of the collateral market might well have very deep effects on the economy. The facilitation of collateral use and rehypothecation, as well as the requirements to use them, either through specific regulatory and contractual frameworks, through the spread of new technology, new accounting rules or simply through the increased abundance of ‘safe assets’ (i.e. increased sovereign debt issuance), might well play a role in business cycles, via the interest rate channel. Indeed, by facilitating or requiring the use of increasingly abundant collateral, interest rates tend to fall. The concept of collateral velocity is in itself valuable: when velocity increases, interest rates tend to fall further as more transactions are executed on a secured basis. Still, are those transactions, and the resulting fall in interest rates, legitimate from an economic point of view? What are the possible effects on the generation of malinvestments?

An example: let’s imagine that a legal framework clarification or modification, and/or regulatory change, increases the use and velocity of safe collateral (government debt). New technological improvements also facilitate the accounting, transfer, and controlling processes of collateral. This increases the demand for government debt, which depresses its yield. Motivated by lower yield, the government indeed issues more debt that flow through financial markets. As the newly-enabled average velocity of collateral increases substantially, more leveraged secured transactions take place and at lower interest rates. While banks still have exogenous limits to credit expansion (as the monetary base is controlled by the central bank), the price of credit (i.e. endogenous money creation) has therefore decreased as a result of a mere regulatory/legal/technological change.

I have been wondering for a while whether or not such a change in the regulatory paradigm of collateral use could actually trigger an Austrian-type business cycle. I do not yet have an answer. Implications seem to be both economic and philosophical. What are the limits to property rights transfer? How would a fully laisse-faire market deal with collateral and react to such technological changes? Perhaps collateral has no real influence on business fluctuations after all. There is nevertheless merit in investigating further. I am likely to explore the collateral topic over the next few months.

PS: I will be travelling in North America over the next 10 days, so might not update this blog much.

* There are many many flaws in Frances’ piece. See this one:

But suppose that instead of a sterling bank account, a smartcard or a smartphone app enabled me to pay a bill in Euros directly from my holdings of UK gilts? This is not as unlikely as it sounds. It would actually be two transactions – a sale of gilts for sterling and a GBPEUR exchange. This pair of transactions in today’s liquid markets could be done instantaneously. I would in effect have paid for my meal with UK government debt.

She fails to see that she would have paid for her mean with Sterling, not with government debt! Government debt must be converted into currency as it is not a medium of exchange/settlement.

{kind=link}

{kind=link}

Recent Comments