News digest (Krugman and deregulation, central banking for Bitcoin…)

A looooooooot of news since the beginning of the week. So I’ll just quickly go over a few of them. Guys please, next time, spread your news more evenly over time. There was nothing to comment on recently!

Not new news but the Swedish bank regulators are thinking of increasing RWAs on mortgages to fight a growing housing bubble. Well, raising them to 25% (from 15% floor…) would still not change much: they would remain below most other asset classes’ level and securitisation (RMBS) would allow banks to bypass the restrictions.

Meanwhile, Yves Mersch, member of the Executive Board of the ECB, spoke about how to revive SME lending in bank-reliant Europe. His solutions involve: strengthening banks, securitisation and… banking union. Any word of capital requirements/risk-weighted assets? Not a single one. When I told you that central bankers don’t seem to get it…

But the UK government wants to ditch the household lending side of the Funding for Lending Scheme! They now only want to provide cheap funding to banks if they prove that they lend to SMEs. Why not, but I doubt it would really work for a few reasons: 1. demand for loans remains quite low, 2. market funding remains cheap (it was cheaper than FLS), 3. banks haven’t drawn much on it anyway, 4. RWAs are still in place! Mortgage and household lending will still attract most of lending volume as it is more profitable from a capital point of view.

Meanwhile (again), SME financing from alternative lenders not subject to RWAs and other stupid capital rules, keeps growing in the UK. However, it is still tough for those lenders to assess the health of the companies that would like to lend to.

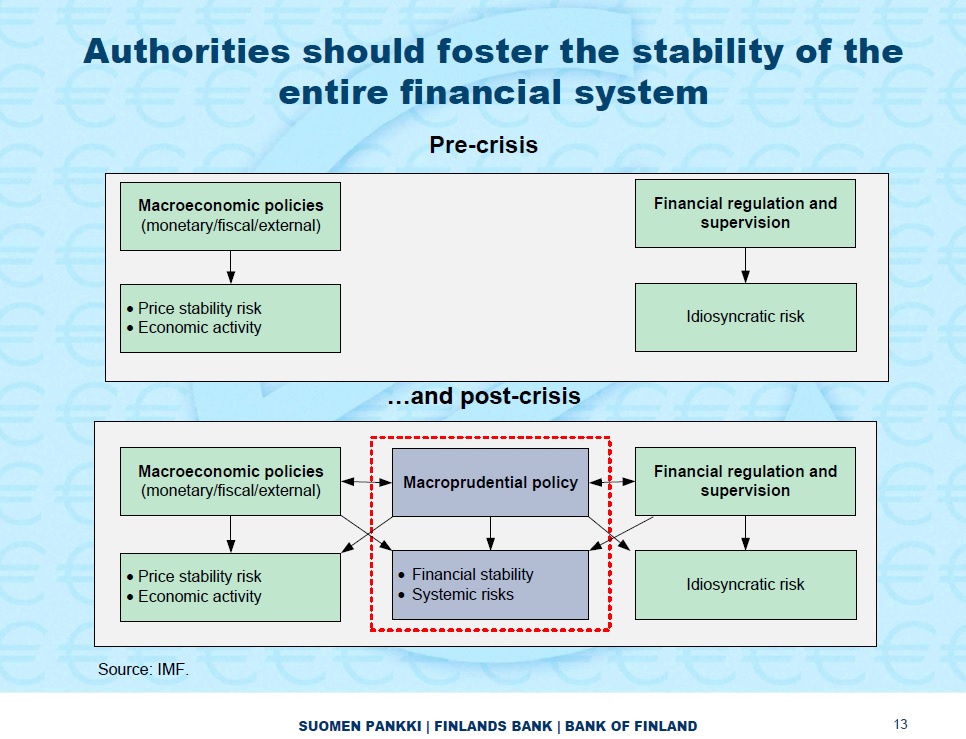

Erkki Liikanen, the Governor of the central bank of Finland, told us about his ideas to improve financial stability. Surprise: they haven’t changed. So macroprudential policy starts interfering with macroeconomic policies and financial regulation, with possibly opposite effects that don’t seem to bother him much. Look at that slide, which is the very definition of a messy policy goal, with multiple targets and interferences:

A very strange piece in the Washington Post: Bitcoin needs a central banker. Wait a second. No, it’s definitely not the 1st of April. First, the author asserts that Bitcoin’s wild changes in value make it difficult to be adopted as a currency. This is extraordinary. Does the author even understand FX rates? If the author wishes to purchase his coffee using Euros, despite the coffee being priced in Dollars, will he also declare that the fact the Euro’s value is unstable (making the effective Euro price of its coffee volatile) makes the currency improper for use? When prices are originally denominated in Bitcoin, the change in the value of the digital currency won’t affect them. When prices are actually denominated in USD, but converted into Bitcoin, then yes, changes in the value of the digital currency will affect them. But this is hardly Bitcoin’s fault… Then he gets mixed up with ‘menu costs’, ‘hyperinflation’, ‘money demand’, etc. Wow. Just one last thing: has he even understood that Bitcoin was designed to be free from central bankers and government intervention in the first place?

Izabella Kaminska in the FT wrote a new piece on Bitcoin and other alternative electronic currencies. She complains about the multiplication of such currencies that nothing backs and pretty much only see speculative motivations underlying them. I am not going to comment on the whole thing, but whether right or wrong, she should ask herself why there is such frenzy about those currencies at the moment. My guess is that, governments’ and central banks’ manipulation of their own currencies have unleashed a beast: people afraid to hold classic currencies started to look for alternatives, pushing up their prices, in turn attracting speculators. The process is similar to ‘bad’ financial innovations (the ones designed specifically to bypass restricting regulation): they often start as a benign innovation for the ‘common good’, but the surprising demand for them and large profits attract speculators until the market crashes. Not the fault of the innovation, but the fault of the regulation that triggered them…

Paul Krugman thinks that “the trouble with economics is economists”, and that mainstream economics is not to blame for the financial crisis. I partly disagree: 1. there are various schools of thought within mainstream economics that often disagree with each other altogether and 2. most (all?) of them cannot fully explain the crisis anyway. But, and this is where Krugman shows his limited knowledge of banking and therefore the limit of his reasoning, he declares that “the mania for financial deregulation, for example, didn’t come out of standard economic analysis.” I’m sorry? Which mania for financial deregulation? The international banking sector had never been as regulated in history as on the eve of the crisis! (even taking into account of the few one-off deregulations) I need to come back to this in a subsequent post. Really, Paul, you have to revise your history. And your reasoning.

On Free Banking, George Selgin urges Scots to ‘poundize’ unilaterally if ever they declare independence from the UK. And “if the British Parliament refuses to cooperate, so much the better. Who knows: Scotland could even end up with a banking system as good as the one it had before 1845, when Parliament, which knew almost as little about currency then as it does now, began to bugger it up.” If only Scotland could enlighten the world a second time and get back to a free banking system!

Recent Comments

| pslebow on ‘Sovereign money’:… | |

| pslebow on A critique of Werner’s view on… | |

| Hugo Kramer on Welcome to Spontaneous Fi… | |

| Nathan on A critique of Werner’s view on… | |

| Nathan on More, more, more money endogen… |

Trackbacks / Pingbacks