TLTRO, a predictable failure

Almost a year and a half ago, I predicted the failure of the ECB’s TLTRO measure:

Finally, the ECB has launched its own-FLS style ‘TLTRO’, a scheme that provides cheap funding to banks if they channel the funds to businesses. Similarly to the BoE’s FLS, I believe such scheme suffers from delusion. Banks are currently deleveraging to lower their RWAs in order to comply with the harsher capital requirements of Basel 3. If there is one thing banks want to avoid, it is to lend to RWA-dense customers such as SMEs… (and instead focus on better RWA/risk-adjusted profitable lending such as… mortgages). Banks can also already extract relatively low wholesale funding rates by issuing secured funding instruments such as covered bonds.

Now Fitch, the rating agency, just published a piece confirming that the TLTRO effects were ‘modest’ at best. I don’t have access to their whole report, but the FT, commenting on the same piece of research, reported that:

A total of €400bn has been injected into the banking system through five TLTRO auctions since September 2014, with demand predominantly from Spanish and Italian institutions. By contrast, bank corporate lending grew by just €4bn between September 2014 and August 2015.

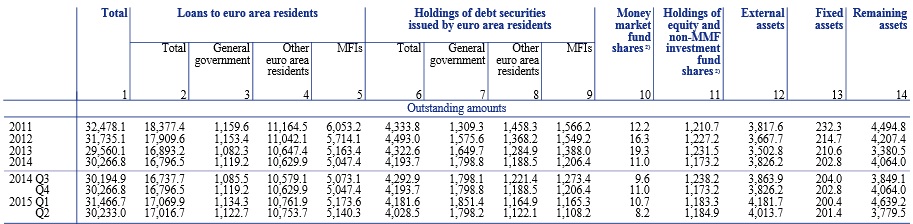

Now compares this €4bn with stats from the ECB (see table below) that show that total lending grew by €279bn in the Eurozone over the same time period, of which €175bn was extended to non-financial private individuals and businesses.

Fitch reports that corporate lending grew in a few northern European countries, and that lack of demand is likely a cause of the slow lending growth across most Eurozone countries. While there is definitely some truth to this, we have to keep in mind that the causation in this case may well go the other way around: demand may be low because rates on business loans are too high to justify borrowing.

TLTRO (as well as the British FLS) is a prime example of how deluded central bankers and policymakers are if they expect monetary policy and unconventional bank funding measures to bypass the negative effects that banking regulation has at the microeconomic level on the banking channel of monetary policy. Throw in as much stimulus as you wish, the money will always flow towards points of the economic system where micro resistance is the weakest. And, that is, money will flow to low-RWA asset classes (ahem…mortgages…ahem).

PS: I really have little time for blogging at the moment. Doing what I can to post updates!

Recent Comments