Breaking banks won’t help economic recovery

In contrast with the bank-bashing environment of the post-crisis period, voices are increasingly being raised to moderate regulatory, political and judiciary risks on the banking system.

Last week, Gillian Tett wrote an article in the FT tittled “Regulatory revenge risks scaring investors away”. She says:

Last month [Roger McCornick’s] project team published its second report on post-crisis penalties, which showed that by late 2013 the top 10 banks had paid an astonishing £100bn in fines since 2008, for misbehaviour such as money laundering, rate-rigging, sanctions-busting and mis-selling subprime mortgages and bonds during the credit bubble. Bank of America headed this league of shame: it had paid £39bn by the end of 2013 for its transgressions. When the 2014 data are compiled, the total penalties will probably have risen towards £200bn.

She argues that “legal risk is now replacing credit risk.” This is a key issue. Banks have already been hit hard by new regulatory requirements, which sometimes require a fundamental restructuring of their business model. The consequences of this framework shift is that profitability, and hence internal capital generation, remain subdued, weakening the system as a whole. Banks now reporting double digit RoEs are more the exceptions than the rule. Moreover, low profitability also reduces the banks’ ability to generate capital externally (i.e. capital raising) because they do not cover their cost of capital. This scares investors away, as they have access to better risk-adjusted investment opportunities elsewhere.

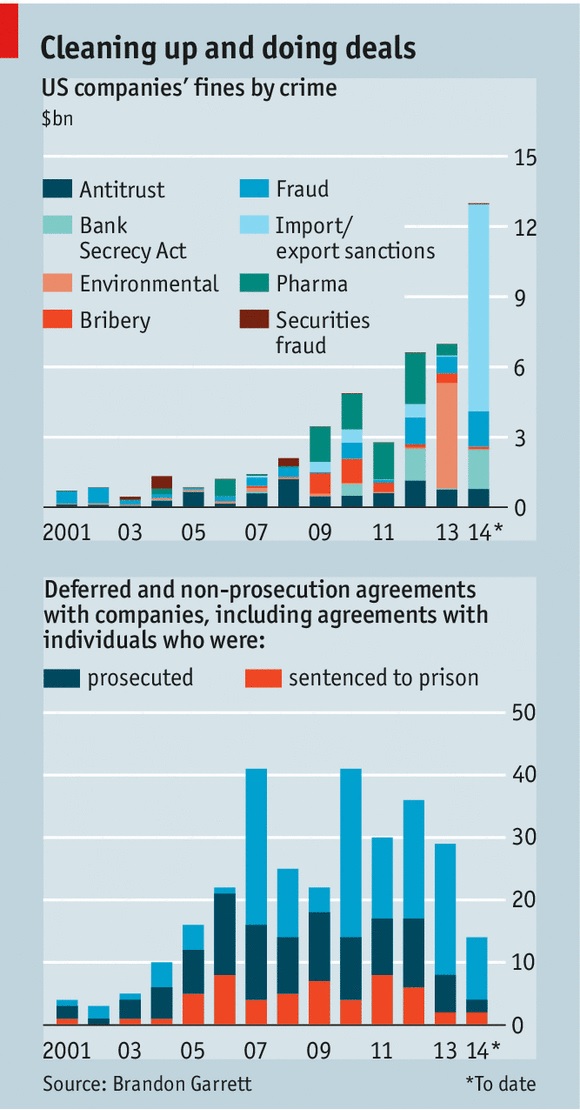

The enormous amounts raised through litigation procedures make such a situation even worse. Admittedly, banks that purposely bypassed laws or committed frauds should be punished. But, as The Economist argues this week in a series of articles called “The criminalisation of American business” (see follow-up article here), the “legal system has become an extortion racket”, whose “most destructive part of it all is the secrecy and opacity” as “the public never finds out the full facts of the case” and “since the cases never go to court, precedent is not established, so it is unclear what exactly is illegal”:

This undermines the predictability and clarity that serve as the foundations for the rule of law, and risks the prospect of a selective—and potentially corrupt—system of justice in which everybody is guilty of something and punishment is determined by political deals. America can hardly tut-tut at the way China’s justice system applies the law to companies in such an arbitrary manner when at times it seems almost as bad itself.

Estimates of capital shortfall at European banks vary between EUR84bn and as much as EUR300bn (another firm, PwC, estimates the shortfall at EUR280bn). Compare those amounts with the hundreds of billions Euros paid or about to be paid by banks as litigation settlements, and it is no surprise that banks have to deleverage to comply with regulatory capital ratio deadlines and upcoming stress tests… Such high amounts, if justified, could probably have been raised by prosecutors at a slower pace in the post-crisis period without endangering the economic recovery (banks’ balance sheets would have been more solid more quickly, which would have facilitated the lending channel of the monetary transmission mechanism).

In the end, regulatory regime uncertainty strikes banks twice: financial regulations keep changing (and new ones are designed), and opaque litigation risk is at an all-time high. Banks are now very risk-averse, depressing lending and international transactions. This seems to me to replicate some of the mistakes made by Roosevelt during the Great Depression. Despite all the central banks’ money injection programmes, this may not be the best way out of an economic crisis…

PS: Commenting on the forthcoming P2P lender Lending Club IPO, Matt Levine argues that:

But Lending Club can grow its balance sheet all it wants. Lending Club is not a bank. So it’s not subject to banking regulation, which means that it can do a core function of banking much more efficiently than an actual bank can.

He is (at least) partly right. By killing banks, regulatory constraints are likely to trigger the emergence of new types of lenders.

Wait… Isn’t it what’s already happened (MMF and other shadow banking entities…)?

Recent Comments