A central banker contradiction?

Last week, Mark Carney, the governor of the Bank of England, was at Cass Business School in London for the annual ‘Mais Lecture’. Coincidentally, I am an alumnus of this school. And I forgot to attend… Yes, I regret it.

Carney’s speech was focused on past, current, and future roles of the BoE. In particular, Carney mentioned the now famous monetary and macroprudential policies combination. It’s a classic for central bankers nowadays. They all have to talk about that.

In January, Andrew Haldane, a very wise guy and one my ‘favourite’ regulators, also from the BoE, made a whole speech about the topic. As Jens Weidmann, president of the Bundesbank, did in February.

I am not going to come back to the all the various possible problems caused and faced by macroprudential policies (see here and here). However, there seems to be a recurrent contradiction in their reasoning.

This is Carney:

The transmission channels of monetary and prudential policy overlap, particularly in their impact on banks’ balance sheets and credit supply and demand – and hence the wider economy. Monetary policy affects the resilience of the financial system, and macroprudential policy tools that affect leverage influence credit growth and the wider economy. […]

The use of macroprudential tools can decrease the need for monetary policy to be diverted from managing the business cycle towards managing the credit cycle. […]

That co-ordination, the shared monitoring of risks, and clarity over the FPC’s tools allows monetary policy to keep Bank Rate as low as necessary for as long as appropriate in order to support the recovery and maintain price stability. For example expectations of the future path of interest rates – and hence longer-term borrowing costs – have not risen as the housing market has begun to recover quickly.

First, it is very unclear from Carney’s speech what the respective roles of monetary policy and macroprudential policies are. He starts by saying (above) that “monetary policy affects the resilience of the financial system”, then later declares “macroprudential policy seeks to reduce systemic risks”, which is effectively the same thing. At least, he is right: both policy frameworks overlap. And this is the problem.

This is Haldane:

In the UK, the Bank of England’s Monetary Policy Committee (MPC) has been pursuing a policy of extra-ordinary monetary accommodation. Recently, there have been signs of renewed risk-taking in some asset markets, including the housing market. The MPC’s macro-prudential sister committee, the Financial Policy Committee (FPC), has been tasked with countering these risks. Through this dual committee structure, the joint needs of the economy and financial system are hopefully being satisfied.

Some have suggested that having monetary and macro-prudential policy act in opposite directions – one loose, the other tight – somehow puts the two in conflict [De Paoli and Paustian, 2013]. That is odd. The right mix of monetary and macro-prudential measures depends on the state of the economy and the financial system. In the current environment in many advanced economies – sluggish growth but advancing risk-taking – it seems like precisely the right mix. And, of course, it is a mix that is only possible if policy is ambidextrous.

Contrary to Haldane, this does absolutely not look odd to me…

Let’s imagine that the central bank wishes to maintain interest rates at a low level in order to boost economic activity after a crisis. After a little while, some asset markets start looking ‘frothy’ or, as Haldane says, there are “renewed signs of risk-taking.” Discretionary macroprudential policy (such as increased capital requirements) is therefore utilised to counteract the lending growth that drives those asset markets. But there is an inherent contradiction here: one of the goals that low interest rates try to achieve is to boost lending growth to stimulate the economy…whereas macroprudential policy aims at…reducing it. Another contradiction: while low interest rates tries to prevent deflation from occurring by promoting lending and thus money supply growth, macroprudential policy attempts to reduce lending, with evident adverse effects on money supply and inflation…

Central bankers remain very evasive about how to reconcile such goals without entirely micromanaging the banking system.

I guess that the growing power of central bankers and regulators means that, at some point, each bank will have an in-house central bank representative that tells the bank who to lend to. For social benefits of course. All very reminiscent of some regions of the world during the 20th century…

Weidman is slightly more realistic:

We have to acknowledge that in the world we live in, macroprudential policy can never be perfectly effective – for instance because safeguarding financial stability is complicated by having to achieve multiple targets all at the same time.

Indeed.

Photograph: Intermonk

The BoE says that money is endo, exo… or something

The Bank of England just published an already very controversial paper, titled “Money creation in the modern economy”. Scott Sumner, Nick Rowe, Cullen Roche, Frances Coppola, JKH, and surely others have already commented on it. Some think the BoE is wrong, some, like Frances, think that this confirms that “the money multiplier is dead”. Some think that the BoE endorses an endogenous money point of view. Many are actually misreading the BoE paper.

To be fair, this might not even be an official BoE report, and might only reflect the views of some of its economists. That type of paper is published in many institutions.

I am unsure what to think about this piece… They seem to get some things right and some other things wrong, and even in contradiction to other things they say. Overall, it is hard to reconcile. What I read was a piece written by economists. Not by banks analysts or market participants. Therefore, some ‘ivory tower’ ideas were present, though in general the paper was surprisingly quite realistic.

I have also been left with a weird feeling. I might be wrong, but almost the whole ‘Limits on how much banks can lend’ section really seems to be paraphrasing my two relatively recent posts on the topic (here, where I criticise the MMT version of endogenous money theory, and here, where I respond to Scott Fullwiller). The paper does say that

The limits to money creation by the banking system were discussed in a paper by Nobel Prize winning economist James Tobin and this topic has recently been the subject of debate among a number of economic commentators and bloggers. (emphasis added)

Indeed…

Contrary to what some seem to believe, the BoE does not endorse a fully endogenous view of the monetary system, and certainly not an MMT-type endogenous money theory.

Let me address point by point what I think they got wrong or contradictory (I am not going to address the points in the QE section, which simply follow the mechanism described in the first section of the paper).

- First, there seems to be an absolute obsession with differentiating the ‘modern’ from the ‘pre-modern’ banking and monetary system. The paper keeps repeating that

in reality, in the modern economy, commercial banks are the creators of deposit money. (page 2)

Well… You know what, guys? It was already the case in the pre-fiat money era… Banks also created broad money on top of gold reserves, thereby creating deposits, the exact same way they now do it on top of fiat money reserves. The only difference is the origins of the reserves/monetary base.

- They very often refer to Tobin’s ‘new view’. But they never mention Leland Yeager, who strongly criticised Tobin’s theory in his article ‘What are Banks?’ As a result, their view is one-sided.

- The point that “saving does not by itself increase the deposits or ‘funds available’ for banks to lend” (page 2) is slightly misinterpreted. By not saving, and hence, consuming, customers are likely to maintain higher real cash balances, leading to a reserve drain. Moreover, even if no reserve drain occurs, banks end up with a much less stable funding structure, that does not make it easier to undertake maturity transformation. It is always easier to lend when you know that your depositors aren’t going to withdraw their money overnight. This is also in contradiction with their later point that

banks also need to manage the risks associated with making new loans. One way in which they do this is by making sure that they attract relatively stable deposits to match their new loans, that is, deposits that are unlikely or unable to be withdrawn in large amounts. This can act as an additional limit to how much banks can lend. (page 5)

- In their attempt to attack the money multiplier theory, they mistakenly say that the theory assumes a constant ratio of broad money to base money (page 2). There is nothing more wrong. What the money multiplier does is to demonstrate the maximum possible expansion of broad money on top of the monetary base. The theory does not state that banks will always, at all times, thrive to achieve this maximum expansion. I still find surreal that so many clever people cannot seem to understand the difference between ‘potentially can’ and ‘always does’. Moreover, the BoE economists once again contradict themselves, when on pages 3 and 5 to 7 they essentially describe a pyramiding system akin to the money multiplier theory!

- The paper also keeps mistakenly attacking the money multiplier theory and reserve requirements while entirely forgetting all the successful implementations of reserve requirement policies by central banks throughout the world (China, Turkey, Brazil…).

- The ‘banks lend out their reserves’ misconception is itself misconceived. I strongly suggest those BoE economists to read my recent post on this very topic. Here again this is in opposition with their later point that individual banks can suffer reserve drains and withdrawals through overlending…

- The ‘Limits on how much banks can lend’ section is very true (though I might be biased given how similar to my posts this section is), and I appreciate the differentiation between individual banks and the system as a whole, differentiation that I kept emphasizing in my various posts and that I believe is absolutely crucial in understanding the banking system. Nonetheless, while their description of the effects of over-expanding individual banks and what this implies for broad money growth is accurate, it is less so in regards to the system as a whole. Indeed, they seem to believe that all banks could expand simultaneously, resulting in each bank avoiding adverse clearing and loss of reserves. This situation cannot realistically occur. Each bank wishes to have a different risk/return profile. As a result, banks with different risk profile would not be expanding at the exact same time, resulting in the more aggressive ones losing reserves at the expense of the more conservative ones in the medium term, stopping their expansion. At this point, we get back to the case I (and they) made of what happens to over-expanding single banks.

- Finally, despite describing a banking system in which lending is built up on top of reserves (pages 3 and 4) and in which banks cannot over-expand due to reserve drains (pages 5 and 6), they still dare declaring that:

In reality, neither are reserves a binding constraint on lending, nor does the central bank fix the amount of reserves that are available. (page 2) (emphasis added)

I just don’t know what to say…

What do we learn from this piece? For one thing, those BoE economists do not believe in the endogenous money theory. This is self-explanatory in the mechanism described in pages 5 and 6. They clearly know that an individual bank cannot expand broad money by itself. They seem to admit that the central bank does not have the ability to provide reserves on demand (despite saying a couple of times that the BoE supplies them on demand, another apparent contradiction). Their only qualification is that this can happen when all banks simultaneously expand their lending. This is theoretically true but impossible in practice as I said above.

Why would the central bank not have the ability to provide those reserves on demand? Actually, it can. It’s just that there is no (or low) demand for those reserves. This is due to the central bank funding stigma, an absolutely key factor that is not referred to even once in this BoE paper. As a result, their description seems to lack something: if individual banks lack reserves to expand further, why aren’t they simply borrowing them from the central bank? By overlooking the stigma, their mechanism lacks a coherent whole.

This is how things work (in the absence of innovations that economise on reserves): money supply expansion is endogenous in the short-term. But any endogenous expansion will also lead to an endogenous contraction in the short-term. In the long-term, only an increase in the monetary base can expand broad money. Only central bank injections free of any stigma, such as OMO, can sustainably expand the monetary base by swapping assets for reserves without touching at banks’ funding structure.

I have a minor qualification to add to this mechanism though. The endogenous contraction does not necessarily always occur around the same time. A period of economic euphoria could well lead to lower risk expectations, allowing banks to reshape their funding structure and the liquidity of their balance sheet in a riskier way than usual before the natural contractionary process kicks in.

In the end, the few ‘ivory tower’ ideas that are present in this research paper make it look incoherent and internally inconsistent. Central banks are notorious for their intentional or unintentional twisting of economic reality and history (see this brand new article by George Selgin on the Fed misrepresenting its history and performance. Brilliant read), so we should always take everything they say with a pinch of salt.

Is the zero lower bound actually a ‘2%-lower bound’?

Following my recent reply to Ben Southwood on the relationship between mortgage rates, BoE base rate and banks’ margins and profitability (see here and here), a question came to my mind: if the BoE rate can fall to the zero lower bound but lending rates don’t, should we still speak of a ‘zero lower bound’? It looks to me that, strictly in terms of lending and deposit rates, setting the base rate at 0% or at 2% would have changed almost nothing at all, at least in the UK.

The culprit? Banks’ operational expenses. Indeed, it looks like the only way to break through the ‘2%-lower bound’ would be for banks to slash their costs…

Let’s take a look at the following mortgage rates chart from one of my previous posts:

From this chart, it is clear that lowering the BoE rate below around 2.5% had no further effect on lowering mortgage rates. As described in my other posts, this is because banks’ net interest income necessarily has to be higher than expenses for them to remain profitable. When the BoE rate falls below a certain threshold that represents operational expenses, banks have to widen the margins on loans as a result.

From this chart, it is clear that lowering the BoE rate below around 2.5% had no further effect on lowering mortgage rates. As described in my other posts, this is because banks’ net interest income necessarily has to be higher than expenses for them to remain profitable. When the BoE rate falls below a certain threshold that represents operational expenses, banks have to widen the margins on loans as a result.

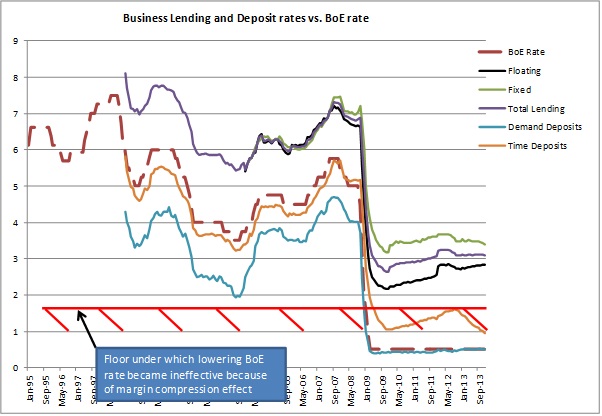

What about business lending rates? Since business lending is funded by both retail and corporate deposits (and excluding wholesale funding for the purpose of the exercise), the analysis must take a different approach. Banks don’t often disclose the share of corporate deposits within their funding base, but I managed to find a retail/corporate deposit split of 75%/25% at a large European peer, which I am going to use as a rough approximation to estimate banks’ business lending margins. Here are the results of my calculations (first chart: margin over time deposits, second chart: margin over demand deposits):

No surprise here, the same margin compression effect appears as a result of the BoE rate collapsing (as well as Libor, as floating corporate lending is often calculated on a Libor + margin basis, unlike mortgages, which are on a BoE + margin basis). Before that period, changes in the BoE and Libor rates had pretty much no effect on margins. After the fall, banks tried to rebuild their margins by progressively repricing their business loan books upward (i.e. increasing the margins over Libor).

No surprise here, the same margin compression effect appears as a result of the BoE rate collapsing (as well as Libor, as floating corporate lending is often calculated on a Libor + margin basis, unlike mortgages, which are on a BoE + margin basis). Before that period, changes in the BoE and Libor rates had pretty much no effect on margins. After the fall, banks tried to rebuild their margins by progressively repricing their business loan books upward (i.e. increasing the margins over Libor).

Here again we can identify a 1.5% BoE rate floor, under which lowering the base rate does not translate into cheaper borrowing for businesses:

This has repercussions on monetary policy. The banking/credit channel of monetary policy aims at: 1. easing the debt burden on indebted household and businesses and, 2. stimulating investments and consumption by making it cheaper to borrow. However, it seems like this channel is restricted in its effectiveness by banks’ ability in passing the lower rate on to customers. Banks’ short-term fixed cost base effectively raises the so-called zero lower bound to around 2%. The only way to make the transmission mechanism more efficient would be for banks to drastically improve their cost efficiency and have assets of good-enough quality not to generate impairment charges, which is tough in crisis times. Unfortunately, there are limits to this process, and a bank without employee and infrastructure is unlikely to lend in the first place…

This has repercussions on monetary policy. The banking/credit channel of monetary policy aims at: 1. easing the debt burden on indebted household and businesses and, 2. stimulating investments and consumption by making it cheaper to borrow. However, it seems like this channel is restricted in its effectiveness by banks’ ability in passing the lower rate on to customers. Banks’ short-term fixed cost base effectively raises the so-called zero lower bound to around 2%. The only way to make the transmission mechanism more efficient would be for banks to drastically improve their cost efficiency and have assets of good-enough quality not to generate impairment charges, which is tough in crisis times. Unfortunately, there are limits to this process, and a bank without employee and infrastructure is unlikely to lend in the first place…

Don’t get me wrong though, I am not saying that lowering the BoE rate (and unconventional monetary policies such as QE) is totally ineffective. Lowering rates also positively impact asset prices and market yields, ceteris paribus. This channel could well be more effective than the banking one but it isn’t the purpose of this post to discuss that topic. Nevertheless, from a pure banking channel perspective, one could question whether or not it is worth penalising savers in order to help borrowers that cannot feel the loosening.

PS: I am not aware of any academic paper describing this issue, so if you do, please send me the link!

A clarification on mortgage rates for ASI’s Ben Southwood

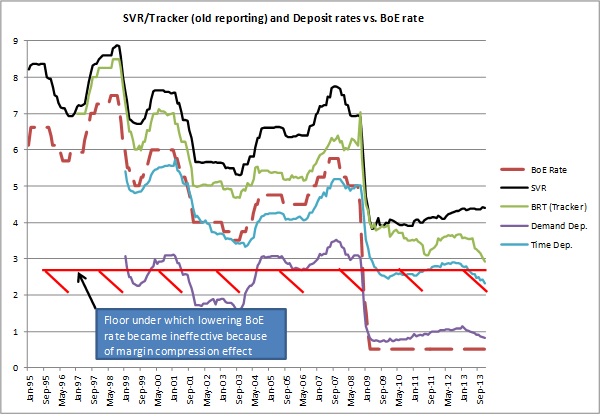

Ben Southwood from the Adam Smith Institute replied to my previous post here. I am still confused about Ben’s claim that the spread varied “widely”. As the following chart demonstrates, the margins of SVR, tracker and total floating lending over the BoE base rate remained remarkably stable between 1998 and 2008, despite the BoE rate varying from a high 7.5% in 1998 to a low of 3.5% in 2003:

Everything changed in 2009 when the BoE rate collapsed to the zero lower bound. Following his comments, I think I need to address a couple of things. Two particular points attracted my attention. Ben said:

If other Bank schemes, like Funding for Lending or quantitative easing were overwhelming the market then we’d expect the spread to be lower than usual, not much higher.

His second big point, that the spread between the Bank Rate and the rates banks charged on markets couldn’t narrow any further 2009 onwards perplexes me. On the one hand, it is effectively an illustration of my general principle that markets set rates—rates are being determined by banks’ considerations about their bottom line, not Bank Rate moves. On the other hand, it seems internally inconsistent. If banks make money (i.e. the money they need to cover the fixed costs Julien mentions) on the spread between Bank Rate and mortgage rates (i.e. if Bank Rate is important in determining rates, rather than market moves) then the absolute levels of the numbers is irrelevant. It’s the spread that counts.

It looks to me that we are both misunderstanding each other here. It is indeed the spread that counts. But the spread over funding (deposit) cost, not BoE rate! (Which seems to me to be consistent with my posts on MMT/endogenous money.) Let me clarify my argument with a simple model.

Assumptions:

- A medium-size bank’s only assets are floating rate mortgages (loan book of GBP1bn). Its only source of revenues is interest income. The bank maintains a fixed margin of 1% above the BoE rate but keeps the right to change it if need be.

- The bank’s funding structure is composed only of demand deposits, for which the bank does not pay any interest. As a result, the bank has no interest expense.

- The bank has a 100% loan/deposit ratio (i.e. the bank has ‘lent out’ the whole of its deposit base and therefore does not hold any liquid reserve).

- The bank has an operational cost base of GBP20m that is inflexible in the short-term (not in the long-term though there are upwards and downwards limits) and no loan impairment charge.

Of course this situation is unrealistic. A 100% loan/deposit bank would necessarily have some sort of wholesale funding as it needs to maintain some liquidity. It would also very likely have a more expensive saving deposit base and some loan impairment charges. But the mechanism remains the same therefore those details don’t matter.

In order to remain profitable, the bank’s interest income has to be superior to its cost base. Moreover, the bank’s interest income is a direct, linear function, of the BoE rate. The higher the rate, the higher the income and the higher the profitability. As a result, the bank’s profitability obeys the following equation:

Net Profit = Interest Income – Costs = f(BoE rate) – Costs,

with f(BoE rate) = BoE rate + margin = BoE rate + 1%.

Consequently, in order for Net Profit > 0, we need f(BoE rate) > Costs.

Now, we know that the bank’s cost base is GBP20m. The bank must hence earn more than GBP20m on its loan book to remain profitable (which does not mean that it is enough to cover its cost of capital).

The BoE rate is 2%, making the rate on the mortgage book of the bank 3%, leading to a GBP30m income and a GBP10m net profit. Almost overnight, the BoE lowers its rate to 0.5%. The bank’s loan book’s average rate is now 1.5%, and generates GBP15m of income. The bank is now making a GBP5m loss. Having inflexible short-term costs, it’s only way of getting back to profitability is to increase its margin by at least 0.5%. The bank’s net profit profile is summarised by the following chart:

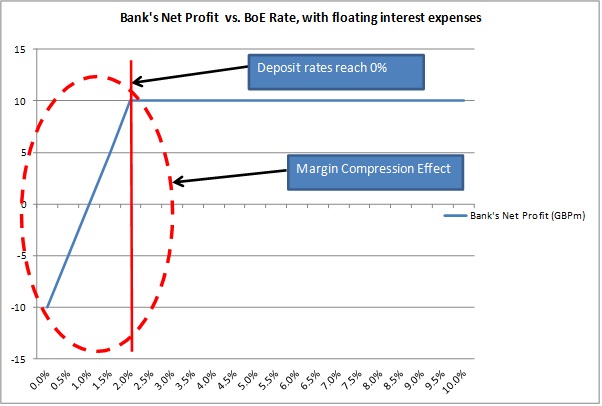

However, a more realistic bank would pay interest on its deposit base (its funding). Let’s now modify our assumptions and make that same bank entirely demand deposit-funded, remunerated at a variable rate. The bank pays BoE rate minus a fixed 2% margin on its deposit base. As a result, what needs to cover the banks operational costs isn’t interest income but net interest income. The bank’s net profit equation is now altered in the following way:

Net Profit = Net Interest Income – Costs

Net Profit = Interest Income – Interest Expense – Costs

Net Profit = f1(BoE rate) – f2(BoE rate) – Costs

with f1(BoE rate) = BoE rate + margin = BoE rate + 1%,

and f2(BoE rate) = BoE rate – margin = BoE rate – 2%.

The equation can be reduced to: Net Profit = 3% (of its loan book) – Costs, as long as BoE rate >= 2% (see below).

Let’s illustrate the net profit profile of the bank with the below chart:

What happens is clear. Independently of its effects on the demand for credit and loan defaults, the BoE rate level has no effect on the bank’s profitability. Everything changes when deposit rates reach the zero lower bound (i.e. there is no negative nominal rate on deposits), which occurs before the BoE rate reaches it. From this point on, the bank’s interest income decreases despite its funding cost unable to go any lower. This is the margin compression effect that I described in my first post. In reality, things obviously aren’t that linear but follow the same pattern nevertheless.

Realistic banks are also funded with saving deposits and senior and subordinated debt, on which interest expenses are higher. This is when schemes such as the Funding for Lending Scheme kicks in, by providing cheaper-than-market funding for banks, in order to reduce the margin compression effect. The other way to do it is to reflect a rate rise in borrowers’ cost, while not increasing deposit rates. This is highly likely to happen, although I guess that banks would only partially transfer a rate hike in order not to scare off customers.

Overall, we could say that markets determine mortgage rates to an extent. But this is only due to the fact that banks have natural (short-term) limits under which they cannot go. It would make no sense for banks not to earn a single penny on their loan book (and they would go bust anyway). Beyond those limits, the BoE still determines mortgage rates.

Although I am going to qualify this assertion: the BoE roughly determines the rate and markets determine the margin. At a disaggregated level, banks still compete for funding and lending. They determine the margins above and below the BoE rate in order to maximise profitability. They, for instance, also have to take into account the fact that an increase in the BoE rate might reduce the demand for credit, thereby not reflecting the whole increase/decrease to customers as long as it still boosts their profitability. Those are some of the non-linear factors I mentioned above. But they remain relatively marginal and the aggregate, competitively-determined, near-equilibrium margin remains pretty stable over time as demonstrated with the first chart above.

With this post I hope to have clarified the mechanism I relied on in my previous post, but feel free to send me any question you may have!

Mortgage rates are still determined by the BoE

Ben Southwood from the Adam Smith Institute wrote an interesting piece this week. I have an objection to his title and the conclusion he reached. Ben wrote:

However, it was recently pointed out to me that since a high fraction of UK mortgages track the Bank of England’s base rate, a jump in rates, something we’d expect as soon as UK economic growth is back on track, could make mortgages much less affordable, clamping down on the demand for housing.

This didn’t chime with my instincts—it would be extremely costly for lenders to vary mortgage rates with Bank Rate so exactly while giving few benefits to consumers—so I set out to check the Bank of England’s data to see if it was in fact the case. What I found was illuminating: despite the prevalence of tracker mortgages the spread between the average rate on both new and existing mortgage loans and Bank Rate varies drastically.

Wait. I really don’t reach the same conclusion from the same dataset. This is what I extracted from the BoE website (using the BoE’s old reporting format, as the new one only started in 2011):

Banks and building societies offer two main types of floating rate mortgages: standard variable rate (SVR) and trackers. Trackers usually follow the BoE rate closely. SVR are slightly different: margins above the BoE rate are more flexible. Banks vary them to manage their revenues but usually fix them for an extended period of time before reviewing them again. During the crisis, some banks that had vowed to maintain their SVR at a certain spread angered their customers when this situation became unsustainable due to low base rates. Some banks and building societies made losses on their SVR portfolio as a result and had to break their promise and increase their SVR.

What we can notice from the chart above is clear: since the mid-1990s, it is the BoE that determine both mortgage and deposit rates. Not the market. All rates moved in tandem with the BoE base rate. Still, the linkage was broken when the BoE rate collapsed to the zero lower bound in 2009. And this is probably why Ben declared that

but what is clear is that tracker mortgages be damned, interest rates are set in the marketplace.

I think this is widely exaggerated. Ben missed something crucial here: banks have fixed operational costs. Banks generate income by earning a margin between their interest income (from loans) and interest expense (from deposits and other sources of funding). They usually pay demand deposits below the BoE rate and saving/time deposits at around the BoE rate, and make money by lending at higher rates. From this net interest income, banks have to deduce their fixed costs (salaries and other administrative expenses) and bad debt provisions.

There is a problem though. Setting the BoE rate near zero involves margin compression. Banks’ back books (lending made over the previous years) on variable rates see their interest income collapse. Banks’ deposit base is stickier: many saving accounts are not on variable rates. Therefore, there is a time lag before the deposit base reprice (we can see this on the chart above: whereas lending reprices instantaneously when the BoE rate moves, deposits show a lag). Moreover, near the zero bound, the spread between demand deposit rates and the BoE rates all but disappears. The two following charts clearly illustrate this margin compression phenomenon:

It is clear that banks started to make losses when the BoE rate fell, as the margin on the floating rate back book (stock) became negative. Using the new BoE reporting would make those margins look even worse*. To offset those losses, banks started to increase the spread on new lending, leading to a spike on the interest margin of the front book (green line above). Banks can potentially reprice their whole loan book at a higher margin, but this takes time, especially with 15 to 30-year mortgages. Consequently, banks not only increased the spread on new lending, but also decided to break their SVR promises and increase their back book SVR rates (see black line in charts). This usually did not go down well with their customers, but some banks had no choice, having entered the crisis with too low SVRs.

What happens to a bank whose net interest income is negative (assuming it has no other income source)? It reports net accounting losses as it still has fixed operational expenses… Continuously depressed margins explain why banks’ RoE remains low. For banks to report net profits, their net interest income must cover (at least) both operational expenses and loan impairment charges. What Ben identified as ‘market-defined interest rates’ or the ‘spread over BoE’s rate’ from 2009 onwards is simply the floor representing banks’ operational costs, under which banks cannot go… The only other (and faster) way to rebuild banks’ bottom line would be to increase the BoE rate.

A mystery though: why didn’t banks decrease their time deposit rates further? I am unsure to have an answer to that question. A possibility is that the spread between demand and time deposits remained the same. Another possibility is that banks’ time deposit rates remained historically roughly in line with UK gilts rates. Decreasing time deposit rates much below those of gilts would provide savers with incentives to invest their money in gilts rather than in banks’ saving accounts.

What would a rate hike mean? Ben thinks it would have little impact, probably because the spread over BoE seems to show quite a lot of breathing space before the base rate impacts lending rates. I don’t think this is the case. A rate increase would likely push lending rates upwards on bank’s back book (i.e. banks are not going to reduce the spread in order to maintain stable mortgage rates). Why? Banks’ net interest margin and return on equity are still very depressed. Moreover, new Basel III regulations are forcing banks to hold more equity, further reducing RoE. Consequently, banks will seek to rebuild their margin and profitability, making customers pay higher rates to compensate for years of low rates and newly-introduced regulatory measures.

* I am unsure why the BoE changed its reporting and what the differences are, but reported lending rates are much lower than with the old reporting standards. Tracker mortgage rates even seem to be lower than time deposit rates. See below and compare with my first chart. If anybody has an explanation, please enlighten me:

Update: I replaced ‘ceiling’ with ‘floor’ in the post as it makes a lot more sense!

Update 2: Ben Southwood replies here…

Update 3: …and I replied there!

A UK housing bubble? Sam Bowman doubts it

On the Adam Smith Institute’s blog, Sam Bowman had a couple of posts (here and a follow-up here, and mentioned by Lars Christensen here) attempting to explain that there might not have been any house price bubble in the UK. He essentially says that there was no oversupply of housing in the 1990s and 2000s. Here’s Sam:

These charts show that housing construction was actually well below historical levels in the 1990s and 2000s, both in absolute terms and relative to population. It is difficult to see how someone could claim that the 2008 bust was caused by too many resources flowing toward housing and subsequently needing time to reallocate if there was no bubble in housing to begin with.

What this suggests is that the Austrian story about the crisis may be wrong in the UK (and, if Nunes’s graphs are right, the US as well). The Hayek-Mises story of boom and bust is not just about rises in the price of housing: it is about malinvestments, or distortions to the structure of production, that come about when relative prices are distorted by credit expansion.

Well, I think this is not that simple. Let me explain.

First, the Hayek/Mises theory does not apply directly to housing. In the UK, there are tons of reasons, both physical and legal, why housing supply is restricted. As a result, increased demand does not automatically translate into increased supply, unlike in Spain, which seems to have lower restrictions as shown by the housing start chart below:

Second, Sam overlooks what happened to commercial real estate. There was indeed a CRE boom in the UK and CRE was the main cause of losses for many banks during the crisis (unlike residential property, whose losses remained relatively limited).

Third, the UK is also characterised by a lot of foreign buyers, who do not live in the UK and hence not included in the population figures. Low rates on mortgages help them purchase properties, pushing up prices, triggering a reinforcing trend while supply in the demanded areas often cannot catch up.

Fourth, the impact of Basel regulations seems to be slightly downplayed. Coincidence or not, the first ‘bubble’ (in the 1980s) appeared right when Basel’s Risk Weighted Assets were introduced. And it is ‘curious’, to say the least, that many countries experienced the same trend at around the same time. Would house lending and house prices have increased that much if those rules had never been implemented? I guess not, as I have explained many times. I have yet to write posts on what happened in several countries. I’ll do it as soon as I find some time.

I recommend you to take a look at my RWA-based Austrian Business Cycle Theory, which seems to show that, while there should indeed be long-term real estate projects started (depending on local constraints of course), there is also an indirect distortion of the capital structure of the non-real estate sector.

While there may well be ‘real’ factors pushing up real estate prices in the UK, there also seems to be regulatory and monetary policy factors exacerbating the rise.

- Chart 1: Spanish Property Insight

- Chart 2: FT Alphaville

- Chart 3: Guardian

News digest (Krugman and deregulation, central banking for Bitcoin…)

A looooooooot of news since the beginning of the week. So I’ll just quickly go over a few of them. Guys please, next time, spread your news more evenly over time. There was nothing to comment on recently!

Not new news but the Swedish bank regulators are thinking of increasing RWAs on mortgages to fight a growing housing bubble. Well, raising them to 25% (from 15% floor…) would still not change much: they would remain below most other asset classes’ level and securitisation (RMBS) would allow banks to bypass the restrictions.

Meanwhile, Yves Mersch, member of the Executive Board of the ECB, spoke about how to revive SME lending in bank-reliant Europe. His solutions involve: strengthening banks, securitisation and… banking union. Any word of capital requirements/risk-weighted assets? Not a single one. When I told you that central bankers don’t seem to get it…

But the UK government wants to ditch the household lending side of the Funding for Lending Scheme! They now only want to provide cheap funding to banks if they prove that they lend to SMEs. Why not, but I doubt it would really work for a few reasons: 1. demand for loans remains quite low, 2. market funding remains cheap (it was cheaper than FLS), 3. banks haven’t drawn much on it anyway, 4. RWAs are still in place! Mortgage and household lending will still attract most of lending volume as it is more profitable from a capital point of view.

Meanwhile (again), SME financing from alternative lenders not subject to RWAs and other stupid capital rules, keeps growing in the UK. However, it is still tough for those lenders to assess the health of the companies that would like to lend to.

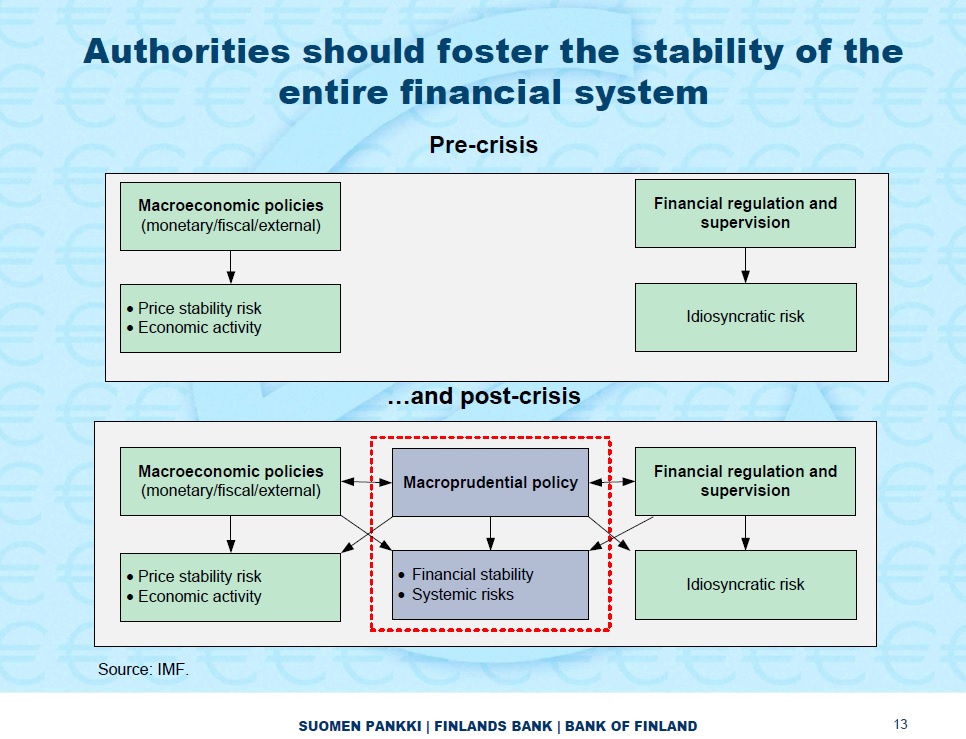

Erkki Liikanen, the Governor of the central bank of Finland, told us about his ideas to improve financial stability. Surprise: they haven’t changed. So macroprudential policy starts interfering with macroeconomic policies and financial regulation, with possibly opposite effects that don’t seem to bother him much. Look at that slide, which is the very definition of a messy policy goal, with multiple targets and interferences:

A very strange piece in the Washington Post: Bitcoin needs a central banker. Wait a second. No, it’s definitely not the 1st of April. First, the author asserts that Bitcoin’s wild changes in value make it difficult to be adopted as a currency. This is extraordinary. Does the author even understand FX rates? If the author wishes to purchase his coffee using Euros, despite the coffee being priced in Dollars, will he also declare that the fact the Euro’s value is unstable (making the effective Euro price of its coffee volatile) makes the currency improper for use? When prices are originally denominated in Bitcoin, the change in the value of the digital currency won’t affect them. When prices are actually denominated in USD, but converted into Bitcoin, then yes, changes in the value of the digital currency will affect them. But this is hardly Bitcoin’s fault… Then he gets mixed up with ‘menu costs’, ‘hyperinflation’, ‘money demand’, etc. Wow. Just one last thing: has he even understood that Bitcoin was designed to be free from central bankers and government intervention in the first place?

Izabella Kaminska in the FT wrote a new piece on Bitcoin and other alternative electronic currencies. She complains about the multiplication of such currencies that nothing backs and pretty much only see speculative motivations underlying them. I am not going to comment on the whole thing, but whether right or wrong, she should ask herself why there is such frenzy about those currencies at the moment. My guess is that, governments’ and central banks’ manipulation of their own currencies have unleashed a beast: people afraid to hold classic currencies started to look for alternatives, pushing up their prices, in turn attracting speculators. The process is similar to ‘bad’ financial innovations (the ones designed specifically to bypass restricting regulation): they often start as a benign innovation for the ‘common good’, but the surprising demand for them and large profits attract speculators until the market crashes. Not the fault of the innovation, but the fault of the regulation that triggered them…

Paul Krugman thinks that “the trouble with economics is economists”, and that mainstream economics is not to blame for the financial crisis. I partly disagree: 1. there are various schools of thought within mainstream economics that often disagree with each other altogether and 2. most (all?) of them cannot fully explain the crisis anyway. But, and this is where Krugman shows his limited knowledge of banking and therefore the limit of his reasoning, he declares that “the mania for financial deregulation, for example, didn’t come out of standard economic analysis.” I’m sorry? Which mania for financial deregulation? The international banking sector had never been as regulated in history as on the eve of the crisis! (even taking into account of the few one-off deregulations) I need to come back to this in a subsequent post. Really, Paul, you have to revise your history. And your reasoning.

On Free Banking, George Selgin urges Scots to ‘poundize’ unilaterally if ever they declare independence from the UK. And “if the British Parliament refuses to cooperate, so much the better. Who knows: Scotland could even end up with a banking system as good as the one it had before 1845, when Parliament, which knew almost as little about currency then as it does now, began to bugger it up.” If only Scotland could enlighten the world a second time and get back to a free banking system!

The EBA banks’ balance sheets assessment and the standardisation problem

About two weeks ago, the European Banking Authority announced their standard definitions of impaired loans (i.e. non-performing loans) and other asset quality standards, which aim at harmonising the various definitions in place throughout Europe for their upcoming asset quality review. Today, I won’t even be mentioning the odd fact to see a regulator getting in a bank for a few days and basically telling the bank that it knows its loan book better than the bankers themselves. No, today I will only speak about the harmonisation issue.

![]()

Banks have different ways of classifying past-due loans, impaired loans, loans in forbearance and so on, not only in between countries but also within countries. For instance, in the UK, I know some banks that will classify all loans in forbearance as impaired, artificially pushing up their headline bad loans ratio, while others do not, looking better as a result to the untrained eye. Most British banks will automatically classify loans 90 days and more in arrears as impaired, whereas most French banks will only apply the impaired definition when loans are 180 days and more in arrears.

So a standardisation seems to be a good thing as data becomes comparable. Well, it is, and it isn’t. To be fair, standardisation within a country is probably a good thing, although shareholders, investors and auditors – rather than regulators – should force management to report financial data the way they deem necessary. However, it makes a lot less sense on an international basis. Why? Countries have different cultural backgrounds and legal frameworks, meaning that certain financial ratios should not be interpreted the same way from one country to another.

Let’s take a few examples. In the US, people are much more likely than Europeans on average to walk away from their home if they can’t pay off their mortgage. Most Europeans, on the other hand, will consider mortgage repayment as priority number 1. As a result, impaired mortgage ratios could well end-up higher in the US. But US banks know that and adapt their loan loss reserves in consequence. Within Europe, legal frameworks and judiciary efficiency are also key: UK banks often set aside fewer funds against mortgage losses as the legal system allows them to foreclose and sell homes relatively quickly and with minimal losses. In France on the other hand, the process is much longer with many regulatory and legal hurdles. Consequently, UK-based mortgage banks seem to have lower loan loss reserves compared with some of their continental Europe peers. Does it mean they are riskier? Not really.

Another (abstract) example: in country A, the local culture pushes people to pay off their debt at all costs, whereas in country B, most people, once they stop paying back when they run into short-term trouble, never resume payment. In country A, banks consider it safe to classify a loan as impaired only after 180 days without payment. In country B though, banks know that the loan will never be paid off as soon as it is 30 days past due. Standardisation would make both countries use the same classification. Why not, but it doesn’t bring much: analysts will still have to take into account local variations (just in a different way). However, it might spark an unnecessary panic in country A when figures suddenly look much worse to the untrained public.

This is the issue with harmonising. Some standardisation may be welcome, but most analysts and investors already know the differences in reporting between countries and don’t take headline figures at par value, making the EBA exercise relatively pointless. For the less-well informed individuals, the EBA harmonisation could also bring a false sense of safety: figures look comparable, but in reality, they’re not entirely. In the end, harmonised reporting or not, adjustments always have to be made…

The same apply to most internationally-applied regulations. Basel rules, for example, effectively apply standardised capital and liquidity requirements throughout the world (with some local implementation differences). Banks in higher-risk countries have to comply with the same capital ratios as banks in lower-risk countries, the adjustment being made through risk-weighted assets…which are easily gamed. But analysts know well enough that a 17% regulatory Tier 1 ratio (a key bank capital safety ratio) is actually poor for an African bank, despite looking high by Western standards and way above official requirements.

In the end, standardisation makes particular sense in geographical areas where both culture and legal frameworks present only minor differences, such as the US. Europe is still a pretty fragmented continent, and it doesn’t look like things are going to change overnight. The EBA hasn’t been very clear about the exact implementation of its criteria. Let’s just hope they keep the issues discussed in this post in mind.

What Walter Bagehot really said in Lombard Street (and it’s not nice for central bankers and regulators)

(Warning: this is quite a long post as I reproduce some parts of Bagehot’s writings)

As I promised in a post a few days ago, I am today getting back to the common ancestor of all of today’s central bankers, Walter Bagehot.

Bagehot is probably one of the most misquoted economist/businessmen of all times. Most people seem to think they can just cherry pick some of his claims to justify their own beliefs or policies, and leave aside the other ones. Sorry guys, it doesn’t work like that. Bagehot’s recommendations work as a whole. Here I am going to summarise what Bagehot really said about banking and regulation in his famous book Lombard Street: A description of the Money Market.

Let’s start with central banking. As I’ve already highlighted a few days ago, Bagehot said that the institution that holds bank reserves (i.e. a central bank) should:

- Lend freely to solvent banks and companies

- Lend at a punitive rate of interest

- Lend only against good quality collateral

I can’t recall how many times I’ve heard central bankers, regulators and journalists repeating again and again that “according to Bagehot” central banks had to lend freely. Period. Nothing else? Nop, nothing else. Sometimes, a better informed person will add that Bagehot said that central banks had to lend to solvent banks only or against good collateral. Very high interest rates? No way. Take a look at what Mark Carney said in his speech last week: “140 years ago in Lombard Street, Walter Bagehot expounded the duty of the Bank of England to lend freely to stem a panic and to make loans on “everything which in common times is good ‘banking security’.”” Typical.

Now hold your breath. What Bagehot said did not only involve central banking in itself but also the banking system in general, as well as its regulation. Bagehot attacked…regulatory ratios. Check this out (chapter 8, emphasis mine):

But possibly it may be suggested that I ought to explain why the American system, or some modification, would not or might not be suitable to us. The American law says that each national bank shall have a fixed proportion of cash to its liabilities (there are two classes of banks, and two different proportions; but that is not to the present purpose), and it ascertains by inspectors, who inspect at their own times, whether the required amount of cash is in the bank or not. It may be asked, could nothing like this be attempted in England? could not it, or some modification, help us out of our difficulties? As far as the American banking system is one of many reserves, I have said why I think it is of no use considering whether we should adopt it or not. We cannot adopt it if we would. The one-reserve system is fixed upon us.

Here Bagehot refers to reserve requirements, and pointed out that banks in the US had to keep a minimum amount of reserves (i.e. today’s equivalent would be base fiat currency) as a percentage of their liabilities (= customer deposits) but that it did not apply to Britain as all reserves were located at the Bank of England and not at individual banks (the US didn’t have a central bank at that time). He then follows:

The only practical imitation of the American system would be to enact that the Banking department of the Bank of England should always keep a fixed proportion—say one-third of its liabilities—in reserve. But, as we have seen before, a fixed proportion of the liabilities, even when that proportion is voluntarily chosen by the directors, and not imposed by law, is not the proper standard for a bank reserve. Liabilities may be imminent or distant, and a fixed rule which imposes the same reserve for both will sometimes err by excess, and sometimes by defect. It will waste profits by over-provision against ordinary danger, and yet it may not always save the bank; for this provision is often likely enough to be insufficient against rare and unusual dangers.

Bagehot thought that ‘fixed’ reserve ratios would not be flexible enough to cope with the needs of day-to-day banking activities and economic cycles: in good times, profits would be wasted; in bad times, the ratio is likely not to be sufficient. Then it gets particularly interesting:

But bad as is this system when voluntarily chosen, it becomes far worse when legally and compulsorily imposed. In a sensitive state of the English money market the near approach to the legal limit of reserve would be a sure incentive to panic; if one-third were fixed by law, the moment the banks were close to one-third, alarm would begin, and would run like magic. And the fear would be worse because it would not be unfounded—at least, not wholly. If you say that the Bank shall always hold one-third of its liabilities as a reserve, you say in fact that this one-third shall always be useless, for out of it the Bank cannot make advances, cannot give extra help, cannot do what we have seen the holders of the ultimate reserve ought to do and must do. There is no help for us in the American system; its very essence and principle are faulty.

To Bagehot, requirements defined by regulatory authorities were evidently even worse, whether for individual banks or applied to a central bank. I bet he would say the exact same thing of today’s regulatory liquidity and capital ratios, which are essentially the same: they can potentially become a threshold around which panic may occur. As soon as a bank reaches the regulatory limit (for whatever reason), alarm would ring and creditors and depositors would start reducing their lending and withdrawing their money, draining the bank’s reserves and either creating a panic, or worsening it. This reasoning could also be applied to all stress tests and public shaming of banks by regulators over the past few years: they can only make things worse.

Even more surprising: the spiritual leader of all of today’s central bankers was actually…against central banking. That’s right. Time and time again in Lombard Street he claimed that Britain’s central banking system was ‘unnatural’ and only due to special privileges granted by the state. In chapter 2, he said:

I shall have failed in my purpose if I have not proved that the system of entrusting all our reserve to a single board, like that of the Bank directors, is very anomalous; that it is very dangerous; that its bad consequences, though much felt, have not been fully seen; that they have been obscured by traditional arguments and hidden in the dust of ancient controversies.

But it will be said—What would be better? What other system could there be? We are so accustomed to a system of banking, dependent for its cardinal function on a single bank, that we can hardly conceive of any other. But the natural system—that which would have sprung up if Government had let banking alone—is that of many banks of equal or not altogether unequal size. In all other trades competition brings the traders to a rough approximate equality. In cotton spinning, no single firm far and permanently outstrips the others. There is no tendency to a monarchy in the cotton world; nor, where banking has been left free, is there any tendency to a monarchy in banking either. In Manchester, in Liverpool, and all through England, we have a great number of banks, each with a business more or less good, but we have no single bank with any sort of predominance; nor is there any such bank in Scotland. In the new world of Joint Stock Banks outside the Bank of England, we see much the same phenomenon. One or more get for a time a better business than the others, but no single bank permanently obtains an unquestioned predominance. None of them gets so much before the others that the others voluntarily place their reserves in its keeping. A republic with many competitors of a size or sizes suitable to the business, is the constitution of every trade if left to itself, and of banking as much as any other. A monarchy in any trade is a sign of some anomalous advantage, and of some intervention from without.

As reflected in those writings, Bagehot judged that the banking system had not evolved the right way due to government intervention (I can’t paste the whole quote here as it would double the size of my post…), and that other systems would have been more efficient. This reminded me of Mervyn King’s famous quote: “Of all the many ways of organising banking, the worst is the one we have today.” Another very interesting passage will surely remind my readers of a few recent events (chapter 4):

And this system has plain and grave evils.

1st. Because being created by state aid, it is more likely than a natural system to require state help.

[…]

3rdly. Because, our one reserve is, by the necessity of its nature, given over to one board of directors, and we are therefore dependent on the wisdom of that one only, and cannot, as in most trades, strike an average of the wisdom and the folly, the discretion and the indiscretion, of many competitors.

Granted, the first point referred to the Bank of England. But we can easily apply it to our current banking system, whose growth since Bagehot’s time was partly based on political connections and state protection. Our financial system has been so distorted by regulations over time than it has arguably been built by the state. As a result, when crisis strikes, it requires state help, exactly as Bagehot predicted. The second point is also interesting given that central bankers are accused all around the world of continuously controlling and distorting financial markets through various (misguided or not) monetary policies.

For all the system ills, however, he argued against proposing a fundamental reform of the system:

I shall be at once asked—Do you propose a revolution? Do you propose to abandon the one-reserve system, and create anew a many-reserve system? My plain answer is that I do not propose it. I know it would be childish. Credit in business is like loyalty in Government. You must take what you can find of it, and work with it if possible.

Bagehot admitted that it was not reasonable to try to shake the system, that it was (unfortunately) there to stay. The only pragmatic thing to do was to try to make it more efficient given the circumstances.

But what did he think was a good system then? (chapter 4):

Under a good system of banking, a great collapse, except from rebellion or invasion, would probably not happen. A large number of banks, each feeling that their credit was at stake in keeping a good reserve, probably would keep one; if any one did not, it would be criticised constantly, and would soon lose its standing, and in the end disappear. And such banks would meet an incipient panic freely, and generously; they would advance out of their reserve boldly and largely, for each individual bank would fear suspicion, and know that at such periods it must ‘show strength,’ if at such times it wishes to be thought to have strength. Such a system reduces to a minimum the risk that is caused by the deposit. If the national money can safely be deposited in banks in any way, this is the way to make it safe.

What Bagehot described is a ‘free banking’ system. This is a laissez faire-type banking system that involves no more regulatory constraints than those applicable to other industries, no central bank centralising reserves or dictating monetary policy, no government control and competitive currency issuance. No regulation? No central bank to adequately control the currency and the money supply and act as a lender of last resort? No government control? Surely this is a recipe for disaster! Well…no. There have been a few free banking systems in history, in particular in Scotland and Sweden in the 19th century, to a slightly lesser extent in Canada in the 19th and early 20th, and in some other locations around the world as well. Curiously (or not), all those banking systems were very stable and much less prone to crises than the central banking ones we currently live in. Selgin and White are experts in the field if you want to learn more. If free banking was so effective, why did it disappear? There are very good reasons for that, which I’ll cover in a subsequent post on the history of central banking.

I am not claiming that Bagehot held those views for his entire life though. A younger Bagehot actually favoured monopolised-currency issuance and the one-reserve system he decried in his later life. I am not even claiming that everything he said was necessarily right. But Bagehot as a defender of free banking and against regulatory requirements of all sort is a far cry from what most academics and regulators would like us to believe today. Personally, I find that, well, very ironic.

BoE’s Mark Carney is burying Walter Bagehot a second time

Banks were partying on Thursday. Mark Carney, the new governor of the Bank of England, decided to ‘relax’ rules that had been put in place by its predecessor, Mervyn King. From now on, the BoE will lend to banks (as well as non-bank financial institutions) for longer maturities, accept less quality collateral in exchange, and lower the interest rate on/cost off those facilities. Mervin King was worried about ‘moral hazard’. Mark Carney has no idea what that means.

According to the FT, Barclays quickly figured out what this move implied: “it reduces the need for, and the cost of, holding large liquidity buffers.” Just wow. So, while we’ve just experienced a crisis during which some banks collapsed because they didn’t hold enough liquid assets on their balance sheet as they expected central banks and governments to step in if required, Carney’s move is expected to make the banks hold……even less liquidity.

It’s obviously nothing to say that this goes against every possible piece of regulation devised over the last few years. While the regulators were right in thinking that banks needed to hold more liquid assets, they took on the wrong problem: it was government and central bank support that brought about low liquidity holdings, and not free-markets recklessness. Anyway, Carney’s move kind of undermines that effort and risks rewarding mismanaged banks at the expense of safer ones.

Carney’s decision also goes against all the principles devised by the ‘father’ of central banking: Walter Bagehot. I guess it is time to decipher Bagehot, as he has been constantly misquoted since the start of the crisis by people who have apparently never read him. As a result he was used to justify what were actually anti-Bagehot policies. Bagehot’s principles are underlined in his famous book Lombard Street, written in 1873. What should a central bank do during a banking crisis? According to Bagehot (as described in chapters 2, 4 and 7), it should:

- Lend freely to solvent banks and companies

- Lend at a punitive rate of interest

- Only accept good quality collateral in exchange

For instance, in chapter 2:

The holders of the cash reserve must be ready not only to keep it for their own liabilities, but to advance it most freely for the liabilities of others. They must lend to merchants, to minor bankers, to ‘this man and that man,’ whenever the security is good.

In chapter 7:

First. That these loans should only be made at a very high rate of interest. This will operate as a heavy fine on unreasonable timidity, and will prevent the greatest number of applications by persons who do not require it. The rate should be raised early in the panic, so that the fine may be paid early; that no one may borrow out of idle precaution without paying well for it; that the Banking reserve may be protected as far as possible.

Secondly. That at this rate these advances should be made on all good banking securities, and as largely as the public ask for them. The reason is plain. The object is to stay alarm, and nothing therefore should be done to cause alarm. But the way to cause alarm is to refuse some one who has good security to offer… No advances indeed need be made by which the Bank will ultimately lose.

No central bank applied Bagehot’s recommendations during the financial crisis. Granted, given the organisation of today’s financial system, it is difficult for central bank to lend to non-financial firms. Nonetheless, it took them a little while to start lending freely and lent to insolvent banks as well. They also started to accept worse quality collateral than what they used to (think about the Fed now purchasing mortgage/asset-backed securities for example). Finally, central banks have never charged a punitive rate on their various facilities. Quite the contrary: interest rates were pushed down as much as humanly possible on all normal and exceptional refinancing facilities.

While the ECB and the Fed have made clear that some of those were temporary measures, Carney now seems to imply that, not only are they here to stay, but they also will be extended in non-crisis times. He calls that being “open for business”. Poor Bagehot must be turning in his grave right now.

According to Carney, those measures will reinforce financial stability. Really? So no moral hazard involved? no bank taking unnecessary risks because it knows that the BoE has its back? If Mervyn King didn’t do everything perfectly while in charge, at least he had a point. Carney, after overseeing a large credit bubble in Canada over the past few years (he first joined the Bank of Canada in 2003, then rejoined it as Governor in 2008), is now applying his brilliant recipe to the UK.

I think that Carney’s decisions introduce considerable incentive distortions in the banking system. This is clearly not what a free-market should look like. In any case, if a new crisis strikes as a result, I am pretty sure that laissez-faire will be blamed again. It is ironic to see that some of those central bankers destroy faith in free-markets while trying to protect them.

Bagehot also said other things that go against the principles driving our current banking and regulatory system. More details in another post!

Photograph: Reuters/Bloomberg

Chart: The Big Picture

Recent Comments