Cachanosky on the productivity norm, Hayek’s rule and NGDP targeting

Nicolas Cachanosky and I should get married (intellectually, don’t get overexcited). Some time ago, I wrote about his very interesting paper attempting to start the integration of finance and Austrian capital theories. A couple of weeks ago, I discovered another of his papers, published a year ago, but which I had completely missed (coincidentally, Ben Southwood also discovered that paper at the exact same time).

Titled Hayek’s Rule, NGDP Targeting, and the Productivity Norm: Theory and Application, this paper is an excellent summary of the policies named above and the theories underpinning them. It includes both theoretical and practical challenges to some of those theories. Cachanosky’s paper reflects pretty much exactly my views and deserved to be quoted at length.

Cachanosky defines the productivity norm as “the idea that the price level should be allowed to adjust inversely to changes in productivity. […] In other words, money supply should react to changes in money demand, not to changes in production efficiency.” Referring to the equation of exchange, he adds that “because a change in productivity is not in itself a sign of monetary disequilibrium, an increase in money supply to offset a fall in P moves the money market outside equilibrium and puts into motion an unnecessary and costly process of readjustment”, which is what current central bank policies of price level targeting do. The productivity norm allows mild secular deflation by not reacting to positive ‘real’ shocks.

He goes on to illustrate in what ways Hayek’s rule and NGDP targeting resemble and differ from the productivity norm:

There are instances where the productivity norm illuminated economists that talked about monetary policy. Two important instances are Hayek during his debate with Keynes on the Great Depression and the market monetarists in the context of the Great Recession. Both, Hayek and market monetarism are concerned with a policy that would keep monetary equilibrium and therefore macroeconomic stability. Hayek’s Rule and NGDP Targeting are the denominations that describe Hayek’s and market monetarism position respectively. Taking the presence of a central bank as a given, Hayek argues that a neutral monetary policy is one that keeps constant nominal income (MV) stable. Sumner argues instead that

“NGDP level targeting (along 5 percent trend growth rate) in the United States prior to 2008 would similarly have helped reduce the severity of the Great Recession.”

Hayek’s Rule of constant nominal income can be understood in total values or as per factor of production. In the former, Hayek’s Rule is a notable case of the productivity norm in which the quantity of factors of production is assumed to be constant. In the latter case, Hayek’s rule becomes the productivity norm. However, for NGDP Targeting to be interpreted as an application that does not deviate from the productivity norm, it should be understood as a target of total NGDP, with an assumption of a 5% increase in the factors of production. In terms of per factor of production, however, NGDP Targeting implies a deviation of 5% from equilibrium in the money market.

Cachanosky then highlights his main criticisms of NGDP targeting as a form of nominal income control, that is the distinction between NGDP as an ‘emergent order’ and NGDP as a ‘designed outcome’. He says that targeting NGDP itself rather than considering NGDP as an outcome of the market can affect the allocation of resources within the NGDP: “the injection point of an increase in money supply defines, at least in the short-run, the effects on relative prices and, as such, the inefficient reallocation of factors of production.” In short, he is referring to the so-called Cantillon effect, in which Scott Sumner does not believe. I am still wondering whether or not this effect could be sterilized (in a closed economy) simply by growing the money supply through injections of equal sums of money directly into everyone’s bank accounts.

To Cachanosky (and Salter), “NGDP level matters, but its composition matters as well.” He believes that targeting an NGDP growth level by itself confuses causes and effects: “that a sound and healthy economy yields a stable NGDP does not mean that to produce a stable NGDP necessary yields a sound and healthy economy.” He points out that the housing bubble is a signal of capital misallocation despite the fact that NGDP growth was pretty stable in pre-crisis years.

I evidently fully agree with him, and my own RWA-based ABCT also points to lending misallocation that would also occur and trigger a crisis despite aggregate lending growth remaining stable or ‘on track’ (whatever that means). I should also add that it is unclear what level of NGDP growth the central bank should target. See the following chart. I can identify many different NGDP growth ‘trends’ since the 1940s, including at least two during the ‘great moderation’. Fluctuations in the trend rate of US NGDP growth can reach several percentage points. What happens if the ‘natural’ NGDP growth changes in the matter of months whereas the central bank continues to target the previous ‘natural’ growth rate? Market monetarists could argue that the differential would remain small, leading to only minor distortions. Possibly, but I am not fully convinced. I also have other objections to NGDP level targeting (related to banking and transmission mechanism), but this post isn’t the right one to elaborate on this (don’t forget that I view NGDP targeting as a better monetary policy than inflation targeting but a ‘less ideal’ alternative to free banking or the productivity norm).

Cachanosky also points out that NGDP targeting policies using total output (Py in the equation of exchange) and total transactions (PT) do not lead to the same result. According to him “the housing bubble before 2008 crisis is an exemplary symptom os this problem, where PT increases faster than Py.”

Cachanosky also points out that NGDP targeting policies using total output (Py in the equation of exchange) and total transactions (PT) do not lead to the same result. According to him “the housing bubble before 2008 crisis is an exemplary symptom os this problem, where PT increases faster than Py.”

Finally, he reminds us that a 100%-reserve banking system would suffer from an inelastic money supply that could not adequately accommodate changes in the demand for money, leading to monetary equilibrium issues.

I can’t reproduce the whole paper here, but it is full of very interesting (though quite technical) details and I strongly encourage you to take a look.

In defence of the leverage ratio

Regular readers know that I blame risk-based capital requirements for many of the ills of our current banking system. Before the introduction of Basel regulations, banks’ capital level used to be assessed using more standard and simple leverage ratios (equity or capital/total assets). Those ratios have mostly disappeared since the end of the 1980s but Basel 3 is now re-introducing its own version (Tier 1 capital/total exposures).

While I believe there should not be any regulatory minimum capital requirement, I also do believe that, if regulators had to pick one main measure of capitalisation, it should be a standard leverage ratio. All RWA-based ratios should be scrapped.

A new study just added to the growing body of evidence that leverage ratios perform better than RWA-based ones as predictor of banks’ riskiness. Andrew Haldane, from the BoE, has been a long-time supporter of leverage ratios. Admati and Hellwig also backed non-risk weighted ratios. Another paper recently suggested that there was nothing in the literature that justified the level of risk-weights.

Still, most economists, central bankers and regulators consider leverage ratios as mere backstops to complement the more ‘scientific’ (read, more complex, as there is no science behind risk-weights) Basel RWA-based ratios. See this speech from Andreas Dombret, which sums up most criticisms towards simple leverage ratios:

Yet a leverage ratio would also create the wrong incentives. If banks had to hold the same percentage of capital against all assets, any institution wanting to maximise its profits would probably invest in high-risk assets, as they produce particularly high returns. This would eradicate the corrective influence of capital cover in reducing risk.

Unfortunately, Mr. Dombret and many others are very misinformed.

A leverage ratio would not incentivise banks to leverage up to the allowed limit. Under Basel’s RWA framework, no banks operated with the bare regulatory minimum. Critics forget that different banks have different risk aversion and different risk/reward profiles. Some banks generate relatively low RoEs in return for lower level of risk. Others are willing to take on more risks to generate higher margins and higher RoEs. Banks are not uniform.

Banks would not necessarily pile into the riskiest assets under a leverage ratio either. The answer to this is the same as above. Banks have different cultures and different risk/return profiles to offer to investors. There is no reason why all banks would suddenly lend to the riskiest borrowers to improve their earnings. Such criticism could also easily apply to Basel capital ratios: why didn’t all banks follow the same investment strategy? Critics forget that banks do not try to maximise their profits. They try to maximise their risk-adjusted profits. Finally, such argument only demonstrates its proponents’ ignorance of banking history, as if all banks had always been investing in the riskiest assets in the 300 years before Basel introduced those risk-weights.

RWA-based capital ratios are very patronising: because the riskiness of the assets is already embedded within the ratio, banks are effectively telling markets how risky they are. This became overly sarcastic with Basel 2, which allowed large banks to calculate their own risk-weights (i.e. the so-called ‘internal rating based’ method). It has been proved that, for a given portfolio of assets, risk-weights were considerably varying across banks (see here and here). Given the same balance sheet, one bank could, say, report a 10% Tier 1 ratio, and another one, 14%, implying massive variations in RWA density (RWAs/total assets). A given bank could also change its RWA calculation model (and hence its RWA density) in between two reporting periods, making a mockery of period to period comparison. Of course, all this is approved by regulators. Consequently RWA-based capital ratios became essentially meaningless.

As a result, a leverage ratio would provide a ‘purer’ measure of capitalisation that markets could then compare with their own assessment of banks’ balance sheet riskiness.

Scrapping RWA-based capital ratios would also provide major economic benefits. As regularly argued on this blog, RWA-incentivised regulatory arbitrage has been hugely damaging for the economy and is in large part responsible for the recent internationally-coordinated housing bubbles and ‘secular’ low level of business lending. Getting rid of such regulatory ratio would benefit us all by removing an indicator that has big distortionary effects on the economy.

Of course, there are still a few issues, though they remain relatively minor. The main one is that differences in accounting standards across jurisdictions do not lead to the same leverage ratios (i.e. US GAAP banks have much less restrictions to net their derivative positions than IFRS ones). But those accounting issues can easily be corrected if necessary for international comparison. The second one is what definition of capital to use: common equity? Tier 1 capital? Another problem is the fact that very low risk banks, which don’t need much capital, would also get penalised. In the end, it’s likely that any regulatory ratio will prove distortive in a way or another. Why not scrap them all and let the market do its job?

Chart: Guardian

Martin Wolf’s not so shocking shocks

Martin Wolf, FT’s chief economist, recently published a new book, The Shifts and the Shocks. The book reads like a massive Financial Times article. The style is quite ‘heavy’ and not always easy to read: Wolf throws at us numbers and numbers within sentences rather than displaying them in tables. This format is more adapted to newspaper articles.

Overall, it’s typical Martin Wolf, and FT readers surely already know most of the content of the book. I won’t come back to his economic policy advices here, as I wish to focus on a topic more adapted to my blog: his views on banking.

And unfortunately his arguments in this area are rather poor. And poorly researched.

Wolf is a fervent admirer of Hyman Minsky. As a result, he believes that the financial system is inherently unstable and that financial imbalances are endogenously generated. In Minsky’s opinion, crises happen. It’s just the way it is. There is no underlying factor/trigger. This belief is both cynical and wrong, as proved by the stability of both the numerous periods of free banking throughout history (see the track record here) and of the least regulated modern banking systems (which don’t even have lenders of last resort or deposit insurance). But it doesn’t fit Wolf’s story so let’s just forget about it: banking systems are unstable; it’s just the way it is.

Wolf identifies several points that led to the 2000s banking failure. In particular, liberalisation stands out (as you would have guessed) as the main culprit. According to him “by the 1980s and 1990s, a veritable bonfire of regulations was under way, along with a general culture of laissez-faire.” What’s interesting is that Wolf never ever bothers actually providing any evidence of his claims throughout the book (which is surprising given the number of figures included in the 350+ pages). What/how many regulations were scrapped and where? He merely repeats the convenient myth that the banking system was liberalised since the 1980s. We know this is wrong as, while high profile and almost useless rules like Glass-Steagall or the prohibition of interest payment on demand deposits were repealed in the US, the whole banking sector has been re-regulated since Basel 1 by numerous much more subtle and insidious rules, which now govern most banking activities. On a net basis, banking has been more regulated since the 1980s. But it doesn’t fit Wolf’s story so let’s just forget about it: banking systems were liberalised; it’s just the way it is.

Financial innovation was also to blame. Nevermind that those innovations, among them shadow banking, mostly arose from or grew because of Basel incentives. Basel rules provided lower risk-weight on securitized products, helping banks improve their return on regulatory capital. But it doesn’t fit Wolf’s story so let’s just forget about it: greedy bankers always come up with innovations; it’s just the way it is.

The worst is: Wolf does come close to understanding the issue. He rightly blames Basel risk-weights for underweighting sovereign debt. He also rightly blames banks’ risk management models (which are based on Basel guidance and validated by regulators). Still, he never makes the link between real estate booms throughout the world and low RE lending/RE securitized risk-weights (and US housing agencies)*. Housing booms happened as a consequence of inequality and savings gluts; it’s just the way it is.

All this leads Wolf to attack the new classical assumptions of efficient (and self-correcting) markets and rational expectations. While he may have a point, the reasoning that led to this conclusion couldn’t be further from the truth: markets have never been free in the pre-crisis era. Rational expectations indeed deserve to be questioned, but in no way does this cast doubt on the free market dynamic price-researching process. He also rightly criticises inflation targeting, but his remedy, higher inflation targets and government deficits financed through money printing, entirely miss the point.

What are Wolf other solutions? He first discusses alternative economic theoretical frameworks. He discusses the view of Austrians and agrees with them about banking but dismisses them outright as ‘liquidationists’ (the usual straw man argument being something like ‘look what happened when Hoover’s Treasury Secretary Mellon recommended liquidations during the Depression: a catastrophe’; sorry Martin, but Hoover never implemented Mellon’s measures…). He also only relies on a certain Rothbardian view of the Austrian tradition and quotes Jesus Huerta de Soto. It would have been interesting to discuss other Austrian schools of thought and writers, such as Selgin, White and Horwitz, who have an entirely different perception of what to do during a crisis. But he probably has never heard of them. He once again completely misunderstands Austrian arguments when he wonders how business people could so easily be misled by wrong monetary policy (and he, incredibly, believes this questions the very Austrian belief in laissez-faire), and when he cannot see that Austrians’ goals is to prevent the boom phase of the cycle, not ‘liquidate’ once the bust strikes…

Unsurprisingly, post-Keynesian Minsky is his school of choice. But he also partly endorses Modern Monetary Theory, and in particular its banking view:

banks do not lend out their reserves at the central bank. Banks create loans on their own, as already explained above. They do not need reserves to do so and, indeed, in most periods, their holdings of reserves are negligible.

I have already written at length why this view (the ‘endogenous money’ theory) is inaccurate (see here, here, here, here and here).

He then takes on finance and banking reform. He doubts of the effectiveness of Basel 3 (which he judges ‘astonishingly complex’) and macro-prudential measures, and I won’t disagree with him. But what he proposes is unclear. He seems to endorse a form of 100% reserve banking (the so-called Chicago Plan). As I have written on this blog before, I am really unsure that such form of banking, which cannot respond to fluctuations in the demand for money and potentially create monetary disequilibrium, would work well. Alternatively, he suggests almost getting rid of risk-weighted assets and hybrid capital instruments (he doesn’t understand their use… shareholder dilution anyone?) and force banks to build thicker equity buffers and report a simple leverage ratio. He dismisses the fact that higher capital requirements would impact economic activity by saying:

Nobody knows whether higher equity would mean a (or even any) significant loss of economic opportunities, though lobbyists for banks suggest that much higher equity ratios would mean the end of our economy. This is widely exaggerated. After all, banks are for the most part not funding new business activities, but rather the purchase of existing assets. The economic value of that is open to question.

Apart from the fact that he exaggerates banking lobbyists’ claims to in turn accuse them of… exaggerating, he here again demonstrates his ignorance of banking history. Before Basel rules, banks’ lending flows were mostly oriented towards productive commercial activities (strikingly, real estate lending only represented 3 to 8% of US banks’ balance sheets before the Great Depression). ‘Unproductive’ real estate lending only took over after the Basel ruleset was passed.

The case for higher capital requirements is not very convincing and primarily depends on the way rules are enforced. Moreover, there is too much focus on ‘equity’. Wolf got part of his inspiration from Admati and Hellwig’s book, The Bankers’ New Clothes. But after a rather awkward exchange I had with Admati on Twitter, I question their actual understanding of bank accounting:

While his discussion of the Eurozone problems is quite interesting, his description of the Eurozone crisis still partly rests on false assumptions about the banking system. Unfortunately, it is sad to see that an experienced economist such as Martin Wolf can write a whole book attacking a straw man.

* In a rather comical moment, Wolf finds ‘unconvincing’ that US government housing policy could seriously inflate a housing bubble. To justify his opinion, he quotes three US Republican politicians who said that this view “largely ignores the credit bubble beyond housing. Credit spreads declined not just for housing, but also for other asset classes like commercial real estate.” Let’s just not tell them that ‘Real Estate’ comprises both residential housing and CRE…

ECB policies: from flop to flop… to flop?

Even central bankers seem to be acknowledging that their measures aren’t necessarily effective…

ECB’s Benoit Coeuré made some interesting comments on negative deposit rates in a speech early September. Surprisingly, he and I agree on several points he makes on the mechanics of negative rates (he and I usually have opposite views). Which is odd. Given the very cautious tone of his speech, why is he even supporting ECB policies?

Here is Coeuré:

Will the transmission of lower short-term rates to a lower cost of credit for the real economy be as smooth? While bank lending rates have come down in the past in line with lower policy rates, there is a limit to how cheap bank lending can be. The mark-up that banks add to the cost of obtaining funding from the central bank compensates for credit risk, term premia and the cost of originating, screening and monitoring loans. The need for such compensation does not necessarily fall when policy rates are lowered. If anything, a central bank lowers rates when the economy needs stimulus, which is precisely when it is difficult for banks to find good loan making opportunities. It remains to be seen whether and to what extent the recent monetary policy accommodation translates into cheaper bank lending.

This is a point I’ve made many times when referring to margin compression: banks are limited in their ability to lower the interest rate they charge customers as, absent any other revenue sources, their net interest income necessarily need to cover their operating costs (at least; as in reality it needs to be higher to cover their cost of capital in the long run). Banks’ only solution to lower rates is to charge customers more for complimentary products (it has been reported that this is in effect what has been happening in the US recently).

Negative rates are similar to a tax on excess reserves, which evidently doesn’t make it easier for a bank to improve its profitability, and as a result its internal capital generation. And Coeuré agrees:

A negative deposit rate can, however, also have adverse consequences. For a start, it imposes a cost on banks with excess reserves and could therefore reduce their profitability. Note, however, that this applies to any reduction of the deposit rate and not just to those that make the rate negative. For sure, lower bank profitability could hamper economic recovery, especially in times when banks have to deleverage owning to stricter regulation and enhanced market scrutiny. But whether bank profitability really falls when policy rates are lowered depends more generally on the slope of the yield curve (as banks’ funding costs may also fall), on banks’ investment policies (as there is scope for them to diversify their cash investment both along the curve and across the credit universe) and on factors driving non-interest income.

Coeuré clearly understands the issue: central banks are making it difficult for banks to grow their capital base, while regulators (often the same central bankers) are asking banks to improve their capitalisation as fast as possible. Still, he supports the policy…

Other regulators are aware of the problem, and not all are happy about it… Andrew Bailey, from the Bank of England’s PRA, said last week that regulatory agencies should co-ordinate:

I am trying to build capital in firms, and it is draining out down the other side.

This says it all.

Meanwhile, and as I expected, the ECB’s TLTRO is unlikely to have much effect on the Eurozone economy… Banks only took up EUR83m of TLTRO money, much below what the central bank expected. It is also likely that a large share of this take up will only be used for temporary liquidity purposes, or even for temporary profitability boosting effects (through the carry trade, by purchasing capital requirement-free sovereign debt), until banks have to pay it off after two years (as required by the ECB, and without penalty, if they don’t lend the money to businesses).

Fitch also commented negatively on TLTRO, with an unsurprising title: “TLTROs Unlikely to Kick-Start Lending in Southern Europe”.

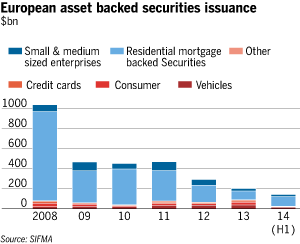

Finally, the ECB also announced its intention to purchase asset-backed securities (which effectively represents a version of QE). While we don’t know the details yet, the scheme has fundamentally a higher probability to have an effect on banks’ behaviour. There is a catch though: ABS issuance volume has been more than subdued in Europe since the crisis struck (see chart below, from the FT). The ECB might struggle to buy the quantity of assets it wishes. Perhaps this is why central bankers started to encourage European banks to issue such structured products, just a few years after blaming banks for using such products.

Oh, actually, there is another catch. ABSs are usually designed in tranches. Equity and mezzanine tranches absorb losses first and are more lowly rated than senior tranches, which usually benefit from a high rating. Consequently, equity and mezzanine tranches are capital intensive (their regulatory risk-weight is higher), whereas senior tranches aren’t. To help banks consolidate their regulatory capital ratios and prevent them from deleveraging, the ECB needs to buy the riskier tranches. But political constraints may prevent it to do so… Will this new ECB scheme also fail? As long as central bankers (and politicians) continue to push for schemes and policies without properly understanding their effects on banks’ internal ‘mechanics’, they will be doomed to fail.

PS: I have been busy recently so few updates. I have a number of posts in the pipeline… I just need to find the time to write them!

Breaking banks won’t help economic recovery

In contrast with the bank-bashing environment of the post-crisis period, voices are increasingly being raised to moderate regulatory, political and judiciary risks on the banking system.

Last week, Gillian Tett wrote an article in the FT tittled “Regulatory revenge risks scaring investors away”. She says:

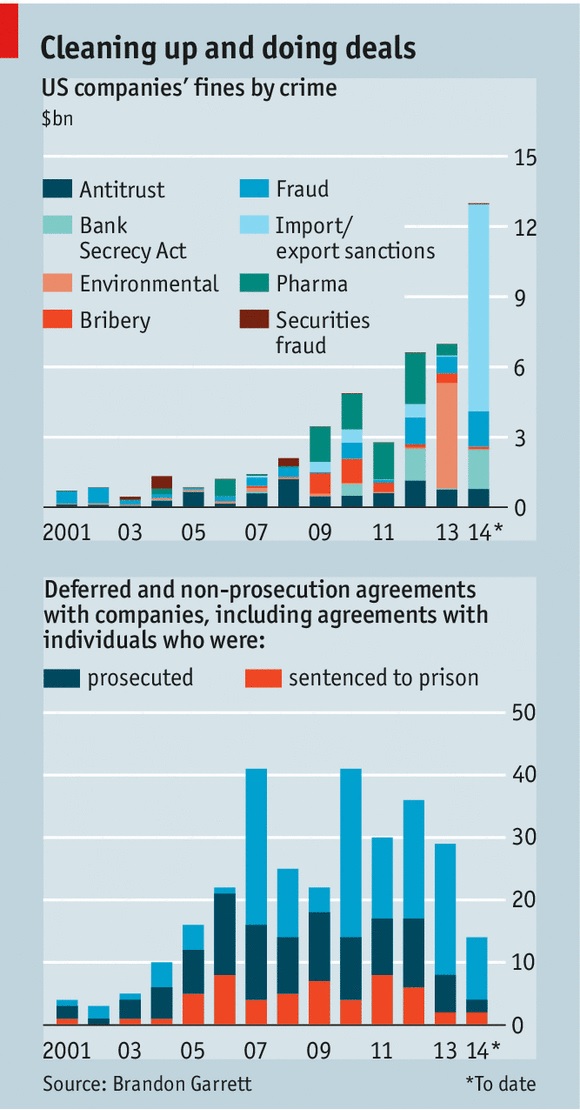

Last month [Roger McCornick’s] project team published its second report on post-crisis penalties, which showed that by late 2013 the top 10 banks had paid an astonishing £100bn in fines since 2008, for misbehaviour such as money laundering, rate-rigging, sanctions-busting and mis-selling subprime mortgages and bonds during the credit bubble. Bank of America headed this league of shame: it had paid £39bn by the end of 2013 for its transgressions. When the 2014 data are compiled, the total penalties will probably have risen towards £200bn.

She argues that “legal risk is now replacing credit risk.” This is a key issue. Banks have already been hit hard by new regulatory requirements, which sometimes require a fundamental restructuring of their business model. The consequences of this framework shift is that profitability, and hence internal capital generation, remain subdued, weakening the system as a whole. Banks now reporting double digit RoEs are more the exceptions than the rule. Moreover, low profitability also reduces the banks’ ability to generate capital externally (i.e. capital raising) because they do not cover their cost of capital. This scares investors away, as they have access to better risk-adjusted investment opportunities elsewhere.

The enormous amounts raised through litigation procedures make such a situation even worse. Admittedly, banks that purposely bypassed laws or committed frauds should be punished. But, as The Economist argues this week in a series of articles called “The criminalisation of American business” (see follow-up article here), the “legal system has become an extortion racket”, whose “most destructive part of it all is the secrecy and opacity” as “the public never finds out the full facts of the case” and “since the cases never go to court, precedent is not established, so it is unclear what exactly is illegal”:

This undermines the predictability and clarity that serve as the foundations for the rule of law, and risks the prospect of a selective—and potentially corrupt—system of justice in which everybody is guilty of something and punishment is determined by political deals. America can hardly tut-tut at the way China’s justice system applies the law to companies in such an arbitrary manner when at times it seems almost as bad itself.

Estimates of capital shortfall at European banks vary between EUR84bn and as much as EUR300bn (another firm, PwC, estimates the shortfall at EUR280bn). Compare those amounts with the hundreds of billions Euros paid or about to be paid by banks as litigation settlements, and it is no surprise that banks have to deleverage to comply with regulatory capital ratio deadlines and upcoming stress tests… Such high amounts, if justified, could probably have been raised by prosecutors at a slower pace in the post-crisis period without endangering the economic recovery (banks’ balance sheets would have been more solid more quickly, which would have facilitated the lending channel of the monetary transmission mechanism).

In the end, regulatory regime uncertainty strikes banks twice: financial regulations keep changing (and new ones are designed), and opaque litigation risk is at an all-time high. Banks are now very risk-averse, depressing lending and international transactions. This seems to me to replicate some of the mistakes made by Roosevelt during the Great Depression. Despite all the central banks’ money injection programmes, this may not be the best way out of an economic crisis…

PS: Commenting on the forthcoming P2P lender Lending Club IPO, Matt Levine argues that:

But Lending Club can grow its balance sheet all it wants. Lending Club is not a bank. So it’s not subject to banking regulation, which means that it can do a core function of banking much more efficiently than an actual bank can.

He is (at least) partly right. By killing banks, regulatory constraints are likely to trigger the emergence of new types of lenders.

Wait… Isn’t it what’s already happened (MMF and other shadow banking entities…)?

New research at last asks the right questions on RWAs

A new piece of research by the US Treasury Department’s Office of Financial Research has started questioning the use and definitions of Basel regulations’ risk-weighted assets (RWAs), which they view as a “rather curious scheme”… RWAs are critical in the Basel framework as they have been underlying regulatory capital ratios since the introduction of Basel 1 back in 1988. Readers of this blog know that I blame RWAs for being a major factor in the economic distortions and resources misallocation that directly led to the crisis (reduction in business lending, jump in real estate lending, securitizations and sovereign lending…) (see also here… and everywhere on this blog).

The authors’ thesis is similar to mine (emphasis added):

This is a rather curious scheme, if we consider that risk is not ordinarily considered additive. One might construe the additive formulation as conservative, but capital requirements affect which assets a bank chooses to hold, so the choice of risk weights affects a bank’s asset mix and not just the overall risk of its portfolio. A risk-weighting scheme may be conservative in its effect on overall risk and yet introduce unintended distortions in the levels of different kinds of lending activities. […]

For our investigation, we take a risk-weighting scheme to have two primary interlinked objectives: to limit the overall risk in a bank portfolio and to do so without an unintended distortion of the mix of assets held by the bank. The first of these objectives is common to all capital regulation, but the second is specific to a risk-weighting scheme because risk weights implicitly assign prices (in terms of additional capital) to asset categories and thus inevitably create incentives for banks to choose some assets over others.

They add that the literature supporting the use (and validating the level) of risk-weights is rather thin, unlike the literature on the nature of banks’ capital (the so-called ‘Tiers’), which has been the focus of most new regulatory measures while RWAs have remained pretty much unchanged.

They propose to tie risk-weights to asset profitability and develop a mathematical framework to help regulators to do so (as they are unlikely to obtain enough information to accurately set their level). This is interesting, but I’d rather get rid of risk-weights altogether: market actors can already assess banks’ profitability vs. asset mix risk and invest accordingly. There is also another issue with such a scheme: assets that do not appear profitable (and hence risky) at first do not necessarily mean they are not, as secured real estate markets demonstrated over the last decade. Moreover, ‘riskier’ business lending rates are currently lower than ‘safer’ mortgage lending ones. Profitability of riskier assets is sometimes subdued, either for relationship purposes (in order to generate revenues elsewhere), and/or if lending terms/collateral nature/haircuts are deemed reasonable. I have to admit that I did not have the time to read their mathematical description in depth and I might be missing something.

Meanwhile, the BoE’s Funding for Lending Scheme still struggles to revive lending to UK businesses. As policy-makers are unlikely to read this blog, perhaps this new research will help?

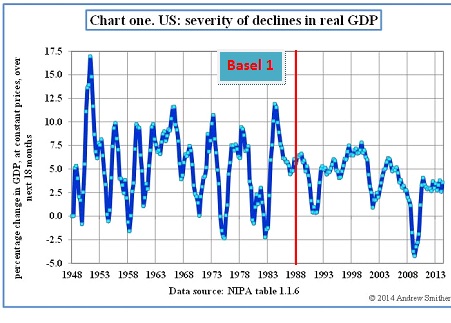

PS: I extracted the following chart from an FT blog post published yesterday and added Basel 1 to it (which introduced risk-weights and led to a decline in business lending). US real GDP growth seems to start declining exactly when business lending falls below trend (compare with second chart):

Raising capital requirements? Not that useful

The recent news of the near-bankruptcy of UK-based Cooperative Bank and Portugal-based Banco Espirito Santo made me question the utility of regulatory capital requirements. What are they for? Is raising them actually that useful? It looks to me that the current conventional view of minimum capital requirements is flawed.

In the pre-crisis era, banks were required to comply with a minimum Tier 1 capital ratio of 4% (i.e. Tier 1 capital/risk-weighted assets >= 4%). Most banks boasted ratios of 2 to 5 percentage points above that level. Basel 3 decided to increase the Tier 1 minimum to 6%, and banks are currently harshly judged if they do not maintain at least a 4% buffer above that level.

Indeed, given the possible sanctions arising from breaching those capital requirements, bankers usually thrive to maintain a healthy enough buffer above the required minimum. Sanctions for breaching those requirements include in most countries: revoking the banking licence, forcing the bank into a state of bankruptcy and/or forcing a restructuring/break-up/deleveraging of the balance sheet. Hence the question: what is the actual effective capital ratio of the banking system?

Companies – as well as banks in the past – are usually deemed insolvent (or bankrupt) once their equity reaches negative territory. At that point, selling all the assets of the company/bank would not generate enough money to pay off all creditors (while shareholders are wiped out).

Let’s assume a world with no Tier 1 capital but only straightforward equity, and without regulatory capital requirements. Following the basic rule outlined above, a bank with a 10% capital ratio can experience a 10% reduction in the value of its assets before it reaches insolvency. Let’s now introduce a minimum capital requirement of 6%. The same bank can now only experience a 4% reduction in the value of its assets before breaching the minimum and be considered good for resolving/restructuring/breaking-up by regulators.

For sure, higher minimum requirements have one advantage: depositors are less likely to experience losses. The larger the equity buffer, the stronger the protection.

However, there are also several significant disadvantages.

Given regulators’ current interpretation of the rules, higher minimum requirements also imply a higher sanction trigger. This creates a few problems:

- Raising the minimum threshold does little to protect taxpayers if regulators believe that a bank should be recapitalised, not when its Tier 1 gets close to or below 0%, but when it simply breaches the 6% level. In such case, it might have been possible for the bank’s capital buffer to absorb further losses without erasing its whole capital base and calling for help. For instance, Espirito Santo’s regulators said that its recapitalisation was compulsory: it reported a 5% equity Tier 1 ratio, below the 7% domestic minimum. And the state (i.e. taxpayers) obliged. But… It still had a 5% equity buffer to absorb further losses. Perhaps this would have been sufficient to absorb all losses and spare the taxpayers (perhaps not, but we may never find out).

- When approaching the minimum requirement, bankers are incentivised to start deleveraging in order to avoid breaching. Alternatively, they can be forced by regulators to do so. This has negative consequences on the availability of credit and on the money supply, possibly worsening a crisis through a debt deflation-type bust in order to comply with an artificially-defined 6% level.

- While depositors’ protection can be improved, it isn’t necessarily the case of other creditors, especially in light of the new bail-in rules that make them share the pain (so-called ‘burden-sharing’). Those rules kick in, not when the bank reaches a 0% capital ratio, but when it breaches the regulatory minimum (see here).

- Reaching the minimum requirement can also be self-defeating and self-fulfilling: fearing a bankruptcy event and the loss of their investments, shareholders run to the exit, pushing the share price down to zero and… effectively bringing about the insolvency of the bank. This doesn’t make much sense when a bank still has a 6% capital buffer. Espirito Santo suffered this fate until trading was suspended (see below).

So what’s the ‘effective’ Tier 1 capital ratio? Well, it is the spread between the reported Tier 1 and the minimum regulatory level. A bank that has an 8% Tier 1 under a 4% requirement, and a bank that has a 10% Tier 1 under a 6% requirement have virtually* the same effective capital ratio: 4%.

Regulatory insolvency events also cause operational problems. Espirito Santo was declared insolvent by its regulators but… not by the ISDA association! Setting regulatory minimums at 5% or 25% would have no impact on the issues listed above, as long as this logic is applied. To make regulatory requirements more effective, sanctions in case of breach should be minimal or non-existent in the short-term but should kick in in the long-term if banks’ capitalisation remains too low after a given period of time.

Regulatory minimums exemplify what Bagehot already tried to warn against already at his time: they are bound to create unnecessary panics. Speaking of liquidity reserves (the same reasoning as above applies), he said in Lombard Street:

[Minimums are bad] when legally and compulsorily imposed. In a sensitive state of the English money market the near approach to the legal limit of reserve would be a sure incentive to panic; if one-third were fixed by law, the moment the banks were close to one-third, alarm would begin, and would run like magic. And the fear would be worse because it would not be unfounded—at least, not wholly. If you say that the Bank shall always hold one-third of its liabilities as a reserve, you say in fact that this one-third shall always be useless, for out of it the Bank cannot make advances, cannot give extra help, cannot do what we have seen the holders of the ultimate reserve ought to do and must do.

* ‘virtually’ as, as described above, depositors protection is nonetheless enhanced, though even this is arguable given what happened in Cyprus

Sovereign debt crisis: another Basel creature?

I often refer to the distortive effects of RWA on the housing and business/SME lending channels. What I don’t say that often is that Basel’s regulations have also other distortive effects, perhaps slightly less obvious at first sight.

Basel is highly likely to be partially responsible for sovereign states’ over-indebtedness, by artificially maintaining interest rates paid by governments below their ‘natural’ level.

How? Through one particular mechanism historically, that you probably start knowing quite well: risk-weighted assets (RWA). Basel 1 indeed applied a 0% risk-weight on OECD countries’ sovereign debt*, meaning banks could load up their balance sheet with such instruments without negatively impacting their regulatory capital ratios at all. Interest income earned on sovereign debt was thus almost ‘free’: banks were incentivised to accumulate them to maximise capital-efficiency and RoE.

This extra demand is likely to have had the effect of pushing interest rates down for a number of countries, whose governments found it therefore much easier to fund their electoral promises. In the end, the financial and economic crisis was triggered by the over-issuance of very specific types of debt: housing/mortgage, sovereign and some structured products. All those asset classes had one thing in common: a preferential capital treatment under Basel’s banking regulations.

Basel 2 introduced some granularity but fundamentally didn’t change anything. Basel 3 doesn’t really help either, although local and Basel regulators have recently announced possible alterations to this latest set of rules in order to force banks to apply risk-weights to sovereign bonds (one option is to introduce a floor). Some banks have already implemented such changes (which cost billions in extra capital requirements).

While those measures go in the right direction, Basel 3 has also introduced a regulatory tool that goes precisely the opposite way: the liquidity coverage ratio (LCR). The LCR requires banks to maintain a large enough liquidity buffer (made of highly-liquid and high quality assets) to cover a 30-day cash outflow. As you may have already guessed, eligible assets include mostly… government securities**.

Here again, Basel artificially elevates the demand for sovereign debt in order to comply with regulatory requirements, pushing yields down in the process. This has two consequences: 1. governments could find a lot easier to raise cash than in free market conditions (with all the perverse incentives this has on a democratic process unconstrained by economic reality) and 2. as sovereign yields are used as risk-free rate benchmarks in the valuation of all other asset classes, the fall in yield due to the artificially-increased demand could well play the role of a mini-QE, boosting asset prices across the board ceteris paribus.

We end up with a policy mix that contaminates both central banks’ monetary policies and domestic political debates. But, worst of all, it is a real malinvestment engine, which trades short-term financial solidity for long-term instability.

* Some non-OECD regions of the world also allow their domestic banks to use 0% risk-weight on domestic sovereign debt. For instance, many African countries are allowed to apply 0% weighing on the sovereign debt of their local governments despite the obvious credit risk it represents as well as its poor marketability (this is partly mitigated as this debt is often repoable at the regional central bank). Moreover, the same regulators prevent their domestic banks from investing their liquidity in Treasuries or European debt, with the obvious goal of benefiting those African states. Consequently, illiquid and risky sovereign bonds comprise most of those banks’ “liquidity” buffers, evidently not making those banking systems much safer…

** The LCR is partly responsible for the ‘shortage of safe assets’ story.

Vince Cable realises too late what banking regulation involves

Back from holidays, and a lot of things to cover…

Let’s start with Vince Cable, Britain’s Secretary of State for Business, who is making a U-turn, though not yet quite finished, as he progressively realises how much he ignored about the pernicious effects of banking regulation.

The way the regulatory system operates has undoubtedly had a suffocating effect on business lending and particularly on our exporters.

Not surprisingly, the result is that banks pump out lending in the mortgage market, while lending to small businesses is restricted. This directly stems from the rules on which the regulatory model is based and has had a very damaging impact.

You may well recognise that he is referring to risk-weighted assets (RWAs), which have been a recurrent theme of this blog (and the focus of my three latest posts). Vince Cable had already sparked controversy pretty much exactly a year ago, when he first attacked the BoE for being a ‘capital Taliban’:

One of the anxieties in the business community is that the so called ‘capital Taliban’ in the Bank of England are imposing restrictions which at this delicate stage of recovery actually make it more difficult for companies to operate and expand.

This is a welcome reaction by one of the country’s top politician. However, let’s go back a few years to find the same Mr Cable vehemently supporting the exact same reforms he now criticises, while fully rejecting bankers’ claims that increased capital requirements would allocate funding away from SMEs (see here, here, here, here and here):

Banks and industry groups have argued more regulation could force institutions to curb lending to small- and medium-sized businesses at a time when the economy is slowing.

Prediction which turned out to be correct.

Mr Cable’s went from blaming banks for the crisis and justifying stronger regulatory requirements to blaming those same requirements for the weak level of business lending in the UK. Unfortunately, his U-turn isn’t fully completed and Mr Cable attacks the wrong target. Capital requirements are defined in Basel, the Swiss city. And he supported them in the first place, without evidently knowing what those rules involved. He also seemingly showed a poor understanding of banking history as his support for banking insulation through ring-fencing demonstrated (though most regulators are to blame as well).

Better late than never? Perhaps, but probably too late to have any effect going forward… Politicians’ and regulators’ rush to design banking rules in order to please the public opinion is making everyone worse off in the end.

Photo: Rex Features

Basel vs. ECB’s TLTRO: The fight

(and vs. BoE’s FLS)

Following my previous post on the mechanics of ECB negative deposit rates, I wanted to back my claims about the likely poor effect of the central bank TLTRO measure on lending.

I argued that despite the cheap funds provided by the ECB to lend to corporate clients (particularly SMEs), Basel’s risk-weighted assets would stand in the way of the scheme as they keep distorting banks’ lending incentives (same is true regarding the BoE and the second version of its Funding for Lending Scheme).

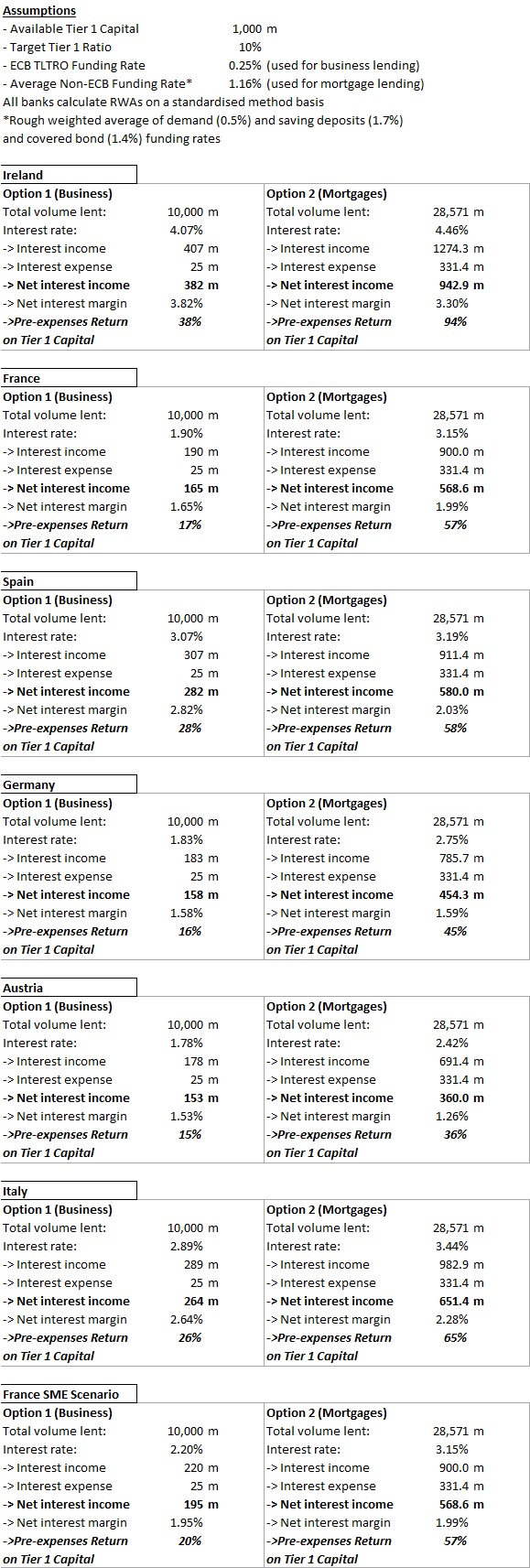

I extracted all the most recent new business and mortgage lending rates from the central banks’ websites of several European countries. Unfortunately, business lending rates are most of the time aggregates of rates charged to large multinational companies, SMEs, and micro-enterprises. Only the Banque of France seemed to provide a breakdown. So most business lending rates below are slightly skewed downward (but not by much as you can see with the French case).

Using this dataset, I built a similar scenario to the one I described in my first RWAs and malinvestments post (as it turned out, I massively overestimated business lending rates in that post…). I wanted to find out what would be the most profitable option for a bank: business lending or mortgage lending, given RWA and capital constraints (banks target a 10% regulatory Tier 1 capital ratio). The results speak for themselves:

Despite the cheap ECB loans, and given a fixed amount of capital, banks are way more profitable raising funding from traditional sources to lend to households for house purchase purposes…

Admittedly, the exercise isn’t perfect. But the difference in net interest income and return on capital is so huge that tweaking it a little wouldn’t change much the results:

- I assume that all business lending is weighted 100%. In reality, apart from the French SME scenario, large corporates (often rated by rating agencies) benefit from lower RWA-density under a standardised method. This would actually raise the profitability of business lending through higher volume (and increased leverage), though not by much. Mortgages are weighted at 35% under that method.

- I assume that all banks use the standardised method to calculate RWAs. In reality, only small and medium-sized banks do. Large banks use the ‘internal rating based’ method, which allows them to risk-weight customers following their own internal models. Here again, most corporates can benefit from lower RWAs. But mortgages also do (RWA-density often decreases to the 10-15% range).

- Cross-selling is often higher with corporates, which desire to hedge and insure their financial or non-financial business positions. Corporates also use banks’ international payment solutions. This adds to revenues.

- Business lending is often less cost-intensive than retail lending. Retail lending indeed traditionally requires a large branch network, which is less the case when dealing with corporates (often grouped within regional corporate centres, though not always for tiny enterprises). However, retail banking is progressively moving online, providing opportunities to banks to cut costs and improve their profitability.

- The lower RWA-density on mortgages allows banks to increase lending volume and leverage. However, this also requires higher funding volumes. In turn, this should increase the rate paid on the marginal increase in funding, raising interest expense somewhat in the case of mortgages.

In the end, even if the adjustments described above reduce the profitability spread by 10 percentage points, the conclusion stands: banks are hugely incentivised to avoid business lending, facilitating misallocation of capital on a massive scale, in particular in a period of raising capital requirements… Moreover, banks also benefit from favourable RWAs for securitised products based on mortgages (CMBS, RMBS…), compounding the effects.

To tell you the truth, I wasn’t expecting such frightening results when I started writing that post… Please someone tell me that I made a mistake somewhere…

Central banks, regulators and politicians will find it hard to prop up business lending with regulations designed to prevent it.

Recent Comments