NESTA’s alternative finance data goldmine

NESTA, a UK-based charity promoting innovation (and which also organised the annual UK Barcamp Bank), just released its new report on alternative finance trends in the UK. It is a goldmine. The report if full of interesting charts and figures and in many ways tells us a lot about the current state of our traditional financial sector (and possibly of the stance of monetary policy).

Some charts and comments are of particular interest. To my surprise, business lending through P2P platforms was the biggest provider of funds in terms of total amount:

According to the report:

79 per cent of borrowers had attempted to get a bank loan before turning to P2P business lending, with only 22 per cent of borrowers being offered a bank loan. 33 per cent thought it was unlikely or very unlikely that they would have been able to secure funding elsewhere had they not been successful in getting a loan through the P2P business lending platform, whereas 44 per cent of respondents thought they would have been likely or very likely to secure funding from other sources had they not used P2P business lending.

Given bank regulation that penalises banks for lending to small firms, none of this is surprising. As I keep saying, regulation is the primary driver of financial innovation. P2P business lending owes a lot to regulators… until it gets regulated itself?

Another very interesting chart was the following one:

This is crazy. Wealthy people pretty much shun P2P and other alternative finance forms. Why is that? Here’s my theory: wealthy people are usually well advised financially and have access to more investment opportunities than less-wealthy household. Consequently, a low interest environment isn’t that much of a problem (in the short-term): they have the ability to move down the risk scale to look for extra yield. On the other hand, household with more ‘moderate’ incomes do not have access to such investment opportunities: they are the ones hit by low returns on investments. P2P provides them with a unique opportunity to boost the meagre returns on their savings as long as real interest rates remain that low (i.e. lower than inflation):

[The funders] in P2P lending and equity-based crowdfunding were primarily driven by the prospect of financial returns with less concern for backing local businesses or supporting social causes.

Figures concerning P2P consumer lending are similar.

Those figures are both worrying and encouraging. Worrying because the harm that low interest rates and regulation seem to have on the economy and the traditional banking sector. Encouraging because finance is reorganising itself to respond to both borrowers’ and lenders’ demands. This is spontaneous order at work. Let just hope this does not add another layer of complexity and opacity to our already overly-complex financial system.

Blurry banks’ future is

A lot of articles on financial innovation and disruption in the FT over the last few days. Here, John Gapper argues that tech firms aim at using the existing financial system rather than challenge it. Here, Martin Arnold argues that banks shouldn’t forget their traditional branch network as this is how they make money through their oldest and wealthiest clients. Here, Luke Johnson argues that crowdfunding is riskier but also more exciting and, in a way, is the future.

John Gapper is right to point out that the regulatory and capital costs of setting up new bank-alike lending entities are very high. Yet he probably overstates his case. P2P lenders do not provide bank-type services: technology has enabled disintermediation by allowing investors to lend money (almost) directly to borrowers, but the money invested is stuck and does not represent a means of payment, unlike bank deposits. P2P lenders have the ability to take over a large market share of the lending market; and their business model does not require a high operating, regulatory and capital costs base (at least for now…). This is where the traditional intermediated lending channel could effectively approach death. On the other hand, P2P lender cannot handle deposits and banks still have a near-monopoly in this area.

Of course, we could imagine a 100%-reserve banking world in which the lending channel has moved entirely to P2P lenders, mutual and hedge funds and equivalent, whereas the deposit and payment system has moved entirely to Paypal-like payment firms. And this excludes alternative options offered by cryptocurrencies. In this world, banks are effectively dead.

Still, I am far from sure this would be the best solution: banks provide an elastic supply of currency (fractional reserve banking) that can adapt to the demand for money. (We could imagine a world without banks but still an elastic currency supply, if for instance the whole money supply only comprised competing cryptocurrencies. Let’s say this is highly unlikely to happen in the foreseeable future)

Banks can also survive by benefiting from those technologies (if ever they dare touching their antique IT systems…). As I’ve been saying for a while, banks can leverage their huge customer base to set up their own P2P/crowdfunding platform. This has already started to happen: RBS just announced the creation of its own P2P lending platform, Santander announced a partnership with Funding Circle, Lending Club is developing partnerships with many US banks. Banks could earn a fee from referring customers to their own (or third-party) platform, while deleveraging and reducing their on-balance sheet credit risk. Investors would earn more on those investments than on time deposits, but bear some risk.

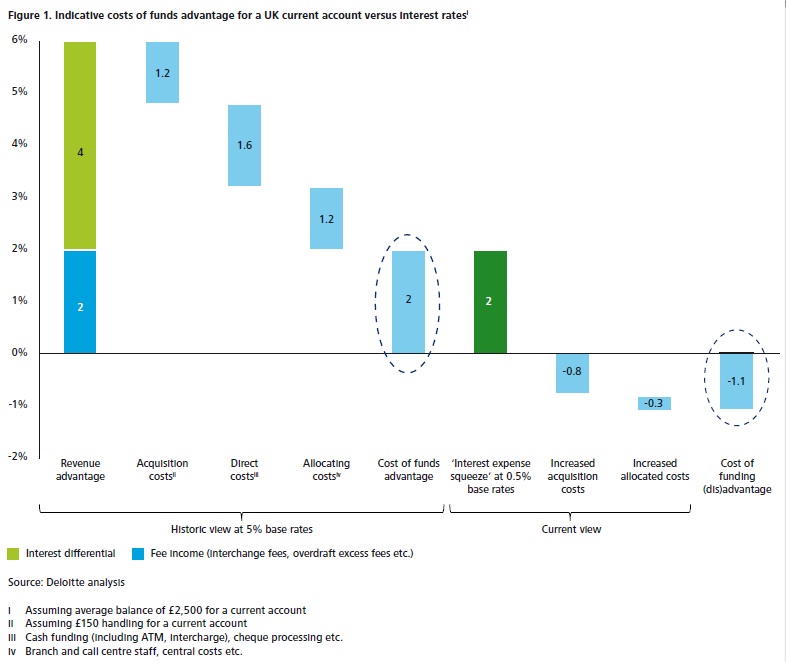

Whatever they decide to do, banks will have to adapt. But timing is key. Gapper referred to this recent, excellent, Deloitte report. They explain the margin compression effect (due to low base rates)*, which depresses banks’ profitability and adds another challenge on top of those that tech-enabled competitors and regulation already represent. According to them, closing down branches and moving online does not sufficiently slash cost to offset the decrease in net interest income. Closing down branches too quickly could also hurt banks by alienating the part of their client base born before the internet age. Deloitte provides evidence that a radical restructuring of IT systems could significantly improve returns, but this requires investments, which banks aren’t necessarily willing to undertake in a period of below-cost of capital RoE.

As the internet makes it easier for customers to compare pricing through aggregators and hence more difficult for banks to ‘extract value’ from them (what they call ’privileged access’), they recommend banks enhance ‘customer proposition’ (i.e. use ‘big data’) and focus on SME lending. As I’ve argued on this blog, capital regulation makes this difficult. They also indeed support the idea of in-house P2P platform, mostly to focus on local SMEs. This would help with capital requirements by maintaining SME exposures off-balance sheet, the risk borne by customers. Banks could effectively become risk assessment providers: rating lending opportunities to help customers (which include investment funds that don’t have such in-house capabilities) make their investment choices.

At the end of the day, banks are indeed likely to die if they don’t adapt. But also if they adapt too quickly. We could however see in the future surviving banks increasingly becoming like non-banks and non-banks increasingly providing banking services. The distinction between both types of institutions is likely to get very blurry. (That is, if regulation doesn’t kill non-banks first)

* Ben Southwood reiterated that interest rates are determined by markets and not by central banks. I already wrote responses to those claims here and here. Scott Sumner just mentioned his latest post, so I thought it would be a good idea to share Deloitte’s insight and own explanation of the margin compression effect and why “the spreads between Bank Rate and market rates seem to be narrow and fairly consistent—until they’re not.” In reality, lending spreads fluctuate only slightly when rates are above a certain threshold (i.e. banks’ risk-adjusted operating costs) and widen when they drop below it (explaining the “until they’re not”; see my previous posts). The fact that the “until they’re not” occurs does not imply that lending rates are “determined by the market”.

Here’s Deloitte own version:

The interest rate paid by banks on current accounts is typically lower than those paid for lump sum deposits (and the rates paid to borrow in the wholesale markets). However, this interest rate does not reflect the full cost of acquiring and servicing these current accounts. In the past, these acquisitions and servicing costs were offset by the fact that banks did not have to pay very high interest rates on current accounts.

Until the financial crisis, central bank interest rates (the ‘base rate’) were traditionally much higher. This meant that current account rates could easily be 500 or more basis points (hundredths of a percentage point) below lump-sum deposit rates.

Because base rates are at unprecedented lows, that maths does not work. Base rates have been low since 2009, and central bankers have signalled that they are likely to stay that way for some time yet. Figure 1 shows the economics of current accounts in the UK, where banks typically do not charge for them. A 200 basis point margin generated by current accounts when base rates are at 5 per cent turns into a 110 basis point loss at a 0.5 per cent base rate.

Two kinds of financial innovation

Paul Volcker famously said that the only meaningful financial innovation of the past decades was the ATM. Not only do I believe that his comment was strongly misguided, but he also seemed to misunderstand the very essence of innovation in the financial services sector.

Financial innovations are essentially driven by:

- Technological shocks: new technologies (information-based mostly) allow banks to adapt existing financial products and risk management techniques to new technological paradigms. Without tech shocks, innovations in banking and finance are relatively slow to appear.

- Regulatory arbitrage: financiers develop financial products and techniques that bypass or use loopholes in existing regulations. Some of those regulatory-driven innovations also benefit from the appearance of new technological and theoretical paradigms. Those innovations are typically quick to appear.

I usually view regulatory-driven innovations as the ‘bad’ ones. Those are the ones that add extra layers of complexity and opacity to the financial system, hiding risks and misleading investors in the process.

It took a little while, but financial innovations are currently catching up with the IT revolution. Expect to change the way you make or receive payments or even invest in the near future.

See below some of the examples of financial innovation in recent news. Can you spot the one(s) that is(are) the most likely to lead to a crisis, and its underlying driver?

- Bank branches: I have several times written about this, but a new report by CACI and estimates by Deutsche Bank forecasted that between 50% and 75% of all UK branches will have disappeared over the next decade. Following the growing branch networks of the 19th and 20th centuries, which were seen as compulsory to develop a retail banking presence, this looks like a major step back. Except that this is actually now a good thing as the IT and mobile revolution is enabling such a restructuring of the banking sector. SNL lists 10,000 branches for the top 6 UK bank and 16,000 in Italy. Cutting half of that would sharply improve banks’ cost efficiency (it would, however, also be painful for banks’ employees). It is widely reported that banks’ branches use has plunged over the past three years due to the introduction of digital and mobile banking.

- In China, regulators have introduced new rules to try to make it harder for mainstream banks to deal with shadow banks in order to slow the growth of the Chinese shadow banking system, which has grown to USD4.9 trillion from almost nothing just a few years ago. The Economist reports that, by using a simple accounting trick, banks got around the new rules. Moreover, while Chinese regulators are attempting to constrain investments in so-called trust and asset management companies, investors and banks have now simply moved the new funds to new products in securities brokerage companies.

- In London, underground travellers can now pay for their journey by simply using their contactless bank card. No need of a specific underground card anymore. NFC-enabled smartphones will be able to do the same in the near future.

- Barclays is experimenting contactless wristband that would effectively replace your contactless card for payments (or, for Londoners, your underground Oyster Card).

- Apple announced Apple Pay, a contactless payment system managed by Apple through its new iPhones and Watch devices. Apple will store your bank card details and charge your account later on. This allows users to bypass banks’ contactless payments devices entirely. Vodafone also just released a similar IT wallet-contactless chip system (why not using the phone’s NFC system though? I don’t know. Perhaps they were also targeting customers that did not own NFC-enabled devices).

- Lending Club, the large US-based P2P lending firm, has announced its IPO. This is a signal that such firms are now becoming mainstream, as well as growing competitors to banks.

Of course, a lot more is going on in the financial innovation area at the moment, and I only highlighted the most recent news. Identifying the regulatory arbitrage-driven innovations will help us find out where the next crisis is most likely to appear.

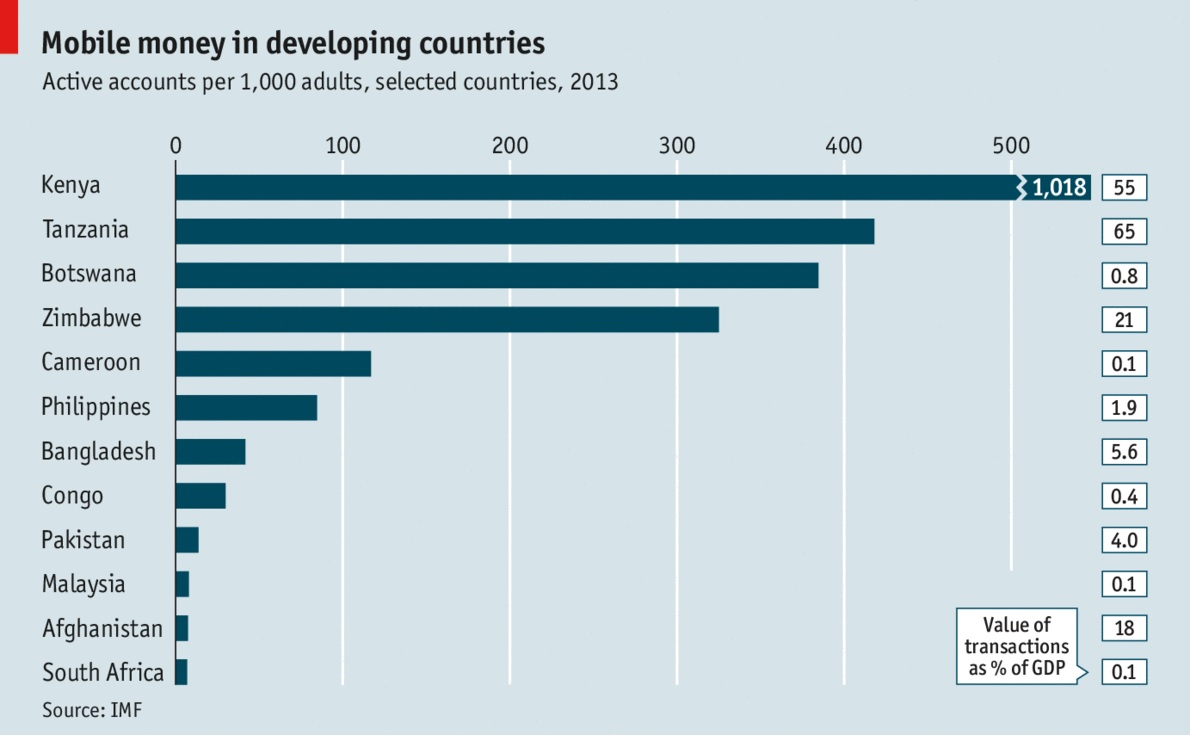

PS: the growth of cashless IT wallets has interesting repercussions on banks’ liquidity management and ability to extend credit (endogenous inside money creation), by reducing the drain of physical cash on the whole banking system’s reserves (outside money). If African economies are any guide to the future (see below, from The Economist), cash will progressively disappear from circulation without governments even outlawing it.

Breaking banks won’t help economic recovery

In contrast with the bank-bashing environment of the post-crisis period, voices are increasingly being raised to moderate regulatory, political and judiciary risks on the banking system.

Last week, Gillian Tett wrote an article in the FT tittled “Regulatory revenge risks scaring investors away”. She says:

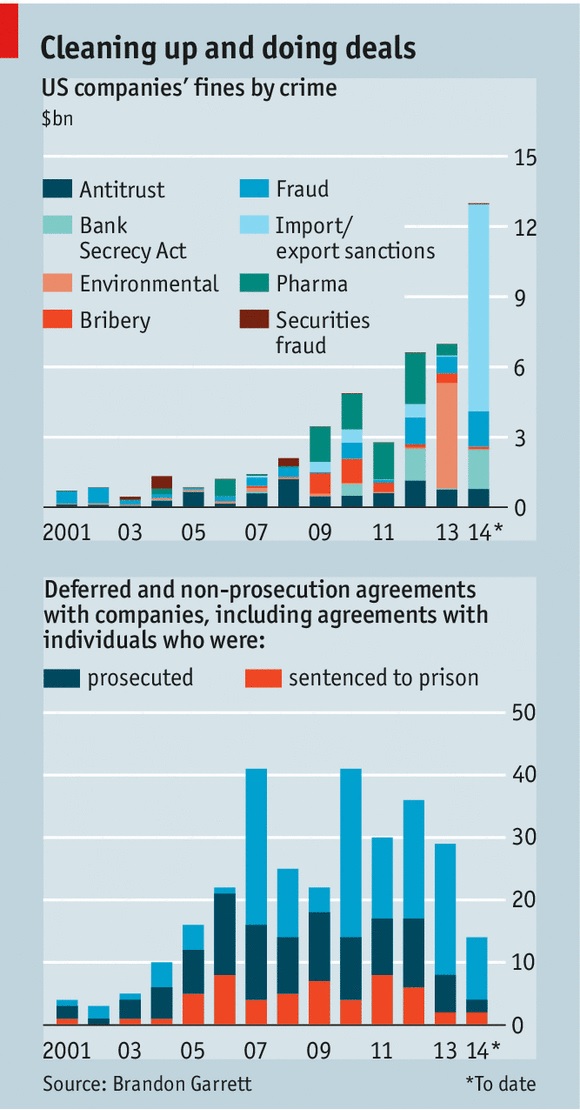

Last month [Roger McCornick’s] project team published its second report on post-crisis penalties, which showed that by late 2013 the top 10 banks had paid an astonishing £100bn in fines since 2008, for misbehaviour such as money laundering, rate-rigging, sanctions-busting and mis-selling subprime mortgages and bonds during the credit bubble. Bank of America headed this league of shame: it had paid £39bn by the end of 2013 for its transgressions. When the 2014 data are compiled, the total penalties will probably have risen towards £200bn.

She argues that “legal risk is now replacing credit risk.” This is a key issue. Banks have already been hit hard by new regulatory requirements, which sometimes require a fundamental restructuring of their business model. The consequences of this framework shift is that profitability, and hence internal capital generation, remain subdued, weakening the system as a whole. Banks now reporting double digit RoEs are more the exceptions than the rule. Moreover, low profitability also reduces the banks’ ability to generate capital externally (i.e. capital raising) because they do not cover their cost of capital. This scares investors away, as they have access to better risk-adjusted investment opportunities elsewhere.

The enormous amounts raised through litigation procedures make such a situation even worse. Admittedly, banks that purposely bypassed laws or committed frauds should be punished. But, as The Economist argues this week in a series of articles called “The criminalisation of American business” (see follow-up article here), the “legal system has become an extortion racket”, whose “most destructive part of it all is the secrecy and opacity” as “the public never finds out the full facts of the case” and “since the cases never go to court, precedent is not established, so it is unclear what exactly is illegal”:

This undermines the predictability and clarity that serve as the foundations for the rule of law, and risks the prospect of a selective—and potentially corrupt—system of justice in which everybody is guilty of something and punishment is determined by political deals. America can hardly tut-tut at the way China’s justice system applies the law to companies in such an arbitrary manner when at times it seems almost as bad itself.

Estimates of capital shortfall at European banks vary between EUR84bn and as much as EUR300bn (another firm, PwC, estimates the shortfall at EUR280bn). Compare those amounts with the hundreds of billions Euros paid or about to be paid by banks as litigation settlements, and it is no surprise that banks have to deleverage to comply with regulatory capital ratio deadlines and upcoming stress tests… Such high amounts, if justified, could probably have been raised by prosecutors at a slower pace in the post-crisis period without endangering the economic recovery (banks’ balance sheets would have been more solid more quickly, which would have facilitated the lending channel of the monetary transmission mechanism).

In the end, regulatory regime uncertainty strikes banks twice: financial regulations keep changing (and new ones are designed), and opaque litigation risk is at an all-time high. Banks are now very risk-averse, depressing lending and international transactions. This seems to me to replicate some of the mistakes made by Roosevelt during the Great Depression. Despite all the central banks’ money injection programmes, this may not be the best way out of an economic crisis…

PS: Commenting on the forthcoming P2P lender Lending Club IPO, Matt Levine argues that:

But Lending Club can grow its balance sheet all it wants. Lending Club is not a bank. So it’s not subject to banking regulation, which means that it can do a core function of banking much more efficiently than an actual bank can.

He is (at least) partly right. By killing banks, regulatory constraints are likely to trigger the emergence of new types of lenders.

Wait… Isn’t it what’s already happened (MMF and other shadow banking entities…)?

Hummel vs. Haldane: the central bank as central planner

Recent speeches and articles from most central bankers are increasingly leaving a bad aftertaste. Take this latest article by Andrew Haldane, Executive Director at the BoE, published in Central Banking. Haldane describes (not entirely accurately…) the history and evolution of central banking since the 19th century and discusses two possible paths for the next 25 years.

His first scenario is that central banks and regulation will step backward and get back to their former, ‘business as usual’, stance, focusing on targeting inflation and leaving most of the capital allocation work to financial markets. He views this scenario as unlikely. He believes that the central banks will more tightly regulate and intervene in all types of asset markets (my emphasis):

In this world, it would be very difficult for monetary, regulatory and operational policy to beat an orderly retreat. It is likely that regulatory policy would need to be in a constant state of alert for risks emerging in the financial shadows, which could trip up regulators and the financial system. In other words, regulatory fine-tuning could become the rule, not the exception.

In this world, macro-prudential policy to lean against the financial cycle could become more, not less, important over time. With more risk residing on non-bank balance sheets that are marked-to-market, it is possible that cycles in financial assets would be amplified, not dampened, relative to the old world. Their transmission to the wider economy may also be more potent and frequent. The demands on macro-prudential policy, to stabilise these financial fluctuations and hence the macro-economy, could thereby grow.

In this world, central banks’ operational policies would be likely to remain expansive. Non-bank counterparties would grow in importance, not shrink. So too, potentially, would more exotic forms of collateral taken in central banks’ operations. Market-making, in a wider class of financial instruments, could become a more standard part of the central bank toolkit, to mitigate the effects of temporary market illiquidity droughts in the non-bank sector.

In this world, central banks’ words and actions would be unlikely to diminish in importance. Their role in shaping the fortunes of financial markets and financial firms more likely would rise. Central banks’ every word would remain forensically scrutinised. And there would be an accompanying demand for ever-greater amounts of central bank transparency. Central banks would rarely be far from the front pages.

He acknowledged that central banks’ actions have already considerably influenced (distorted?…) financial markets over the past few years, though he views it as a relatively good thing (my emphasis):

With monetary, regulatory and operational policies all working in overdrive, central banks have had plenty of explaining to do. During the crisis, their actions have shaped the behaviour of pretty much every financial market and institution on the planet. So central banks’ words resonate as never previously. Rarely a day passes without a forensic media and market dissection of some central bank comment. […]

Where does this leave central banks today? We are not in Kansas any more. On monetary policy, we have gone from setting short safe rates to shaping rates of return on longer-term and wider classes of assets. On regulation, central banks have gone from spectator to player, with some granted micro-prudential as well as macro-prudential regulatory responsibilities. On operational matters, central banks have gone from market-watcher to market-shaper and market-maker across a broad class of assets and counterparties. On transparency, we have gone from blushing introvert to blooming extrovert. In short, central banks are essentially unrecognisable from a quarter of a century ago.

This makes me feel slightly unconfortable and instantly remind me of the – now classic – 2010 article by Jeff Hummel: Ben Bernanke vs. Milton Friedman: The Federal Reserve’s Emergence as the U.S. Economy’s Central Planner. While I believe there are a few inaccuracies and omissions in Hummel’s description of the financial crisis, his article is really good and his conclusion even more valid today than at the time of his writing:

In the final analysis, central banking has become the new central planning. Under the old central planning—which performed so poorly in the Soviet Union, Communist China, and other command economies—the government attempted to manage production and the supply of goods and services. Under the new central planning, the Fed attempts to manage the financial system as well as the supply and allocation of credit. Contrast present-day attitudes with the Keynesian dark ages of the 1950s and 1960s, when almost no one paid much attention to the Fed, whose activities were fairly limited by today’s standard. […]

As the prolonged and incomplete recovery from the recent recession suggests, however, the Fed’s new central planning, like the old central planning, will ultimately prove an unfortunate and possibly disastrous failure.

The contrast between central bankers’ (including Haldane’s) beliefs of a tightly controlled financial sector to those of Hummel couldn’t be starker.

Where it indeed becomes really worrying is that Hummel was only referring to Bernanke’s decision to allocate credit and liquidity facilities to some particular institutions, as well as to the multiplicity of interest rates and tools implemented within the usual central banking framework. At the time of his writing, macro-prudential policies were not as discussed as they are now. Nevertheless, they considerably amplify the central banks’ central planner role: thanks to them, central bankers can decide to reduce or increase the allocation of loanable funds to one particular sector of the economy to correct what they view as financial imbalances.

Moreover, central banks are also increasingly taking over the role of banking regulator. In the UK, for instance, the two new regulatory agencies (FCA and PRA) are now departments of the Bank of England. Consequently, central banks are in charge of monetary policy (through an increasing number of tools), macro-prudential regulation, micro-prudential regulation, and financial conduct and competition. Absolutely all aspects of banking will be defined and shaped at the central bank level. Central banks can decide to ‘increase’ competition in the banking sector as well as favour or bail-out targeted firms. And it doesn’t stop here. Tighter regulatory oversight is also now being considered for insurance firms, investment managers, various shadow banking entities and… crowdfunding and peer-to-peer lending.

Hummel was right: there are strong similarities between today’s financial sector planning and post-WW2 economic planning. It remains to be seen how everything will unravel. Given that history seems to point to exogenous origins of financial imbalances (whereas central bankers, on the other hand, believe in endogenous explanations, motivating their policies), this might not end well… Perhaps this is the only solution though: once the whole financial system is under the tight grip of some supposedly-effective central planner, the blame for the next financial crisis cannot fall on laissez-faire…

News digest: P2P lending and HFT, CoCo bonds, Co-op Bank…

Ron Suber, President at Prosper, the US-based P2P lending company, sent me a very interesting NY Times article a few days ago. The article is titled “Loans That Avoid Banks? Maybe Not.” This is not really accurate: the article indeed mentions institutional investors such as mutual and hedge funds increasingly investing in bundles of P2P loans through P2P platforms, but never refers to banks. Unlike what the article says, I don’t think platforms were especially set up to bypass institutional investors… They were set up to bypass banks and their costly infrastructure and maturity transformation.

Some now fear that the industry won’t be ‘P2P’ for very long as institutional investors increasingly take over a share of the market. I think those beliefs are misplaced. Last year, I predicted that this would create opportunities for niche players to enter the market, focusing on real ‘P2P’.

A curious evolution is the application of high-frequency trading strategies to P2P. I haven’t got a lot of information about their exact mechanisms, but I doubt they would resemble the ones applied in the stock market given that P2P is a naturally illiquid and borrower-driven market.

The main challenge of the industry at the moment seems to be the lack of potential customer awareness. Despite offering better deals (i.e. cheaper borrowing rates) than banks, demand for loans remains subdued and the industry tiny next to the banking sector.

In this FT article, Alberto Gallo, head of macro-credit research at RBS, argues that regulators should intervene on banks’ contingent convertible bonds’ risks. I think this is strongly misguided. Investors’ learning process is crucial and relying on regulators to point out the potential risks is very dangerous in the long-term. Not only such paternalism disincentives investors to make their own assessment, but also regulators have a very bad track record at spotting risks, bubbles and failures (see Co-op bank below).

This piece here represents everything that’s wrong with today’s banking theory:

We know that a combination of transparency, high capital and liquidity requirements, deposit insurance and a central bank lender of last resort can make a financial system more resilient. We doubt that narrow banking would.

Not really… They also argue that 100% reserve banking would not prevent runs on banks:

The mutual funds of the narrow banking world would be subject to the same runs. Indeed, recent research highlights that – in the presence of small investors – relatively illiquid mutual funds are more likely to face exit in the event of past bad performance. […] Since the mutual funds would be holding illiquid loans – remember, they are taking over functions of banks – collective attempts at liquidation to meet withdrawal requests would lead to ruinous fire sales.

They misunderstand the purpose of such a banking system. Those ‘mutual funds’ would not be similar to the ones we currently have, which invests in relatively liquid securities on the stock market, and can as a result exit their positions relatively quickly and easily. Those 100% reserve funds would invest in illiquid loans and investors in those funds would have their money contractually locked in for a certain time. With no legal power to withdraw, no risk of bank run.

The FT reported a few days ago the results of the investigation on the Co-operative bank catastrophe. Despite regulators not noticing any of the problems of the bank, from corporate governance to bad loans and capital shortfall, as well as approving unsuitable CEOs and mergers, the report recommends to… “heed regulatory warnings.” I see…

The impossible sometimes happens: I actually agree with Paul Krugman’s last week piece on endogenous money. No guys, the BoE paper didn’t reveal any mystery of banking or anything…

Finally, Chris Giles wrote a very good article in the FT today, very clearly highlighting the contradictions in the Bank of England policies and speeches, and their tendency to be too dovish whatever the circumstances:

Mark Carney, the governor, certainly displays dovish leanings. Before he took the top job, he said monetary policy could be tightened once growth reached “escape velocity”. But now that growth has shot above 3 per cent, he advocates waiting until the economy has “sustained momentum” – without acknowledging that his position has changed. His attitude to prices also betrays a knee-jerk dovishness. When inflation was above target, he stressed the need to look at forecasts showing a more benign period ahead. Now that inflation is lower it is apparently the short-term data that matters – and it justifies stimulus.

So much for forward guidance… Time to move to a rule-based monetary policy?

Crowdfunding, naivety and scandals

John Kay wrote an interesting article for the FT yesterday, titled “Regulators will get the blame for the stupidity of crowds.” He argues that, despite crowdfunding and P2P enthousiasts blaming regulators for being too slow and too cautious, this new market will eventually crash and trigger calls for more advanced regulation as well as the setup of compensation schemes. Desintermediation firms would then reintermediate lending and effectively transform into… banks.

I partly agree with Kay. A collapse/crash/losses/fraud/scandals is/are inevitable. And this is a good thing.

I have already written about the importance of failure in free market financial systems. New financial innovations need to experience failures in order to end up reinforced, to distinguish what works from what doesn’t work. This is a Darwinian learning process. The system then becomes ‘antifragile’. Consequently, the state should refrain from intervening in order not to postpone this necessary learning process and resulting adjustments. When crowdfunding crashes, the state should resist any call for intervention/bailout/regulation. This is the only way crowdfunding can become a mature industry.

I however also partly disagree with Kay, who I believe does not see the bigger picture.

Kay argues that investors (in this case ‘crowds’) are naïve. That intermediation has benefits and non-professional investors lack the ‘cynicism’ to assess the risk/reward profile of those investments.

Where Kay is wrong though, is in considering P2P lending as “a substitute for deposit account.” It is not. P2P lending is an investment. Unsophisticated retail investors can also lose much of their money by investing in various stocks. Or by betting on the wrong horse. I don’t believe investors mistake crowdfunding for bank deposits…

I think that what Kay also fails to see is that, if historically many start-ups and young SMEs have struggled to grow and eventually failed, it is partly because they lacked the funds required to grow. Some start-ups ended-up collapsing or selling themselves to larger competitors simply because funding became scarce at the second or third round of funding. This funding gap was particularly prevalent in some markets such as the UK (less so in the US). Some other markets, such as France, on the other hand, lack first round financing (seed funding, mainly provided by ‘Angel’ investors).

When the supply for loanable funds is scarce relative to the demand, demanded return on investment is high. Many new firms, particularly in non-growth markets, find it hard to cope with this situation and are pretty much avoided by venture capital investors. What equity crowdfunding and P2P lending do is to increase the supply of loanable funds, reducing the average required rate of return. Refinancing risk mechanically recedes, guaranteeing the success or the failure of an SME on its business strategy and execution alone.

In addition, crowdfunding multiply investment opportunities, making it easier to diversify a portfolio of investments. Historically, venture capital funds could not diversify too much if they wanted to maintain appropriate levels of returns.

Scandals are inevitable, but the learning mechanism inherent to the market process must be allowed to run its course. Learning, combined with the increased supply of loanable funds, would reduce the probability of scandals occurring in the long-run and make crowdfunding a solid industry.

Could P2P Lending help monetary policy break through the ‘2%-lower bound’?

The ‘cut the middle man’ effect of P2P lending is already celebrated for offering better rates to both lenders and borrowers. But what many people miss is that this effect could also ease the transmission mechanism of central banks’ monetary policy.

I recently explained that the banking channel of monetary policy was limited in its effects by banks’ fixed operational costs. I came up with the following simplified net profit equation for a bank that only relies on interest income on floating rate lending as a source of revenues:

Net Profit = f1(central bank rate) – f2(central bank rate) – Costs, with

f1(central bank rate) = interest income from lending

= central bank rate + margin and,

f2(central bank rate) = interest expense on deposits

= central bank rate – margin

(I strongly advise you to take a look at the details here, which was a follow-up to my response to Ben Southwood’s own response on the Adam Smith Institute blog to my original post…which was also a response to his own original post…)

Consequently, banks can only remain profitable (from an accounting point of view) if the differential between interest income and interest expense (i.e. the net interest income) is greater than their operational costs:

Net interest income >= Costs

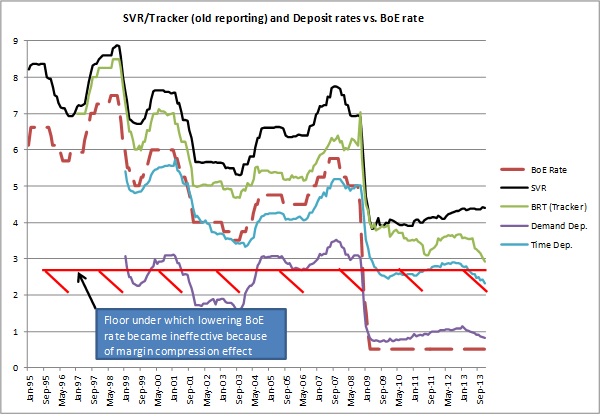

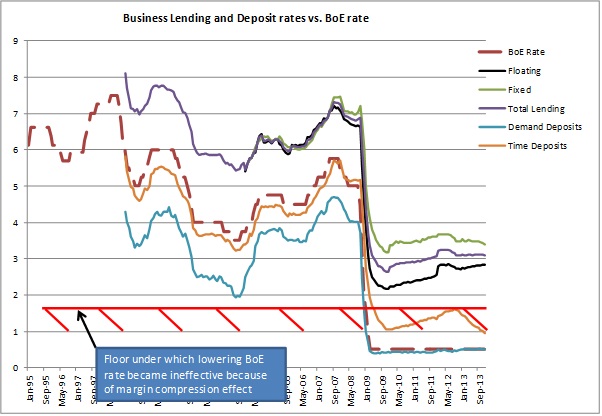

When the central bank base rate falls below a certain threshold, f2 reaches zero and cannot fall any lower, while f1 continues to decrease. This is the margin compression effect.

Above the threshold, the central bank base rate doesn’t matter much. Below, banks have to increase the margin on variable rate lending in order to cover their costs. This was evidenced by the following charts:

As the UK experience seems to show, banks stopped passing BoE rate cuts on to customers around a 2% BoE rate threshold. I called this phenomenon the ‘2%-lower bound’. I have yet to take a look at other countries.

Enter P2P lending.

By directly matching savers and borrowers and/or slicing and repackaging parts of loans, P2P platforms cut much of banks’ vital cost base. P2P platforms’ online infrastructure is much less cost-intensive than banks’ burdensome branch networks. As a result, it is well-known that both P2P savers and borrowers get better rates than at banks, by ‘cutting the middle man’. This is easy to explain using the equations described above, as costs approach zero in the P2P model. This is what Simon Cunningham called “the efficiency of Peer to Peer Lending”. As Simon describes:

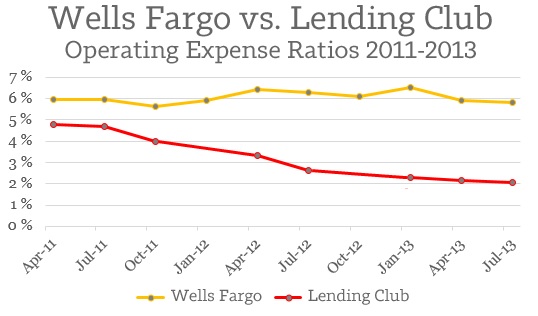

Looking purely at the numbers, Lending Club does business around 270% more efficiently than the comparable branch of a major American bank

Simon calculated the ‘efficiency’ of each type of lender by dividing the outstanding loans of Wells Fargo and Lending Club by their respective operational expenses (see chart below). I believe Lending Club’s efficiency is still way understated, though this would only become apparent as the platform grows. The marginal increase in lending made through P2P platforms necessitates almost no marginal increase in costs.

Perhaps P2P platforms’ disintermediation model could lubricate the banking channel of monetary policy the closer central banks’ base rate gets to the zero bound?

Possibly. From the charts above, we notice that the spread between savings rates and lending rates that banks require in order to cover their costs range from 2 to 3.5%. This is the cost of intermediation and maturity transformation. Banks hire experts to monitor borrowers and lending opportunities in-house and operate costly infrastructures as some of their liabilities (i.e. demand deposits) are part of the money supply and used by the payment system.

However, disintermediated demand and supply for loanable funds are (almost) unhampered by costs. As a result, the differential between borrowers and savers’ rate can theoretically be minimal, close to zero. That is, when the central bank lowers its target rate to 0%, banks’ deposit rates and short-term government debt yield should quickly follow. Time deposits and longer-dated government debt will remain slightly above that level. Savers would be incentivised to invest in P2P if the proposed rate at least matches them, adjusting for credit risk.

Let’s take an example: from the business lending chart above, we notice that business time deposit rates are currently quoted at around 1%. However, business lending is currently quoted at an average rate of about 3%. Banks generate income from this spread to pay salaries and other fixed costs, and to cover possible loan losses. Let’s now imagine that companies deposit their money in a time deposit-equivalent P2P product, yielding 1.5%. Theoretically, business lending could be cut to only slightly above 1.5%. This represents a much cheaper borrowing rate for borrowers.

P2P platforms would thus more closely follow the market process: the law of supply and demand. If most investments start yielding nothing, P2P would start attracting more investors through arbitrage, increasing the supply of loanable funds, and in turn lowering rates to the extent that they only cover credit risk.

The only limitation to this process stems from the nature of products offered by platforms. Floating rate products tend to be the most flexible and quickly follow changes in central banks’ rates. Fixed rate products, on the other hand, take some time to reprice, introducing a time lag in the implementation of monetary policy. I believe that most P2P products originated so far were fixed rate, though I could not seem to find any source to confirm that.

In the end, P2P lending is similar to market-based financing. The bond market already ‘cuts the middle man’, though there remains fees to underwriting banks, and only large firms can hope to issue bonds on the financial markets. In bond markets, investors exactly earn the coupon paid by borrowers. There is no differential as there is no middle man, unlike in banking. P2P platforms are, in a way, mini fixed-income markets that are accessible to a much broader range of borrowers and investors.

However, I view both bond markets and P2P lending as some version of 100%-reserve banking. While they could provide an increasingly large share of the credit supply, banks still have a role to play: their maturity transformation mechanism provides customers with a means of storing their money and accessing it whenever necessary. Would P2P platform start offering demand deposit accounts, their cost base would rise closer to that of banks, potentially raising the margin between savers and borrowers as described above.

It seems that, by partly shifting from the banking channel to the P2P channel over time, monetary policy could become more effective. I am sure that Yellen, Carney and Draghi will appreciate.

News digest: Scotland, CoCos and electronic trading

Sam Bowman had a very good piece on the Adam Smith Institute blog about Scotland setting up a pound Sterling-based free banking system unilaterally (yeah I know I keep mentioning this blog now, but activity there seems to have been picking up recently). It draws on George Selgin’s post and is a very good read. One particular point was more than very interesting in the context of my own blog (emphasis added):

George Selgin has pointed to research by the Federal Reserve Bank of Atlanta about the Latin American countries that unilaterally use the dollar. Because these countries – Panama, Ecuador and El Salvador – lack a Lender of Last Resort, their banking systems have had to be far more prudent and cautious than most of their neighbours.

Panama, which has used the US Dollar for one hundred years, is the most useful example because it is a relatively rich and stable country. A recent IMF report said that:

“By not having a central bank, Panama lacks both a traditional lender of last resort and a mechanism to mitigate systemic liquidity shortages. The authorities emphasized that these features had contributed to the strength and resilience of the system, which relies on banks holding high levels of liquidity beyond the prudential requirement of 30 percent of short-term deposits.”

Panama also lacks any bank reserve requirement rules or deposit insurance. Despite or, more likely, because of these factors, the World Economic Forum’s Global Competitiveness Report ranks Panama seventh in the world for the soundness of its banks.

I don’t think I have anything to add…

SNL reported yesterday that Germany’s laws seem to make the issuance of contingent convertible bonds (CoCos) almost pointless. This is a vivid reminder of my previous post, which highlighted some of the ‘good’ principles of financial regulation and which advocated stable, simple and clear rules, a position I have had since I’ve opened this blog. All authorities and regulators try to push banks (including German banks) to boost their capital level, which are deemed too low by international standards. CoCos, which are bonds that convert into equity if the bank’s regulatory capital ratio gets below a certain threshold, are a useful tool for banks (as it allows them to prevent shareholder dilution by issuing equity) and investors (whose demand is strong as those bonds pay higher coupon rates). Yet lawmakers, who love to bash banks for their low level of capitalisation, seem to be in no hurry to provide a clear framework that would allow to partially solve the very problems they point at in the first place… This is a very obvious example of regime uncertainty. As one lawyer declared:

One thing is clear: Nothing is clear

Bloomberg reports that FX traders are facing ‘extinction’ due to the switch to electronic trading. In fact, this has been ongoing for now several years, with asset classes moving one after another towards electronic platforms. Electronic trading now represents 66% of all FX transactions (vs. 20% in 2001). Traditional traders are going to become increasingly scarce and replaced by IT specialists that set and programme those machines. Overall, this should also mean less staff and a lower cost base for banks that are still plagued by too high cost/income ratios. Part of this shift is due to regulation, which makes it even more expensive to trade some of those products. This only reinforces my belief that regulation is historically one of the primary drivers of financial innovation, from money market funds to P2P lending…

The Financial Times on Bitcoin, P2P lending and secular stagnation

The FT has a few articles on some of my favourite topics today.

John Authers argue that it is time to take Bitcoin seriously. Who would say that I disagree? In his article he refers to several points I had already mentioned in some of my previous posts. He adds an interesting analogy with previous internet firms and concepts:

[…] even if Bitcoin is as successful as it is possible now to imagine, it looks overvalued at recent prices. It is in a bubble.

But this does not prove that the concept has no future. Shares in Amazon.com were also in a bubble in the late 1990s, and yet proved a great long-term investment after the bubble burst. Wild swings in value are typical when new technologies arrive.

A commenter also had a very good point, which highlighted Bitcoin’s (or other similar alternative digital currencies’) potential trade-boosting abilities:

Can you imagine a world where anyone can set up a shop on the internet and instantly accept payments from all over the world to sell its product or service without any intermediary? Well that’s only one face of what Bitcoin enables.

Naysayers will keep saying that Bitcoin is useless or only diverts wealth from ‘productive opportunities’ anyway.

FT Alphaville continued its long tradition of confused/confusing posts with this one on P2P lending today. I don’t know about you, but it does look to me that everything in the financial world that’s innovative and far from regulators’ grip is now under attack from Alphaville bloggers. They could have a point. But in this case, they don’t. They completely miss the point. The author misunderstands the financial crisis and draws the wrong conclusions from it.

According to the author, P2P is ‘pro-cyclical’ and has ‘no skin in the game’, which makes this asset class of systemic risk. He’d like to see P2P platforms to hold capital buffers to absorb losses. This makes no sense whatsoever. P2P is an investment. There are tons on possible investments. Anybody can invest directly in equities or bonds or FX or whatever, or through mutual funds/investment managers. P2P works the same way. Are we asking mutual funds to hold a capital buffer to absorb losses suffered by their clients’ portfolio? Of course not.

Banks need to retain capital as they hold deposits, which are part of the money supply and can be drawn down at any time by depositors, and also because they play a critical role in the payment system. If banks make losses on lending, capital allows them not to transfer the loss onto customers, who often just wanted to store their money there. This has absolutely nothing to do with the kind of voluntary investments I described above. Moreover, some P2P platforms have already set up loss-absorbing funds anyway… Platforms also have their ‘skin in the game’: if everybody stops lending through them, they don’t earn any revenue and go out of business. While I agree that platforms should not hide the fact that losses could occur on P2P investments, paternalism and regulation is the wrong way to go. Education and responsibility should be the goals.

In another Alphaville blog post, Izabella Kaminska reports the arguments of two economists against the Summers/Krugman secular stagnation story. And it basically reflects mine: it doesn’t exist. It also has a particular Austrian flavour: savings and productivity generate long-term economic growth, and low interest rates caused the economy to boom above potential (debt accumulation) and caused malinvestments (investments that generated short-term growth but that no one wanted in the end).

• There is no shortage of high return investment projects in the world. And the dearth of global corporate investment, which drove the great recession, means that productive potential is shrinking despite corporate profitability, leverage and cash balances being sound.

• The three ingredients for growth are a) a stable macro environment; b) a sound banking system; c) economic reforms that encourage entrepreneurship. What is missing right now is private sector confidence in the ability of governments and central bankers to provide all three.

• Credit bubbles can boost growth only temporarily and incur heavy costs in terms of subsequent deleveraging and misallocation of resources.

Hedge funds keep attracting new money (assets under management are up 16% since end-2012)… I won’t remind you that I’m wondering whether or not this is a sign that nominal interest rates are lower than their Wicksellian natural rates, forcing investors to take extra risk to achieve the real rates of return they would normally obtain from safer investments. But I guess that Summers and Krugman would say that, anyway, bubbles are necessary for the economy. Another side of the story is that not that many people seem to believe anymore in hedge funds outperforming the markets. Hedge funds seem to be transformed into mutual funds… But in this case, why paying such high management and performance fees? This doesn’t make so much sense.

Recent Comments