New research at last asks the right questions on RWAs

A new piece of research by the US Treasury Department’s Office of Financial Research has started questioning the use and definitions of Basel regulations’ risk-weighted assets (RWAs), which they view as a “rather curious scheme”… RWAs are critical in the Basel framework as they have been underlying regulatory capital ratios since the introduction of Basel 1 back in 1988. Readers of this blog know that I blame RWAs for being a major factor in the economic distortions and resources misallocation that directly led to the crisis (reduction in business lending, jump in real estate lending, securitizations and sovereign lending…) (see also here… and everywhere on this blog).

The authors’ thesis is similar to mine (emphasis added):

This is a rather curious scheme, if we consider that risk is not ordinarily considered additive. One might construe the additive formulation as conservative, but capital requirements affect which assets a bank chooses to hold, so the choice of risk weights affects a bank’s asset mix and not just the overall risk of its portfolio. A risk-weighting scheme may be conservative in its effect on overall risk and yet introduce unintended distortions in the levels of different kinds of lending activities. […]

For our investigation, we take a risk-weighting scheme to have two primary interlinked objectives: to limit the overall risk in a bank portfolio and to do so without an unintended distortion of the mix of assets held by the bank. The first of these objectives is common to all capital regulation, but the second is specific to a risk-weighting scheme because risk weights implicitly assign prices (in terms of additional capital) to asset categories and thus inevitably create incentives for banks to choose some assets over others.

They add that the literature supporting the use (and validating the level) of risk-weights is rather thin, unlike the literature on the nature of banks’ capital (the so-called ‘Tiers’), which has been the focus of most new regulatory measures while RWAs have remained pretty much unchanged.

They propose to tie risk-weights to asset profitability and develop a mathematical framework to help regulators to do so (as they are unlikely to obtain enough information to accurately set their level). This is interesting, but I’d rather get rid of risk-weights altogether: market actors can already assess banks’ profitability vs. asset mix risk and invest accordingly. There is also another issue with such a scheme: assets that do not appear profitable (and hence risky) at first do not necessarily mean they are not, as secured real estate markets demonstrated over the last decade. Moreover, ‘riskier’ business lending rates are currently lower than ‘safer’ mortgage lending ones. Profitability of riskier assets is sometimes subdued, either for relationship purposes (in order to generate revenues elsewhere), and/or if lending terms/collateral nature/haircuts are deemed reasonable. I have to admit that I did not have the time to read their mathematical description in depth and I might be missing something.

Meanwhile, the BoE’s Funding for Lending Scheme still struggles to revive lending to UK businesses. As policy-makers are unlikely to read this blog, perhaps this new research will help?

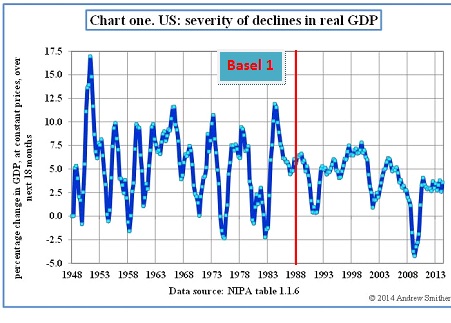

PS: I extracted the following chart from an FT blog post published yesterday and added Basel 1 to it (which introduced risk-weights and led to a decline in business lending). US real GDP growth seems to start declining exactly when business lending falls below trend (compare with second chart):

4 responses to “New research at last asks the right questions on RWAs”

Trackbacks / Pingbacks

- - 23 September, 2014

- - 21 November, 2014

Leave a comment

Recent Comments

| pslebow on ‘Sovereign money’:… | |

| pslebow on A critique of Werner’s view on… | |

| Hugo Kramer on Welcome to Spontaneous Fi… | |

| Nathan on A critique of Werner’s view on… | |

| Nathan on More, more, more money endogen… |

Awesome post! Made me think of a few things, would love to hear your thoughts:

1) Probably the lowest RWA loan asset – besides buying sovereign debt – is margin lending which you can do at a 0 RWA (or formerly 10% under Basel I). However most margin lending has been limited to broker-dealers (i.e. prime brokerage done out of a broker-dealer entity) which don’t have access to deposit funding and lend on an overnight basis. Do you have any thoughts on why there was never an explosion of margin loans done out of banks, for term, against big stock positions over the past 15 years? Would have definitely heard about a lot of these in the crisis if big positions got blown out.

2) From 50,000 feet in the air, do you think that the introduction of high leverage ratios, which will often be binding and probably force banks to do ROE analysis at the margin, will “fix” this issue of loan asset selection driven by capital treatment?

1) It does look to me that there was a boom in margin loans:

http://seekingalpha.com/article/50635-margin-debt-grows-risk-grows-too

There have been massive margin calls during the crisis and some financial institutions suffered because of that (I think it was a reason behind AIG’s collapse, if I remember correctly).

2) The leverage ratio won’t solve the problem entirely but will effectively introduce a ceiling. I know some mortgage banks with close to 30% Tier 1 ratio that have big issues with their leverage.