TLTRO, a predictable failure

Almost a year and a half ago, I predicted the failure of the ECB’s TLTRO measure:

Finally, the ECB has launched its own-FLS style ‘TLTRO’, a scheme that provides cheap funding to banks if they channel the funds to businesses. Similarly to the BoE’s FLS, I believe such scheme suffers from delusion. Banks are currently deleveraging to lower their RWAs in order to comply with the harsher capital requirements of Basel 3. If there is one thing banks want to avoid, it is to lend to RWA-dense customers such as SMEs… (and instead focus on better RWA/risk-adjusted profitable lending such as… mortgages). Banks can also already extract relatively low wholesale funding rates by issuing secured funding instruments such as covered bonds.

Now Fitch, the rating agency, just published a piece confirming that the TLTRO effects were ‘modest’ at best. I don’t have access to their whole report, but the FT, commenting on the same piece of research, reported that:

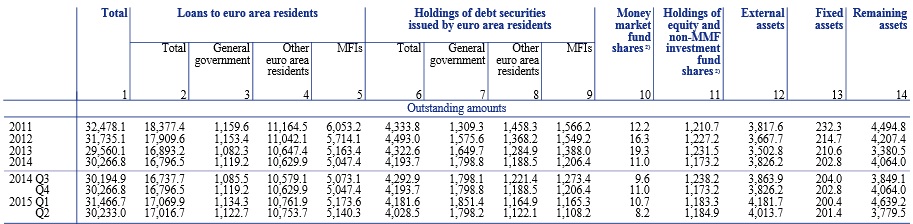

A total of €400bn has been injected into the banking system through five TLTRO auctions since September 2014, with demand predominantly from Spanish and Italian institutions. By contrast, bank corporate lending grew by just €4bn between September 2014 and August 2015.

Now compares this €4bn with stats from the ECB (see table below) that show that total lending grew by €279bn in the Eurozone over the same time period, of which €175bn was extended to non-financial private individuals and businesses.

Fitch reports that corporate lending grew in a few northern European countries, and that lack of demand is likely a cause of the slow lending growth across most Eurozone countries. While there is definitely some truth to this, we have to keep in mind that the causation in this case may well go the other way around: demand may be low because rates on business loans are too high to justify borrowing.

TLTRO (as well as the British FLS) is a prime example of how deluded central bankers and policymakers are if they expect monetary policy and unconventional bank funding measures to bypass the negative effects that banking regulation has at the microeconomic level on the banking channel of monetary policy. Throw in as much stimulus as you wish, the money will always flow towards points of the economic system where micro resistance is the weakest. And, that is, money will flow to low-RWA asset classes (ahem…mortgages…ahem).

PS: I really have little time for blogging at the moment. Doing what I can to post updates!

Easy money is secondary to bank regulation in triggering housing booms

I’ve already reported on the excellent piece of research that Jordà et al published last year. Last month, they elaborated on their previous research to publish another good paper, titled Betting the House. While their previous paper focused on gathering and aggregating real estate and business lending data across most major economies since the second half of the 19th century, their new paper built on this great database to try to extract correlations between ‘easy’ monetary conditions and housing bubbles.

Remember their remarkable chart, to which I had added Basel and trend lines:

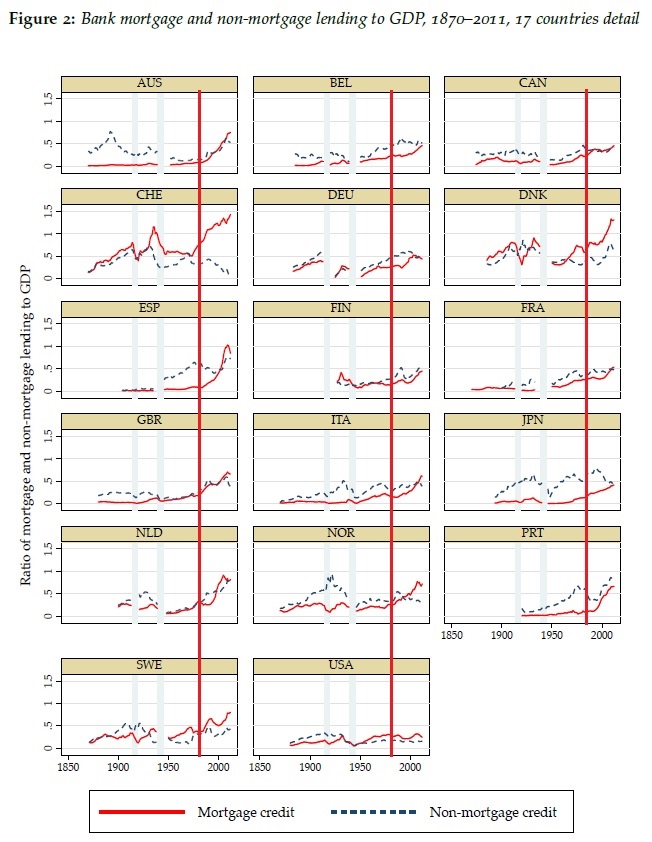

They also produced the following chart, which shows disaggregated data across countries (click on it to zoom in). I added red vertical bars that show the introduction of Basel 1 regulations (roughly… it’s not very precise). What’s striking is that, almost everywhere, mortgage debt boomed as a share of GDP and overtook business lending. It was a simultaneous paradigm change that can hardly be separated from the major changes in banking regulation and supervision that occurred at that time.

They also produced the following chart, which shows disaggregated data across countries (click on it to zoom in). I added red vertical bars that show the introduction of Basel 1 regulations (roughly… it’s not very precise). What’s striking is that, almost everywhere, mortgage debt boomed as a share of GDP and overtook business lending. It was a simultaneous paradigm change that can hardly be separated from the major changes in banking regulation and supervision that occurred at that time.

Their new study repeats most of what had been said in their previous one (i.e. that mortgage credit had been the primary driver of post-WW2 bank lending) and then compares real estate lending cycles with monetary policy. And they conclude that:

Their new study repeats most of what had been said in their previous one (i.e. that mortgage credit had been the primary driver of post-WW2 bank lending) and then compares real estate lending cycles with monetary policy. And they conclude that:

loose monetary conditions lead to booms in real estate lending and house prices bubbles; these, in turn, materially heighten the risk of financial crises. Both effects have become stronger in the postwar era.

As I said in my post on Jordà et al’s previous research, most (if not all) of what they identify as post-WW2 housing cycles actually happened post-Basel implementation. I wish they had differentiated pre- and post-Basel cycles.

They start by assessing the stance of monetary policy in the Eurozone over the past 15 years, using the Taylor rule as an indicator of easy/tight monetary policy. While the Taylor rule is possibly not fully adequate to measure the natural rate of interest, it remains better than the simplistic reasoning that low rates equal ‘easy’ money and high rates equal ‘tight’ money. According to their Taylor rule calculation, the stance of monetary policy in the Eurozone before the crisis was too tight in Germany and too loose in Ireland and Spain. In turn they say, this correlated well with booms in mortgage lending and house prices (see chart below).

At first sight, this seems to confirm the insight provided by the Austrian business cycle theory: Spain and Ireland benefited from interest rates that were lower than their domestic natural rates, launching a boom/bust cycle driven by the housing market. (While Germany was the ‘sick’ man of Europe as the ECB policy was too tight in its case)

At first sight, this seems to confirm the insight provided by the Austrian business cycle theory: Spain and Ireland benefited from interest rates that were lower than their domestic natural rates, launching a boom/bust cycle driven by the housing market. (While Germany was the ‘sick’ man of Europe as the ECB policy was too tight in its case)

And while this is probably right, this is far from being the whole story. In fact, I would say that ‘easy’ monetary policy is only secondary to banking regulation in causing financial crises through real estate booms. As I have attempted to describe a little more technically here, Basel reorganised the allocation of loanable funds towards real estate, at the expense of business lending. This effectively lowered the market rate of interest on real estate lending below its natural rate, triggering the unsustainable housing cycle, and preventing a number of corporations to access funds to grow their business. By itself, Basel causes the discoordination in the market for loanable funds: usage of the newly extended credit does not reflect the real intertemporal preference of the population. No need for any central bank action.

What ‘easy’ monetary policy does is to amplify the downward movement of interest rates, boosting real estate lending further. But it is not the initial cause. In a world without Basel rules, the real estate boom would certainly have occurred in those proportions, and quick lending growth would have been witnessed across sectors and asset classes. The disproportion between real estate and business lending in the pre-crisis years suggests otherwise.

* They continue by building a model that tries to identify the stance of monetary policy throughout the more complex pre-WW2 and pre-1971 monetary arrangements. I cannot guarantee the accuracy of their model (I haven’t spent that much time on their paper) but as described above, everything changed from the 1980s onward anyway.

PS: The ‘RWA-based ABCT’ that I described above is one of the reasons why I recently wrote a post arguing that the original ABCT needed new research to be adapted to our modern financial system and be of interest to policymakers and the wider public.

EU banking dis-union

The EU wants to put in place its now famous banking union. The ECB is taking over as the single regulator of all the banks of the Eurozone (and countries that wish to participate). The rationale is that the Eurozone banking system is getting ever more integrated within the ‘single market’, hence justifying having a single ruleset and a single supervisor. But is it really?

In a recent speech, Andrew Haldane pointed out that cross-border banking claims had strongly declined since the crisis:

But a new paper by Bouvatier and Delatte (full version here) now provides some interesting disagregated data to this trend. Controlling for the impact of the economic and financial crisis on the integration of the banking system across Eurozone countries, they conclude that

the decline in banking activities observed after the crisis was due to temporary frictions in all countries outside the euro area. In contrast, the economic downturn faced by the euro area since 2008 is not sufficient to account for the massive retrenchement of international banking activities. Euro area banks have reduced their international exposure inside and outside the euro area to a similar extent. We also find that this decline is not a correction of previous overshooting but a marked disintegration.

According to their model, Eurozone banking integration is 37% below where it should be. So much for a banking union. On the other hand, they find that non-Eurozone banking systems have increased their claims on foreign countries.

This is very interesting. However, I believe two minor issues distort some of their conclusions: 1. Their sample of banks only consider 14 OECD countries. It would have been interesting to include emerging economies. 2. Their analysis stops in 2012, which is a flaw. Since then, many non-Eurozone banks have cut in their cross-border activities as complying with the increasing regulatory burden became too onerous. I actually suspect that most banks from OECD/developed countries have started to dis-integrate, whereas banks from a number of emerging economies have actually started to grow outside of their domestic borders*.

This is very interesting. However, I believe two minor issues distort some of their conclusions: 1. Their sample of banks only consider 14 OECD countries. It would have been interesting to include emerging economies. 2. Their analysis stops in 2012, which is a flaw. Since then, many non-Eurozone banks have cut in their cross-border activities as complying with the increasing regulatory burden became too onerous. I actually suspect that most banks from OECD/developed countries have started to dis-integrate, whereas banks from a number of emerging economies have actually started to grow outside of their domestic borders*.

They do not provide the reasons behind this phenomenon. However, I believe that regulatory and political pressure is the number 1 reason behind this retrenchment. In their haste to make banks safe, regulators are actually doing the exact opposite.

I have already reported on BoE research that demonstrated that global integration of banking systems led to stability of funding flows within what researchers called the ‘internal capital markets’ of banking groups (I also added several historical examples to back this research).

More and more research is produced that actually contradicts the whole current regulatory thinking. A new study by NY Fed researchers Correa, Goldberg and Rice also confirmed the importance of banking group’s internal liquidity transfers across cross-border entities:

In global banks, internal liquidity management is a consistent driver of explaining cross-sectional differences in loan growth in response to changing liquidity risk. Those banks with higher net borrowing from affiliated entities had consistently strong loan growth (domestic, foreign, cross-border, credit) when liquidity risks increased. As shown in the last column of Table 2 Panel B, these global banks with larger unused credit commitments borrow relatively more (net) from their affiliates when liquidity conditions worsen and then sustain lending to a greater degree.

Clearly, the ability of global groups to transfer liquidity and capital across borders can play the role of risk absorber when a crisis strikes. Yet national regulators are implementing new measures that have the exact opposite effect (i.e. ring-fencing and so on). Measures that, among others, result in the disintegration of banking across the Eurozone.

Consequently, regulators’ and politicians’ enthusiasm for the banking union seems a little bit misplaced. See this recent speech by Vítor Constâncio, Vice-President of the ECB:

Another important objective of Banking Union is to overcome financial fragmentation and promote financial integration. In particular, this will constitute a key task of the Single Supervisory Mechanism.

Really? This seems to me to contradict the very actions of regulators in the EU. It can only be one way Mr. Constancio, not both ways.

Then he adds something that is, I believe, a fundamental error:

There are four ways which I expect the SSM to make a difference to banking in Europe: by improving the quality of supervision; by creating a more homogeneous application of rules and standards; by improving incentives for deeper banking integration; and by strengthening the application of macro-prudential policies.

The prudential supervision of credit institutions will be implemented in a coherent and effective manner. More specifically, the Single Rule Book and a single supervisory manual will ensure that homogeneous supervisory standards are applied to credit institutions across euro area countries. This implies that common principles and parameters will be applied to banks’ use of internal models, for example. This will improve the reliability and coherence in banks’ calculation of risk-weighted assets across the Banking Union. On another front, the harmonisation in the treatment of non-performing exposures and provisioning rules will mean that investors can directly compare balance sheets across jurisdictions.

While I believe that the single resolution mechanism can indeed be beneficial (even though it looks overly complicated and it remains to be seen how it’s going to work in practice), a single regulatory treatment of all banks across economies and jurisdictions as varied as those of the EU is mistake. Here is what I said more than a year ago about the standardisation problem:

So a standardisation seems to be a good thing as data becomes comparable. Well, it is, and it isn’t. To be fair, standardisation within a country is probably a good thing, although shareholders, investors and auditors – rather than regulators – should force management to report financial data the way they deem necessary. However, it makes a lot less sense on an international basis. Why? Countries have different cultural backgrounds and legal frameworks, meaning that certain financial ratios should not be interpreted the same way from one country to another.

Let’s take a few examples. In the US, people are much more likely than Europeans on average to walk away from their home if they can’t pay off their mortgage. Most Europeans, on the other hand, will consider mortgage repayment as priority number 1. As a result, impaired mortgage ratios could well end-up higher in the US. But US banks know that and adapt their loan loss reserves in consequence. Within Europe, legal frameworks and judiciary efficiency are also key: UK banks often set aside fewer funds against mortgage losses as the legal system allows them to foreclose and sell homes relatively quickly and with minimal losses. In France on the other hand, the process is much longer with many regulatory and legal hurdles. Consequently, UK-based mortgage banks seem to have lower loan loss reserves compared with some of their continental Europe peers. Does it mean they are riskier? Not really.

Indeed, look at the World Bank’s Doing Business data. The Economist selected a few countries below, all of them from the EU:

EU countries have very disparate legal frameworks and cultural backgrounds. What Constancio is saying is that the same criteria are going to be applied to all banks across all countries above. This does not make sense. The ‘single EU market’ remains for now a multiplicity of various heterogeneous markets, with their own rules, that have merely facilitated cross-border trade and labour movement.

This is a fundamental issue with the EU. Monetary and banking union should have come last, after all other laws had been harmonised. Not first. For now, EU politicians want to force a banking union on a geographical area that has limited legal and political integration. Let alone that domestic politicians and regulators are forcing their domestic banks to focus on business within their national borders, not within the EU borders.

* Indeed, another recent paper by Claessens and van Horen (summary on VOX here) suggests that

After a continued rise until 2008, the number of foreign banks from high-income countries has started to decline, from 948 in 2008 to 814 in 2013, mostly on account of a retrenchment by crisis-affected Western European banks.

On the other hand, banks from emerging markets and developing countries continued their pre-crisis growth and further increased their presence. Currently these banks own 441 foreign banks, representing 8% of all foreign assets, a doubling of their share as of 2007. As these banks tend to invest mainly in their own geographical regions, global banking now both encompasses a larger variety of players and at the same time is more regional, with the average intraregional share increasing by some five percentage points.

Chinese regulation, the European way

Some European banking regulators are currently considering the implementation of a sovereign bond exposure cap of 25% of capital to any one sovereign. Their goal is to break the link between sovereigns and banks. I think they don’t really know what they are doing.

European sovereign bond markets are distorted in all possible ways:

- The Basel banking regulation framework has been awarding 0% risk-weight to OECD sovereign debt since the 1980s, meaning purchasing such asset does not require any capital. Recent rules haven’t changed anything to this.

- On the contrary, Basel 3 introduces a liquidity ratio (LCR) basically requiring banks to hold even more sovereign debt on their balance sheet (as part of so-called highly-liquid ‘Level 1 assets’).

- Meanwhile, the ECB, as well as the BoE, have been trying to revive business lending (which suffers from the opposite problem: high risk-weights) by launching cheap funding programmes (LTRO, TLTRO, FLS…). Banks drawn on those facilities to invest in… more 0% weighted sovereign debt, and earn capital-free interest income. We call this the ‘carry trade’.

- Furthermore, investors (including banks) have started seeing peripheral European debt as virtually risk-free thanks to the ECB pledge that it would do whatever it takes to prevent defaults in those countries.

There you are: had European regulators wanted to reinforce the link between sovereigns and banks, they wouldn’t have been more successful. Their usual talk of breaking the link between banks and sovereigns has been completely undermined by their own actions.

The easy solution would have been to scrap risk-weights (or at least increase them on sovereign bonds). But this was too simple, so European policymakers decided to go the Chinese way: never scrap a bad rule; design a new one to fix it; and another one to fix the previous one that fixed the original one.

The new 25% cap would only add further distortion: while Basel’s risk-weights do not differentiate between Portuguese and German bonds, the 25% rule doesn’t either. But, you would retort, this isn’t the point: the point is to limit the exposure to any single sovereign. I agree that diversification is usually a good thing. But 1. lack of diversification has been encouraged by policymakers’ own decisions, and 2. forcing banks to diversify away from the safest sovereigns just for the sake of diversifying may well put many banks’ balance sheet more at risk.

Finally, Fitch estimates at EUR1.1Trn the amount of debt that would need to be offloaded. This is very likely to affect markets and could result in banks taking serious one-off hits on their available-for-sale and marked-to-market bond portfolios, resulting in weaker capital positions. This could also raise overall interest rates, in particular in riskier (and weaker) European countries. Fitch believes banks could rebalance into Level 1-elligible covered bonds. Maybe, but this would only introduce even more distortions in the market by artificially raising the demand for their underlying assets, and this would encumber banks’ balance sheets even further, creating other sorts of risks.

Why pick a simple solution when you can do it the Chinese way?

Photo: picture-alliance / dpa through www.dw.de

Frances Coppola on regulatory arbitrage

Frances Coppola recently wrote an interesting article on the origins of the financial crisis, which reflects several of the points that I have made on this blog time and time again: the crisis is the resulting product of the combination of regulatory arbitrage and interest rates below their natural level (as well as a few other things). I encourage you to read her article (which is at least necessary to follow my own post).

Yet I believe her story isn’t fully accurate. While US banks were subject to a leverage ratio, they were also subject to Basel 1 rules. As I have demonstrated, Basel 1 caused a surge in real estate and sovereign lending, and boosted the use of securitization, through regulatory arbitrage as Basel applied low risk-weights to those asset classes (for the most recent evidence, see here). Unlike what Hyun Song Shin believes, banks were already circumventing the ‘spirit’ of Basel 1 as soon as it was published in 1988… Basel 2 didn’t change much, and its implementation in Europe was anyway too late to have much of an influence on the crisis storyline (which had been building up since the late 1980s).

As a result, I don’t believe that, if European banks had been subject to a leverage ratio, they would not have been able to invest in American securitized products. They would still have done it, and perhaps sacrificed other type of lending or investments in other securities instead. Why? Because RMBSs and other CDOs offered higher yields for lower capital requirements, ceteris paribus. Risk-adjusted profit-maximising banks quickly figure it out.

She concludes:

The story of the financial crisis is a story of the failure of safe assets. That is why it was so traumatic. People expect to take losses on risky investments. They don’t expect to take losses on safe ones. Yet we are still trying to make the financial system “safer” and encourage investors to invest in “safe” assets. When will we learn that the safest investment is a risky one, and the most dangerous investments are those that are believed to be completely safe?

And it is also a warning of the consequences of regulatory arbitrage. The fact that the US and European banks had different regulatory regimes created a golden opportunity for unregulated institutions to exploit, with catastrophic consequences. Yet the US, the UK and the EU are still devising their own systems of regulation with scant regard for international consistency. When will we learn that an international industry requires international regulation?

I would say that the crisis wasn’t a failure of safe assets per se. It was a failure of regulation that wanted us (or actually, forced us) to believe that some assets were safe, creating a vicious spiral as banks piled into those asset classes to maximise their return on regulatory capital.

Moreover, regulatory arbitrage isn’t a cross-border issue. Most countries experienced the same symptoms: increasing real estate prices and securitization-issuance volumes, and lower sovereign debt yields. This points to intra-Basel distortions within countries, not to extra-Basel arbitrage across countries. Regulatory arbitrage-driven financial imbalances are endogenous to Basel regulations. Cross-border arbitrage, the Euro, populist politics (which never dies, as US politicians – incredibly – want to revive Fannie and Freddie…), also played a secondary (and surely exacerbating) role, but they were not at the very root of the crisis.

PS: Frances just published a new article on the ECB stress tests. I don’t disagree with her, but I believe that it is easy to criticise the test in hindsight, once we found out the number of banks that failed: she could have attacked the methodology at the time it was published. She also missed that, if banks don’t increase lending post-result announcements, it isn’t necessarily because they are zombies (some may well be). But the test was run on phased-in Basel 3 CET1 figures, not fully-loaded ones. Many banks still have large capital adjustments/deleveraging to make before complying with fully-loaded Basel 3 requirements, which isn’t going to help lending growth, especially given that banks currently don’t cover their cost of capital. (Another inconsistency of the test is that some banks were tested against fully-loaded ratios, and in the end obviously appeared uglier than if they had been tested against the same standards as other banks. If all banks had been tested against fully-loaded capital ratios, 36 would have failed)

ECB policies: from flop to flop… to flop?

Even central bankers seem to be acknowledging that their measures aren’t necessarily effective…

ECB’s Benoit Coeuré made some interesting comments on negative deposit rates in a speech early September. Surprisingly, he and I agree on several points he makes on the mechanics of negative rates (he and I usually have opposite views). Which is odd. Given the very cautious tone of his speech, why is he even supporting ECB policies?

Here is Coeuré:

Will the transmission of lower short-term rates to a lower cost of credit for the real economy be as smooth? While bank lending rates have come down in the past in line with lower policy rates, there is a limit to how cheap bank lending can be. The mark-up that banks add to the cost of obtaining funding from the central bank compensates for credit risk, term premia and the cost of originating, screening and monitoring loans. The need for such compensation does not necessarily fall when policy rates are lowered. If anything, a central bank lowers rates when the economy needs stimulus, which is precisely when it is difficult for banks to find good loan making opportunities. It remains to be seen whether and to what extent the recent monetary policy accommodation translates into cheaper bank lending.

This is a point I’ve made many times when referring to margin compression: banks are limited in their ability to lower the interest rate they charge customers as, absent any other revenue sources, their net interest income necessarily need to cover their operating costs (at least; as in reality it needs to be higher to cover their cost of capital in the long run). Banks’ only solution to lower rates is to charge customers more for complimentary products (it has been reported that this is in effect what has been happening in the US recently).

Negative rates are similar to a tax on excess reserves, which evidently doesn’t make it easier for a bank to improve its profitability, and as a result its internal capital generation. And Coeuré agrees:

A negative deposit rate can, however, also have adverse consequences. For a start, it imposes a cost on banks with excess reserves and could therefore reduce their profitability. Note, however, that this applies to any reduction of the deposit rate and not just to those that make the rate negative. For sure, lower bank profitability could hamper economic recovery, especially in times when banks have to deleverage owning to stricter regulation and enhanced market scrutiny. But whether bank profitability really falls when policy rates are lowered depends more generally on the slope of the yield curve (as banks’ funding costs may also fall), on banks’ investment policies (as there is scope for them to diversify their cash investment both along the curve and across the credit universe) and on factors driving non-interest income.

Coeuré clearly understands the issue: central banks are making it difficult for banks to grow their capital base, while regulators (often the same central bankers) are asking banks to improve their capitalisation as fast as possible. Still, he supports the policy…

Other regulators are aware of the problem, and not all are happy about it… Andrew Bailey, from the Bank of England’s PRA, said last week that regulatory agencies should co-ordinate:

I am trying to build capital in firms, and it is draining out down the other side.

This says it all.

Meanwhile, and as I expected, the ECB’s TLTRO is unlikely to have much effect on the Eurozone economy… Banks only took up EUR83m of TLTRO money, much below what the central bank expected. It is also likely that a large share of this take up will only be used for temporary liquidity purposes, or even for temporary profitability boosting effects (through the carry trade, by purchasing capital requirement-free sovereign debt), until banks have to pay it off after two years (as required by the ECB, and without penalty, if they don’t lend the money to businesses).

Fitch also commented negatively on TLTRO, with an unsurprising title: “TLTROs Unlikely to Kick-Start Lending in Southern Europe”.

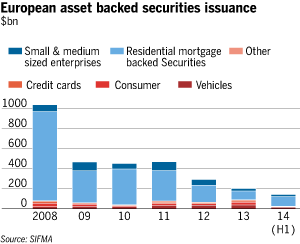

Finally, the ECB also announced its intention to purchase asset-backed securities (which effectively represents a version of QE). While we don’t know the details yet, the scheme has fundamentally a higher probability to have an effect on banks’ behaviour. There is a catch though: ABS issuance volume has been more than subdued in Europe since the crisis struck (see chart below, from the FT). The ECB might struggle to buy the quantity of assets it wishes. Perhaps this is why central bankers started to encourage European banks to issue such structured products, just a few years after blaming banks for using such products.

Oh, actually, there is another catch. ABSs are usually designed in tranches. Equity and mezzanine tranches absorb losses first and are more lowly rated than senior tranches, which usually benefit from a high rating. Consequently, equity and mezzanine tranches are capital intensive (their regulatory risk-weight is higher), whereas senior tranches aren’t. To help banks consolidate their regulatory capital ratios and prevent them from deleveraging, the ECB needs to buy the riskier tranches. But political constraints may prevent it to do so… Will this new ECB scheme also fail? As long as central bankers (and politicians) continue to push for schemes and policies without properly understanding their effects on banks’ internal ‘mechanics’, they will be doomed to fail.

PS: I have been busy recently so few updates. I have a number of posts in the pipeline… I just need to find the time to write them!

Continuously ignoring and misinterpreting history

This recent speech by the Vice President of the ECB, Vítor Constâncio, is in my opinion one of the foremost examples of how a partial reading or misinterpretation of history that becomes accepted as mainstream can lead to bad policy-making.

This speech is typical. Constâncio argues that

the build-up of systemic risk over the financial cycle is an endogenous outcome – a man-made construct – and the job of macro-prudential policy is to try to smoothen this cycle as much as possible. […]

The […] most important source of systemic risk is the risk of the unravelling of financial imbalances. These imbalances may build up gradually, mostly endogenously, and can then unravel abruptly. They form part of the inherent pro-cyclicality of the financial system.

It is crucial to recognise that the financial cycle has an important endogenous component which arises because banks take too much solvency and liquidity risk. The aim of macro-prudential policy should be to temper the financial cycle rather than to merely enhance the resilience of the financial sector ahead of crises.

While Constâncio is right that there is some truth in the pro-cyclicality of financial systems as a long economic boom impairs risk perception, risk assessment and risk premiums, he never highlights why such booms and busts occur in the first place. Outside of negative supply shocks, are they a ‘natural’ consequence of the activity of the economic system? Or are they exogenously triggered by bad government or monetary policies?

Several economic schools of thought have different explanations and theories. Yet, there is one thing that cannot be denied: historical experiences of financial stability.

This is where the flaw of Constâncio’s (and of most central bankers’ and mainstream economists’) thinking resides: history proves that, when the banking sector is left to itself, systemic endogenous accumulation of financial imbalances is minimal, if not non-existent…

According to Larry White in a recent article summing up the history of thought and historical occurrences of free banking, Kurt Schuler identified sixty banking episodes to some extent akin to free banking. White’s paper describes 11 of them, many of which had very few institutional and regulatory restrictions on banking. He quotes Kevin Dowd:

As Kevin Dowd fairly summarizes the record of these historical free banking systems, “most if not all can be considered as reasonably successful, sometimes quite remarkably so.” In particular, he notes that they “were not prone to inflation,” did not show signs of natural monopoly, and boosted economic growth by delivering efficiency in payment practices and in intermediation between savers and borrowers. Those systems of plural note-issue that were panic-prone, like the pre-1913 United States and pre-1832 England, were not so because of competition but because of legal restrictions that significantly weakened banks.

Yet, there is no trace of such events in conventional/mainstream financial history. Central bankers seem to be completely oblivious to those facts (this is surely self-serving) and economists only partially aware of the causes of financial crises. Moreover, free banking episodes also proved that banks were not inherently prone to take “too much solvency and liquidity risk”: indeed, historical records show that banks in such periods were actually well capitalised and rarely suffered liquidity crises. In short, laissez-faire banking’s robustness was far superior to our overly-designed ones’. Consequently we keep making the same mistakes over and over again in believing that a crisis occurred because the previous round of regulation was inadequate…

What we end up with is a banking system shaped by layers and layers of regulations and central banks’ policies. Every financial product, every financial activity, was awarded its own regulation as well as multiple ‘corrective’ rules and patches, was influenced by regulators’ ‘recommendations’, was limited by macro-prudential tools and manipulated through various interest rates under the control by a small central authority. On top of such regulatory intervention, short-term political interference compounds the problem by purposely designing and adjusting financial systems for short-term electoral gains. Markets are distorted in all possible ways as the price system ceases to work adequately, defeating their capital allocation purposes and creating bubbles after bubbles.

Studying banking and financial history demonstrates that it is quite ludicrous to pretend that banking systems are inherently subject to failure through endogenous accumulation of risk. In the quest for an explanation of the crisis, better look at the intersection of moral hazard, political incentives, and the regulatory-originated risk opacity. It might turn out that imbalances are, well, mostly… exogenous.

Please let finance organise itself spontaneously.

Photo: José Carlos Pratas

The surprising effects of negative rates on German banks

Several banks have already made public their intentions to withdraw their excess reserves from the ECB, following the central bank’s decision to charge banks for keeping excess reserves deposited with it (i.e. negative deposit rates). It is unclear what’s going to happen to this cash. If it is redeposited at another Eurozone bank, then it still ends up on an ECB account. Euros could potentially be placed somewhere outside the Eurozone to reduce the aggregate amount of excess reserves in the system, but there is no guarantee they would not come back either (through non-Euro companies paying Euro suppliers for instance). Banks could also withdraw paper money, but this involves storage costs.

Very low ECB main rates already represented a pressure on banks’ net interest margins. The ECB negative deposit rates were seen as a way to bolster the interbank money markets. Unfortunately, many banks are now also retracting from interbank markets altogether because of the very poor yields obtained on those placements… thanks to the low ECB main rate. Seen this way, very low ECB refinancing rates and negative ECB deposit rates look contradictory.

But there’s something new.

In Germany, some banks (mostly the largest ones), are now passing on negative rates to… their clients. Handelsblatt reported last week that institutional clients such as mutual funds and insurers have now been asked to pay interests on short-term deposits… To be honest, I wasn’t really expecting such a move, given the instability it can create in banks’ funding structure. However, the effects remain for now limited as retail clients, as well as other types of corporate clients, are unaffected.

Let’s get back to our basic bank’s profit equation:

Economic Profit = II – IE – OC – Q

where II represents interest expense, IE interest income, OC operating costs (which include impairment charges on bad debt), and Q liquidity cost.

As we recently saw, low ECB interest rates impact II downward, negative ECB deposit rates impact IE upward, meaning ceteris paribus that the only thing banks can do to remain profitable in the short-run is to cut fixed costs (OC). Ex-post, banks can also influence IE by repricing their loan book upward.

This is indeed what has been happening in Germany: banks have been cutting staff, deleveraging, and outsourcing expenses to low-cost countries. The spread between new lending rates and the ECB main rate has also remained consistently high since the rate cuts, and has even started to increase again following the most recent rate cuts (see below, blue arrows represent rate cuts, red arrows represent spread increases).

By passing negative deposit rates onto customers, banks found a way of quickly increasing II to partially offset the increase in IE. The effects are faster than further increasing the interests charged on lending, as it directly impacts the outstanding stock of deposits (unlike repricing, whose pace depends on the volume and maturity profile of the bank’s loan book).

However, this provides customers with an incentive to withdraw their deposits, introducing instability in the banks’ funding structure, increasing Q. Given the limited range of customer concerned so far, those banks probably thought it was a worthwhile temporary bet. Indeed, increasing their lending volume to reduce their excess reserves, or investing those reserves somewhere, would also have increased Q anyway. Furthermore, those institutional clients are likely to have significant brokerage/trading/custody relationships with those banks, making it difficult for them to close their accounts and move funds away without disrupting their business.

I have no information regarding the implementation of such policies by other banks of the Eurozone so far. If those policies become widespread, the ECB’s decisions will not only have been pointless, but they will also have succeeded in making the funding structure of the whole Eurozone banking system more unstable and in reducing the purchasing power of non-bank corporations that have to maintain deposits in the Eurozone.

Basel vs. ECB’s TLTRO: The fight

(and vs. BoE’s FLS)

Following my previous post on the mechanics of ECB negative deposit rates, I wanted to back my claims about the likely poor effect of the central bank TLTRO measure on lending.

I argued that despite the cheap funds provided by the ECB to lend to corporate clients (particularly SMEs), Basel’s risk-weighted assets would stand in the way of the scheme as they keep distorting banks’ lending incentives (same is true regarding the BoE and the second version of its Funding for Lending Scheme).

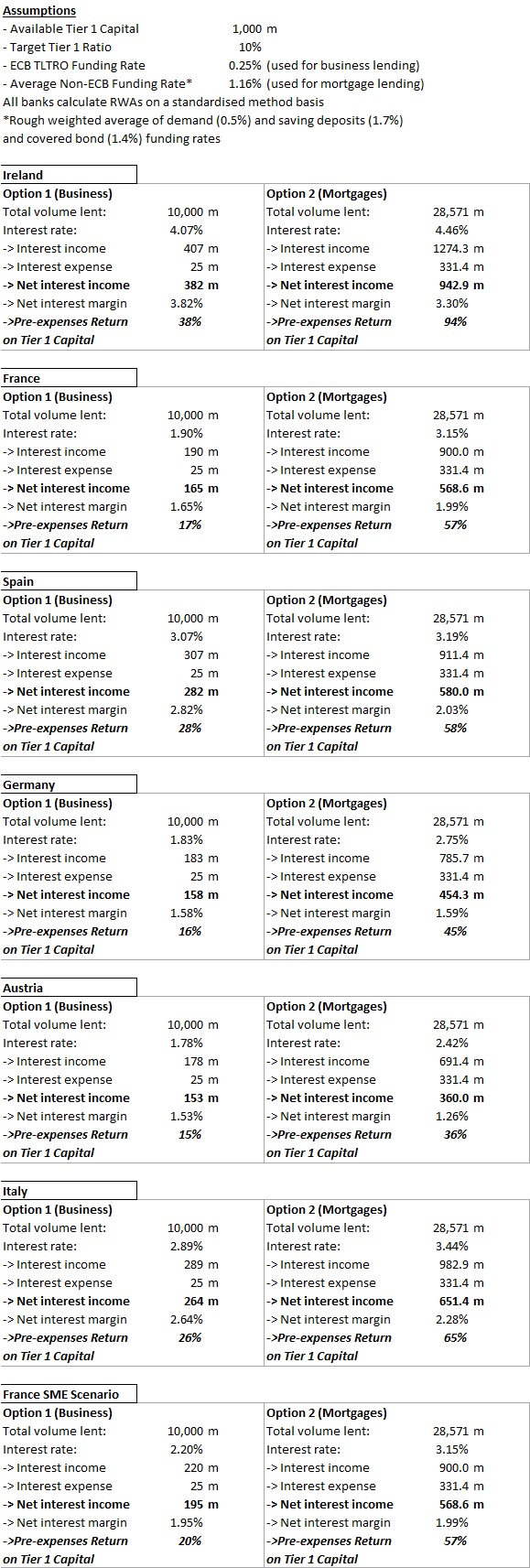

I extracted all the most recent new business and mortgage lending rates from the central banks’ websites of several European countries. Unfortunately, business lending rates are most of the time aggregates of rates charged to large multinational companies, SMEs, and micro-enterprises. Only the Banque of France seemed to provide a breakdown. So most business lending rates below are slightly skewed downward (but not by much as you can see with the French case).

Using this dataset, I built a similar scenario to the one I described in my first RWAs and malinvestments post (as it turned out, I massively overestimated business lending rates in that post…). I wanted to find out what would be the most profitable option for a bank: business lending or mortgage lending, given RWA and capital constraints (banks target a 10% regulatory Tier 1 capital ratio). The results speak for themselves:

Despite the cheap ECB loans, and given a fixed amount of capital, banks are way more profitable raising funding from traditional sources to lend to households for house purchase purposes…

Admittedly, the exercise isn’t perfect. But the difference in net interest income and return on capital is so huge that tweaking it a little wouldn’t change much the results:

- I assume that all business lending is weighted 100%. In reality, apart from the French SME scenario, large corporates (often rated by rating agencies) benefit from lower RWA-density under a standardised method. This would actually raise the profitability of business lending through higher volume (and increased leverage), though not by much. Mortgages are weighted at 35% under that method.

- I assume that all banks use the standardised method to calculate RWAs. In reality, only small and medium-sized banks do. Large banks use the ‘internal rating based’ method, which allows them to risk-weight customers following their own internal models. Here again, most corporates can benefit from lower RWAs. But mortgages also do (RWA-density often decreases to the 10-15% range).

- Cross-selling is often higher with corporates, which desire to hedge and insure their financial or non-financial business positions. Corporates also use banks’ international payment solutions. This adds to revenues.

- Business lending is often less cost-intensive than retail lending. Retail lending indeed traditionally requires a large branch network, which is less the case when dealing with corporates (often grouped within regional corporate centres, though not always for tiny enterprises). However, retail banking is progressively moving online, providing opportunities to banks to cut costs and improve their profitability.

- The lower RWA-density on mortgages allows banks to increase lending volume and leverage. However, this also requires higher funding volumes. In turn, this should increase the rate paid on the marginal increase in funding, raising interest expense somewhat in the case of mortgages.

In the end, even if the adjustments described above reduce the profitability spread by 10 percentage points, the conclusion stands: banks are hugely incentivised to avoid business lending, facilitating misallocation of capital on a massive scale, in particular in a period of raising capital requirements… Moreover, banks also benefit from favourable RWAs for securitised products based on mortgages (CMBS, RMBS…), compounding the effects.

To tell you the truth, I wasn’t expecting such frightening results when I started writing that post… Please someone tell me that I made a mistake somewhere…

Central banks, regulators and politicians will find it hard to prop up business lending with regulations designed to prevent it.

The (negative) mechanics of negative ECB deposit rates

The ECB has finally announced last week that it would be lowering its main refinancing rate from 0.25% to 0.15%, and that it would lower the rate it pays on its deposit facility from 0% to -1%. The ECB hopes to incentivise banks to take money out of that facility and lend it to customers*, providing a boost to the broad money supply and counteracting deflation risks.

The interest rate of the ECB deposit facility is supposed to help the central bank define a floor under which the overnight interbank lending rate (EONIA) should not go. The reason is that deposits at the ECB are supposedly risk-free (or at least less risky than placing the money anywhere else). Consequently, banks would never place money (i.e. excess reserves) at another bank/ investment (which involves credit risk) for a lower rate. When the deposit facility rate is high, banks are incentivised to reduce their interbank lending exposures and leave their money at the ECB (and vice versa). On the other hand, the main refinancing rate is supposed to represent an upper boundary to the interbank lending rates: theoretically, banks should not borrow from another bank at a higher rate than what it would pay at the ECB. In practice, this is not exactly true, as banks do their best to avoid the stigma associated with borrowing from the central bank.

Unfortunately, there is a fundamental microeconomic reason why banks cannot diminish their lending rate indefinitely. I have already described how banks are not able to transmit interest rates lower than a certain threshold to their customers due to the margin compression effect (see also here). Indeed, banks’ net interest income must be able to cover banks’ fixed operating costs for the bank to remain profitable from an accounting point of view. When rates drop below a certain level, banks have to reprice their loan book by increasing the spread above the central bank rate on the marginal loans they make, breaking the transmission mechanism of the lending channel of monetary policy. As we have already seen, in the UK, that threshold seems to be around 2%.

But the same thing seems to happen in other European countries. This is Ireland (enlarge the charts)**:

We can notice the margin compression effect on the first chart. The lending rate stops dropping despite the ECB rate falling as banks reprice their lending upward to re-establish profitability (evidenced from the second chart, where interest rates on new lending increase rather than decrease).

This is France:

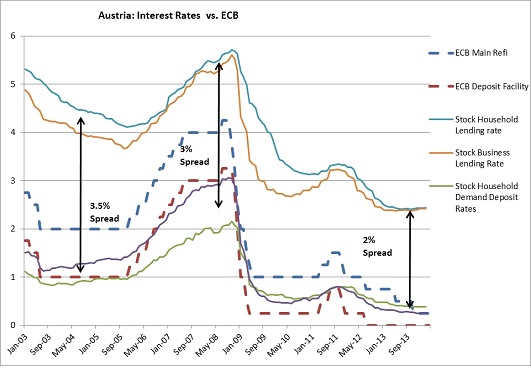

This is Austria:

Clearly, what happens in the UK regarding margin compression also occurs in those countries. When the ECB rate dropped, outstanding floating rate lending rates also dropped (because floating rate lending is indexed on either the ECB base rate or on Euribor), causing pressure on revenues. As long as deposit rates could also fall (this varies a lot by country, as French banks never pay anything on demand deposits), the loss in interest income was offset by reduced interest expense. But once deposit rates reached 0 and couldn’t fall any lower, banks in those countries experienced margin compression and their net interest income started to suffer. Moreover, this happened exactly when loan impairment charges peaked because of increased credit risk.

Banks in emerging countries have constantly high non-performing loans ratios. But they still manage to remain (often highly) profitable by maintaining very high net interest income and margins. In Western Europe, banks saw their net profits all but disappear with rates dropping that low. As a result, it is likely that the new ECB rate cut won’t affect lending rates much…

Nonetheless, the ECB had been trying to revive, or encourage, interbank lending throughout most of the crisis, and had already lowered to its deposit rate to 0%. Nevertheless, banks maintained cash in those accounts. Why would a bank leave its money in an account that pays 0%? Because banks adjust those interest rates for risk. An ECB risk-adjusted 0% can be worth more than a risk-adjusted 4% interbank deposit at a zombie/illiquid/insolvent bank. However, the ECB is clearly not satisfied with the situation: it now wants banks to take their money out of the facility and lend it to the ‘real economy’.

How do the combination of low refi rate and negative ECB deposit rates impact banks? Let’s remember banks’ basic profit equations:

Accounting Profit = II – IE – OC, and Economic Profit = II – IE – OC – Q

where II represents interest expense, IE interest income, OC operating costs (which include impairment charges on bad debt), and Q liquidity cost.

For a bank to remain economically profitable (or even viable in the long-term), the rate of economic profit must be at least equal to the bank’s cost of equity.

To maximise their economic profits, banks look for the most-profitable risk-adjusted lending opportunities. ‘Lending’ to the ECB is one of those opportunities. Placing money at the ECB generates interest income. This interest income is more than welcome to (at least) maintain some level of accounting profitability (though not necessarily economic profitability) when economic conditions are bad and income from lending drops while impairment charges jump***.

With deposit rates at 0, banks’ income became fully constrained by financial markets and the economy. With rates in negative territory, not only banks see their interest income vanish but also their interest expense increase. From the equations above, it is clear that it makes banks less profitable****. On top of that, lending that cash can make banks less liquid, which increases their riskiness and elevates their cost of capital (the ‘Q’ above). The question becomes: adjusted for credit and liquidity risk, is it still worth keeping that cash at the ECB? The answer is probably yes.

(unless banks find worthwhile investments outside of the Eurozone, which wouldn’t be of much help to prop up Euro economies…)

To summarise, ‘II’ is negatively impacted by a low base rate whereas ‘IE’ reaches a floor (= margin compression). ‘IE’ then increases when the central bank deposit rate turns negative. Meanwhile, ‘OC’ increases as loan impairment charges jump due to heightened credit risk. Profitability is depressed, partly due to the central bank’s decisions.

Many European banks aren’t currently lending because they are trying to implement new regulatory requirements (which makes them less profitable) in the middle of an economic crisis (which… also makes them less profitable). As a result, the ECB measures seem counterproductive: in order to lend more, banks need to be economically profitable. Healthy banks lend, dying ones don’t.

The ECB is effectively increasing the pressure on banks’ bottom line, hardly a move that will provide a boost to lending. The only option for banks will be to cut costs even further. And when a bank cut costs, it effectively reduces its ability to expand as it has less staff to monitor lending opportunities, and consequently needs to deleverage. Once profitability is re-established, hiring and lending could start growing again.

A counterintuitive (and controversial) approach to provide a boost to lending would be to subsidise even more the banking sector by increasing interest rates on both the refinancing and deposit facilities.

Defining the appropriate level of interest rates would be subtle work though: struggling over-indebted households and businesses may well start defaulting on their debt. On the other hand banks’ revenues would increase as margin compression disappears, making them able to lend more eventually. The subtle balance would be achieved when interest income improvements more than offset credit losses increases. Not easy to achieve, but pushing rates ever lower is likely to cripple the banking system ever more and reduce lending in proportion (while allowing zombie firms to survive).

Furthermore, banks are repricing their loan book upward anyway, making the ECB rate cuts pointless. The process takes time though and it would be better for banks to rebuild their revenue stream sooner than later. The ECB could still use other monetary tools to influence a range of interest rates and prices through OMO and QE measures, which would be less disruptive to banks’ margins.

Finally, the ECB has launched its own-FLS style ‘TLTRO’, a scheme that provides cheap funding to banks if they channel the funds to businesses. Similarly to the BoE’s FLS, I believe such scheme suffers from delusion. Banks are currently deleveraging to lower their RWAs in order to comply with the harsher capital requirements of Basel 3. If there is one thing banks want to avoid, it is to lend to RWA-dense customers such as SMEs… (and instead focus on better RWA/risk-adjusted profitable lending such as… mortgages). Banks can also already extract relatively low wholesale funding rates by issuing secured funding instruments such as covered bonds. (UPDATE: see this follow-up post on that topic)

* This does not mean that banks would ‘lend out’ money to customers, unless they withdraw it as cash. But by increasing lending, absolute reserve requirements increase and banks have to transfer money from the deposit facility to the reserve facility.

** Data comes from respective central banks. They are not fully comparable. I gathered data from many different Eurozone countries, but unfortunately, some central banks don’t provide the data I need (or the statistics database doesn’t work, as in Italy…). Spreads are approximate ones calculated between the middle point of deposit rates and the middle point of lending rates. Analysis is very superficial, and for a more comprehensive methodology please refer to my equivalent posts on the UK/BoE.

*** Don’t get me wrong though. Fundamentally speaking, I am not in favour of such central bank mechanisms as I believe this is akin to a subsidy that distorts banks’ risk-taking behaviour. In a central banking environment, like Milton Friedman I’d rather see the central bank manipulate interest rates solely through OMO-type operations.

**** Of course this remains marginal. But in crisis times, ‘marginal’ can save a bank. Let’s also not forget booming litigation charges, currently estimated at USD104Bn… Evidently making it a lot easier for banks to lend as you can imagine…

Recent Comments