I’d rather not have a fox as bank regulator

We can sometimes read stupefying things on the internet. I almost fell off my chair yesterday when I read MC Klein’s latest banking piece on FT Alphaville. He suggests that the right way to regulate banks might well be to be “crazy like a fox”…

Throughout his ‘surprising’ post, he writes things like:

While simple rules about capital and short-term debt still have tremendous appeal, there is value in having a regulatory regime that is onerous precisely because of its complexity and its unpredictability.

And

As Matt Yglesias notes, the value of having lots of pointless but annoying rules is that they distract the bank lobbyists from the really important stuff. The swap pushout was the first in what is hopefully a long line of defence. We’re tempted to say that crafty policymakers should immediately propose several new and even more annoying rules for the banks.

Fortunately, regulators have other means of harassing their adversaries, hopefully keeping them busy enough to avoid exploiting the system too much.

Andrew Haldane must be having a heart attack right now.

This goes against some of the most basic economic principles, and against the very thing that allows any business to exist and thrive in the first place: the rule of law.

Let’s start with Matt Yglesias’ post. Perhaps not surprising for someone who once wrote that Dodd-Frank was an ‘achievement’ that created a ‘safer banking system’, Yglesias again proves that he has a very low understanding of how banking works. CDS contacts have apparently become ‘custom swaps’ that are used to “bet on the potential bankruptcy of a given country or company or the failure of a new financial product.” Hedging anyone? Insurance that can protect even the most vanilla-like institutions against some specific default risks? No, this is just an evil Wall Street speculative tool. Nevermind that some CDS are traded on behalf of clients, and banks’ positions taken to offset customers’ needs. Nevermind that siloing banking activities/liquidity/capital across different entities of a same banking group actually decrease the safety of the system (see also here).

Despite this rather limited knowledge of the industry, Klein builds on Yglesias’ reasoning: any repealed rule should be replaced by many pointless ones to distract lobbyists.

Now, I am still trying to understand the logic behind constantly adding red tape for no reason rather than judging rules and bureaucracy on their actual value-added and efficiency. Here again, nevermind that countries with the least efficient and most numerous rules are the least business-friendly, and that too much red tape and regulatory uncertainty is around the top issue for most US businesses at the moment. No, banking is (apparently) different.

Let me suggest that a few years working for a bank would probably help dispel some of those myths. That, lobbyists aren’t that dumb, and that, if they attack some specific rules, it is surely that these would be harmful for the banks (and indeed, both Yglesias and Klein are plain wrong in considering this CDS rule ‘pointless’). That the 30,000-page rulebook that Dodd-Frank created might not fully facilitate banking processes and lending. That, by constantly changing the rules as Klein suggests, banks might well be tempted to move away from any risky activity that might end up being considered unlawful at some point in the future, hurting risky lending in the process (i.e. usually SME lending, as if it were not already low enough) with all the associated potential economic consequences.

Banks have been closing entire lines of business, de-globalising, preventing international payments to go through, harming international trade and economic activity. The multiplication of rules could, not only lead to resource misallocation, but also to increased management time. Management time that would be better spent on analysing and controlling the business than on bureaucratic, ‘pointless’, but dangerous (because of potential fines) rules. Unexpected consequences if you like. Still, it looks acceptable for Klein.

This is exactly why avoiding regulatory uncertainty and discretionary policies, and applying a predictable set of rules (i.e. rule of law), is so crucial in facilitating business and economic development.

As Kevin Dowd clearly illustrates in a very good recent paper:

One has to understand that the banks have no defense against this regulatory onslaught. There are so many tens or hundreds of thousands or maybe millions of rules that no one can even read them all, let alone comply with them all: even with armies of corporate lawyers to assist you, there are just too many, and they contradict each other, often at the most fundamental level. For example, the main intent of the Privacy Act was to promote privacy, but the main impact of the USA PATRIOT Act was to eviscerate it. This state of lawlessness gives ample scope for regulators to pursue their own or the government’s agendas while allowing defendants no effective legal recourse. One also has to bear in mind the extraordinary criminal penalties to which senior bank officers are exposed. Government officials can then pick and choose which rules to apply and can always find technical infringements if they look for them; they can then legally blackmail bankers without ever being held to account themselves. The result is the suspension of the rule of law and a state of affairs reminiscent of the reign of Charles I, Star Chamber and all. Any doubt about this matter must surely have been settled with the Dodd-Frank Act, which doled out extralegal powers like confetti and allows the government to do anything it wishes with the banking system.

A perfect example of this governmental lawlessness was the “Uncle Scam” settlement in October 2013 of a case against JP Morgan Chase, in which the bank agreed to pay a $13billion fine relating to some real estate investments. This was the biggest ever payout asked of a single company by the government, and it didn’t even protect the bank against the possibility of additional criminal prosecutions. What is astonishing is that some 80 percent of the banks’ RMBS had been acquired at the request of the federal government when it bought Bear Stearns and WaMu in 2008, and now the bank was being punished for having them. Leaving aside its inherent unpleasantness, this act of government plunder sets a very bad precedent: going forward, no sane bank will now buy a failing competitor without forcing it through Chapter 11. It’s one thing to face an acquired institution’s own problems, but it is quite another to face looting from the government for cooperating with the government itself.

The argument’s logic is also very weak. If rules are believed to let excessive risks “fall through the cracks”, then they should never be adopted in the first place. Why even adopting rules which we already know create systemic risks? If regulators really believe those rules will cover most (or all) risks, there is no point in planning to replace them with other rules, just for the sake of changing the rules, as the new ones are likely to be less effective. Otherwise those new, more effective, rules are the ones that should have been implemented in the first place. The whole logic of the argument just doesn’t hold*.

What about the practicality of ever changing the regulatory framework? Here again the argument fails. There aren’t hundreds of derivative settlement options and assets acceptable as collateral or as liquidity buffer. While the theory sounds nice in FT Alphaville’s columns, it is simply not possible to implement in practice.

The financial imbalances that led to our previous crisis, for a large part, originated in the most complex banking rule set devised in history, compounded by politically-incentivised housing agendas (along with misguided monetary policy and accounting rules). Klein’s (and Yglesias’) failure is to ignore this and assume that more, and tighter, rules are more effective. Moreover, regulators’ failure to foresee crises has probably been a constant throughout history. Yet, Klein backs an ever-more complex and constantly-changing regulatory framework at the discretion of those same regulators.

Calomiris and Nissim, two academics that know and understand a thing or two about banking, declared that:

We worry that regulatory uncertainty – and especially the persistent waves of political attacks on global universal banks – is taking a toll.

It is important to recognize that bank stockholders are not alone in suffering from the low stock prices that result from these attacks. The supply of bank loans, and banks’ ability to provide other crucial financial services in support of economic growth, reflect the risk-bearing capacity of banks, which is directly related to market valuations of bank franchises. If banks’ earnings get little respect from the market, banks’ abilities to help the economy grow will be commensurately hobbled.

Even The Economist, which has been a supporter of banking regulatory reform over the past few years, is against regulatory discretion and is well-aware of regulators’ weaknesses (emphasis mine):

Attracting the capital that will make banking safer will be hard, with profit forecasts so anaemic. However it will also be made unnecessarily difficult by capricious behaviour from the very watchdogs who are ordering banks to raise the funds.

One problem is the endless tinkering with the rules. For all Mr Carney’s talk of finishing the job, global regulators have yet to set the minimum level for several of their new capital requirements. National regulators are just as bad. No bank can be certain how much capital it will need in a few years’ time. Pension funds and insurance companies rightly fret that even a tiny tweak in any of the new regulatory tests is enough to send a bank’s share price plummeting (or, less often, rocketing). […]

Banks can hardly be surprised that regulators have rewritten the rule-book and then thrown it at them. But, for the health of the system, the rules need to be predictable, transparent and consistent. Incredibly, the regulations emanating from America’s Dodd-Frank financial reforms are still being written, more than four years after the law was passed. Europe is scarcely better. Impose demanding capital rules, but stop adding more red tape: that should be the mantra of bank regulators just about everywhere.

The worst is: Klein does identify some of the problems with our current regulatory regime, which is easily gameable because of its complexity. In terms of regulation and forecasting, simple rules and models have always performed better (see some of the links above). But instead of stepping back and getting back to simpler, less distortive, rules, his policy of choice seems to be more bank-bashing, never-ending regulatory regime uncertainty, more complexity, the possible paralysis of bank lending and the build-up of risk within the more opaque shadow banking system. I guess it’s going to be a real success.

* He could reply that the very purpose of ‘pointless’ rules is that they have no real impact on anything. Let me clarify something: all rules have an impact, whether it is small, big, negative, positive, or both (and again, the CDS rule was far from pointless). He could also reply that changing the rules limit the gameability of the system. But this makes little sense, as ‘pointless’ rules changes would probably not prevent the accumulation of risk anyway and, even for ‘non-pointless’ rules, there are only a few available options as described above (changing capital requirements by 1% up or down, including or excluding A+ rated bonds as LCR-compliant, increasing/decreasing haircut requirements by 5%, and so forth, really would have very little impact on gameability or stability).

I am also a free banking theorist

George Selgin wrote a very true post on Freebanking.org. He claims that we are all, in a way or another, free banking theorists. Why? As Selgin very well explains:

Consider: an economist says that central banks prevent or limit the severity of financial crises, or that without mandatory deposit insurance even sound banks are likely to face runs, or that banks can never be expected to hold enough capital unless we force them to, or that commercially-supplied banknotes will tend to be discounted. All such claims–which is to say any claims about the need for or consequences of government intervention in banking–depend, if not on an explicit understanding of the nature and workings of a laissez-faire banking system, then on some implicit understanding. And this understanding in turn implies a theory of some sort, for reference to experience alone won’t suffice for drawing the sort of sweeping conclusions I’m talking about. It follows that all economists who have anything to say about the effects of government intervention in the banking system are either self-proclaimed free banking theorists or are free banking theorists who don’t admit (and perhaps don’t realize) it.

Indeed, most banking academic research studies and banking reform proposals base their ideas and models on certain assumptions of how the banking system, left to its own device, would behave, and how to correct the market failures that could possibly arise from such systems.

As my (and most people’s) experience can also testify, this tacit conventional wisdom is present in the mind of the general public and finance practitioners (I can still remember my father’s face when I told him we should get rid of central banks. Like he had just spotted some sort of ghost). The success of the usual US-centric misrepresentation of banking history is almost complete.

With this blog, I have been trying to explain what would (not) have happened if we had left banking free of all the rules that distort its natural behaviour. Seen this way, I am also a free banking theorist. I am trying to get back to the roots, asking questions such as: let’s supposed we never implemented Basel rules, would have real estate lending grown that much over the past three decades? What about securitization? Or interest rates on sovereign debt? And banks’ capital and liquidity buffers? What if we hadn’t had central banks nor deposit insurance over the period? What compounded what?

A lot of this is counterfactual, hence uncertain. Still, the intellectual challenge this represents is worth it, as current banking reformers and regulators still rely on and take for granted the inaccurate conventional story to justify the exponential growth of increasingly tight rules. Rules which, as I explain on this blog, are more likely to harm the banking system than to make it safer.

Larry White once says that free banks should be ‘anti-fragile’, and that the only reason they remain fragile is because of government-institutionalised rules that prevent them from self-correcting and learning. I have also already said that this does not mean that banks would never fail or that no crisis would ever occur. But it is likely that the accumulation of financial imbalances, which under our current system slowly emerge hidden behind the regulatory curtain until it is too late, would appear much sooner, limiting the destructive potential of any crisis. The market process, in order to become anti-fragile, needs to learn through experience. The more ‘safety’ rules one implement the less likely market actors will learn and the more likely the following crisis is going to be catastrophic. Institutionalised paternalism is self-defeating.

Unfortunately, the conventional story has seriously twisted everyone’s mind, and it is highly likely that any government announcing the end of the Fed/ECB/BoE/deposit insurance/currency monopoly would trigger market crashes and a lack of confidence in banks. Most commentators would describe the move as “crazy given what we’ve learnt from history”. In short, it would be a ‘history misreading-induced’ panic. While this would be short-lived, this would also be damaging. It is our role to tell the public that, in fact, it should not fear such changes. It should welcome them.

Chinese regulation, the European way

Some European banking regulators are currently considering the implementation of a sovereign bond exposure cap of 25% of capital to any one sovereign. Their goal is to break the link between sovereigns and banks. I think they don’t really know what they are doing.

European sovereign bond markets are distorted in all possible ways:

- The Basel banking regulation framework has been awarding 0% risk-weight to OECD sovereign debt since the 1980s, meaning purchasing such asset does not require any capital. Recent rules haven’t changed anything to this.

- On the contrary, Basel 3 introduces a liquidity ratio (LCR) basically requiring banks to hold even more sovereign debt on their balance sheet (as part of so-called highly-liquid ‘Level 1 assets’).

- Meanwhile, the ECB, as well as the BoE, have been trying to revive business lending (which suffers from the opposite problem: high risk-weights) by launching cheap funding programmes (LTRO, TLTRO, FLS…). Banks drawn on those facilities to invest in… more 0% weighted sovereign debt, and earn capital-free interest income. We call this the ‘carry trade’.

- Furthermore, investors (including banks) have started seeing peripheral European debt as virtually risk-free thanks to the ECB pledge that it would do whatever it takes to prevent defaults in those countries.

There you are: had European regulators wanted to reinforce the link between sovereigns and banks, they wouldn’t have been more successful. Their usual talk of breaking the link between banks and sovereigns has been completely undermined by their own actions.

The easy solution would have been to scrap risk-weights (or at least increase them on sovereign bonds). But this was too simple, so European policymakers decided to go the Chinese way: never scrap a bad rule; design a new one to fix it; and another one to fix the previous one that fixed the original one.

The new 25% cap would only add further distortion: while Basel’s risk-weights do not differentiate between Portuguese and German bonds, the 25% rule doesn’t either. But, you would retort, this isn’t the point: the point is to limit the exposure to any single sovereign. I agree that diversification is usually a good thing. But 1. lack of diversification has been encouraged by policymakers’ own decisions, and 2. forcing banks to diversify away from the safest sovereigns just for the sake of diversifying may well put many banks’ balance sheet more at risk.

Finally, Fitch estimates at EUR1.1Trn the amount of debt that would need to be offloaded. This is very likely to affect markets and could result in banks taking serious one-off hits on their available-for-sale and marked-to-market bond portfolios, resulting in weaker capital positions. This could also raise overall interest rates, in particular in riskier (and weaker) European countries. Fitch believes banks could rebalance into Level 1-elligible covered bonds. Maybe, but this would only introduce even more distortions in the market by artificially raising the demand for their underlying assets, and this would encumber banks’ balance sheets even further, creating other sorts of risks.

Why pick a simple solution when you can do it the Chinese way?

Photo: picture-alliance / dpa through www.dw.de

New research confirms the role of regulation and housing in modern business cycles

I think readers will find it hard to imagine how excited I was yesterday when I discovered (through an Amir Sufi piece in the FT) a brand new piece of research called: The Great Mortgaging: Housing Finance, Crises, and Business Cycles

(The authors, Jordà, Schularick and Taylor (JST), also published a free version here, and a summary on VOX)

I wish the authors had read my blog before writing their paper as it confirms many of my theses (unless they had?). It’s so interesting that I could almost quote two thirds of the paper here. I obviously encourage you to read it all and I will selectively copy and paste a few pieces below.

In my recent piece on updating the Austrian business cycle theory (ABCT), I pointed out that the nature of lending (and banks’ balance sheets) had changed over time since the 19th century (and particularly post-WW2), mainly due to banking regulation and government schemes. I had already provided a revealing post-WW2 chart for the US to demonstrate the effects of Basel 1 on business and real estate lending volumes.

JST went further. They went further back in time and gathered a dataset of disaggregated lending figures covering 17 developed countries over close to 140 years. Their conclusions confirm my views. Regulations – and in particular Basel – changed everything.

Here is their aggregate credit to GDP chart across all covered countries, to which I added the introduction of Basel 1 as well as pre-Basel trends:

I don’t think there is anything clearer than this chart (I’m not sure that securitized mortgages are included, in which case those figures are understated). Since the 1870s, non-mortgage lending had been the main vector of credit and money supply growth, and mortgage lending represented a relatively modest share of banks’ balance sheet. Basel turned this logic upside-down. How? I have already described the process countless times (risk-weights and capital regulation), so let see what JST say about it:

Over a period of 140 years the level of non-mortgage lending to GDP has risen by a factor of about 3, while mortgage lending to GDP has risen by a factor of 8, with a big surge in the last 40 years. Virtually the entire increase in the bank lending to GDP ratios in our sample of 17 advanced economies has been driven by the rapid rise in mortgage lending relative to output since the 1970s. […]

In addition to country-specific housing policies, international banking regulation also contributed to the growing attractiveness of mortgage lending from the perspective of the banks. The Basel Committee on Bank Supervision (BCBS) was founded in 1974 in reaction to the collapse of Herstatt Bank in Germany. The Committee served as a forum to discuss international harmonization of international banking regulation. Its work led to the 1988 Basle Accord (Basel I) that introduced minimum capital requirements and, importantly, different risk weights for assets on banks’ balance sheets. Loans secured by mortgages on residential properties only carried half the risk weight of loans to companies. This provided another incentive for banks to expand their mortgage business which could be run with higher leverage. As Figure 1 shows, a significant share of the global growth of mortgage lending occurred in recent years following the first Basel Accord.

I wish they had expanded on this topic and made the logical next step: Basel helped set up the largest financial crisis in our lifetime through regulatory arbitrage. Nevertheless, the implications are crystal clear.

To JST, this growth in real estate lending is the reason underlying our most recent financial crises:

We document the rising share of real estate lending (i.e., bank loans secured against real estate) in total bank credit and the declining share of unsecured credit to businesses and households. We also document long-run sectoral trends in lending to companies and households (albeit for a somewhat shorter time span), which suggest that the growth of finance has been closely linked to an explosion of mortgage lending to households in the last quarter of the 20th century. […]

Since WWII, it is only the aftermaths of mortgage booms that are marked by deeper recessions and slower recoveries. This is true both in normal cycles and those associated with financial crises. […]

The type of credit does seem to matter, and we find evidence that the changing nature of financial intermediation has shifted the locus of crisis risks increasingly toward real estate lending cycles. Whereas in the pre-WWII period mortgage lending is not statistically significant, either individually or when used jointly with unsecured credit, it becomes highly significant as a crisis predictor in the post-WWII period.

JST confirm what I was describing in my post on updating the ABCT: that is, that banks don’t play the same role as in early 20th century, when the theory was first outlined:

The intermediation of household savings for productive investment in the business sector—the standard textbook role of the financial sector—constitutes only a minor share of the business of banking today, even though it was a central part of that business in the 19th and early 20th centuries.

JST describe the post-WW2 changes in mortgage lending originally as a result of government schemes to favour home building and ownership, followed by international regulatory arrangements (Basel) from the 1980s onward. Those measures and rules led to a massive restructuring of banks’ balance sheet, as demonstrated by this chart:

While the empirical findings of this paper will be of no surprise to readers of this blog, this research paper deserves praise: its data gathering and empirical analysis are simply brilliant, and it at last offers us the opportunity to make other mainstream academics and regulators aware of the damages their ideas and policies have made to our economy over the past decades. It also puts the idea of ‘secular stagnation’ into perspective: our societies are condemned to stagnate if regulatory arbitrage starve our productive businesses of funds and the only way to generate wealth is through housing bubbles.

While the empirical findings of this paper will be of no surprise to readers of this blog, this research paper deserves praise: its data gathering and empirical analysis are simply brilliant, and it at last offers us the opportunity to make other mainstream academics and regulators aware of the damages their ideas and policies have made to our economy over the past decades. It also puts the idea of ‘secular stagnation’ into perspective: our societies are condemned to stagnate if regulatory arbitrage starve our productive businesses of funds and the only way to generate wealth is through housing bubbles.

Breaking banks won’t help economic recovery

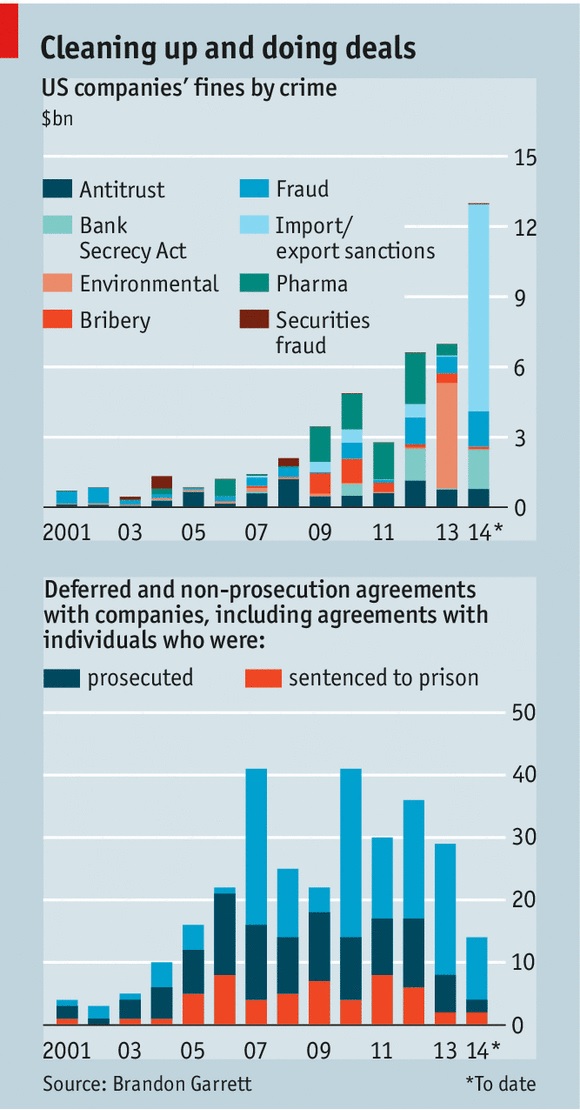

In contrast with the bank-bashing environment of the post-crisis period, voices are increasingly being raised to moderate regulatory, political and judiciary risks on the banking system.

Last week, Gillian Tett wrote an article in the FT tittled “Regulatory revenge risks scaring investors away”. She says:

Last month [Roger McCornick’s] project team published its second report on post-crisis penalties, which showed that by late 2013 the top 10 banks had paid an astonishing £100bn in fines since 2008, for misbehaviour such as money laundering, rate-rigging, sanctions-busting and mis-selling subprime mortgages and bonds during the credit bubble. Bank of America headed this league of shame: it had paid £39bn by the end of 2013 for its transgressions. When the 2014 data are compiled, the total penalties will probably have risen towards £200bn.

She argues that “legal risk is now replacing credit risk.” This is a key issue. Banks have already been hit hard by new regulatory requirements, which sometimes require a fundamental restructuring of their business model. The consequences of this framework shift is that profitability, and hence internal capital generation, remain subdued, weakening the system as a whole. Banks now reporting double digit RoEs are more the exceptions than the rule. Moreover, low profitability also reduces the banks’ ability to generate capital externally (i.e. capital raising) because they do not cover their cost of capital. This scares investors away, as they have access to better risk-adjusted investment opportunities elsewhere.

The enormous amounts raised through litigation procedures make such a situation even worse. Admittedly, banks that purposely bypassed laws or committed frauds should be punished. But, as The Economist argues this week in a series of articles called “The criminalisation of American business” (see follow-up article here), the “legal system has become an extortion racket”, whose “most destructive part of it all is the secrecy and opacity” as “the public never finds out the full facts of the case” and “since the cases never go to court, precedent is not established, so it is unclear what exactly is illegal”:

This undermines the predictability and clarity that serve as the foundations for the rule of law, and risks the prospect of a selective—and potentially corrupt—system of justice in which everybody is guilty of something and punishment is determined by political deals. America can hardly tut-tut at the way China’s justice system applies the law to companies in such an arbitrary manner when at times it seems almost as bad itself.

Estimates of capital shortfall at European banks vary between EUR84bn and as much as EUR300bn (another firm, PwC, estimates the shortfall at EUR280bn). Compare those amounts with the hundreds of billions Euros paid or about to be paid by banks as litigation settlements, and it is no surprise that banks have to deleverage to comply with regulatory capital ratio deadlines and upcoming stress tests… Such high amounts, if justified, could probably have been raised by prosecutors at a slower pace in the post-crisis period without endangering the economic recovery (banks’ balance sheets would have been more solid more quickly, which would have facilitated the lending channel of the monetary transmission mechanism).

In the end, regulatory regime uncertainty strikes banks twice: financial regulations keep changing (and new ones are designed), and opaque litigation risk is at an all-time high. Banks are now very risk-averse, depressing lending and international transactions. This seems to me to replicate some of the mistakes made by Roosevelt during the Great Depression. Despite all the central banks’ money injection programmes, this may not be the best way out of an economic crisis…

PS: Commenting on the forthcoming P2P lender Lending Club IPO, Matt Levine argues that:

But Lending Club can grow its balance sheet all it wants. Lending Club is not a bank. So it’s not subject to banking regulation, which means that it can do a core function of banking much more efficiently than an actual bank can.

He is (at least) partly right. By killing banks, regulatory constraints are likely to trigger the emergence of new types of lenders.

Wait… Isn’t it what’s already happened (MMF and other shadow banking entities…)?

Hummel vs. Haldane: the central bank as central planner

Recent speeches and articles from most central bankers are increasingly leaving a bad aftertaste. Take this latest article by Andrew Haldane, Executive Director at the BoE, published in Central Banking. Haldane describes (not entirely accurately…) the history and evolution of central banking since the 19th century and discusses two possible paths for the next 25 years.

His first scenario is that central banks and regulation will step backward and get back to their former, ‘business as usual’, stance, focusing on targeting inflation and leaving most of the capital allocation work to financial markets. He views this scenario as unlikely. He believes that the central banks will more tightly regulate and intervene in all types of asset markets (my emphasis):

In this world, it would be very difficult for monetary, regulatory and operational policy to beat an orderly retreat. It is likely that regulatory policy would need to be in a constant state of alert for risks emerging in the financial shadows, which could trip up regulators and the financial system. In other words, regulatory fine-tuning could become the rule, not the exception.

In this world, macro-prudential policy to lean against the financial cycle could become more, not less, important over time. With more risk residing on non-bank balance sheets that are marked-to-market, it is possible that cycles in financial assets would be amplified, not dampened, relative to the old world. Their transmission to the wider economy may also be more potent and frequent. The demands on macro-prudential policy, to stabilise these financial fluctuations and hence the macro-economy, could thereby grow.

In this world, central banks’ operational policies would be likely to remain expansive. Non-bank counterparties would grow in importance, not shrink. So too, potentially, would more exotic forms of collateral taken in central banks’ operations. Market-making, in a wider class of financial instruments, could become a more standard part of the central bank toolkit, to mitigate the effects of temporary market illiquidity droughts in the non-bank sector.

In this world, central banks’ words and actions would be unlikely to diminish in importance. Their role in shaping the fortunes of financial markets and financial firms more likely would rise. Central banks’ every word would remain forensically scrutinised. And there would be an accompanying demand for ever-greater amounts of central bank transparency. Central banks would rarely be far from the front pages.

He acknowledged that central banks’ actions have already considerably influenced (distorted?…) financial markets over the past few years, though he views it as a relatively good thing (my emphasis):

With monetary, regulatory and operational policies all working in overdrive, central banks have had plenty of explaining to do. During the crisis, their actions have shaped the behaviour of pretty much every financial market and institution on the planet. So central banks’ words resonate as never previously. Rarely a day passes without a forensic media and market dissection of some central bank comment. […]

Where does this leave central banks today? We are not in Kansas any more. On monetary policy, we have gone from setting short safe rates to shaping rates of return on longer-term and wider classes of assets. On regulation, central banks have gone from spectator to player, with some granted micro-prudential as well as macro-prudential regulatory responsibilities. On operational matters, central banks have gone from market-watcher to market-shaper and market-maker across a broad class of assets and counterparties. On transparency, we have gone from blushing introvert to blooming extrovert. In short, central banks are essentially unrecognisable from a quarter of a century ago.

This makes me feel slightly unconfortable and instantly remind me of the – now classic – 2010 article by Jeff Hummel: Ben Bernanke vs. Milton Friedman: The Federal Reserve’s Emergence as the U.S. Economy’s Central Planner. While I believe there are a few inaccuracies and omissions in Hummel’s description of the financial crisis, his article is really good and his conclusion even more valid today than at the time of his writing:

In the final analysis, central banking has become the new central planning. Under the old central planning—which performed so poorly in the Soviet Union, Communist China, and other command economies—the government attempted to manage production and the supply of goods and services. Under the new central planning, the Fed attempts to manage the financial system as well as the supply and allocation of credit. Contrast present-day attitudes with the Keynesian dark ages of the 1950s and 1960s, when almost no one paid much attention to the Fed, whose activities were fairly limited by today’s standard. […]

As the prolonged and incomplete recovery from the recent recession suggests, however, the Fed’s new central planning, like the old central planning, will ultimately prove an unfortunate and possibly disastrous failure.

The contrast between central bankers’ (including Haldane’s) beliefs of a tightly controlled financial sector to those of Hummel couldn’t be starker.

Where it indeed becomes really worrying is that Hummel was only referring to Bernanke’s decision to allocate credit and liquidity facilities to some particular institutions, as well as to the multiplicity of interest rates and tools implemented within the usual central banking framework. At the time of his writing, macro-prudential policies were not as discussed as they are now. Nevertheless, they considerably amplify the central banks’ central planner role: thanks to them, central bankers can decide to reduce or increase the allocation of loanable funds to one particular sector of the economy to correct what they view as financial imbalances.

Moreover, central banks are also increasingly taking over the role of banking regulator. In the UK, for instance, the two new regulatory agencies (FCA and PRA) are now departments of the Bank of England. Consequently, central banks are in charge of monetary policy (through an increasing number of tools), macro-prudential regulation, micro-prudential regulation, and financial conduct and competition. Absolutely all aspects of banking will be defined and shaped at the central bank level. Central banks can decide to ‘increase’ competition in the banking sector as well as favour or bail-out targeted firms. And it doesn’t stop here. Tighter regulatory oversight is also now being considered for insurance firms, investment managers, various shadow banking entities and… crowdfunding and peer-to-peer lending.

Hummel was right: there are strong similarities between today’s financial sector planning and post-WW2 economic planning. It remains to be seen how everything will unravel. Given that history seems to point to exogenous origins of financial imbalances (whereas central bankers, on the other hand, believe in endogenous explanations, motivating their policies), this might not end well… Perhaps this is the only solution though: once the whole financial system is under the tight grip of some supposedly-effective central planner, the blame for the next financial crisis cannot fall on laissez-faire…

Raising capital requirements? Not that useful

The recent news of the near-bankruptcy of UK-based Cooperative Bank and Portugal-based Banco Espirito Santo made me question the utility of regulatory capital requirements. What are they for? Is raising them actually that useful? It looks to me that the current conventional view of minimum capital requirements is flawed.

In the pre-crisis era, banks were required to comply with a minimum Tier 1 capital ratio of 4% (i.e. Tier 1 capital/risk-weighted assets >= 4%). Most banks boasted ratios of 2 to 5 percentage points above that level. Basel 3 decided to increase the Tier 1 minimum to 6%, and banks are currently harshly judged if they do not maintain at least a 4% buffer above that level.

Indeed, given the possible sanctions arising from breaching those capital requirements, bankers usually thrive to maintain a healthy enough buffer above the required minimum. Sanctions for breaching those requirements include in most countries: revoking the banking licence, forcing the bank into a state of bankruptcy and/or forcing a restructuring/break-up/deleveraging of the balance sheet. Hence the question: what is the actual effective capital ratio of the banking system?

Companies – as well as banks in the past – are usually deemed insolvent (or bankrupt) once their equity reaches negative territory. At that point, selling all the assets of the company/bank would not generate enough money to pay off all creditors (while shareholders are wiped out).

Let’s assume a world with no Tier 1 capital but only straightforward equity, and without regulatory capital requirements. Following the basic rule outlined above, a bank with a 10% capital ratio can experience a 10% reduction in the value of its assets before it reaches insolvency. Let’s now introduce a minimum capital requirement of 6%. The same bank can now only experience a 4% reduction in the value of its assets before breaching the minimum and be considered good for resolving/restructuring/breaking-up by regulators.

For sure, higher minimum requirements have one advantage: depositors are less likely to experience losses. The larger the equity buffer, the stronger the protection.

However, there are also several significant disadvantages.

Given regulators’ current interpretation of the rules, higher minimum requirements also imply a higher sanction trigger. This creates a few problems:

- Raising the minimum threshold does little to protect taxpayers if regulators believe that a bank should be recapitalised, not when its Tier 1 gets close to or below 0%, but when it simply breaches the 6% level. In such case, it might have been possible for the bank’s capital buffer to absorb further losses without erasing its whole capital base and calling for help. For instance, Espirito Santo’s regulators said that its recapitalisation was compulsory: it reported a 5% equity Tier 1 ratio, below the 7% domestic minimum. And the state (i.e. taxpayers) obliged. But… It still had a 5% equity buffer to absorb further losses. Perhaps this would have been sufficient to absorb all losses and spare the taxpayers (perhaps not, but we may never find out).

- When approaching the minimum requirement, bankers are incentivised to start deleveraging in order to avoid breaching. Alternatively, they can be forced by regulators to do so. This has negative consequences on the availability of credit and on the money supply, possibly worsening a crisis through a debt deflation-type bust in order to comply with an artificially-defined 6% level.

- While depositors’ protection can be improved, it isn’t necessarily the case of other creditors, especially in light of the new bail-in rules that make them share the pain (so-called ‘burden-sharing’). Those rules kick in, not when the bank reaches a 0% capital ratio, but when it breaches the regulatory minimum (see here).

- Reaching the minimum requirement can also be self-defeating and self-fulfilling: fearing a bankruptcy event and the loss of their investments, shareholders run to the exit, pushing the share price down to zero and… effectively bringing about the insolvency of the bank. This doesn’t make much sense when a bank still has a 6% capital buffer. Espirito Santo suffered this fate until trading was suspended (see below).

So what’s the ‘effective’ Tier 1 capital ratio? Well, it is the spread between the reported Tier 1 and the minimum regulatory level. A bank that has an 8% Tier 1 under a 4% requirement, and a bank that has a 10% Tier 1 under a 6% requirement have virtually* the same effective capital ratio: 4%.

Regulatory insolvency events also cause operational problems. Espirito Santo was declared insolvent by its regulators but… not by the ISDA association! Setting regulatory minimums at 5% or 25% would have no impact on the issues listed above, as long as this logic is applied. To make regulatory requirements more effective, sanctions in case of breach should be minimal or non-existent in the short-term but should kick in in the long-term if banks’ capitalisation remains too low after a given period of time.

Regulatory minimums exemplify what Bagehot already tried to warn against already at his time: they are bound to create unnecessary panics. Speaking of liquidity reserves (the same reasoning as above applies), he said in Lombard Street:

[Minimums are bad] when legally and compulsorily imposed. In a sensitive state of the English money market the near approach to the legal limit of reserve would be a sure incentive to panic; if one-third were fixed by law, the moment the banks were close to one-third, alarm would begin, and would run like magic. And the fear would be worse because it would not be unfounded—at least, not wholly. If you say that the Bank shall always hold one-third of its liabilities as a reserve, you say in fact that this one-third shall always be useless, for out of it the Bank cannot make advances, cannot give extra help, cannot do what we have seen the holders of the ultimate reserve ought to do and must do.

* ‘virtually’ as, as described above, depositors protection is nonetheless enhanced, though even this is arguable given what happened in Cyprus

Continuously ignoring and misinterpreting history

This recent speech by the Vice President of the ECB, Vítor Constâncio, is in my opinion one of the foremost examples of how a partial reading or misinterpretation of history that becomes accepted as mainstream can lead to bad policy-making.

This speech is typical. Constâncio argues that

the build-up of systemic risk over the financial cycle is an endogenous outcome – a man-made construct – and the job of macro-prudential policy is to try to smoothen this cycle as much as possible. […]

The […] most important source of systemic risk is the risk of the unravelling of financial imbalances. These imbalances may build up gradually, mostly endogenously, and can then unravel abruptly. They form part of the inherent pro-cyclicality of the financial system.

It is crucial to recognise that the financial cycle has an important endogenous component which arises because banks take too much solvency and liquidity risk. The aim of macro-prudential policy should be to temper the financial cycle rather than to merely enhance the resilience of the financial sector ahead of crises.

While Constâncio is right that there is some truth in the pro-cyclicality of financial systems as a long economic boom impairs risk perception, risk assessment and risk premiums, he never highlights why such booms and busts occur in the first place. Outside of negative supply shocks, are they a ‘natural’ consequence of the activity of the economic system? Or are they exogenously triggered by bad government or monetary policies?

Several economic schools of thought have different explanations and theories. Yet, there is one thing that cannot be denied: historical experiences of financial stability.

This is where the flaw of Constâncio’s (and of most central bankers’ and mainstream economists’) thinking resides: history proves that, when the banking sector is left to itself, systemic endogenous accumulation of financial imbalances is minimal, if not non-existent…

According to Larry White in a recent article summing up the history of thought and historical occurrences of free banking, Kurt Schuler identified sixty banking episodes to some extent akin to free banking. White’s paper describes 11 of them, many of which had very few institutional and regulatory restrictions on banking. He quotes Kevin Dowd:

As Kevin Dowd fairly summarizes the record of these historical free banking systems, “most if not all can be considered as reasonably successful, sometimes quite remarkably so.” In particular, he notes that they “were not prone to inflation,” did not show signs of natural monopoly, and boosted economic growth by delivering efficiency in payment practices and in intermediation between savers and borrowers. Those systems of plural note-issue that were panic-prone, like the pre-1913 United States and pre-1832 England, were not so because of competition but because of legal restrictions that significantly weakened banks.

Yet, there is no trace of such events in conventional/mainstream financial history. Central bankers seem to be completely oblivious to those facts (this is surely self-serving) and economists only partially aware of the causes of financial crises. Moreover, free banking episodes also proved that banks were not inherently prone to take “too much solvency and liquidity risk”: indeed, historical records show that banks in such periods were actually well capitalised and rarely suffered liquidity crises. In short, laissez-faire banking’s robustness was far superior to our overly-designed ones’. Consequently we keep making the same mistakes over and over again in believing that a crisis occurred because the previous round of regulation was inadequate…

What we end up with is a banking system shaped by layers and layers of regulations and central banks’ policies. Every financial product, every financial activity, was awarded its own regulation as well as multiple ‘corrective’ rules and patches, was influenced by regulators’ ‘recommendations’, was limited by macro-prudential tools and manipulated through various interest rates under the control by a small central authority. On top of such regulatory intervention, short-term political interference compounds the problem by purposely designing and adjusting financial systems for short-term electoral gains. Markets are distorted in all possible ways as the price system ceases to work adequately, defeating their capital allocation purposes and creating bubbles after bubbles.

Studying banking and financial history demonstrates that it is quite ludicrous to pretend that banking systems are inherently subject to failure through endogenous accumulation of risk. In the quest for an explanation of the crisis, better look at the intersection of moral hazard, political incentives, and the regulatory-originated risk opacity. It might turn out that imbalances are, well, mostly… exogenous.

Please let finance organise itself spontaneously.

Photo: José Carlos Pratas

The era of the neverending bubble?

The IMF got the timing right. It published last week a new ‘Global Housing Watch‘, and warned that house prices were way above trend in a lot of different countries all around the world. The FT also reports here:

The world must act to contain the risk of another devastating housing crash, the International Monetary Fund warned on Wednesday, as it published new data showing house prices are well above their historical average in many countries.

As I said, perfect timing, as this announcement follows my previous post on the influence of Basel’s RWAs on mortgage lending.

As long as international banking authorities don’t get rid of this mechanism, we are likely to experience reoccuring housing bubbles with their devastating economic effects (hint for Piketty: and investors/speculators will have an easy life making capital gains).

PS: I am on holidays until the end of the week, so probably not many updates over the next few days.

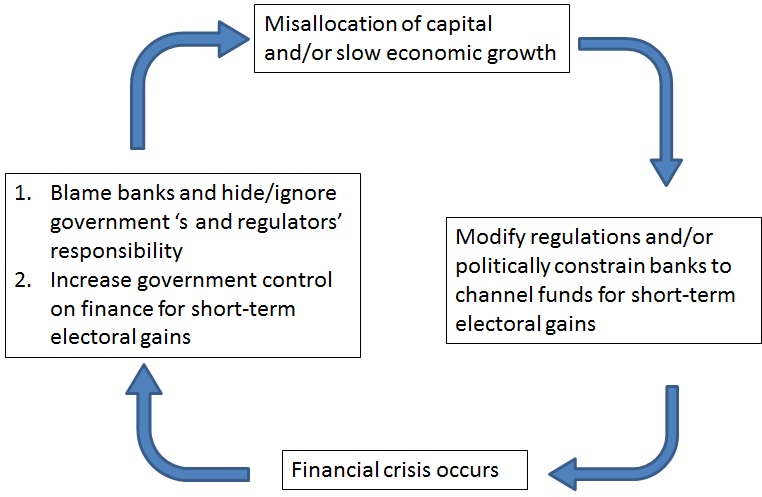

The political banking cycle

A couple of weeks ago, The Economist reported that Mel Watt, the new regulator of the US federal housing agencies Fannie Mae and Freddie Mac, wanted those two agencies to stop shrinking and continue purchasing mortgage loans from banks in order to help homeowners and the housing market (also see the WSJ here). To twist the system further, the compensation of the agencies’ executives will be linked to those political goals. Mr Watt used to be one of the main proponents of more accessible house lending for poor households through Fannie and Freddie before the crisis.

As The Economist asks, “what could go wrong?”…

Lars Christensen and Scott Sumner also find this ridiculously misguided government intervention horrifying. I find myself in complete agreement (and this is an understatement). Who could still honestly say that we are (or were) in a laissez-faire environment?

This, along with UK’s FLS and Help to Buy schemes, made me think that there has been a ‘political banking cycle’ throughout the 20th century. Why 20th century? From all the banking history I’ve read so far, populations seemed to better understand banking before the introduction of safety net measures such as central banks, deposit insurances or systematic government bail-outs. When financial crashes occurred, blame was usually shared between governments and banks, if not governments only. This is why many crises triggered deregulation processes rather than reregulation ones. This contrasts with the mainstream view our society has had since the Great Depression: when a financial crash happens, whatever the government’s responsibility is, banks and free market capitalism are the ones to blame.

This political cycle looks like that:

The worst is: it works. Politicians escaped pretty much unscathed from the financial crisis despite the huge role they played in triggering it*. The majority of the population now sincerely believes that the crisis was caused by greedy bankers (see here, here, here and here). This is as far from the truth as it can be (I don’t deny ‘greed’ played a role though, but channelled through and exacerbated by a combination of other factors, i.e. moral hazard etc.). Unfortunately, it is undeniable: politicians won. And not only politicians won, but they also managed to self-convince that they played no role in the crisis, as the example of Mr Watt shows (he either truly believes that government intervention in the US housing market was a good thing, or he has an incredibly cynical short-term political view).

The crucial question is: why did 19th century populations seem more educated about banking? The answer is that the lack of state paternalism through various protection schemes forced bank depositors and investors to oversee and monitor their banks. Once protection is implemented, there is no incentive or reason anymore to maintain any of those skills.

Who is easier to manipulate: a knowledgeable electorate or an ignorant one?

PS: This chart is mostly accurate for democracies that have a populist tendency. Not all countries seem to be prone to such cycle (this can be due to cultural or institutional arrangements).

* I won’t get into the details here, but if you’re interested, just read Engineering the Financial Crisis, Fragile by Design or Alchemists of Loss……. or simply this NYT article from 1999.

Recent Comments