Myths are slowly being debunked. Slowly…

A few institutions have recently raised voices to try to debunk some of the banking legends that had appeared and became conventional knowledge as a result of the crisis. Here’s an overview.

S&P, the rating agency, just published a note declaring that, surprise surprise, the UK’s ring fencing plans could have clear adverse consequences. Those include: possible downgrade to ‘junk’ status and lower ‘stability’ of the non-ring fenced entities, costs for customers could rise, credit supply could be squeezed, and, what I view as the most important problem of all, ring fencing rules “will undoubtedly further constrain fungibility.” According to the S&P analyst, as reported by Reuters:

“The sharing of resources (and brand, expertise, and economies of scale) means we view most banking groups as being more than the sum of their parts,” the report said.

It said disrupting these benefits could lead S&P to have a weaker view of the group as a whole and to lower its credit ratings on some parts of the banks.

S&P said the complexity of separating functions “represents a significant operational challenge” for banks at a time of multiple other regulations.

I cannot agree more. I have already written four long pieces explaining why intragroup liquidity and capital transfers were key in maintaining a banking group safe. Ring fencing does the exact opposite, putting those liquidity buffers and capital bases in silos from which they cannot be used elsewhere, potentially endangering the whole bank.

The BoE just reported that households could actually cope with raising interest rates. One of the Bank’s justification for not raising rates was that it would push many households towards default, so it is now kind of contradicting itself. And anyway, as I have described previously, lowering rates ceased to translate into lower borrowing rates due to margin compression. Patrick Honohan, Governor of the central bank of Ireland, reported that the exact same phenomenon occurred in Ireland:

Because of the impact on trackers, though, the lower ECB interest rates have not directly improved the banks’ profitability, because the average and marginal cost of bank funds does not fall as much. The banks’ drive to restore their profitability, combined with the lack of sufficient new competition, has meant that, far from lowering their standard variable rates over the past three years as ECB rates have fallen, they have (as is well known) actually increased the standard variable rates somewhat. […] These rates indicate that standard variable rate borrowers are still paying less than they were before the crisis, but not by much. A widening of mortgage interest rate spreads over policy rates also occurred in the UK and in many euro area countries after the crisis, but spreads have begun to narrow in the UK and elsewhere. Until very recently bank competition has been too weak in Ireland to result in any substantial inroads on rates.

This chart exactly looks like what happened in the UK. Spread over BoE/ECB rates have increased, and increasing rates could actually translate into the same level of mortgage rates. This is because, as margin compression starts disappearing, competition can start driving down the spread over BoE/ECB. Households may have to remortgage to benefit from the same rates though.

In Germany, regulators said that the ECB’s negative deposit rates could incite more risk-taking and declared that:

Excess liquidity could even threaten the banking system if it is put to poor use

Regulators vs. ECB. This is getting interesting.

In FT Alphaville, David Keohane reports a few charts from Morgan Stanley. One of them clearly shows the Chinese Central Bank’s use of reserve requirements to manage lending growth. I’m sure my MMT and ‘endogenous money’ friends will appreciate.

Chinese regulation, the European way

Some European banking regulators are currently considering the implementation of a sovereign bond exposure cap of 25% of capital to any one sovereign. Their goal is to break the link between sovereigns and banks. I think they don’t really know what they are doing.

European sovereign bond markets are distorted in all possible ways:

- The Basel banking regulation framework has been awarding 0% risk-weight to OECD sovereign debt since the 1980s, meaning purchasing such asset does not require any capital. Recent rules haven’t changed anything to this.

- On the contrary, Basel 3 introduces a liquidity ratio (LCR) basically requiring banks to hold even more sovereign debt on their balance sheet (as part of so-called highly-liquid ‘Level 1 assets’).

- Meanwhile, the ECB, as well as the BoE, have been trying to revive business lending (which suffers from the opposite problem: high risk-weights) by launching cheap funding programmes (LTRO, TLTRO, FLS…). Banks drawn on those facilities to invest in… more 0% weighted sovereign debt, and earn capital-free interest income. We call this the ‘carry trade’.

- Furthermore, investors (including banks) have started seeing peripheral European debt as virtually risk-free thanks to the ECB pledge that it would do whatever it takes to prevent defaults in those countries.

There you are: had European regulators wanted to reinforce the link between sovereigns and banks, they wouldn’t have been more successful. Their usual talk of breaking the link between banks and sovereigns has been completely undermined by their own actions.

The easy solution would have been to scrap risk-weights (or at least increase them on sovereign bonds). But this was too simple, so European policymakers decided to go the Chinese way: never scrap a bad rule; design a new one to fix it; and another one to fix the previous one that fixed the original one.

The new 25% cap would only add further distortion: while Basel’s risk-weights do not differentiate between Portuguese and German bonds, the 25% rule doesn’t either. But, you would retort, this isn’t the point: the point is to limit the exposure to any single sovereign. I agree that diversification is usually a good thing. But 1. lack of diversification has been encouraged by policymakers’ own decisions, and 2. forcing banks to diversify away from the safest sovereigns just for the sake of diversifying may well put many banks’ balance sheet more at risk.

Finally, Fitch estimates at EUR1.1Trn the amount of debt that would need to be offloaded. This is very likely to affect markets and could result in banks taking serious one-off hits on their available-for-sale and marked-to-market bond portfolios, resulting in weaker capital positions. This could also raise overall interest rates, in particular in riskier (and weaker) European countries. Fitch believes banks could rebalance into Level 1-elligible covered bonds. Maybe, but this would only introduce even more distortions in the market by artificially raising the demand for their underlying assets, and this would encumber banks’ balance sheets even further, creating other sorts of risks.

Why pick a simple solution when you can do it the Chinese way?

Photo: picture-alliance / dpa through www.dw.de

When regulators become defiant of… regulation

After years of regulatory boom, some politicians, and regulators, seem to be – slowly – waking up. I have already described how UK’s Vince Cable seemed to now partially understand that regulation doesn’t make it easy for banks to lend to small and medium-sized businesses, and how Andrew Bailey, from the Bank of England’s Prudential Regulation Authority, complained about the lack of regulatory coordination across country:

I am trying to build capital in firms, and it is draining out down the other side.

Well, Bailey is at it again. Reuters summarized Bailey’s latest speech as:

The over-zealous application of anti-money laundering rules is hampering British banks abroad and cutting off poorer countries from global financial markets, a top Bank of England regulator said on Tuesday.

He said:

We have no sympathy with money laundering, but we are facing a frankly serious international coordination problem. […] We are seeing clear evidence … of parts of the world and activities that are being cut off from the mainstream banking system. […] It cannot be a good thing for the development of the world economy and the support of emerging countries … that we get into that situation. […] I have to spend a large part of my time dealing with the issues that come up in this field … because some of the consequences of the actions taken are potentially existential.

I find it quite ironic to see a regulator disapproving ‘over-zealous’ regulation. Another regulator, Jon Cunliffe, Deputy Governor of the Bank of England, declared that:

Liquidity and market making does seem to have been reduced. […] We’re not sure how much of it is the result of regulatory action, and how much of it is do with the change in business model for the institutions.

While he believes that some of the pre-crisis liquidity was ‘illusory’, his statement clearly indicates that he knows that regulation might not have had only positive effects. (Four days after I spoke about regulatory effects on market liquidity, Fitch published a press release arguing the exact same thing. I still have to write that post…)

Unfortunately, not all regulators are waking up. Reuters reported that David Rule, also from the BoE, said that:

banks had responded to regulatory incentives and increased their focus on the real economy, rather than financial market trading for its own sake.

Really? With business lending stuck at the bottom and mortgage lending (a very productive form a lending to the real economy) booming again? I see.

Andreas Dombret, of the Bundesbank, recently declared in a relatively reasonable speech* that:

But are we really overregulating? If we look at the benefits to society of a stable banking system and the social costs of a banking crisis, I believe the costs of regulation are justifiable.

Clearly he and Bailey should have a proper conversation…

Others, like Andrea Enria, Chairman of the European Banking Authority, which recently ran the European stress tests, warned that

The story is not over, even for the banks who passed it

I am unsure what the goal of that sort of threatening comment is, but I don’t see how this can reintroduce confidence in the European banking system. It certainly will push bankers to consolidate their balance sheet further rather than to start lending more. Let’s not forget that the EBA and ECB tests have the power to create a panic and destabilise markets when nothing would have occurred. Too soft and nobody would trust the tests. Too tough and a panic might set in (imagine the headlines: “Half of European banks at risk of failure!”). Another risk is that investors and commentators stop relying on their own judgment and analysis and start relying too much on regulators’ assessment. This would be extremely dangerous. Yet this already happens to an extent. Perhaps, as more and more regulators start waking up to the potentially harmful side effects of regulatory measures, they will back off and let the market play its role?

* While the speech is overall reasonable, Dombret still comes up with usual myths such as

Yet a leverage ratio would also create the wrong incentives. If banks had to hold the same percentage of capital against all assets, any institution wanting to maximise its profits would probably invest in high-risk assets, as they produce particularly high returns.

This is not correct.

Funnily, he also kind of admitted that regulators did not always understand how banking works, as I’ve been arguing a few times recently:

Do supervisors have to be the “better bankers”? No, absolutely not. Business decisions must be left to those being paid to make them. However, supervisors have to know – and understand – how banking works. Against this background, I personally would very much welcome an increase in the migration of staff between the banking industry and the supervisory agencies.

Still, many regulators influence business decisions…

Two kinds of financial innovation

Paul Volcker famously said that the only meaningful financial innovation of the past decades was the ATM. Not only do I believe that his comment was strongly misguided, but he also seemed to misunderstand the very essence of innovation in the financial services sector.

Financial innovations are essentially driven by:

- Technological shocks: new technologies (information-based mostly) allow banks to adapt existing financial products and risk management techniques to new technological paradigms. Without tech shocks, innovations in banking and finance are relatively slow to appear.

- Regulatory arbitrage: financiers develop financial products and techniques that bypass or use loopholes in existing regulations. Some of those regulatory-driven innovations also benefit from the appearance of new technological and theoretical paradigms. Those innovations are typically quick to appear.

I usually view regulatory-driven innovations as the ‘bad’ ones. Those are the ones that add extra layers of complexity and opacity to the financial system, hiding risks and misleading investors in the process.

It took a little while, but financial innovations are currently catching up with the IT revolution. Expect to change the way you make or receive payments or even invest in the near future.

See below some of the examples of financial innovation in recent news. Can you spot the one(s) that is(are) the most likely to lead to a crisis, and its underlying driver?

- Bank branches: I have several times written about this, but a new report by CACI and estimates by Deutsche Bank forecasted that between 50% and 75% of all UK branches will have disappeared over the next decade. Following the growing branch networks of the 19th and 20th centuries, which were seen as compulsory to develop a retail banking presence, this looks like a major step back. Except that this is actually now a good thing as the IT and mobile revolution is enabling such a restructuring of the banking sector. SNL lists 10,000 branches for the top 6 UK bank and 16,000 in Italy. Cutting half of that would sharply improve banks’ cost efficiency (it would, however, also be painful for banks’ employees). It is widely reported that banks’ branches use has plunged over the past three years due to the introduction of digital and mobile banking.

- In China, regulators have introduced new rules to try to make it harder for mainstream banks to deal with shadow banks in order to slow the growth of the Chinese shadow banking system, which has grown to USD4.9 trillion from almost nothing just a few years ago. The Economist reports that, by using a simple accounting trick, banks got around the new rules. Moreover, while Chinese regulators are attempting to constrain investments in so-called trust and asset management companies, investors and banks have now simply moved the new funds to new products in securities brokerage companies.

- In London, underground travellers can now pay for their journey by simply using their contactless bank card. No need of a specific underground card anymore. NFC-enabled smartphones will be able to do the same in the near future.

- Barclays is experimenting contactless wristband that would effectively replace your contactless card for payments (or, for Londoners, your underground Oyster Card).

- Apple announced Apple Pay, a contactless payment system managed by Apple through its new iPhones and Watch devices. Apple will store your bank card details and charge your account later on. This allows users to bypass banks’ contactless payments devices entirely. Vodafone also just released a similar IT wallet-contactless chip system (why not using the phone’s NFC system though? I don’t know. Perhaps they were also targeting customers that did not own NFC-enabled devices).

- Lending Club, the large US-based P2P lending firm, has announced its IPO. This is a signal that such firms are now becoming mainstream, as well as growing competitors to banks.

Of course, a lot more is going on in the financial innovation area at the moment, and I only highlighted the most recent news. Identifying the regulatory arbitrage-driven innovations will help us find out where the next crisis is most likely to appear.

PS: the growth of cashless IT wallets has interesting repercussions on banks’ liquidity management and ability to extend credit (endogenous inside money creation), by reducing the drain of physical cash on the whole banking system’s reserves (outside money). If African economies are any guide to the future (see below, from The Economist), cash will progressively disappear from circulation without governments even outlawing it.

Hummel vs. Haldane: the central bank as central planner

Recent speeches and articles from most central bankers are increasingly leaving a bad aftertaste. Take this latest article by Andrew Haldane, Executive Director at the BoE, published in Central Banking. Haldane describes (not entirely accurately…) the history and evolution of central banking since the 19th century and discusses two possible paths for the next 25 years.

His first scenario is that central banks and regulation will step backward and get back to their former, ‘business as usual’, stance, focusing on targeting inflation and leaving most of the capital allocation work to financial markets. He views this scenario as unlikely. He believes that the central banks will more tightly regulate and intervene in all types of asset markets (my emphasis):

In this world, it would be very difficult for monetary, regulatory and operational policy to beat an orderly retreat. It is likely that regulatory policy would need to be in a constant state of alert for risks emerging in the financial shadows, which could trip up regulators and the financial system. In other words, regulatory fine-tuning could become the rule, not the exception.

In this world, macro-prudential policy to lean against the financial cycle could become more, not less, important over time. With more risk residing on non-bank balance sheets that are marked-to-market, it is possible that cycles in financial assets would be amplified, not dampened, relative to the old world. Their transmission to the wider economy may also be more potent and frequent. The demands on macro-prudential policy, to stabilise these financial fluctuations and hence the macro-economy, could thereby grow.

In this world, central banks’ operational policies would be likely to remain expansive. Non-bank counterparties would grow in importance, not shrink. So too, potentially, would more exotic forms of collateral taken in central banks’ operations. Market-making, in a wider class of financial instruments, could become a more standard part of the central bank toolkit, to mitigate the effects of temporary market illiquidity droughts in the non-bank sector.

In this world, central banks’ words and actions would be unlikely to diminish in importance. Their role in shaping the fortunes of financial markets and financial firms more likely would rise. Central banks’ every word would remain forensically scrutinised. And there would be an accompanying demand for ever-greater amounts of central bank transparency. Central banks would rarely be far from the front pages.

He acknowledged that central banks’ actions have already considerably influenced (distorted?…) financial markets over the past few years, though he views it as a relatively good thing (my emphasis):

With monetary, regulatory and operational policies all working in overdrive, central banks have had plenty of explaining to do. During the crisis, their actions have shaped the behaviour of pretty much every financial market and institution on the planet. So central banks’ words resonate as never previously. Rarely a day passes without a forensic media and market dissection of some central bank comment. […]

Where does this leave central banks today? We are not in Kansas any more. On monetary policy, we have gone from setting short safe rates to shaping rates of return on longer-term and wider classes of assets. On regulation, central banks have gone from spectator to player, with some granted micro-prudential as well as macro-prudential regulatory responsibilities. On operational matters, central banks have gone from market-watcher to market-shaper and market-maker across a broad class of assets and counterparties. On transparency, we have gone from blushing introvert to blooming extrovert. In short, central banks are essentially unrecognisable from a quarter of a century ago.

This makes me feel slightly unconfortable and instantly remind me of the – now classic – 2010 article by Jeff Hummel: Ben Bernanke vs. Milton Friedman: The Federal Reserve’s Emergence as the U.S. Economy’s Central Planner. While I believe there are a few inaccuracies and omissions in Hummel’s description of the financial crisis, his article is really good and his conclusion even more valid today than at the time of his writing:

In the final analysis, central banking has become the new central planning. Under the old central planning—which performed so poorly in the Soviet Union, Communist China, and other command economies—the government attempted to manage production and the supply of goods and services. Under the new central planning, the Fed attempts to manage the financial system as well as the supply and allocation of credit. Contrast present-day attitudes with the Keynesian dark ages of the 1950s and 1960s, when almost no one paid much attention to the Fed, whose activities were fairly limited by today’s standard. […]

As the prolonged and incomplete recovery from the recent recession suggests, however, the Fed’s new central planning, like the old central planning, will ultimately prove an unfortunate and possibly disastrous failure.

The contrast between central bankers’ (including Haldane’s) beliefs of a tightly controlled financial sector to those of Hummel couldn’t be starker.

Where it indeed becomes really worrying is that Hummel was only referring to Bernanke’s decision to allocate credit and liquidity facilities to some particular institutions, as well as to the multiplicity of interest rates and tools implemented within the usual central banking framework. At the time of his writing, macro-prudential policies were not as discussed as they are now. Nevertheless, they considerably amplify the central banks’ central planner role: thanks to them, central bankers can decide to reduce or increase the allocation of loanable funds to one particular sector of the economy to correct what they view as financial imbalances.

Moreover, central banks are also increasingly taking over the role of banking regulator. In the UK, for instance, the two new regulatory agencies (FCA and PRA) are now departments of the Bank of England. Consequently, central banks are in charge of monetary policy (through an increasing number of tools), macro-prudential regulation, micro-prudential regulation, and financial conduct and competition. Absolutely all aspects of banking will be defined and shaped at the central bank level. Central banks can decide to ‘increase’ competition in the banking sector as well as favour or bail-out targeted firms. And it doesn’t stop here. Tighter regulatory oversight is also now being considered for insurance firms, investment managers, various shadow banking entities and… crowdfunding and peer-to-peer lending.

Hummel was right: there are strong similarities between today’s financial sector planning and post-WW2 economic planning. It remains to be seen how everything will unravel. Given that history seems to point to exogenous origins of financial imbalances (whereas central bankers, on the other hand, believe in endogenous explanations, motivating their policies), this might not end well… Perhaps this is the only solution though: once the whole financial system is under the tight grip of some supposedly-effective central planner, the blame for the next financial crisis cannot fall on laissez-faire…

Lars Christensen on Yellen and bubbles, and UK regulators at full speed

Lars Christensen published a sarcastic post on his blog, which coincidentally treats the monetary policy and bubbles problem as the same time as my previous post. I fully agree with him that Yellen’s comments are ridiculous.

This is Lars:

it seems to part of a growing tendency among central bankers globally to be obsessing about “financial stability” and “bubbles”, while at the same time increasingly pushing their primary nominal targets in the background.

While I agree with Lars that central banks should provide ‘nominal stability’, I don’t think inflation targeting provides such framework (and I believe Lars agrees). Inflation is very hard to measure, let alone to define, and can be very misleading (Scott Sumner believes that inflation indicators are meaningless). According to a Wicksellian framework, it does look like something’s wrong with interest rates at the moment. Banking regulation, due to its roles in ‘channelling’ interest rates, surely also plays a big role that monetary policy cannot influence. In the end, maintaining inflation right on target is in no way insurance of actual nominal (and financial) stability.

David Beckworth, in a new paper published a few days ago, also criticised inflation targeting on the ground that it contributes to financial instability. I agree with Market Monetarists that a policy stabilising NGDP growth would provide a more robust economy and financial system, though it is in my view still imperfect (I’ll come back to that in another post).

Totally unrelated: in the UK, regulators are working at full speed. Here is a summary of some of the latest regulatory announcements:

- Regulators believe that asset managers ‘waste’ too much client money on sell-side analysts research and want to regulate the process, risking to transform the market into an oligopoly as smaller research providers may not be able to cope with the reduced fee-generation (see here and here)

- HMRC wants to get the power to access your bank account and check your spending habits without going through court to make sure that you are able to pay the taxes they claim you owe them (even if they are wrong). I have personally dealt many times with HMRC (I didn’t owe them money, they did) and the least I can say is that it wasn’t necessarily a pleasant experience: waiting 45min on the phone to end up speaking to someone who sounds very suspicious that you are trying to trick tax authorities… (to be fair, I also ended up speaking to competent and pleasant people) HMRC makes mistakes all the time and I would be very cautious in granting them such powers… (see here and here)

- New rules capping the fees payday lenders can charge are effectively about to kill a large number of them… It probably won’t help much (see here)

- Bank account holders aren’t taking advantage of the best offers available to them and don’t spend their time constantly changing bank to get the best pricing and as a result earn poor returns? The regulator also wants to change that, though I submit that it should tell his boss (the BoE) that, if savers indeed earn poor returns, it possibly is because rates aren’t very high… (see here)

- The BoE and PRA want global banking regulators to reduce RWAs or capital requirements for small banks. Not saying this is a bad thing, but this sounds kind of contradictory to me, given everything we’ve been hearing for years from the same regulators… (see here)

Vince Cable realises too late what banking regulation involves

Back from holidays, and a lot of things to cover…

Let’s start with Vince Cable, Britain’s Secretary of State for Business, who is making a U-turn, though not yet quite finished, as he progressively realises how much he ignored about the pernicious effects of banking regulation.

The way the regulatory system operates has undoubtedly had a suffocating effect on business lending and particularly on our exporters.

Not surprisingly, the result is that banks pump out lending in the mortgage market, while lending to small businesses is restricted. This directly stems from the rules on which the regulatory model is based and has had a very damaging impact.

You may well recognise that he is referring to risk-weighted assets (RWAs), which have been a recurrent theme of this blog (and the focus of my three latest posts). Vince Cable had already sparked controversy pretty much exactly a year ago, when he first attacked the BoE for being a ‘capital Taliban’:

One of the anxieties in the business community is that the so called ‘capital Taliban’ in the Bank of England are imposing restrictions which at this delicate stage of recovery actually make it more difficult for companies to operate and expand.

This is a welcome reaction by one of the country’s top politician. However, let’s go back a few years to find the same Mr Cable vehemently supporting the exact same reforms he now criticises, while fully rejecting bankers’ claims that increased capital requirements would allocate funding away from SMEs (see here, here, here, here and here):

Banks and industry groups have argued more regulation could force institutions to curb lending to small- and medium-sized businesses at a time when the economy is slowing.

Prediction which turned out to be correct.

Mr Cable’s went from blaming banks for the crisis and justifying stronger regulatory requirements to blaming those same requirements for the weak level of business lending in the UK. Unfortunately, his U-turn isn’t fully completed and Mr Cable attacks the wrong target. Capital requirements are defined in Basel, the Swiss city. And he supported them in the first place, without evidently knowing what those rules involved. He also seemingly showed a poor understanding of banking history as his support for banking insulation through ring-fencing demonstrated (though most regulators are to blame as well).

Better late than never? Perhaps, but probably too late to have any effect going forward… Politicians’ and regulators’ rush to design banking rules in order to please the public opinion is making everyone worse off in the end.

Photo: Rex Features

The BoE’s FLS delusion

The Bank of England reported yesterday the latest statistics of one of its flagship measures, the Funding for Lending Scheme. Unsurprisingly, they are disappointing. No, more than that actually: the FLS has been pretty much useless.

When launched mid-2012, the FLS was supposed to offer cheap funding to British banks in exchange for increased business and mortgage lending (though originally, authorities strongly emphasised SMEs in their PR as you can imagine) in order to ‘stimulate the economy’. The only effect of the scheme was to boost… mortgage lending.

The BoE, unhappy, decided to refocus the scheme on businesses (including SMEs) only, in November last year. Well, as I predicted, it was evidently a great success: in Q114, net lending to businesses was –GBP2.7bn and net lending to SMEs was –GBP700m. Since the inception of the scheme, business lending has pretty much constantly fallen (see chart below).

According to the FT:

Figures from the British Bankers’ Association showed net lending to companies fell by £2.3bn in April to £275bn, the biggest monthly decline since last July.

The BoE argues that we don’t know what would have happened without the scheme. Perhaps lending would have fallen even more? That’s a poor argument for a scheme that was supposed to boost lending, not merely reduce its fall. Not even all large UK banks participated in the scheme (HSBC and Santander didn’t). Moreover, some banks withdrew only modest amounts because they could already access cheaper financial markets by issuing covered bonds and other secured funding instruments, or, if they couldn’t, used the FLS to pay off existing wholesale funding rather than increase lending… The FLS funding that did end up being used to lend was effective in boosting… the mortgage lending supply.

The UK government has also ‘urged’ banks to extend more credit to SMEs. Still, nothing is happening and nobody seems to understand why. For sure, low demand for credit plays a role as businesses rebuild their balance sheet following the pre-crisis binge. Still, nobody seems to understand the role played by current regulatory measures. Central bankers are supposed to understand the banking system. The fact that they seem so oblivious to such concepts is worrying.

On the one hand, you have politicians, regulators and central bankers trying to push bankers to lend to SMEs, which often represent relatively high credit risk. On the other hand, the same politicians, regulators and central bankers are asking the banks to… derisk their business model and increase their capitalisation. You can’t be more contradictory.

The problem is: regulation reflects the derisking point of view. Basel rules require banks to increase their capital buffer relatively to the riskiness of their loan book; riskiness measures (= risk-weighted assets) which are also derived from criteria defined by Basel (and ‘validated’ by local regulators when banks are on an IRB basis, i.e. use their own internal models).

Those criteria require banks to hold much more capital against SME exposures than against mortgage ones. Banks that focus on SMEs end up squeezed: risk-adjusted SME lending return is not enough to generate the RoE that covers the cost of capital on a thicker equity base. Banks’ best option is to reduce interest income but reduce proportionally more their capital base to generate higher RoEs. Apart from lending to sovereigns and sovereign-linked entities, the main way they can currently do that is to lend… secured on retail properties…

(I have already described here how this process creates misallocation of capital and possibly business cycles)

As such, it is unsurprising that mortgage lending never turned negative in the UK (even a single month) throughout the crisis. Even credit card exposures haven’t been cut by banks, as their risk-adjusted returns were more beneficial for their RoE than SMEs’. Furthermore, alternative lenders, who are not subject to those capital requirements, actually see demand for credit by SMEs increase (see also here).

Let’s get back to the 29th of November 2013. At that time, after it was announced that the FLS would be modified, I declared:

RWAs are still in place! Mortgage and household lending will still attract most of lending volume as it is more profitable from a capital point of view.

Well…

As long as those Basel rules, which have been at the root of most real estate cycles around the world since the 1980s, aren’t changed, SMEs are in for a hard time. And economic growth too in turn. Secular stagnation they said?

PS: this topic could easily be linked to my previous one on intragroup funding and regulators “killing banking for nothing”. Speaking of the ‘death of banking’, Izabella Kaminska managed to launch a new series on this very subject without ever saying a word about regulation, which is the single largest driver behind financial innovations and reshaped business models. I sincerely applaud the feat.

PPS: The FT reported how far regulators (here the FCA) are willing to go to reshape banking according to their ideal: equity research in the UK is in for a pretty hard time. This is silly. Let investors decide which researchers they wish to remunerate. Oversight of the financial sector is transforming into paternalism, if not outright regulatory threats and uncertainty.

PPS: I wish to thank Lars Christensen who mentioned my blog yesterday and had some very nice comments about it.

Is regulation killing banking… for nothing? The importance of intragroup funding

Last week, Barclays, the large UK-based bank, announced massive job cuts and asset reductions in its investment banking division which effectively signal the end of its ambition to compete with Tier 1 US banks. One of the main causes of that withdrawal is clear: regulations now make it a lot more costly to sustain capital market activities as Basel 3 has increased market risk capital requirements. But also, UK-specific rules, which advocate a ring-fencing of retail activities, also played a role in disadvantaging British banks. By ring-fencing retail banks from their sister investment ones, banks have to set up separate funding structures and look for separate funding sources, which makes it more expensive to fund investment banking divisions. Some would say that this is a good thing, as investment banking is “risky and caused the crisis”. This is wrong. In the UK and most of the world, it is mostly retail banks that failed as their asset quality strongly declined following the lending boom*.

This clampdown on investment banking is unfortunate, but wouldn’t undermine the whole banking system by itself. Regrettably, all aspects of banking are now being revisited and harmonised to please ‘out of control’ (in the words of one of my friends) regulators. Often though, the measures they take actually make banks weaker.

A brand new study published last month by the Bank of England itself (does the BoE read its own reports?) highlighted this very contradiction (see summarised post on Vox). What did it find?

The left-hand side panel of Figure 3 shows that interbank funding fell on average across our sample of BIS reporters by almost 30% between September 2008 and the end of 2009. Yet, in contrast, intragroup funding increased in the immediate aftermath of the collapse of Lehman Brothers and was stable for the remainder of the crisis period.

The contrasting behaviour of interbank and intragroup flows is not limited, however, to the recent global financial crisis. To see this, in the right-hand side panel of Figure 3, we present the distributional relationship across time between cross-border bank-to-bank funding and the VIX index.

We find that on average, between 1998 and 2011, interbank funding contracted by 2% during quarters when the VIX index was at an elevated level (upper-25th percentile), while during the same quarters intragroup funding expanded by over 2%. In the quarters when the VIX index was particularly low (lower-25th percentile), both intragroup and interbank funding expanded by approximately 4%.

This is self-explanatory. Globalisation of banking led to increased stability of funding flows. Local subsidiaries with excess liquidity were able to transfer some reserves to sister subsidiaries in other countries (or within the same country) and parent banks were also able to retrieve some of those excess funds in case they were under pressure at home. Banking system whose interbank funding comprises high share of intragroup experienced much lower drop in funding during the crisis**.

But, wait a minute… What’s the current regulatory logic? In the UK, the goal of ring-fencing is clear: ‘insulation’ (see the UK Commission report on banking reform). Globally, Basel 3 regulations now require each subsidiary of international banking groups to hold high levels of liquid assets and comply with a Net Stable Funding Ratio. By itself, this means that subsidiaries have a limited power to transfer liquidity intragroup even if they don’t need it at a given moment. Only liquidity/funding in excess of those (already high) limits could be transferred. In theory, local regulators can decide to supersede the original Basel framework. In practice, regulators are often reluctant to allow cross-border intragroup support, as they narrowly focus on their own national banking system and actually raise extra barriers, including capital controls. This happened during the crisis and potentially made it worse. This is what a BIS survey reported:

Respondents indicated that in some jurisdictions a banking parent can easily and almost without limit support its subsidiaries provided the parent continues to meet its liquidity standards. However, banking subsidiaries face legal lending limits on the amount of liquidity they can upstream to their parent even when they have excess liquidity.

Certain respondents claimed that these legal lending limits are inefficient when managing the liquidity and funding position of a banking group overall and advised that they expect future banking regulation to further institutionalise these inefficiencies. As such, in their view, subsidiaries will need a liquidity buffer for their own positions that the greater group is not able to use.

Furthermore, since the survey, financial nationalism has increased. As Bloomberg reported in February:

The Federal Reserve approved new standards for foreign banks that will require the biggest to hold more capital in the U.S., joining other countries in erecting walls around domestic financial systems.

In turn, European regulators threatened to retaliate… In short, regulators throughout the world, in an attempt to make their own financial system safer, are raising barriers and fragmenting the global financial system. But as this new research demonstrates, reducing the ability of banking groups to move funds around is weakening both global and domestic financial systems, not strengthening them.

I find bewildering that regulators don’t seem to get that logic. Let’s imagine that Bank X, based in the UK, has a subsidiary that shares the same name in the US. The US authorities believe that by making the US-based subsidiary stronger it will make it less likely to fail. Fair enough. Let’s now imagine that Bank X in the UK is experiencing difficulties and need to recover some funds located in its US sub to ensure its survival. Unfortunately, US rules prevent this transfer and Bank X effectively collapses. Do US regulators really believe that the US sub will remain untouched? Even if looking solid locally, this sub suffers massive reputational and operational damages from the collapse of its parent. This is likely to trigger a downward spiral, if not an outright bank run on those US operations. The original goal of the US authorities was thus self-defeating.

While such regulations can indeed make domestic subsidiaries look stronger, this isn’t the case on a consolidated basis. We have another fallacy of composition example here. None of those regulatory requirements can ever make banks fully crisis-proof. Consequently, when a truly large crisis strikes, healthy banks won’t be able to support their struggling sister banks, which can potentially even endanger their own existence through indirect contagion.

Even during non-crisis times, banks, and in turn economies, get penalised by those measures as banks’ cost of funding rises to reflect the inherent higher riskiness of each subsidiary/parent companies, making credit either more scarce and/or expensive.

Coincidentally, I am currently reading Fragile by Design, a new book by Calomiris and Haber, which argues that nations’ political frameworks influence the design of local banking systems and that some political arrangements (including the one in the US) are more prone to banking collapses. I guess current events are proving them right…

There are other, ‘counterintuitive’, solutions to stability in banking (which, guess what, involve less government intervention in banking, not more). Unfortunately, what we are currently witnessing is the sacrifice of competition in banking on the altar of instability… In the end, everybody loses.

* I should add that a lot of losses in investment banking divisions actually emanated from structured products (RMBS, CDOs) based on… dodgy retail lending. Nonetheless, those losses were marked-to-market and only few structured products outright defaulted (see also here). But mark-to-market losses, even when temporary, are enough to make a bank insolvent, according to current IFRS and US GAAP accounting rules.

** I am however a little curious about the claim of the authors that this result contradicts economic theory. I don’t know what ‘economic theory’ they are referring to, but those results look fully logical to me. Banking groups know what part of the group lacks liquidity. Because of reputational reasons, they have a clear incentive to transfer extra liquidity to struggling subsidiaries/divisions/holding companies. Letting a part of the group collapse is likely to trigger a dangerous chain reaction for the whole group.

Update: I modified the title of this post to more accurately reflect the content and the follow-up posts

Mobile banking keeps growing, payday lenders perhaps not so much anymore

The Fed published last week a new mobile banking survey in the US. Here are the highlights: 33% of all mobile phone owners have used mobile banking over the past twelve months, up from 28% a year earlier. When only considering smartphones, those figures increased to 51% and 48% respectively, with 12% of mobile users who plan to move on to mobile banking soon. 39% of the ‘underbanked’ population used mobile banking over the period. Checking balances, monitoring transactions and transferring money are the most common activities.

Still more than half of mobile users who do not currently use mobile banking are reluctant to use it in the future though. But usage is correlated with age. 18 to 29yo users represent 39% of all mobile banking users but only 21% of mobile phones users, whereas 45 to 60yo represent 27% of mobile banking users but 53% of mobile users. I am indeed not surprised by those results, and, as I have described in a previous post, as current young people age, the bank branch will slowly disappear and mobile banking become the norm. (Bloomberg published an article on the end of the bank branch yesterday)

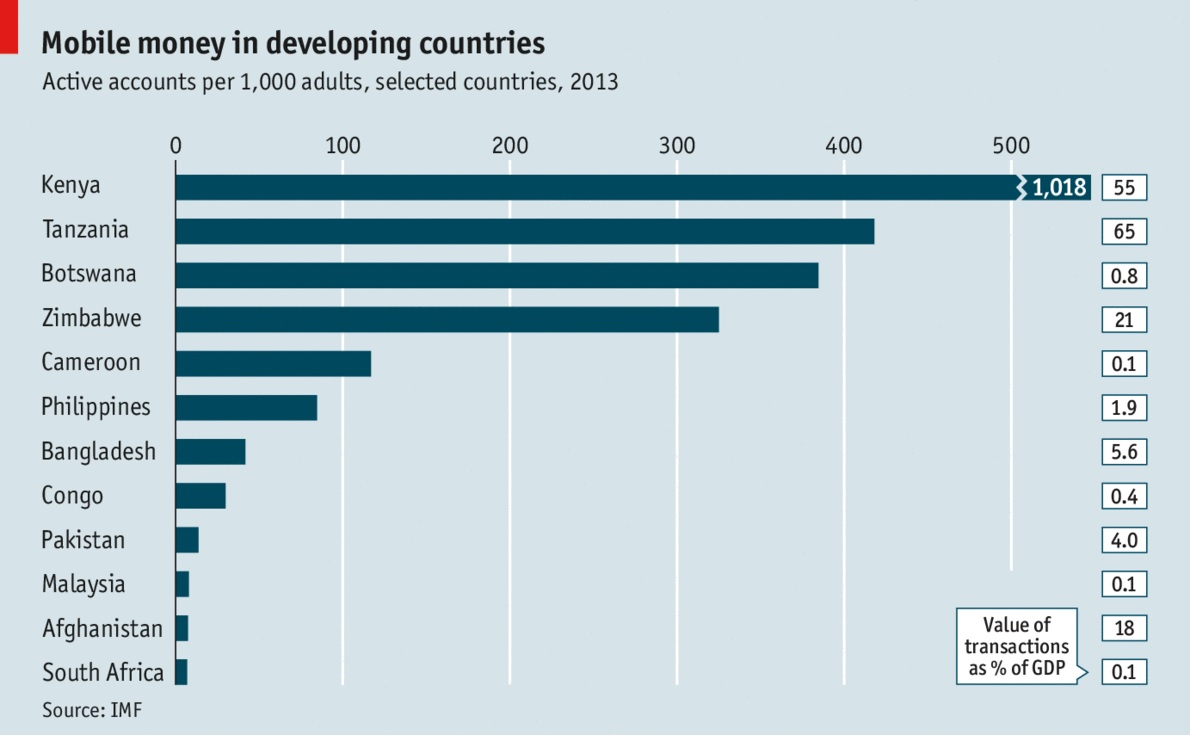

That the underbanked naturally benefit from mobile banking isn’t surprising, and isn’t new at all. The widespread use of the M-Pesa system in Kenya rested on the fact that a very large share of the population had no or limited access to banking services. However, some African countries with slightly more developed banking systems are resisting the introduction of mobile money in order not to interfere with the business as usual of the local incumbent banks. Another case of politicians and regulators acting for the greater good of their country. Anyway, mobile money/banking is now instead making its way to… Romania, as almost everyone there owns a mobile phone but more than a third of the population does not have access to conventional banking.

Meanwhile, in the UK, the regulators are doing what they can to clamp down on payday lenders. As I have described in a previous post, the result of this move is only likely to prevent underbanked people from accessing any sort of credit, as other regulations seriously limit mainstream banks’ ability to lend to those higher-risk customers.

Here again, the Fed mobile banking survey is quite enlightening. They asked underbanked people their reasons for using payday lenders. Here are their answers:

Right… So what are the consequences when you prevent people from temporarily borrowing small amount of cash that their bank aren’t willing to provide and who need it to pay for utility bills or buying some food or for any other emergency expenses? It looks like regulators believe that those families would indeed be better off not being able to pay their water bills.

Of course, over-borrowing is an issue (as are abuse and fraud), but regulators are merely clamping down on symptoms here. Society is confronted with a dilemma: either those households are unable to pay their bills or buy enough food, or they might face over-indebtedness… None of those two options are attractive. But in such a situation, it is customers’ responsibility to choose. If they can avoid payday lenders, so they should. If they really can’t, this option should remain on the table. Sam Bowman from the Adam Smith Institute made very good comments on BBC radio Wales earlier today (see here from 02:05:00) on this topic.

I know I am repeating myself, but you cannot regulate problems away.

Recent Comments