Will Switzerland reveal the lower bound?

Given that a number of central banks have moved some of their monetary policy tools into negative territory for the first time in their history, many people have questioned the assumption that the zero lower bound is effectively the lower bound that conventional economic theory describes. However, most economists do think that the lower bound exists; it is simply negative (as storing cash also involves a cost) and nobody really knows what its precise level is.

Hence the interesting experiment now happening in Switzerland, which seems to provide us with some indications. The SNB target range has now been in negative territory for a little while, and demand deposits at the central bank are currently charged a negative rate of 0.75%:

This is causing some issues for Swiss banks, in particular those that don’t have any international presence. SNL (link) reports that overall Swiss net interest income is declining by 6% this year and net interest margin is down from 1.8% in 2007 to less than 1.3% in 2014. Including the two largest and international Swiss lenders, NIM drops to 60pb, lower than in Japan. Between 2013 and 2015, NIM is forecasted to fall by 11%. Unsurprisingly, profitability is low. Add the harsh Swiss banking regulation and SNL now calls Swiss banks ‘low-return low-risk utilities’. This is a typical effect of the margin compression effect I keep mentioning on this blog.

Evidently, many Swiss banks are private entities that don’t really enjoy this situation. First, despite the lowest interest rates ever, banks have increased rates on mortgages; a phenomenon I had predicted in a margin compression period (see my discussion with Ben Southwood, who believes that competitive pressure cannot allow banks to raise rates). Second, a number of Swiss banks have been charging negative rates on large corporate deposits for several months already. Recently. a small Swiss bank revealed it would charge 0.125% on slightly less than a third of its clients’ accounts.

SNL reports that a large pension fund attempted to withdraw physical cash earlier in the year. Attempt that failed. But there is apparently growing demand for safe deposit boxes in the country, although demand remains limited as negative rates are only charged on corporate, and now some large retail, deposits.

While those are early signs, they remain important signs that we are getting closer to the actual lower bound. Various types of customers can also have different lower bound tolerance, and small retail depositors, for now unconcerned by negative rates, may be less tolerant of such charges. Once negative rates generalise, we’ll find out how deep the lower bound really is.

Central bankers, who believe they can stabilise the economy by imposing negative rates, might well endanger it in reality. If negative rates generalise, the banking sector will be weakened: not only its profitability will get depressed (and you need a healthy banking system to extend credit for productive purposes), but also its funding structure will become much more unstable. Indeed, depositors will be more likely to withdraw their deposits and avoid getting locked in longer maturity saving products, exacerbating banks’ maturity mismatches. Eventually, the net effect of negative rates might not be that positive.

PS: I’d like to know what the proponents of ‘the Wicksellian natural rate of interest is negative because of our depressed economy’ think in the case of Switzerland. Its economy doesn’t look particularly under stress, yet it is imposed negative rates by its central bank to control FX fluctuations. George Selgin also has a nice post on deflation in Switzerland, which, unlike conventional wisdom, doesn’t seem to be damaging.

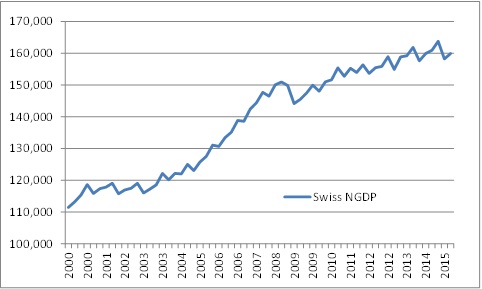

This is the quarterly Swiss NGDP since 2000, extracted from the SNB website:

Note that the post-crisis NGDP trend has not caught up with pre-crisis trend. Very far from that (also note that the growth trend changed twice over the past 15 years). I suspect that some would advocate a much larger SNB stimulus to cause inflation to get NGDP back on track (but on which track?). Despite this ‘output gap’, the Swiss economy seems to be relatively healthy, at least for European standards.

PPS: an analyst, interviewed by SNL on the topic of the abolition of cash cherished by Kimball or Buiter, perfectly answered:

“That,” said Maier, “would be my definition of hell.”

7 responses to “Will Switzerland reveal the lower bound?”

Leave a comment

Recent Comments

| pslebow on ‘Sovereign money’:… | |

| pslebow on A critique of Werner’s view on… | |

| Hugo Kramer on Welcome to Spontaneous Fi… | |

| Nathan on A critique of Werner’s view on… | |

| Nathan on More, more, more money endogen… |

I think Lars Christensen had an interesting post on Swiss monetary policy a couple of years ago where he suggested the SNB has been implicitly targeting the level of Nominal Gross Domestic Demand (which he thought was more appropriate for a small open economy):

It would be interesting to see how well this has held up since then.

Thanks Andrew.

My problem with Lars’s post is that his ‘trend’ seems to be picked to match his argument.

Start the ‘trend’ in 2002 or at some other point and it doesn’t look at all the same.

This is one of my issues with NGDP targeting. US NGDP growth trend is often measured from the early 2000s and this shows a drop from 2009. But things look also very different if the trend starting point is taken earlier.

As for Lars’ post, even using his trend line the SNB significantly undershot then significantly overshot the trend for many years in a row in both cases.

Good point, the decision of what to consider “the” trend is rather arbitrary. Still Lars ranks high among Market Monetarists in my opinion for being very supportive of free banking, so I thought it was interesting that he thought the Swiss have relatively good monetary policy. Their experience with Good Deflation is very promising if it is allowed to continue.

You don’t need to look for anecdotal evidence of the effective lower bound. Just download the SNB’s monthly cash-outstanding data series. If it is showing trend growth, then the ELB hasn’t been hit. If it is accelerating, the ELB has been encountered. When I checked last month, cash was not yet showing above trend growth.

Sorry for the late reply JP. Too busy at the moment…

You’re right.

However, I don’t think trend would change as long as retail clients haven’t been hit. And now some are starting to be.

Also, we need to have access to a breakdown of cash in circulation to make sure. For example, a share of cash in circulation is held by banks. But if customers withdraw some of their cash and place it in safe boxes, aggregate cash in circulation does not necessarily increase; what may decrease is the amount of physical cash held by banks.

But it’s very hard to get that sort of data, either from monetary authorities or from banks’ financial reporting.

This problem with the narrowing of the NIM can be solved if central banks lend money to banks at negative rate, higher than the deposit rate, right?

achilleas,

In principle, yes. But in reality, it would involve massive sums of money lent by the CB, way above what the CB funding that is currently utilised by banks. And banks try to avoid to use CB lending facilities for funding in order to avoid the stigma associated to it.